Hybrid and Electric Vehicles the Electric Drive Delivers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SAIC MOTOR CORPORATION LIMITED Annual Report 2016

SAIC MOTOR ANNUAL REPORT 2016 Company Code:600104 Abbreviation of Company: SAIC SAIC MOTOR CORPORATION LIMITED Annual Report 2016 Important Note 1. Board of directors (the "Board"), board of supervisors, directors, supervisors and senior management of the Company certify that this report does not contain any false or misleading statements or material omissions and are jointly and severally liable for the authenticity, accuracy and integrity of the content. 2. All directors attended Board meetings. 3. Deloitte Touche Tohmatsu Certified Public Accountants LLP issued standard unqualified audit report for the Company. 4. Mr. Chen Hong, Chairman of the Board, Mr. Wei Yong, the chief financial officer, and Ms. Gu Xiao Qiong. Head of Accounting Department, certify the authenticity, accuracy and integrity of the financial statements contained in the annual report of the current year. 5. Plan of profit distribution or capital reserve capitalization approved by the Board The Company plans to distribute cash dividends of RMB 16.50 (inclusive of tax) per 10 shares, amounting to RMB 19,277,711,252.25 in total based on total shares of 11,683,461,365. The Company has no plan of capitalization of capital reserve this year. The cash dividend distribution for the recent three years accumulates to RMB48,605,718,485.39 in total (including the year of 2016). 6. Risk statement of forward-looking description √Applicable □N/A The forward-looking description on future plan and development strategy in this report does not constitute substantive commitment to investors. Please note the investment risk. 7. Does the situation exist where the controlling shareholders and their related parties occupy the funds of the Company for non-operational use? No. -

Competing in the Global Truck Industry Emerging Markets Spotlight

KPMG INTERNATIONAL Competing in the Global Truck Industry Emerging Markets Spotlight Challenges and future winning strategies September 2011 kpmg.com ii | Competing in the Global Truck Industry – Emerging Markets Spotlight Acknowledgements We would like to express our special thanks to the Institut für Automobilwirtschaft (Institute for Automotive Research) under the lead of Prof. Dr. Willi Diez for its longstanding cooperation and valuable contribution to this study. Prof. Dr. Willi Diez Director Institut für Automobilwirtschaft (IfA) [Institute for Automotive Research] [email protected] www.ifa-info.de We would also like to thank deeply the following senior executives who participated in in-depth interviews to provide further insight: (Listed alphabetically by organization name) Shen Yang Senior Director of Strategy and Development Beiqi Foton Motor Co., Ltd. (China) Andreas Renschler Member of the Board and Head of Daimler Trucks Division Daimler AG (Germany) Ashot Aroutunyan Director of Marketing and Advertising KAMAZ OAO (Russia) Prof. Dr.-Ing. Heinz Junker Chairman of the Management Board MAHLE Group (Germany) Dee Kapur President of the Truck Group Navistar International Corporation (USA) Jack Allen President of the North American Truck Group Navistar International Corporation (USA) George Kapitelli Vice President SAIC GM Wuling Automobile Co., Ltd. (SGMW) (China) Ravi Pisharody President (Commercial Vehicle Business Unit) Tata Motors Ltd. (India) © 2011 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. All rights reserved. Competing in the Global Truck Industry – Emerging Markets Spotlight | iii Editorial Commercial vehicle sales are spurred by far exceeded the most optimistic on by economic growth going in hand expectations – how can we foresee the with the rising demand for the transport potentials and importance of issues of goods. -

Presentation to Repsol

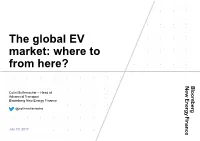

The global EV market: where to from here? Colin McKerracher – Head of Advanced Transport Bloomberg New Energy Finance @colinmckerrache July 10, 2017 Analysis to help you understand the future of energy Solar Wind Power and Gas Carbon Energy Smart Storage Electric Mobility and Frontier Emerging Utilities Markets & Technologies Vehicles Autonomous Power Technologies Climate Driving Americas Europe, Middle East Asia Pacific & Africa 1 July 10, 2017 Global EV sales by region 2011-2017e, thousand units YoY growth +69% +40% +56% +55% +47% Thousand units 1,200 We expect passenger EV 1,018 1,000 sales to be just over 1m in 46 2017 800 218 695 21 600 158 283 448 23 400 209 288 32 115 206 29 200 122 27 116 182 435 96 36 283 30 96 56 66 114 0 2012 2013 2014 2015 2016 2017 China Europe US Japan Canada South Korea RoW Note: Includes highway-capable PHEV and BEV passenger vehicles only; RoW is “Rest of World” 2 July 10, 2017 Countries where EVs were above 1% of total passenger vehicle sales Bloomberg New Energy Finance, Marklines 3 July 10, 2017 BEV model availability, 2008-20 Jaguar Tesla VW I.D.* Land Rover Toyota Trumpchi VW I.D. CROZZ Defender RAV4 GS4 I-Pace pickup* Mitsubishi eX BMW i5 Volvo 40.2* SUVs/Trucks Tesla Tesla M-B EQ VW Model Y* Model X Chehejia Audi E-tron Budd-e M-B B-Class BYD e6 NIO ES8* SUV* Quattro Porsche E-sport Renault DeZir Qianto Q50 Venturi Fetish Tesla Roadster Tesla Model S Sports cars Tesla Roadster* M-B SLS eDrive Hyundai Ioniq Aston Martin GLM G4 NIO ES9 Audi R8 E-tron Exagon Furtive Mahindra eVerito RapidE Geely Emgrand NIO EVE ChangAn SAIC E-Lavida Tesla Model 3 LeEco LeSEE Eado Mullen 700e Lucid Air Sedans CODA EV Audi E-tron Faraday Honda Clarity BAIC EU260 Sportback JAC iEV4 Renault Fluence BYD e5 FF91 Kia Ray Hyundai BMW i3 M-B E-Cell BlueOn VW e-Golf Chevy Bolt VW I.D. -

Global Monthly Is Property of John Doe Total Toyota Brand

A publication from April 2012 Volume 01 | Issue 02 global europe.autonews.com/globalmonthly monthly Your source for everything automotive. China beckons an industry answers— How foreign brands are shifting strategies to cash in on the world’s biggest auto market © 2012 Crain Communications Inc. All rights reserved. March 2012 A publication from Defeatglobal spurs monthly dAtA Toyota’s global Volume 01 | Issue 01 design boss Will Zoe spark WESTERN EUROPE SALES BY MODEL, 9 MONTHSRenault-Nissan’sbrought to you courtesy of EV push? www.jato.com February 9 months 9 months Unit Percent 9 months 9 months Unit Percent 2011 2010 change change 2011 2010 change change European sales Scenic/Grand Scenic ......... 116,475 137,093 –20,618 –15% A1 ................................. 73,394 6,307 +67,087 – Espace/Grand Espace ...... 12,656 12,340 +316 3% A3/S3/RS3 ..................... 107,684 135,284 –27,600 –20% data from JATO Koleos ........................... 11,474 9,386 +2,088 22% A4/S4/RS4 ..................... 120,301 133,366 –13,065 –10% Kangoo ......................... 24,693 27,159 –2,466 –9% A6/S6/RS6/Allroad ......... 56,012 51,950 +4,062 8% Trafic ............................. 8,142 7,057 +1,085 15% A7 ................................. 14,475 220 +14,255 – Other ............................ 592 1,075 –483 –45% A8/S8 ............................ 6,985 5,549 +1,436 26% Total Renault brand ........ 747,129 832,216 –85,087 –10% TT .................................. 14,401 13,435 +966 7% RENAULT ........................ 898,644 994,894 –96,250 –10% A5/S5/RS5 ..................... 54,387 59,925 –5,538 –9% RENAULT-NISSAN ............ 1,239,749 1,288,257 –48,508 –4% R8 ................................ -

Schriftliche Anfrage

Drucksache 18 / 17 933 Schriftliche Anfrage 18. Wahlperiode Schriftliche Anfrage des Abgeordneten Marcel Luthe (FDP) vom 13. Februar 2019 (Eingang beim Abgeordnetenhaus am 18. Februar 2019) zum Thema: Autos in Berlin III und Antwort vom 27. Februar 2019 (Eingang beim Abgeordnetenhaus am 01. März 2019) Die Drucksachen des Abgeordnetenhauses sind bei der Kulturbuch-Verlag GmbH zu beziehen. Hausanschrift: Sprosserweg 3, 12351 Berlin-Buckow · Postanschrift: Postfach 47 04 49, 12313 Berlin, Telefon: 6 61 84 84; Telefax: 6 61 78 28. Senatsverwaltung für Inneres und Sport Herrn Abgeordneten Marcel Luthe (FDP) über den Präsidenten des Abgeordnetenhauses von Berlin über Senatskanzlei - G Sen - Antwort auf die Schriftliche Anfrage Nr. 18/17 933 vom 13. Februar 2019 über Autos in Berlin III ----------------------------------------------------------------------------------------------------------------- Im Namen des Senats von Berlin beantworte ich Ihre Schriftliche Anfrage wie folgt: 1) Wie setzt sich der Fahrzeugbestand an in Berlin zugelassenen PKW nach Herstellern zum 01.01.2019 zusammen? Zu 1.: Zur Beantwortung der Frage 1 wird als Anlage eine Auswertung des Fahrzeugbestandes zum Stand 20. Februar 2019 übermittelt. Zahlen zum Fahrzeugbestand lassen sich nur tagesaktuell ermitteln, weshalb eine rückwirkende Auswertung (z.B. zum 01.01.2019) nicht möglich ist. 2) Wie viele Einsätze des Kriminaldauerdienstes hat es in den einzelnen Direktionen in den Jahren 2012 bis 2018 jeweils jährlich gegeben? 3) Wie viele dieser Einsätze erfolgten wegen Einbruchsdiebstählen -

Le Vehicule De Demain

L’avenir de l’automobile « Transports et nouvelles mobilités, nouveaux usages » Joel Danroc H2 La voiture du futur - Les évolutions de l’automobile Billions 400World Energy Needs 350 - Pourquoi ne peut on pas continuer ainsi? Les stratégies 300 250 200 150 Fossil Energies 100 50 -La voiture électrique à batterie et à pile à Hydrogène 0 19002000 2100 2200 2300 - Les nouveaux modèles de mobilité - mais que fait le CEA ? La recherche, les démonstrateurs et les transferts de technologie L’avant pétrole : une courte période 1899 : « Voitures électrique » « Jamais contente » +100Km/h 1896 Invention « Tricycle Benz » - moteurs électriques, 67 CV - batteries Fulmen, Moteur gaz - Carroserie aluminium + Hybrides Porsche ! Après 1900 « Ere Pétrole » Endormissement de l‟électrique « On n’invente pas le téléphone à partir des pigeons voyageurs ! » Michelin « Le passage de la calèche à l’automobile actuelle » Une rupture technologique majeure Voitures Rencontre Pétrole/Moteur combustion interne Pétrole L‟histoire de l‟automobile ponctuée par quelques éléments marquants dans les domaines «sociétal, économique, technique» Succès de l‟automobile : « Quatre roues, un volant, du plaisir et du rêve » 1974 Premier Choc pétrolier 1990 Début de l‟expériences hors pétrole ( Voiture électrique, PAC …) 2012 : 80 millions de voitures produites par an La Chine est le premier marché mondial Arrivée des générations Y connectées! « RETOUR VERS LE FUTUR » 1900 : tout avait été imaginé du point de vue mécanique ! 1950 / 1960 on se « reprojette » sur : - de nouvelles -

25Th International Colloquim of Gerpisa Revolutions New

25th International Colloquim of Gerpisa Revolutions New Technologies and services in the automotive industry 14-16 june 2017 ENS Cachan, Paris. Electric vehicle platform strategies by Chinese automakers: what's going on on EV arena in China? Sergio Muñiz & Bruce Belzowski Electric Vehicle Platform Strategies by Chinese Automakers: What’s Going On EV Arena In China? Presentation for the 25th Gerpisa International Colloquium 2017 - Paris (Cachan): R/Evolutions. New technologies and services in the automotive industry BRUCE M. BELZOWSKI SERGIO TADEU GONÇALVES MUNIZ CAMILLE CU Belzowski, Bruce; Muniz, Sergio; Cu, Camille. - Electric Vehicle Platform Strategies by Chinese Automakers: What’s Going On EV Arena In China? THE AUTHORS: Bruce M. Belzowski Managing Director of University of Michigan Transportation Research Institute (UMTRI) Automotive Futures Group. Sergio Tadeu Gonçalves Muniz Associate Professor - Federal University of Technology - Paraná (UTFPR), Brazil and was visiting researcher at University of Michigan Transportation Research Institute (UMTRI), Automotive Futures Group. Camille Cu Undergraduate Student at University of Michigan. UMTRI Automotive Futures Assistant in Research. Belzowski, Bruce; Muniz, Sergio; Cu, Camille. - Electric Vehicle Platform Strategies by Chinese Automakers: What’s Going On EV Arena In China? Chinese market In the EV market, more than 95% of the market are dominated by domestic brands: the price and government subsidies are crucial. China electric vehicle industry: 200+ carmakers, with currently about 4,000 new energy vehicle (NEV) models in development. China became the world’s leading automotive market in 2009. China surpassed the U.S. in 2015 to become the world’s biggest market for New Energy Vehicles (NEVs): comprising PHEVs, BEVs, FCEVs Great Potential: in United States: 0.8 vehicles/resident; in China: 0.1 vehicles/resident. -

Final Report

25 June 2015 Final Report Assessment of the normative and policy framework governing the Chinese economy and its impact on international competition For: AEGIS EUROPE Brussels Belgium THINK!DESK China Research & Consulting Prof. Dr. Markus Taube & Dr. Christian Schmidkonz GbR Merzstrasse 18 81679 München Tel.: +49 - (0)89 - 26 21 27 82 [email protected] www.thinkdesk.de 1 This report has been prepared by: Prof. Dr. Markus Taube Peter Thomas in der Heiden 2 Contents Executive Summary ························································································· 11 1. Introduction ······························································································ 27 Part I: The Management of the Chinese Economy: Institutional Set-up and Policy Instruments 2. Centralised Planning and Market Forces in the Chinese Economy ··················· 32 2.1 The Role of Planning in the Chinese Economy ············································ 32 2.1.1 Types of Plans ··············································································· 32 2.1.2 Plans and Complementary Documents················································ 41 2.2 Dedicated Government Programmes for Industry Guidance ··························· 45 2.2.1 Subsidies – An Overview ································································· 45 2.2.1.1 Examples for Preferential Policies and Grant Giving Operations by Local Governments ································································ 51 2.2.1.2 Recent Initiatives by the Central Government -

Rapport : Des Technologies Compétitives Au Service Du

CAS n° 51 > 472 pages. Dos : 27.5 mm. Sans innovation technologique, il sera impossible de relever les défi s économiques, sociaux et environne- mentaux que soulève notre engagement en faveur du développement durable. La mission de prospective pré- sidée par Jean Bergougnoux s’efforce ici de recenser les progrès susceptibles d’intervenir à horizon 2030 et 18, rue de Martignac 2050 dans trois domaines clés : l’énergie, le bâtiment 2012 no51 75700 Paris Cedex 07 et le transport. Pour chaque technologie examinée, on Tél. 01 42 75 60 00 tente d’apprécier sa contribution potentielle au déve- www.strategie.gouv.fr loppement durable et les conditions de son intégration dans les systèmes existants (ou à créer). Quels sec- teurs verront se produire des sauts technologiques ? Des technologies compétitives Quel est le degré de maturité technique, économique et au service du développement durable sociale de ces avancées ? Enfi n, quels sont les atouts de notre pays sur la scène internationale ? Car cette revue des technologies porteuses d’avenir n’oublie pas que la maîtrise de l’innovation est aussi un élément déterminant de la compétitivité. Dans un contexte de contrainte budgétaire et de forte concurrence mondiale, les pouvoirs publics se doivent d’adapter leur soutien aux fi lières innovantes à l’état de la technologie et aux perspectives de développement. Développement durable Rapport de la mission présidée par -:HSMBLA=U^V\]^: Jean Bergougnoux Diffusion Direction de l’information légale et administrative Imprimé en France au service compétitives -

China Autos Asia China Automobiles & Components

Deutsche Bank Markets Research Industry Date 18 May 2016 China Autos Asia China Automobiles & Components Vincent Ha, CFA Fei Sun, CFA Research Analyst Research Analyst (+852 ) 2203 6247 (+852 ) 2203 6130 [email protected] [email protected] F.I.T.T. for investors What you should know about China's new energy vehicle (NEV) market Many players, but only a few are making meaningful earnings contributions One can question China’s target to put 5m New Energy Vehicles on the road by 2020, or its ambition to prove itself a technology leader in the field, but the surge in demand with 171k vehicles sold in 4Q15 cannot be denied. Policy imperatives and government support could ensure three-fold volume growth by 2020, which would make China half of this developing global market. New entrants are proliferating, with few clear winners as yet, but we conclude that Yutong and BYD have the scale of NEV sales today to support Buy ratings. ________________________________________________________________________________________________________________ Deutsche Bank AG/Hong Kong Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016. Deutsche Bank Markets Research Asia Industry Date China 18 May 2016 Automobiles & China -

2016 Annual Report.Pdf

International Energy Agency Implementing Agreement for Co-operation on Hybrid and Electric Vehicle Technologies and Programmes From 2016 on renamed to Technology Collaboration Programme on Hybrid and Electric Vehicles (HEV TCP) Hybrid and Electric Vehicles The Electric Drive Commutes June 2016 www.ieahev.org IA-HEV, formally known as the Implementing Agreement for Co-operation on Hybrid and Electric Vehicle Technologies and Programmes, functions within a framework created by the International Energy Agency (IEA). Views, findings, and publications of IA-HEV do not necessarily represent the views or policies of the IEA Secretariat or of all its individual member countries. From 2016 on the IA-HEV has been renamed to Technology Collaboration Programme on Hybrid and Electric Vehicles (HEV TCP). Cover Photo: Volvo electric bus. The bus is running on route 55 in Gothenburg (Sweden) as part of the ElectriCity collaboration. Further information about ElectriCity can be obtained over www.goteborgelectricity.se. (Image courtesy of Volvo Buses) The Electric Drive Commutes Cover Designer: Anita Theel, VDI/VDE Innovation + Technik GmbH ii International Energy Agency Implementing Agreement for Co-operation on Hybrid and Electric Vehicle Technologies and Programmes* Annual Report Prepared by the Executive Committee and Task 1 over the Year 2015 Hybrid and Electric Vehicles The Electric Drive Commutes Editor: Gereon Meyer (Operating Agent Task 1, VDI/VDE Innovation + Technik GmbH) Co-editors: Jadranka Dokic, Heike Jürgens, Diana M. Tobias (VDI/VDE Innovation + Technik GmbH) Contributing Authors: Markku Antikainen Tekes Finland James Barnes Barnes Tech Advising United States Martin Beermann Joanneum Research Austria Graham Brennan SEAI Ireland Carol Burelle Natural Resources Canada Canada Pierpaolo Cazzola IEA France Mario Conte ENEA Italy Cristina Corchero IREC Spain Andreas Dorda A3PS Austria Julie Francis Allegheny Science & Technology United States Marine Gorner IEA France Halil S. -

Pdf/Asian Highwaynetwork.Pdf (Дата Доступа: 15.01.2018)

1 МИНИСТЕРСТВОНАУКИ И ВЫСШЕГО ОБРАЗОВАНИЯ РОССИЙСКОЙ ФЕДЕРАЦИИ Федеральное государственное бюджетное учреждение науки Институт Дальнего Востока Российской академии наук На правах рукописи ЧЭНЬ СЯО АВТОМОБИЛЬНЫЙ ТРАНСПОРТ КНР: ОТРАСЛЕВОЙ И РЕГИО- НАЛЬНЫЙ АСПЕКТ Специальность 08.00.14 – Мировая экономика Диссертация на соискание ученой степени кандидата экономических наук Научный руководитель кандидат экономических наук Сазонов Сергей Леонидович Москва – 2019 2 ОГЛАВЛЕНИЕ ВВЕДЕНИЕ…………………………………………………………………………..3 ГЛАВА 1. АВТОМОБИЛЬНЫЙ ТРАНСПОРТ КНР…………………………….17 1.1 Современное состояние автомобильной промышленности Китая………….17 1.2 Развитие национальной сети автомобильных магистралей…………………41 ГЛАВА 2. ИННОВАЦИОННОЕ РАЗВИТИЕ КИТАЙСКОГО АВТОПРОМА ..63 2.1 Технологический прорыв в производстве автомобилей, использующих альтернативные источники энергии………………………………………………63 2.2 Развитие технологий производства аккумуляторов и инфраструктуры запра- вочных станций для электромобилей………………………………………..……94 2.3 Пути решения проблем автомобильного транспорта в крупнейших мегапо- лисах Китая………………………………………………………………………..109 ГЛАВА 3. МЕСТО И РОЛЬ АВТОМОБИЛЬНОГО ТРАНСПОРТА КНР В РЕ- АЛИЗАЦИИ ПЛАНОВ СТРОИТЕЛЬСТВА «ЭКОНОМИЧЕСКОГО ПОЯСА ШЕЛКОВОГО ПУТИ» И «МОРСКОГО ШЕЛКОВОГО ПУТИ XXI В.»…………………………………………………………………………………..127 3.1 Инициатива «одного пояса и одного пути» как важнейший фактор стимули- рования экономического развития Китая и сопредельных стран……………………………………………………………………………..…127 3.2 Автомобильный транспорт в реализации инициативы «одного пояса и одно-