Investment Checklist

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CBI South East Regional Council Directory of Members

CBI South East Regional Council Directory of members South East Delivering prosperity through private-sector growth Getting Britain building Creating a global role for Britain in a new Europe Encouraging high-growth export champions Delivering for consumers and communities CBI South East Regional Council: Directory of members 3 Chairman’s message Having been an active member of the CBI SE These are all great foundations but to make real council for a number of years I am delighted to progress a great deal more building work needs to begin my two year term as the CBI South East be done. To achieve this we have set out our Regional Chairman, taking over the reins from workplan – our own growth agenda – for 2013, Debbie McGrath who I must congratulate and under the banner ‘Delivering prosperity through thank for doing such a fine job. private sector growth.’ The four central pillars will In addition to being an informal networking seek to: Get Britain Building; Create a global role opportunity and an unrivalled forum in which to for the UK; To encourage high-growth export share views on the current state of business and champions; and Deliver for consumers and trade, the Council above all, plays a vital role in communities. ensuring that the CBI’s national campaigns reflect These though will not be in isolation to the many the views of businesses in the region. I am looking other issues affecting business, so members will forward to working with so many experienced continue to contribute to discussions on, for business leaders and council members from a example, aviation, energy, business reputation diverse range of business and educational and of course the economic and business case establishments that singles out the South East relevant to the European referendum debate that and Thames Valley as unique and highly will gain momentum over the next two years. -

Restoring Strength, Building Value

Restoring Strength, Building Value QinetiQ Group plc Annual Report and Accounts 2011 Group overview Revenue by business The Group operates three divisions: US Services, 29% UK Services and Global Products; to ensure efficient 35% leverage of expertise, technology, customer relationships and business development skills. Our services businesses which account for more 36% than 70% of total sales, are focused on providing 2011 2010 expertise and knowledge in national markets. Our £m £m products business provides the platform to bring US Services 588.2 628.0 valuable intellectual property into the commercial UK Services 611.6 693.9 markets on a global basis. Global Products 502.8 303.5 Total 1,702.6 1,625.4 Division Revenue Employees US Services £588.2m 4,500 (2010: £628.0m) (2010: 5,369) Underlying operating profit* £44.3m (2010: £52.6m) Division Revenue Employees UK Services £611.6m 5,045 (2010: £693.9m) (2010: 5,707) Underlying operating profit* £48.7m (2010: £59.1m) Division Revenue Employees Global £502.8m 1,663 Products (2010: £303.5m) (2010: 2,002) Underlying operating profit* £52.4m (2010: £8.6m) * Definitions of underlying measures of performance are in the glossary on page 107. Underlying operang profit* by business Revenue by major customer type Revenue by geography 7% 17% 36% 31% 52% 37% 56% 31% 33% 2011 2010 2011 2010 2011 2010 £m £m £m £m £m £m US Services 44.3 52.6 US Government 894.3 754.1 North America 949.2 825.3 UK Services 48.7 59.1 UK Government 526.5 614.5 United Kingdom 623.7 720.0 Global Products 52.4 8.6 Other 281.8 -

Weekend News Summary

Weekend News Summary THE SUNDAY TIMES INDICES THIS MORNING Current (%) 1W% Change Profits go Sky high for Robey Warshaw partners: Three bankers at Value Change* Robey Warshaw have shared almost £50 million after advising on FTSE 100 7,502.3 2.0% 1.6% blockbuster takeovers. Profits at the boutique Mayfair firm more than DAX 30 13,351.0 0.5% 0.9% doubled to £48.4 million from £21.3 million in the year to the end of CAC 40 5,966.2 0.8% 0.8% March, accounts at Companies House show. DJIA** 28,135.4 - 0.4% Labour rout relieves investors in rail and utility providers: Industries S&P 500** 3,168.8 - 0.7% threatened with nationalisation by Labour rallied as the party’s NASDAQ Comp.** 8,734.9 - 0.9% resounding defeat erased the threat of cut-price state takeovers. Nikkei 225 23,952.4 -0.3% 2.9% Energy, water, rail and telecoms stocks including those of SSE, Severn Hang Seng 40 27,508.1 -0.6% 4.5% Trent, Go-Ahead and BT all posted strong gains as Executives and Shanghai Comp 2,984.4 0.6% 1.9% investors breathed a sigh of relief at the Conservative victory. Kospi 2,168.2 -0.1% 4.2% Minouche Shafik favourite as decision on Bank of England governor BSE Sensex 40,938.7 -0.2% 1.4% expected within days: A new Bank of England Governor is expected to S&P/ASX 200 6,849.7 1.6% 0.5% be named within days to succeed Mark Carney, who leaves at the end Current Values as at 11:15 BST, *%Chg from Friday Close, ** As on Friday Close of January. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

Chair's Introduction

Governance statement I have also met with a number of our major customers. I see it as an important part of the Chair’s role to have a strong relationship with key customers that complements the depth and breadth of the Group’s management relationships, through a programme of regular senior-level meetings. I intend to develop this role further, and am committed to supporting the continued improving momentum of dialogue with our primary customers. We have been pleased to welcome customers to participate in a number of contract reviews at the Board during the year. I have also enjoyed meeting many of Babcock’s shareholders to hear, directly from them, their views, concerns and Ruth Cairnie priorities. The Board and I are clear about Chair the importance of corporate governance and its role in the long-term success of the Group. Purpose and culture Chair’s introduction At the Board we recognise the essential role that a clear purpose and a strong corporate culture play in assuring the I am pleased to present my first Group’s long-term success. During the year the Board has worked to clarify Chair’s report on the work of the Babcock’s purpose, which we describe on Babcock Board. Since joining the page 10, and we expect to do more on Board in April last year, I have focused this over the coming year. This purpose is underpinned by the corporate culture, much time engaging with Babcock’s based on strong values that I found in stakeholders in order to get a real evidence across my induction visits. -

Defence Companies Anti-Corruption Index (DCI) 2019 Full List of Companies Included Part of the 2019 Assessment

Defence Companies Anti-Corruption Index (DCI) 2019 Full list of companies included part of the 2019 assessment: AAR Corporation General Dynamics Corporation Patria Oyj Abu Dhabi Shipbuilding General Electric Aviation Perspecta Accenture PLC GKN Aerospace Polish Defence Holdings AECOM Glock Poongsan Corporation PT Dirgantara Indonesia (Indonesian Aerojet Rocketdyne (formerly GenCorp) Hanwha Aerospace Aerospace) Airbus Group Harris Corporation QinetiQ Group PLC AirTanker Hewlett-Packard Enterprise Company Rafael Advanced Defense Systems Ltd Alion Science & Technology Corp High Precision Systems Raytheon Company Almaz-Antey Hindustan Aeronautics Limited Rheinmetall A.G. Arab Organisation for Industrialisation Honeywell International Rockwell Collins Inc. (AOI) Arsenal JSC Huntington Ingalls Industries Inc. Roketsan Aselsan A.S. Hyundai Rotem Company Rolls Royce PLC Austal IHI Corporation RTI Systems Aviation Industry Corporation of China IMI Systems Ltd RUAG Holding Ltd. (AVIC) Babcock International Group PLC Indian Ordnance Factories Russian Helicopters JSC BAE Systems PLC Indra Sistemas, S.A. Saab AB Ball Aerospace & Technologies Corp Israel Aerospace Industries Ltd Safran S.A. Battelle Memorial Institute Jacobs Engineering Science Applications Int. Corp. (SAIC) Bechtel Corporation Japan Marine United Corporation Serco Group PLC BelTechExport Company JSC Kawasaki Heavy Industries Ltd. ST Engineering STM Savunma Teknolojileri Muhendislik Bharat Dynamics KBR Inc. ve Ticaret A.S. King Abdullah II Design and Bharat Electronics Tactical Missiles Corporation, JSC Development Bureau Boeing Komatsu u Ltd. Turkish Aerospace Industries (TAI) Booz Allen Hamilton Inc. Kongsberg Gruppen ASA Tashkent Mechanical Plant CACI International Inc. Korea Aerospace Industries Tatra Trucks, A.S. CAE Inc. Krauss-Maffei Wegmann GmbH & Co. Teledyne Technologies Inc. CEA Technologies L-3 Communications Holdings Inc. Telephonics Corporation Chemring Group PLC Leidos Inc. -

FTSE Factsheet

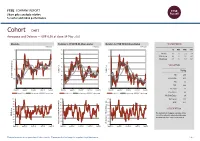

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Cohort CHRT Aerospace and Defense — GBP 6.56 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 7 115 105 1D WTD MTD YTD 110 Absolute 0.6 0.3 2.2 3.8 100 Rel.Sector -2.2 -1.3 -1.1 -0.1 105 Rel.Market -0.5 1.7 1.5 -5.0 6.5 100 95 VALUATION 95 6 90 90 Trailing Relative Price Relative Price Relative 85 85 PE 27.5 Absolute Price (local currency) (local Price Absolute 5.5 EV/EBITDA 13.9 80 80 PB 3.5 75 PCF 22.6 5 70 75 Div Yield 1.6 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales 2.0 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.4 100 90 90 Div Payout 43.4 90 80 80 ROE 13.1 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 The Company is the parent company of five 40 40 40 RSI RSI (Absolute) innovative, agile and responsive businesses 30 operating in defence and related markets. -

Premium Listed Companies Are Subject to the UK's Super-Equivalent Rules Which Are Higher Than the EU Minimum "Standard Listing" Requirements

List of Premium Equity Comercial Companies - 29th April 2020 Definition: Premium listed companies are subject to the UK's super-equivalent rules which are higher than the EU minimum "standard listing" requirements. Company Name Country of Inc. Description of Listed Security Listing Category Market Status Trading Venue Home Member State ISIN(S) 4IMPRINT GROUP PLC United Kingdom Ordinary Shares of 38 6/13p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB0006640972 888 Holdings Plc Gibraltar Ordinary Shares of 0.5p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GI000A0F6407 AA plc United Kingdom Ordinary Shares of 0.1p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BMSKPJ95 Admiral Group PLC United Kingdom Ordinary Shares of 0.1p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00B02J6398 AGGREKO PLC United Kingdom Ordinary Shares of 4 329/395p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BK1PTB77 AIB Group Plc Ireland Ordinary Shares of EUR0.625 each; fully paid Premium Equity Commercial Companies RM LSE Ireland IE00BF0L3536 Air Partner PLC United Kingdom Ordinary Shares of 1p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BD736828 Airtel Africa plc United Kingdom Ordinary Shares of USD0.50 each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BKDRYJ47 AJ Bell plc United Kingdom Ordinary Shares of GBP0.000125 each; fully paid Premium -

FTSE 350 Companies Audited by KPMG

FTSE 350 companies audited by KPMG KPMG LLP1 expects to issue an audit report for 67 FTSE 350 companies within the next 12 months Data as at 30 June 2021 Company FTSE Index2 Industry classification (ICB Supersector)2 3i Group Plc FTSE 100 Financial services Aggreko Plc FTSE 250 Industrial goods and services AO World Plc FTSE 250 Retail Ascential Plc FTSE 250 Technology Ashmore Group Plc FTSE 250 Financial services Auto Trader Group Plc FTSE 100 Technology AVI Global Trust plc FTSE 250 Financial services Avon Rubber Plc FTSE 250 Industrial goods and services B&M European Value Retail SA FTSE 100 Retail Baillie Gifford Japan Trust Plc FTSE 250 Financial services Baillie Gifford Shin Nippon FTSE 250 Financial services Baillie Gifford US Growth Trust FTSE 250 Financial services Balfour Beatty Plc FTSE 250 Consumer products and services Barclays Plc FTSE 100 Banks Berkeley Group Holdings (The) Plc FTSE 100 Consumer products and services Big Yellow Group plc FTSE 250 Real estate British American Tobacco Plc FTSE 100 Food, beverage and tobacco BT Group Plc FTSE 100 Telecommunications Capita Plc FTSE 250 Industrial goods and services Chemring Group Plc FTSE 250 Industrial goods and services Compass Group Plc FTSE 100 Consumer products and services Computacenter Plc FTSE 250 Technology Croda International Plc FTSE 100 Basic resources Entain Plc FTSE 100 Travel and leisure Experian Plc FTSE 100 Industrial goods and services Grainger Plc FTSE 250 Real estate HICL Infrastructure Plc FTSE 250 Financial services International Consolidated Airlines Group -

SAVANNAH Q2 2020 BOARD REVIEW an Analysis of the FTSE 100 & FTSE 250 Executive and Non-Executive Board Appointments in Q2 2020

www.savannah-group.com SAVANNAH Q2 2020 BOARD REVIEW An analysis of the FTSE 100 & FTSE 250 Executive and Non-Executive Board appointments in Q2 2020 INTRODUCTION I am pleased to present our analysis of the 2019 when 69% of the non-executive appointments appointments to the FTSE 100 and FTSE 250 boards to the FTSE 350 companies were female. We show in the second quarter of 2020. As usual, we report more detail on this later in the report. the appointments of executive and non-executive directors to the boards of the FTSE 100 and FTSE 250 At the time of writing this report, women are holding companies, identify the trends and the individuals 37% of the non-executive director roles on the FTSE concerned. 350 boards. If we include executive directors, that number falls sharply to 31% again demonstrating Readers will recall that our Q1 report coincided the “gender gap” at the executive director level that with the February release of the Parker Review we have highlighted in earlier reports. While there is Committee Update Report on the representation much work to be done in bringing more women into of ethnic minorities on the boards of the biggest the executive director ranks, it is worth reminding UK companies. In that context, we identified the ourselves that in 2010 women held less than 10% of Black, Asian & Minority Ethnic Minority (“BAME”) the FTSE 350 board seats (see Davies Review 2011). appointments for the first time. We do that again in this report and will continue to do so in future Moving away from diversity, in this report we also reports. -

Good Anti-Corruption Practices in Defence Companies

June 2013 Raising the bar Good anti-corruption practices in defence companies Part I: Seven practices that distinguish the best “Those defence companies that do take corruption risk seriously have the chance to be seen by their government clients as better companies with which to do business. As governments toughen their attitudes towards corruption, having a reputation for zero tolerance of corruption will be a distinguishing asset for a defence company.” The Rt Hon Lord Robertson of Port Ellen KT GCMG honFRSE PC, Former Secretary General of NATO June 2013 Raising the bar Good anti-corruption practices in defence companies Part I: Seven practices that distinguish the best 2 Executive Summary Executive Summary The Defence Companies Anti-Corruption These are demanding questions. This report Index (CI) was published on 4 October 2012. looks in some detail at each topic and gives This analysis, the first of its kind, provided examples. We think that companies scoring full comparative information on the disclosure and marks on these topics represent today’s good quality of anti-corruption systems in 129 major practice. defence companies. In Part II of this report—available as a Whilst the media focused primarily on the separate online document—we have extracted banding results, the analysis also contains 104 good practice examples in relation to all of many examples of good practice by defence the 34 questions in the Index. These examples companies. Our objective is to help raise are mostly in the public domain. However, there anti-corruption standards in the defence sector were also examples of good practice from the worldwide. -

General Assembly Divestment/ Proscription List

PRESBYTERIAN CHURCH (USA) 2020 General Assembly Divestment/ Proscription List Effective January 1, 2020 Committee on Mission Responsibility Through Investment (MRTI) Compassion, Peace and Justice Ministries Presbyterian Mission Agency Approved by MRTI on October 15, 2019 The General Assembly of the Presbyterian Church (USA) urges divestment and/or proscription of some corporations due to their involvement in military-related production (MR), tobacco (TO), human rights violations (HR), and operating for-profit prisons (FPP). The following is a comprehensive list of corporations or securities affected by those General Assembly policies, organized by policy screen. Top 5 Military-Related Ticker ISIN Industry 1 BAE Systems PLC BA/LN GB0002634946 MR 2 Boeing Company, The BA US0970231058 MR 3 Lockheed Martin Corporation LMT US5398301094 MR 4 Northrop Grumman Corporation NOC US6668071029 MR 5 Raytheon Company RTN US7551115071 MR Top 100 + 50 percent sales 1 Bharat Electronics Ltd. BEL.NS INE263A01024 MR 2 Cobham PLC COB GB00B07KD360 MR 3 Elbit Systems LTD ESLT IL0010811243 MR 4 Korea Aerospace Industries 047810 KR7047810007 MR 5 ManTech International Corporation MANT US5645631046 MR 6 Saab Ab SAABB SE0000112385 MR Weapons whose use can lead to mass or indiscriminate injury (Nuclear/Chemical/Biological) 1 Aerojet Rocketdyne Holdings, Inc. AJRD US0078001056 MR 2 Aryt Industries ARYT IL0005870147 MR 3 Babcock International Group PLC BAB GB0009697037 MR 4 CACI International Inc CACI US1271903049 MR 5 Chemring Group Plc CHG GB00B45C9X44 MR 6 Cohort plc CHRT.L GB00B0YD2B94 MR 7 Fortive Corporation FTV US34959J1088 MR 8 General Dynamics Corporation GD US3695501086 MR 9 Hanwha Techwin Co Ltd 012450 KR7012450003 MR 10 Huntington Ingalls Industries HII US4464131063 MR L3 Harris Technologies Inc.