CBI South East Regional Council Directory of Members

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investment Checklist

ukvalueinvestor.com UKValueInvestor High quality value investing for income & growth May 2012 Back in recession again Contents Although we’ve managed to avoid it for quite some time, the UK is back in recession. I don’t Market Overview think this is much of a surprise to most people; the UK economy has gone pretty much With the FTSE 100 at 5,700 the nowhere since the credit crunch started back in 2007/8. market is once again back in the ‘cheap’ range, with 7-year total As always though, it isn’t the end of the world just yet. The US is starting to show signs of returns expected to be around recovery and in the past most recessions ended when the US pulled us out. With any luck, 10% per annum. the same process will apply this time round. Model Portfolio Obviously most people would much prefer that we got back to growth sooner rather than Annual results are in from JD later, but from an investing point of view it shouldn’t matter too much one way or the other. Sports One of the basic assumptions of sound investing is that the future will always hold unpleasant Buy Alert surprises and that prudent and rational investors should be prepared for them at all times. A leading home shopping retailer This means sticking to the basics of being diversified, picking high quality companies, buying will be joining the portfolio. them when they are attractively valued and selling them when they’re not. FTSE 350 Sorted by Rating Find the top rated stocks in next New name, new rating system to no time. -

Restoring Strength, Building Value

Restoring Strength, Building Value QinetiQ Group plc Annual Report and Accounts 2011 Group overview Revenue by business The Group operates three divisions: US Services, 29% UK Services and Global Products; to ensure efficient 35% leverage of expertise, technology, customer relationships and business development skills. Our services businesses which account for more 36% than 70% of total sales, are focused on providing 2011 2010 expertise and knowledge in national markets. Our £m £m products business provides the platform to bring US Services 588.2 628.0 valuable intellectual property into the commercial UK Services 611.6 693.9 markets on a global basis. Global Products 502.8 303.5 Total 1,702.6 1,625.4 Division Revenue Employees US Services £588.2m 4,500 (2010: £628.0m) (2010: 5,369) Underlying operating profit* £44.3m (2010: £52.6m) Division Revenue Employees UK Services £611.6m 5,045 (2010: £693.9m) (2010: 5,707) Underlying operating profit* £48.7m (2010: £59.1m) Division Revenue Employees Global £502.8m 1,663 Products (2010: £303.5m) (2010: 2,002) Underlying operating profit* £52.4m (2010: £8.6m) * Definitions of underlying measures of performance are in the glossary on page 107. Underlying operang profit* by business Revenue by major customer type Revenue by geography 7% 17% 36% 31% 52% 37% 56% 31% 33% 2011 2010 2011 2010 2011 2010 £m £m £m £m £m £m US Services 44.3 52.6 US Government 894.3 754.1 North America 949.2 825.3 UK Services 48.7 59.1 UK Government 526.5 614.5 United Kingdom 623.7 720.0 Global Products 52.4 8.6 Other 281.8 -

Weekend News Summary

Weekend News Summary THE SUNDAY TIMES INDICES THIS MORNING Current (%) 1W% Change Profits go Sky high for Robey Warshaw partners: Three bankers at Value Change* Robey Warshaw have shared almost £50 million after advising on FTSE 100 7,502.3 2.0% 1.6% blockbuster takeovers. Profits at the boutique Mayfair firm more than DAX 30 13,351.0 0.5% 0.9% doubled to £48.4 million from £21.3 million in the year to the end of CAC 40 5,966.2 0.8% 0.8% March, accounts at Companies House show. DJIA** 28,135.4 - 0.4% Labour rout relieves investors in rail and utility providers: Industries S&P 500** 3,168.8 - 0.7% threatened with nationalisation by Labour rallied as the party’s NASDAQ Comp.** 8,734.9 - 0.9% resounding defeat erased the threat of cut-price state takeovers. Nikkei 225 23,952.4 -0.3% 2.9% Energy, water, rail and telecoms stocks including those of SSE, Severn Hang Seng 40 27,508.1 -0.6% 4.5% Trent, Go-Ahead and BT all posted strong gains as Executives and Shanghai Comp 2,984.4 0.6% 1.9% investors breathed a sigh of relief at the Conservative victory. Kospi 2,168.2 -0.1% 4.2% Minouche Shafik favourite as decision on Bank of England governor BSE Sensex 40,938.7 -0.2% 1.4% expected within days: A new Bank of England Governor is expected to S&P/ASX 200 6,849.7 1.6% 0.5% be named within days to succeed Mark Carney, who leaves at the end Current Values as at 11:15 BST, *%Chg from Friday Close, ** As on Friday Close of January. -

List of Shareholdings of the Linde Group

LINDE FINANCIAL REPORT 2014 [41] List of shareholdings of The The results of companies acquired in 2014 are included as of the date of acquisition. The information about the equity Linde Group and Linde AG at and the net income or net loss of the companies is as at 31 December 2014 in accordance 31 December 2014 and complies with International Financial with the provisions of § 313 (2) Reporting Standards, unless specifically disclosed below. No. 4 of the Ger man Commercial Code (HGB) 138 COMPANIES INCLUDED IN THE GROUP FINANCIAL STATEMENTS (IN ACCORDANCE WITH IFRS 10) Partici- Net Coun- pating Thereof income/ Registered office try interest Linde AG Equity net loss Note in percent in percent in € million in € million Gases Division EMEA AFROX – África Oxigénio, Limitada Luanda AGO 100 – 0.1 0.4 c, d LINDE GAS MIDDLE EAST LLC Abu Dhabi ARE 49 49 11.4 –1.7 f LINDE HEALTH CARE MIDDLE EAST LLC Abu Dhabi ARE 49 49 –1.1 –2.9 f LINDE HELIUM M E FZCO Jebel Ali ARE 100 3.4 0.2 ATION Linde Electronics GmbH Stadl- Paura AuT 100 10.8 2.1 ORM Linde Gas GmbH Stadl- Paura AuT 100 230.8 24.9 F 246 Bad Wimsbach- ER IN ER PROVISIS Gase & Service GmbH Neydharting AuT 100 0.5 0.1 H T O Chemogas N. V. Grimbergen BEL 100 8.0 2.5 Linde Gas Belgium NV Grimbergen BEL 100 1.2 0.8 Linde Homecare Belgium SPRL Scalyn BEL 100 100 4.0 0.0 Linde Gas Bulgaria EOOD Stara Zagora BGR 100 8.8 0.1 Linde Gas BH d. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

Mergers & Acquisitions in the US Industrial Gas Business

Mergers & Acquisitions in the US Industrial Gas Business PART II – THE MAJOR INDUSTRY SHAPERS By Peter V. Anania, Leaders LLC he Industrial Gas (IG) industry has seen tremendous growth a process to separate oxygen in 1880. In 1886 the brothers Brin started over the past 100 years, fueled by rapidly expanding technol- commercially developing the use of oxygen. T ogy in market leading countries that required more mixes of Interestingly, one of BOC’s first mergers — and now its last — was gases (including the exotics), purer gases for high-tech applications, with Linde. In 1906, Linde joined with Brin Oxygen by contributing as well as new applications of traditional gases. With the develop- its British Linde patents. These patents represented a new method for ment of industry in emerging economies, demand for industrial producing oxygen by cryogenic distillation of air. The resulting gases continues to grow worldwide. This is Part II of this series that merged entity was renamed British Oxygen Company or BOC. In the examines mergers and acquisitions activity in the industrial gas busi- 1920s, a process for the large-scale production of liquid oxygen ness. In this feature we look at some of the “majors” and how they allowed the oxygen to be delivered in liquid form by road tanker and have grown over the years through acquisitions. In compiling this greatly expanded its market applications. article, we researched the websites of many of the companies men- BOC’s growth in the first half of the 20th century was achieved tioned herein, had access to the archives of JR Campbell Associates, largely by developing or acquiring rights to new technology and Inc., along with discussions with Buzz Camp- processes, including further improvements in liq- bell, and used The History of Industrial Gases, uefaction and cryogenic cooling in the 1930s. -

Chair's Introduction

Governance statement I have also met with a number of our major customers. I see it as an important part of the Chair’s role to have a strong relationship with key customers that complements the depth and breadth of the Group’s management relationships, through a programme of regular senior-level meetings. I intend to develop this role further, and am committed to supporting the continued improving momentum of dialogue with our primary customers. We have been pleased to welcome customers to participate in a number of contract reviews at the Board during the year. I have also enjoyed meeting many of Babcock’s shareholders to hear, directly from them, their views, concerns and Ruth Cairnie priorities. The Board and I are clear about Chair the importance of corporate governance and its role in the long-term success of the Group. Purpose and culture Chair’s introduction At the Board we recognise the essential role that a clear purpose and a strong corporate culture play in assuring the I am pleased to present my first Group’s long-term success. During the year the Board has worked to clarify Chair’s report on the work of the Babcock’s purpose, which we describe on Babcock Board. Since joining the page 10, and we expect to do more on Board in April last year, I have focused this over the coming year. This purpose is underpinned by the corporate culture, much time engaging with Babcock’s based on strong values that I found in stakeholders in order to get a real evidence across my induction visits. -

Defence Companies Anti-Corruption Index (DCI) 2019 Full List of Companies Included Part of the 2019 Assessment

Defence Companies Anti-Corruption Index (DCI) 2019 Full list of companies included part of the 2019 assessment: AAR Corporation General Dynamics Corporation Patria Oyj Abu Dhabi Shipbuilding General Electric Aviation Perspecta Accenture PLC GKN Aerospace Polish Defence Holdings AECOM Glock Poongsan Corporation PT Dirgantara Indonesia (Indonesian Aerojet Rocketdyne (formerly GenCorp) Hanwha Aerospace Aerospace) Airbus Group Harris Corporation QinetiQ Group PLC AirTanker Hewlett-Packard Enterprise Company Rafael Advanced Defense Systems Ltd Alion Science & Technology Corp High Precision Systems Raytheon Company Almaz-Antey Hindustan Aeronautics Limited Rheinmetall A.G. Arab Organisation for Industrialisation Honeywell International Rockwell Collins Inc. (AOI) Arsenal JSC Huntington Ingalls Industries Inc. Roketsan Aselsan A.S. Hyundai Rotem Company Rolls Royce PLC Austal IHI Corporation RTI Systems Aviation Industry Corporation of China IMI Systems Ltd RUAG Holding Ltd. (AVIC) Babcock International Group PLC Indian Ordnance Factories Russian Helicopters JSC BAE Systems PLC Indra Sistemas, S.A. Saab AB Ball Aerospace & Technologies Corp Israel Aerospace Industries Ltd Safran S.A. Battelle Memorial Institute Jacobs Engineering Science Applications Int. Corp. (SAIC) Bechtel Corporation Japan Marine United Corporation Serco Group PLC BelTechExport Company JSC Kawasaki Heavy Industries Ltd. ST Engineering STM Savunma Teknolojileri Muhendislik Bharat Dynamics KBR Inc. ve Ticaret A.S. King Abdullah II Design and Bharat Electronics Tactical Missiles Corporation, JSC Development Bureau Boeing Komatsu u Ltd. Turkish Aerospace Industries (TAI) Booz Allen Hamilton Inc. Kongsberg Gruppen ASA Tashkent Mechanical Plant CACI International Inc. Korea Aerospace Industries Tatra Trucks, A.S. CAE Inc. Krauss-Maffei Wegmann GmbH & Co. Teledyne Technologies Inc. CEA Technologies L-3 Communications Holdings Inc. Telephonics Corporation Chemring Group PLC Leidos Inc. -

Further Records and Updates of Range Expansion in House Crow Corvus Splendens

Colin Ryall 39 Bull. B.O.C. 2016 136(1) Further records and updates of range expansion in House Crow Corvus splendens by Colin Ryall Received 31 May 2015 Summary.—House Crow Corvus splendens continues its ship-assisted global invasion, reaching locations further from its native range in the Indian Subcontinent. This report reviews the species’ recent spread as well as changes in the status of existing introduced populations where information is available. With the collapse of long-standing eradication programmes in Kenya and Tanzania, and a spread to inland sites in both countries, it is inevitable that House Crows will colonise the heart of Africa. In South and East Asia too, the species is spreading unobstructed through the region. Nevertheless, there is now a growing recognition of the threats of invasive alien species in general, including House Crow, and a willingness by some authorities and funding bodies to prevent the species’ proliferation. As a result, control programmes are now in operation at several locations where House Crows have established, and increasingly proactive approaches involving risk assessments, surveillance and action plans are being developed where a risk of invasion exists. Native to the Indian Subcontinent, southern Iran, Myanmar and western Yunnan (China), House Crow Corvus splendens has, over the past century or so, shown itself to be an invasive alien species (IAS) that is progressively spreading globally. Initially, the spread was mediated by deliberate releases in Aden (Yemen), Zanzibar and Klang (Malaysia) as of the late 1800s, for the purpose of dealing with refuse and crop pests. However, this was soon superseded by ship-assisted range expansion, at first within the Red Sea, Indian Ocean and its islands, probably via ships from Mumbai and Colombo, but also from ports including Aden and Suez, which possess large House Crow populations. -

FTSE Factsheet

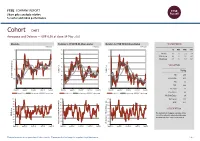

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Cohort CHRT Aerospace and Defense — GBP 6.56 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 7 115 105 1D WTD MTD YTD 110 Absolute 0.6 0.3 2.2 3.8 100 Rel.Sector -2.2 -1.3 -1.1 -0.1 105 Rel.Market -0.5 1.7 1.5 -5.0 6.5 100 95 VALUATION 95 6 90 90 Trailing Relative Price Relative Price Relative 85 85 PE 27.5 Absolute Price (local currency) (local Price Absolute 5.5 EV/EBITDA 13.9 80 80 PB 3.5 75 PCF 22.6 5 70 75 Div Yield 1.6 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales 2.0 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.4 100 90 90 Div Payout 43.4 90 80 80 ROE 13.1 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 The Company is the parent company of five 40 40 40 RSI RSI (Absolute) innovative, agile and responsive businesses 30 operating in defence and related markets. -

Shareholdings of Linde Aktiengesellschaft As of 31

GROUP FINANCIAL STATEMENTS NOTES TO THE GROUP FINANCIAL STATEMENTS OTHER INFORMATION [39] List of shareholdings of The results of companies acquired in 2017 are included as of the date of acquisition. The information about The Linde Group and Linde AG the equity and the net income or net loss of the com- at 31 December 2017 in panies is as at 31 December 2017 and complies with International Financial Reporting Standards, unless accordance with the provisions specifically disclosed below. of § 313 (2) of the German Commercial Code (HGB) COMPANIES INCLUDED IN THE GROUP FINANCIAL STATEMENTS (IN ACCORDANCE WITH IFRS 10) 132 Partici- pating Thereof Profit/loss Registered office Country interest Linde AG Equity for the year Note in percent in percent in EUR m in EUR m Gases Division EMEA AFROX – África Oxigénio, Limitada Luanda AGO 100 – – LINDE GAS MIDDLE EAST LLC Abu Dhabi ARE 49 49 2.1 –3.9 f LINDE HEALTHCARE MIDDLE EAST LLC Abu Dhabi ARE 49 49 –7.7 –1.3 f LINDE HELIUM M E FZCO Jebel Ali ARE 100 4.7 0.6 Linde Electronics GmbH Stadl-Paura AUT 100 11.4 1.5 Linde Gas GmbH Stadl-Paura AUT 100 297.2 21.6 Bad Wimsbach- PROVISIS Gase & Service GmbH Neydharting AUT 100 1.7 0.5 Linde Gas Belgium NV Grimbergen BEL 100 3.9 0.9 Linde Homecare Belgium SPRL Scladina BEL 100 100 3.7 0.5 Linde Gas Bulgaria EOOD Stara Zagora BGR 100 7.7 – 0.1 "Linde Gaz Bel" FLLC Telmy BLR 100 99 0.3 – 0.3 AFROX GAS & ENGINEERING SUPPLIES (BOTSWANA) (PTY) LIMITED Gaborone BWA 100 – – BOTSWANA OXYGEN COMPANY (PTY) LIMITED Gaborone BWA 100 – – BOTSWANA STEEL ENGINEERING (PTY) LIMITED Gaborone BWA 100 – – HANDIGAS (BOTSWANA) (PTY) LIMITED Gaborone BWA 100 – – HEAT GAS (PTY) LIMITED Gaborone BWA 100 – – KIDDO INVESTMENTS (PTY) LIMITED Gaborone BWA 100 – – PanGas AG Dagmersellen CHE 100 103.8 23.5 RDC GASES & WELDING (DRL) LIMITED Lubumbashi COD 100 0.8 – LINDE HADJIKYRIAKOS GAS LIMITED Nicosia CYP 51 51 10.6 1.7 Linde Gas a. -

Version Management

CORE Metadata, citation and similar papers at core.ac.uk Provided by Cranfield CERES Cranfield University - School of Management PhD submission 2005 – 6 Charles Stephens Enablers and inhibitors to horizontal collaboration between competitors: an investigation in UK retail supply chains Supervisor: Dr Paul Chapman © Cranfield University, 2006. All rights reserved. No part of this publication may be reproduced without the written permission of the copyright holder. Table of contents 1.1 Introduction........................................................................................1 1.2 Scoping the Research: The UK Food Retailing Market .....................7 1.2.2 A new paradigm: Co-operation between Competing Retailers .12 1.2.3 Efficient Consumer Response (ECR) .......................................13 1.3 Cross Chain Collaboration through Opportunity Technologies? ......17 1.3.1 The contribution of PD Contractors to ECR..............................19 1.3.2 Transaction Cost Economics....................................................22 1.3.3 Managed Primary Networks .....................................................27 1.4 Collaboration in Practice..................................................................33 1.5 Conclusion.......................................................................................39 2.1 Exploratory phase – UK Food Retailers...........................................45 2.2 Secondary Research .......................................................................48 2.2.1 Parity between Retailer