Tax Guide 2019 Experience an Easy Tax Return!

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tax Appeals Rules Procedures

Tax Appeals Tribunal Rules & Procedures The rules of the game February 2017 Glossary of terms KRA Kenya Revenue Authority TAT Tax Appeals Tribunal TATA Tax Appeals Tribunal Act TPA Tax Procedures Act VAT Value Added Tax 2 © Deloitte & Touche 2017 Definition of terms Tax decision means: a) An assessment; Tax law means: b) A determination of tax payable made to a a) The Tax Procedures Act; trustee-in-bankruptcy, receiver, or b) The Income Tax Act, Value Added liquidator; Tax Act, and Excise Duty Act; and c) A determination of the amount that a tax c) Any Regulations or other subsidiary representative, appointed person, legislation made under the Tax director or controlling member is liable Procedures Act or the Income Tax for under specified sections in the TPA; Act, Value Added Tax Act, and Excise d) A decision on an application by a Duty Act. taxpayer to amend their self-assessment return; Objection decision means: e) A refund decision; f) A decision requiring repayment of a The Commissioner’s decision either to refund; or allow an objection in whole or in part, or g) A demand for a penalty. disallow it. Appealable decision means: a) An objection decision; and b) Any other decision made under a tax law but excludes– • A tax decision; or • A decision made in the course of making a tax decision. 3 © Deloitte & Touche 2017 Pre-objection process; management of KRA Audit KRA Audit Notes The TPA allows the Commissioner to issue to • The KRA Audits are a tax payer a default assessment, amended undertaken by different assessment or an advance assessment departments of the KRA that (Section 29 to 31 TPA). -

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries Creating Incentives for Greener Products Policy Manual for Eastern Partnership Countries 2014 About the OECD The OECD is a unique forum where governments work together to address the economic, social and environmental challenges of globalisation. The OECD is also at the forefront of efforts to understand and to help governments respond to new developments and concerns, such as corporate governance, the information economy and the challenges of an ageing population. The Organisation provides a setting where governments can compare policy experiences, seek answers to common problems, identify good practice and work to co-ordinate domestic and international policies. The OECD member countries are: Australia, Austria, Belgium, Canada, Chile, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The European Union takes part in the work of the OECD. Since the 1990s, the OECD Task Force for the Implementation of the Environmental Action Programme (the EAP Task Force) has been supporting countries of Eastern Europe, Caucasus and Central Asia to reconcile their environment and economic goals. About the EaP GREEN programme The “Greening Economies in the European Union’s Eastern Neighbourhood” (EaP GREEN) programme aims to support the six Eastern Partnership countries to move towards green economy by decoupling economic growth from environmental degradation and resource depletion. The six EaP countries are: Armenia, Azerbaijan, Belarus, Georgia, Republic of Moldova and Ukraine. -

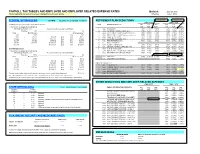

PAYROLL TAX TABLES and EMPLOYEE and EMPLOYER RELATED EXPENSE RATES Updated: June 27, 2012 *Items Highlighted in Yellow Have Been Changed Since the Last Update

PAYROLL TAX TABLES AND EMPLOYEE AND EMPLOYER RELATED EXPENSE RATES Updated: June 27, 2012 *items highlighted in yellow have been changed since the last update. Effective: July 1, 2012 FEDERAL WITHHOLDING 26 PAYS FEDERAL TAX ID NUMBER 86-6004791 RETIREMENT PLAN DEDUCTIONS 10.5% AT 50/50 10.5% AT 50/50 EMPLOYEE EMPLOYER (a) SINGLE person (including head of household) - CODE RETIREMENT PLAN DED OLD NEW DED OLD NEW If the amount of wages (after subtracting CODE RATE RATE CODE RATE RATE withholding allowances) is: The amount of income tax to withhold is: 1 ASRS PLAN-ASRS 7903 11.13% 10.90% 7904 9.87% 10.90% Not Over $83 ............................................................................................. $0 2 CORP JUVENILE CORRECTIONS (501) 7905 8.41% 8.41% 7906 9.92% 12.30% Over But not over - of excess over - 3 EORP ELECTED OFFICIALS & JUDGES (415) 7907 10.00% 11.50% 7908 17.96% 20.87% $83 - $417 10% $83 4 PSRS PUBLIC SAFETY (007) (ER pays 5% EE share) 7909 3.65% 4.55% 7910 38.30% 48.71% $417 - $1,442 $33.40 plus 15% $417 5 PSRS GAME & FISH (035) 7911 8.65% 9.55% 7912 43.35% 50.54% $1,442 - $3,377 $187.15 plus 25% $1,442 6 PSRS AG INVESTIGATORS (151) 7913 8.65% 9.55% 7914 90.08% 136.04% $3,377 - $6,954 $670.90 plus 28% $3,377 7 PSRS FIRE FIGHTERS (119) 7915 8.65% 9.55% 7916 17.76% 20.54% $6,954 - $15,019 $1,672.46 plus 33% $6,954 9 N/A NO RETIREMENT $15,019 ………………………………………………………$4,333.91 plus 35% $15,019 0 CORP CORRECTIONS (500) 7901 8.41% 8.41% 7902 9.15% 11.14% B PSRS LIQUOR CONTROL OFFICER (164) 7923 8.65% 9.55% 7924 38.77% 46.99% (b) MARRIED person F PSRS STATE PARKS (204) 7931 8.65% 9.55% 7932 18.50% 25.16% If the amount of wages (after subtracting G CORP PUBLIC SAFETY DISPATCHERS (563) 7933 7.96% 7.96% 7934 7.50% 7.90% withholding allowances) is: The amount of income tax to withhold is: H PSRS DEFERRED RET OPTION (DROP) 7957 8.65% 9.55% 0.24% AT 50/50 Not Over $312 ............................................................................................ -

Overview of the SWISS TAX SYSTEM

OVERVIEW OF THE SWISS TAX SYSTEM 10.1 Taxation of Corporate Taxpayers ...................................... 109 10.2 Tax Rate in an International Comparison ........................ 112 10 10.3 Taxation of Individual Taxpayers ..................................... 113 10.4 Withholding Tax ................................................................ 116 10.5 Value Added Tax................................................................ 117 10.6 Other Taxes........................................................................ 120 10.7 Double Tax Treaties .......................................................... 121 10.8 Corporate Tax Reform III .................................................. 121 10.9 Transfer Pricing Rules....................................................... 121 Image Tax return, stock image The Swiss tax system mirrors Switzerland’s federal struc- 10.1 TAXATION OF CORPORATE TAXPAYERS ture, which consists of 26 sovereign cantons with 2,352 10.1.1 Corporate Income Tax – Federal Level independent municipalities. Based on the constitution, all The Swiss federal government levies corporate income tax at a flat rate of 8.5% on profit after tax of corporations and cooperatives. cantons have full right of taxation except for those taxes For associations, foundations, and other legal entities as well as that are exclusively reserved for the federal government. As investment trusts, a flat rate of 4.25% applies. At the federal level, no capital tax is levied. a consequence, Switzerland has two levels of taxation: the -

Tax Us If You Can 2012 FINAL.Pdf

City Research Online City, University of London Institutional Repository Citation: Murphy, R. and Christensen, J.F. (2012). Tax us if you can. Chesham, UK: Tax Justice Network. This is the published version of the paper. This version of the publication may differ from the final published version. Permanent repository link: https://openaccess.city.ac.uk/id/eprint/16543/ Link to published version: Copyright: City Research Online aims to make research outputs of City, University of London available to a wider audience. Copyright and Moral Rights remain with the author(s) and/or copyright holders. URLs from City Research Online may be freely distributed and linked to. Reuse: Copies of full items can be used for personal research or study, educational, or not-for-profit purposes without prior permission or charge. Provided that the authors, title and full bibliographic details are credited, a hyperlink and/or URL is given for the original metadata page and the content is not changed in any way. City Research Online: http://openaccess.city.ac.uk/ [email protected] tax us nd if you can 2Edition INTRODUCTION TO THE TAX JUSTICE NETWORK The Tax Justice Network (TJN) brings together charities, non-governmental organisations, trade unions, social movements, churches and individuals with common interest in working for international tax co-operation and against tax avoidance, tax evasion and tax competition. What we share is our commitment to reducing poverty and inequality and enhancing the well being of the least well off around the world. In an era of globalisation, TJN is committed to a socially just, democratic and progressive system of taxation. -

Note on Taxation System

Note on Taxation system Introduction Today an important problem against each government is that how to get income temporarily by debt also, but they have to return it after some time. Some government income is received from government enterprises, administrative and judicial tasks and other such sources, but a big part of government income is received from taxation. Taxes: - Taxes are those compulsory payments which are used without any such hope towards government by tax payers that they will get direct benefit in return of them. According to Prof. Seligman, ‘’ Tax is that compulsory contribution given to Government by individuals which is paid in the payment of expenses in all general favours and no special benefit is given in lieu of that.’’ According to Trussing, ‘’The special thing is that in regard of tax in comparison to all amounts taken by government, quid pro quo is not found directly between taxpayer and government administration in it.’’ Characteristics of a Tax It is clear by above mentioned definitions that some specialties are found in tax which are as follows: - (1) Compulsory Contribution—Tax is a contribution given to state by people living within the premises of country due to residence and property etc. or by citizens and this contribution is given for general use only. Though it is a compulsory contribution, therefore, no individual can deny from the payment of tax. For example, no person can say that he is not getting benefit from some services provided by that state or he didn’t get the right to vote, therefore, he is not bound to pay tax. -

Can My Church Benefit from a CARES Act Forgivable Loan?

I hope this finds you well and living confidently into the times. Congress passed and the President signed the CARES Act this past Friday, March 27, 2020. I write to share specific information from the CARES Act that answers some of the questions that I have heard being asked. Can my church benefit from a CARES Act forgivable loan? This question is on the minds of most pastors and church leaders since the passage of the $2 trillion relief package. As I continue to participate in some and receive information from other webcasts and conference calls across the connection, there are some things you can begin to do to prepare to apply for the loan program. While I do not encourage you to borrow funds for normal operating expenses, it appears that this loan has the potential to become a grant that you would not need to repay. Attorneys and accountants are studying the bill and awaiting guidelines from the Small Business Administration (SBA) and the U.S. Treasury on how the CARES Act will be administered. However, it appears that churches and non-profits may be able to borrow money that could be completely forgiven if they maintain their previous 12-month staffing levels through June of 2020. Key Provisions: • Paycheck Protection Program (“PPP”) - Eligible churches and non-profits will be able to borrow up to 2.5 times their average monthly payroll and benefits up to $100,000. While this appears to cap the amount to approximately $40,000 of monthly current costs, it is not yet known if that is for all employees in the salary-paying entity or per person. -

Curacao Highlights 2020

International Tax Curaçao Highlights 2020 Updated January 2020 Recent developments: For the latest tax developments relating to Curaçao, see Deloitte tax@hand. Investment basics: Currency – Netherlands Antilles Guilder (ANG) Foreign exchange control – A 1% license fee will be calculated as a percentage of the gross outflow of money on transfers from residents to nonresidents, and on foreign currency cash transactions. Holding companies may obtain an exemption from the fee. Accounting principles/financial statements – IAS/IFRS applies. Financial statements must be prepared annually. Principal business entities – These are the public and private company (NV and BV), general partnership, (private) foundation, Curaçao trust, limited partnership, and branch of a foreign corporation. Corporate taxation: Rates Corporate income tax rate 22%/3%/0% Branch tax rate 22%/3%/0% Capital gains tax rate 22%/3%/0% Residence – A corporation is resident if it is incorporated under the laws of Curaçao or managed and controlled in Curaçao. Basis – In principle, residents are taxed on worldwide income. Exemptions may apply for profits derived by permanent establishments located abroad. In addition, as from 1 July 2018, foreign-source income is excluded from the profit tax base (although there is an exception for certain services, including insurance and reinsurance activities; trust activities; the services of notaries, lawyers, public accountants and tax consultants; related services; income derived from the exploitation of intellectual property (IP); and shipping activities). Page 1 of 7 Curaçao Highlights 2020 Nonresidents are taxed only on Curaçao-source income. Foreign-source income derived by residents that is not excluded from the profit tax base is subject to corporation tax in the same way as Curaçao-source income. -

Transfer of Ownership Guidelines

Transfer of Ownership Guidelines PREPARED BY THE MICHIGAN STATE TAX COMMISSION Issued October 30, 2017 TABLE OF CONTENTS Background Information 3 Transfer of Ownership Definitions 4 Deeds and Land Contracts 4 Trusts 5 Distributions Under Wills or By Courts 8 Leases 10 Ownership Changes of Legal Entities (Corporations, Partnerships, Limited Liability Companies, etc.) 11 Tenancies in Common 12 Cooperative Housing Corporations 13 Transfer of Ownership Exemptions 13 Spouses 14 Children and Other Relatives 15 Tenancies by the Entireties 18 Life Leases/Life Estates 19 Foreclosures and Forfeitures 23 Redemptions of Tax-Reverted Properties 24 Trusts 25 Court Orders 26 Joint Tenancies 27 Security Interests 33 Affiliated Groups 34 Normal Public Trades 35 Commonly Controlled Entities 35 Tax-Free Reorganizations 37 Qualified Agricultural Properties 38 Conservation Easements 41 Boy Scout, Girl Scout, Camp Fire Girls 4-H Clubs or Foundations, YMCA and YWCA 42 Property Transfer Affidavits 42 Partial Uncapping Situations 45 Delayed Uncappings 46 Background Information Why is a transfer of ownership significant with regard to property taxes? In accordance with the Michigan Constitution as amended by Michigan statutes, a transfer of ownership causes the taxable value of the transferred property to be uncapped in the calendar year following the year of the transfer of ownership. What is meant by “taxable value”? Taxable value is the value used to calculate the property taxes for a property. In general, the taxable value multiplied by the appropriate millage rate yields the property taxes for a property. What is meant by “taxable value uncapping”? Except for additions and losses to a property, annual increases in the property’s taxable value are limited to 1.05 or the inflation rate, whichever is less. -

Die Leiden Des Steuerlichen Wertes

Die Leiden des steuerlichen Wertes Introduction to German Tax Translation Introduction • Basis for taxation in Germany • Major legislative acts • Overview to major tax types • Recent changes to tax law • Resources Basis of Taxation • Grundgesetz (Basic Law) • Abgabenordung, “AO” (General Tax Code) • Finanzgerichtsordnung (Tax Court Procedural Code) Finanzverwaltungsgesetz (Financial/Fiscal Administration Act) Bewertungsgesetz (Valuation Act) • Establishes uniform rules on tax valuation • Applicable to all federal taxes and levies • Defines several common terms, e.g. – gemeiner Wert – Teilwert – Steuerbilanzwert – Einheitswert Major Tax Types • Direct versus indirect • Purpose – Revenue – Repricing (“social” taxes to affect demand) – Redistribution • Taxing (receiving) authority Major Legislation • Einkommensteuergesetz (Personal Income Tax Act) • Körperschaftsteuergesetz (Corporate Income Tax Act) • Umsatzsteuergesetz (Value Added Tax (VAT) Act • Gewerbesteuergesetz (Municipal Trade Tax Act) • Jahressteuergesetz (Annual Tax Act) • Erbschaftsteuergesetz (Inheritance Tax Act) • Grunderwerbsteuergesetz (Real Property Acquisition Tax Act) • Grundsteuergesetz (Real Property Tax Act) • Umwandlungssteuergesetz (Reorganization Tax Act) Tax Revenues in Germany Steuerart Tax Type 2007 revenues Percentage in € bn. 2007 Steueraufkommen Tax revenue 493.818 100.00% insgesamt in Deutschland Total in Germany Gemeinschaftliche Steuern Joint taxes 381.309 77.22% Payroll withholding Lohnsteuer und andere and other personal Einkommensteuern income taxes Direct -

The Cost of the Vote: Poll Taxes, Voter Identification Laws, and the Price of Democracy

File: Ellis final for Darby Created on: 4/9/2009 8:17:00 PM Last Printed: 5/19/2009 1:10:00 PM THE COST OF THE VOTE: POLL TAXES, VOTER IDENTIFICATION LAWS, AND THE PRICE OF DEMOCRACY ATIBA R. ELLIS† INTRODUCTION The election of Barack Obama as the forty-fourth President of the United States represents both the completion of a historical campaign season and a triumph of the Civil Rights revolution of the twentieth cen- tury. President Obama’s 2008 campaign, along with the campaigns of Senators Hillary Rodham Clinton and John McCain, was remarkable in both the identities of the politicians themselves1 and the attention they brought to the political process. In particular, Obama attracted voters from populations which have not been traditionally represented in na- tional politics. His run was hallmarked, in large part, by significant grassroots fundraising, a concerted effort to generate popular appeal, and, most important, massive voter turnout efforts.2 As a result, this election cycle generated significant increases in participation during the primary season.3 Turnout in the general election did not meet anticipated record † Legal Writing Instructor, Howard University School of Law. J.D., M.A., Duke Univer- sity, 2000. An early version of this paper was presented at the Writer’s Workshop of the Legal Writing Institute in summer 2007. Later versions were presented at the November 2007 Howard University School of Law faculty colloquy and the September 2008 Northeast People of Color Legal Scholarship Conference. I gratefully acknowledge Andrew Taslitz, Sherman Rogers, Derek Black, Paulette Caldwell, Phoebe Haddon, and Daniel Tokaji for their thoughtful comments on earlier drafts of this paper. -

Department of Customs

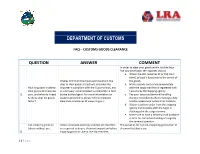

DEPARTMENT OF CUSTOMS FAQ – CUSTOMS GOODS CLEARANCE QUESTION ANSWER COMMENT In order to clear your goods within the five hour – five day timeframe, the importer should: a. Obtain the CRF (whether DI or PSI) from BIVAC at least 5 days prior to the arrival of It takes minimum five hours and maximum five the goods. days to clear goods at Customs, provided the b. Make a goods declaration immediately How long does it take to importer is compliant with the Customs laws, and after the cargo manifest is registered with clear goods at a Customs all necessary documentation is completed in time Customs by the shipping agency. 1. port, and what do I need by the broker/agent. For more information on c. Pay your taxes and terminal handling to do to clear my goods customs procedures, please refer to Customs charges immediately after receiving a duty faster? clearance procedures at www.lra.gov.lr. and tax assessment notice from Customs. d. Obtain a delivery order from the shipping agency immediately after the cargo is discharged in the cargo terminal. e. Make sure to have a delivery truck available in time for immediate loading of cargo by the terminal operator. Can I ship my goods to Unless otherwise expressly exempt, all importers The penalties for not pre-inspecting goods prior to Liberia without pre- are required to do pre-shipment inspection before shipment to Liberia are: 2. shipping goods to Liberia. the Government, 1 | P a g e shipment inspection through Administrative Regulation No. 12. 14263 – a. 10% of CIF value for first and second (PSI)? 2/MOF/R/BCE/14 October 2013, requires offense penalties for failure to have goods pre-inspected.