FTSE New Zealand Index

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Country's Biggest Warehouse Stationery Store

group executive GREG MUIR DAVID WILSON ROBERT SMITH PAUL HUTCHINSON BRUCE GORDON GRAHAM CHAD NEVILLE BROWN KEITH SMITH HAMISH McKENZIE BRENT WALDRON JOAN WITHERS STEPHEN TINDALL DAVE RICKARDS ROBERT CHALLINOR GLEN INGER NEIL PLUMMER JOHN AVERY JOHN DAHLSEN GRAHAM EVEVANSANS directors contents Chief Executive Officer’s Review ..........................................................................................................3 Triple Bottom Line Summary Report ....................................................................................................11 Corporate Governance ......................................................................................................................14 Founder’s Report ..............................................................................................................................22 Ten Year Review ..............................................................................................................................24 Financials ........................................................................................................................................26 highlights of the year Between 1 August 2000 and 31 July 2001 The Warehouse Group achieved an audited net surplus after tax of $60.8 million The Warehouse Group achieved sales of $1.665 billion The Warehouse New Zealand opened nine new stores - six in new locations and three replacement stores Warehouse Stationery opened nine new stores The Warehouse Australia opened ten new stores - eight in new locations -

Download PDF

Table of Contents Executive summary ............................................................................................... 2 What Auckland consumers have to say about electricity retail issues ........................... 3 The EAP has not fully met the requirements of the terms of reference ......................... 4 The big-5 incumbent retailers are to blame for residential price increases .................... 5 Sweet-heart deals with Tiwai Smelter are keeping prices artificially high ...................... 6 Stronger wholesale and retail competition needed to make electricity more affordable ... 8 Saves & Winbacks is making the two-tier retail market problem worse ...................... 11 Late payment penalties disadvantage vulnerable Kiwis unable to pay on time ............. 14 Prepayment arrangements exploit vulnerable consumers ......................................... 18 There are questions about compliance with the Vulnerable Consumer Guidelines and the objectives of the Guidelines .................................................................................. 19 Concluding remarks and recommendations ............................................................. 20 Appendix 1: Price increases over the last 18-years largely driven by retail (energy) .... 22 Appendix 2: Manipulation of pricing data can make it look like lines are to blame ........ 27 Appendix 3: The electricity retail and generation markets are highly “concentrated” .... 30 Appendix 4: Retail competition improvements driven by the last inquiry reforms -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Decision No 540

PUBLIC VERSION ISSN NO. 0114-2720 J6822 Commerce Commission Decision No 540 Determination pursuant to the Commerce Act 1986 in the matter of an application for clearance of a business acquisition involving: VECTOR LIMITED and NGC HOLDINGS LIMITED The Commission: P R Rebstock D R Bates QC D F Curtin Summary of Application: Vector Limited or an interconnected body corporate has sought clearance to acquire, whether directly or indirectly, up to and including 100% of the shares in NGC Holdings Limited Determination: Pursuant to section 66(3) (a)/(b) of the Commerce Act 1986, the Commission determines to give clearance to the proposed acquisition. Date of Determination: 10 December 2004 CONFIDENTIAL MATERIAL IN THIS REPORT IS CONTAINED IN SQUARE BRACKETS 2 TABLE OF CONTENTS THE PROPOSAL ....................................................................................................................4 STATUTORY FRAMEWORK..............................................................................................4 ANALYTICAL FRAMEWORK............................................................................................4 THE PARTIES.........................................................................................................................5 Vector....................................................................................................................................5 NGC.......................................................................................................................................5 PREVIOUS -

Attendee Conference Pack

Wind Energy Conference 2021 Rising to the Challenge 12 May 2021, InterContinental Hotel, Wellington, New Zealand Programme Joseph, aged 9 We would like to thank our sponsors for their support 2021 Wind Energy Conference – 12th May 2021 Wind Energy Conference Programme 12 May 2021 InterContinental, Wellington Rising to the Challenge Welcome and Minister’s The energy sector and renewables Presentation ▪ Hon Dr Megan Woods, Minister of Energy and Resources 8.30 – 9.00 Session 1 Facilitator: Dr Christina Hood, Compass Climate Decarbonising the New Zealand’s journey to net zero carbon energy sector ▪ Hon James Shaw, Minister of Climate Change 9.00 to 10.45 Infrastructure implications of decarbonisation ▪ Ross Copland, New Zealand Infrastructure Commission The industrial heat opportunity ▪ Linda Mulvihill, Fonterra Panel and Audience Discussion – testing our key opportunities and level of ambition ▪ Ross Copland, New Zealand Infrastructure Commission ▪ Linda Mulvihill, Fonterra ▪ Briony Bennett (she/her), Ministry of Business, Innovation and Employment ▪ Matt Burgess, The New Zealand Initiative ▪ Liz Yeaman, Retyna Ltd Morning Tea Sponsored by Ara Ake 10.45 to 11.15 Session 2 Waipipi, Delivering a wind farm during a global pandemic Jim Pearson, Tilt Renewables Building new wind Australian renewables and wind development update 11.15 -1.00 ▪ Kane Thornton, Clean Energy Council DNV’s Energy Transition Outlook what it means for wind energy ▪ Graham Slack, DNV A changing regulatory landscape and implications for wind and other renewables ▪ Amelia -

Westpac NZD Account 8.36% New Zealand Local Government

FULL PORTFOLIO HOLDINGS Offer name: Kiwi Wealth KiwiSaver Scheme Offer number: OFR10715 Fund name: Default Fund number: FND553 Periodic disclosure applies [dd/mm/yyyy] 30/06/2021 Asset Name % of fund net assets Security Code Westpac NZD Account 8.36% New Zealand Local Government Funding Agency Bond 3.5% 14 Apr 33 1.86% NZLGFDT009C0 14/4/2033 New Zealand Local Government Funding Agency Bond 4.5% 15 Apr 27 1.57% NZLGFDT007C4 15/4/2027 New Zealand Local Government Funding Agency Bond 1.5% 20 Apr 29 1.47% NZLGFDT012C4 20/4/2029 Westpac New Zealand - TD - 0.93% 05 Jul 21 5/7/2021 1.46% DU0TZ21705D8 Housing New Zealand Ltd 3.42% 18 Oct 28 18/10/2028 1.38% NZHNZD0628L7 Kommunalbanken AS 4% 20 Aug 25 20/8/2025 1.34% NZKBNDT009C6 International Bank for Reconstruction & Development 1.625% 10 1.24% NZIBDDT018C3 May 28 10/5/2028 Landwirtschaftliche Rentenbank 0.75% 09 Jun 25 9/6/2025 1.13% NZLRBDT014C1 New Zealand Government Bond 2% 15 May 32 15/5/2032 1.10% NZGOVDT532C8 Kommunalbanken AS 1.25% 02 Jul 30 2/7/2030 1.08% NZKBNDT012C0 Bank of China Ltd - TD - 0.75% 08 Sep 21 8/9/2021 1.05% DU0TZ21908A4 ANZ Bank Ltd - TD - 0.85% 13 Sep 21 13/9/2021 0.99% DU0TZ21913C0 Transpower New Zealand Ltd 1.735% 04 Sep 25 4/9/2025 0.96% NZTRPD0070L9 ANZ Bank Ltd - TD - 0.85% 20 Sep 21 20/9/2021 0.94% DU0TZ21920B7 ASB Bank - TD - 0.81% 22 Dec 21 22/12/2021 0.93% DU0TZ21D22A6 ANZ Bank Ltd - TD - 0.85% 26 Jul 21 26/7/2021 0.88% DU0TZ21726C6 ANZ Bank Ltd - TD - 0.85% 24 Aug 21 24/8/2021 0.88% DU0TZ21824A3 Westpac New Zealand - TD - 0.77% 29 Nov 21 29/11/2021 0.88% DU0TZ21N29C6 -

Wind, Rain, Fire and Sun: Towards Zero Carbon Electricity for New Zealand

Wind, rain, fire and sun: towards zero carbon electricity for New Zealand. Mina Bahrami Gholamia, Stephen Polettib and Iain Staffellc Abstract We examine different scenarios with large amounts of intermittent generation to achieve close to a 100% renewable electricity market in New Zealand. We use a cost based dispatch model to simulate market prices. Previous modelling has estimated electricity prices using the Long Run Marginal Cost approach. Our study is the first to model market prices explicitly, for scenarios with close to 100% renewable electricity, to see if the “energy only market” revenues are enough for investment cost recovery. Our modelling suggest that large amounts of wind on its own are better than mixed wind and solar scenarios. We also see a collapse in spot prices, as we get very close to 100% renewable. These prices are well below those needed to cover investment costs. We argue that there should be a market design change to a design that that includes direct payments for capacity, as well as for electricity output, to ensure investment cost recovery. Keywords: electricity markets; Solar PV; New Zealand; intermittent generation, hydro, 100% renewable. a Meridian Energy. Email [email protected] b Corresponding Author. Energy Centre, University of Auckland. Email [email protected] c Centre for Environmental Policy, Imperial College London. Email [email protected] 1 1. Introduction The New Zealand government parliament recently passed the Climate Change Response (Zero Carbon) Amendment Act, which formalises its intention to have net zero emissions for all greenhouse gases except for biogenic methane by 2050 (Ministry for the Environment, 2019). -

Energy Freedom for a Changing World

ENERGY FREEDOM FOR A CHANGING WORLD. 2020 ANNUAL REPORT // MERCURY NZ LIMITED MENU. ABOUT THIS MENU 1. ENERGY FREEDOM TODAY. 2. OUR WORLD OF ENERGY FREEDOM. REPORT. 04 WHO WE ARE 14 THE WORLD AROUND US 05 OUR DIRECTION 18 ENGAGING WITH OUR STAKEHOLDERS Mercury is committed to providing transparent disclosures in 06 OUR BUSINESS MODEL 20 THE RISKS WE FACE easily understood, comparable and engaging ways so that we meet the expectations of our many stakeholders. 09 CHAIR & CHIEF EXECUTIVE 21 PULLING IT ALL TOGETHER UPDATE 22 CREATING VALUE IN FY20 This report follows the Integrated Reporting <IR> framework. We describe Our Business Model, including inputs, outputs and the outcomes of our strategic approach across five pillars, taking a long-term view of value creation. We also include a specific Global Reporting Initiative (GRI) Standards index and our climate change section follows the Task Force on Climate- ABOUT THIS REPORT 3. LIVING ENERGY FREEDOM. related Financial Disclosures (TCFD). OUR PILLAR STORIES We have grouped our reporting into five sections to help you find areas of particular interest, but note that they are all part of who we are, what we do and why. Across all this, we seek to report openly and honestly on our performance in a way that shows the integrated approach CUSTOMER PARTNERSHIPS KAITIAKITANGA PEOPLE COMMERCIAL we take. If you have any comments about this report, including things 24 27 30 36 39 we could do better, please email [email protected] STATEMENT FROM THE DIRECTORS PREPARING FOR CLIMATE CHANGE The directors are pleased to present Mercury NZ Limited’s 33 integrated Annual Report and Financial Statements for the year ended 30 June 2020. -

Meridian Energy Limited

Opuha Water Limited Opuha Dam Dam Safety Review 7. Mechanical and Electrical Works 7.1 Introduction As outlined in section 5.3, we believe that the plant items critical to dam safety are: The service spillway gates including their operating equipment and power supplies. Gate lowering is essential for the passage of floods. The bypass valve including its operating equipment and power supplies. Valve operation is important for lowering the pond level in response to a dam safety emergency. The radial gate installed in the re-regulation pond outlet structure, including its operating equipment and power supplies. Although the re-regulation pond is a “low” PIC structure, gate opening is important for lowering the pond level in response to a dam safety emergency. The control and communication systems necessary for operation of the above facilities. The performance reliability of these systems is critical for an automatic and remotely controlled facility. 7.2 Mechanical and Electrical Inspection Observations made during our site inspection on the 23rd of March 2012 are summarised in table 7.1. The weather was initially foggy and then cloudy, and mild with no wind. The Opuha reservoir level was RL390.19m and remained fairly constant throughout the inspection. The re-regulation pond water level was RL338.17m and the radial gate was discharging 12m3/s. Table 7.1: Site Inspection Feature Remarks Spillway Gates Access Easy access from State Highway 79 via Trentham Road and the unsealed Opuha dam road. Power Supplies A 100kVA, 33/0.4kV pole mounted transformer connected to the 33kV line feeds the powerhouse 400V switchboard, from which a 400V cable feeds the gatehouse equipment. -

Meridian Energy Limited Cash Flow Powerhouse

25 September 2013 Meridian Energy Limited Cash Flow Powerhouse Important Notice, Disclosures, Limitations & Disclaimer – Please refer to page 2 for important disclosures, limitations and disclaimer. • Meridian Energy Limited (Meridian) is New Zealand’s largest electricity Analyst generator, generating around 13,000 GWh annually from low cost hydro and Nevill Gluyas, CFA wind sources. It supplies 272,000 customers and 5,000 GWh p.a. to the Tiwai +64 4 496 5338 Point aluminium smelter. Reliance on hydro generation and its influence on [email protected] electricity prices can result in significant earnings volatility from year to year. • Our risk weighted DCF valuation of $2.00 per share assumes Tiwai smelter remains operating at a 1,500GWh reduced load after 2015 and that real electricity prices increase from circa $70/MWh to $80/MWh by 2025. It also incorporates a modest chance of the Labour/Greens policy being implemented and a chance that Tiwai smelter may close. In contrast, using comparable valuation multiples for Contact Energy (CEN) and Mighty River Power (MRP) imply Meridian shares may trade around $1.50. • We estimate the Labour/Green proposal to reform the NZ electricity market would reduce our base case valuation by $0.69 to $1.39. However, the estimated impact of Tiwai smelter closing is only $0.02 per share. • Factors which could result in an increase in Meridian’s share price include: • • Potential revision of transmission pricing - $0.25 per share. • • Cost reductions - $0.10 per share. • Retail electricity margin improvement - $0.05 per share. Meridian Energy Cash Flow Powerhouse Important Notice, Limitations and Disclaimer Important Notice: Before making an investment decision, investors must consider whether they have sufficient information also having regard to their particular investment needs, objectives, level of acceptable risk and financial circumstances and, if necessary, seek financial advice. -

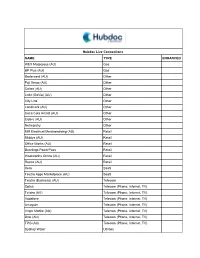

Hubdoc Live Connections NAME TYPE ENHANCED WEX Motorpass

Hubdoc Live Connections NAME TYPE ENHANCED WEX Motorpass (AU) Gas BP Plus (AU) Gas Bartercard (AU) Other Fuji Xerox (AU) Other Caltex (AU) Other Linkt (GoVia) (AU) Other City Link Other Landmark (AU) Other Coca Cola Amatil (AU) Other Elders (AU) Other Netregistry Other MM Electrical Merchandising (AU) Retail Middys (AU) Retail Office Works (AU) Retail Bunnings PowerPass Retail Woolworths Online (AU) Retail Reece (AU) Retail Xero SaaS Telstra Apps Marketplace (AU) SaaS Telstra (Business) (AU) Telecom Optus Telecom (Phone, Internet, TV) Telstra (AU) Telecom (Phone, Internet, TV) Vodafone Telecom (Phone, Internet, TV) Amaysim Telecom (Phone, Internet, TV) Virgin Mobile (AU) Telecom (Phone, Internet, TV) iiNet (AU) Telecom (Phone, Internet, TV) TPG (AU) Telecom (Phone, Internet, TV) Sydney Water Utilities AGL Energy Online (Business) Utilities Link Market Services (Portfolio Login) (AU) Utilities Sensis (AU) Utilities Energy Australia Utilities Synergy (AU) Utilities Origin Energy (AU) Utilities AGL Energy Online Utilities Servus (Business) Banks and Credit Cards Meridian Credit Union Banks and Credit Cards Yes RBC Banks and Credit Cards Yes CIBC Banks and Credit Cards Yes Scotiabank Banks and Credit Cards Yes Interior Savings Credit Union Banks and Credit Cards ATB Financial (Business) Banks and Credit Cards Yes Tangerine (ING Direct) Banks and Credit Cards Yes RBC Express Banks and Credit Cards American Express (Canada) Banks and Credit Cards Yes Westoba Credit Union Banks and Credit Cards BMO Debit Card Banks and Credit Cards Yes President's -

2018 Annual Report

VECTOR:// EMPOWERING AR 2018 for new zealand’s energy consumer revolution. 01/05: 2 Vector://AR 18 TODAY POWERFUL FORCES ARE SHAPING ENERGY USE. NEW ENERGY TECHNOLOGIES ARE IMPROVING. CONSUMERS ARE EXPECTING MORE AND MORE CHOICE AND CONTROL. THE ECONOMY IS PROGRESSIVELY ELECTRIFYING – STARTING WITH TRANSPORT. USE OF SOLAR, WIND, AND BATTERY IS ON THE WAY UP. CLIMATE CHANGE IS INCREASINGLY BEING FELT. VECTOR IS EMBRACING ALL THESE FORCES – TO PUT MORE POWER IN YOUR HANDS. VECTOR.CO.NZ EMPOWERING YOU. 3 Vector://AR 18 02/05: STAYING AHEAD OF THE CURVE.WE BELIEVE IT’S ABOUT SHOWING LEADERSHIP, TECHNOLOG- ICALLY, CONNECTIVELY AND SUSTAINABLY. LEADERSHIP ON ENERGISING YOUR LIFE, HOME, AND BUSINESS. LEADERSHIP ON DIVERSIFYING INTO NEW BUSINESSES AND NEW ENERGY TECHNOLOGIES TO CREATE FRESH CUSTOMER SOLUTIONS. LEADERSHIP ON CREATING CHANGE TO BENEFIT CONSUMERS. LEADERSHIP ON ADDRESSING CLIMATE CHANGE AND EXTREME WEATHER EVENTS. LEADERSHIP ON SAFETY, DIVERSITY, AND THE THINGS THAT MATTER MOST. 4 Vector://AR 18 5 Vector://AR 1718 03/05: 6 Vector://AR 18 CHANGE WILL ONLY ACCELERATE. VECTOR HAS COME A LONG WAY OVER THE YEARS. WE’VE STRENGTHENED OUR CONNECTION TO AUCKLAND, AND REPOSITIONED FOR THE FUTURE. WE’RE THINKING BEYOND TODAY, AND LEARNING FAST AS WE GO. NEW ZEALAND’S ENERGY FUTURE WILL BE EVEN MORE DISRUPTIVE, MORE CONSUMER ORIENTED, MORE TECHNOLOGY-ENABLED, MORE RESILIENT, MORE DEMOCRATIC, MORE SUSTAINABLE AND, ULTIMATELY, MORE ABOUT CHOICE. YOUR CHOICE. 7 Vector://AR 18 04/05: COMMITTED TO THE LONG GAME. ACCELERATING CHANGE MAKES OUR VISION MORE VITAL THAN EVER. WE HAVE TO KEEP MOVING AND STAY COMMITTED TO PLAYING THE LONG GAME, BEING RESILIENT AND BEING RESPONSIVE TO THE POWERFUL FORCES THAT ARE SHAPING ENERGY USE.