2012 IBM Annual Report a Letter from the Chairman 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IBM Software Support

Version 5.0.0 What’s New . Phone Contacts We have eliminated the phone number section from this document and direct you to IBM Planetwide for contact information. I would appreciate your feedback on what you like and what you think should be improved about this document. e-mail me at mcknight@ us.ibm.com Cover design by Rick Nelson, IBM Raleigh 2 June, 2014 Contents What’s New ................................................................................... 2 Overview of IBM Support .............................................................. 4 IBM Commitment......................................................................... 4 Software Support Organization ...................................................... 4 Software Support Portfolio ................................................................. 5 IBM Software Support ...................................................... 5 Support Foundation .......................................................................... 5 Passport Advantage & IBM Software Maintenance ................................ 6 System z (S/390) ......................................................................... 7 Support Line and SoftwareXcel ..................................................... 7 IBM Selected Support Offering ....................................................... 8 Premium Support ............................................................................ 8 Enhanced Technical Support ........................................................ 8 IBM Software Accelerated Value -

IBM Cloud Unit 2016 IBM Cloud Unit Leadership Organization

IBM Cloud Technical Academy IBM Cloud Unit 2016 IBM Cloud Unit Leadership Organization SVP IBM Cloud Robert LeBlanc GM Cloud Platform GM Cloud GM Cloud Managed GM Cloud GM Cloud Object Integration Services Video Storage Offering Bill Karpovich Mike Valente Braxton Jarratt Line Execs Line Execs Marie Wieck John Morris GM Strategy, GM Client Technical VP Development VP Service Delivery Business Dev Engagement Don Rippert Steve Robinson Harish Grama Janice Fischer J. Comfort (GM & CTO) J. Considine (Innovation Lab) Function Function Leadership Leadership VP Marketing GM WW Sales & VP Finance VP Human Quincy Allen Channels Resources Steve Cowley Steve Lasher Sam Ladah S. Carter (GM EcoD) GM Design VP Enterprise Mobile GM Digital Phil Gilbert Phil Buckellew Kevin Eagan Missions Missions Enterprise IBM Confidential IBM Hybrid Cloud Guiding Principles Choice with! Hybrid ! DevOps! Cognitive Powerful, Consistency! Integration! Productivity! Solutions! Accessible Data and Analytics! The right Unlock existing Automation, tooling Applications and Connect and extract workload in the IT investments and composable systems that insight from all types right place and Intellectual services to increase have the ability to of data Property speed learn Three entry points 1. Create! 2. Connect! 3. Optimize! new cloud apps! existing apps and data! any app! 2016 IBM Cloud Offerings aligned to the Enterprise’s hybrid cloud needs IBM Cloud Platform IBM Cloud Integration IBM Cloud Managed Offerings Offerings Services Offerings Mission: Build true cloud platform -

Chicago Board Options Exchange Annual Report 2001

01 Chicago Board Options Exchange Annual Report 2001 cv2 CBOE ‘01 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 CBOE is the largest and 01010101010101010most successful options 01010101010101010marketplace in the world. 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010ifc1 CBOE ‘01 ONE HAS OPPORTUNITIES The NUMBER ONE Options Exchange provides customers with a wide selection of products to achieve their unique investment goals. ONE HAS RESPONSIBILITIES The NUMBER ONE Options Exchange is responsible for representing the interests of its members and customers. Whether testifying before Congress, commenting on proposed legislation or working with the Securities and Exchange Commission on finalizing regulations, the CBOE weighs in on behalf of options users everywhere. As an advocate for informed investing, CBOE offers a wide array of educational vehicles, all targeted at educating investors about the use of options as an effective risk management tool. ONE HAS RESOURCES The NUMBER ONE Options Exchange offers a wide variety of resources beginning with a large community of traders who are the most experienced, highly-skilled, well-capitalized liquidity providers in the options arena. In addition, CBOE has a unique, sophisticated hybrid trading floor that facilitates efficient trading. 01 CBOE ‘01 2 CBOE ‘01 “ TO BE THE LEADING MARKETPLACE FOR FINANCIAL DERIVATIVE PRODUCTS, WITH FAIR AND EFFICIENT MARKETS CHARACTERIZED BY DEPTH, LIQUIDITY AND BEST EXECUTION OF PARTICIPANT ORDERS.” CBOE MISSION LETTER FROM THE OFFICE OF THE CHAIRMAN Unprecedented challenges and a need for strategic agility characterized a positive but demanding year in the overall options marketplace. The Chicago Board Options Exchange ® (CBOE®) enjoyed a record-breaking fiscal year, with a 2.2% growth in contracts traded when compared to Fiscal Year 2000, also a record-breaker. -

My Detailed Resume

William B. Davis, Jr. Windsor Heights, IA (515) 360-0445 linkedin.com/in/billdavisjr [email protected] SOFTWARE & WEB DEVELOPER Accomplished IT professional with extensive experience in all facets of software development lifecycle, user training, and support. Skilled at documentation and user interface design. Always interested in examining new technologies while keeping focus on long-term system planning and maintainability. TECHNICAL SKILLS ● Computers: PCs (Windows, Mac, other), minicomputers (DEC/HP VAX and Alpha), and mainframe (IBM 3090). ● Web technologies: HTML, CSS, Java Server Pages, ASP, and ASP.NET. ● Languages: Java & JSP, JavaScript, Visual BASIC 6 & VBA, VMS BASIC, Microsoft BASIC, Microsoft C, Lattice C, Perl, SQL, COBOL, Pascal, Ruby / Rails, various Assembly languages. ● Scripting: VMS DCL, IBM JCL, Microsoft VBA and VBScript, Unix bash, Windows/DOS batch scripting. ● Operating Systems: Windows, Mac OS & OS X, DEC/HP OpenVMS, Unix, AIX, Linux, other. ● Integrated Development Environments (IDEs): Eclipse, IBM RAD 6, ISPF & Panvalet, Visual -

Service Description IBM Kenexa Talent Acquisition This Service Description Describes the Cloud Service IBM Provides to Client

Service Description IBM Kenexa Talent Acquisition This Service Description describes the Cloud Service IBM provides to Client. Client means the company and its authorized users and recipients of the Cloud Service. The applicable Quotation and Proof of Entitlement (PoE) are provided as separate Transaction Documents 1. IBM Kenexa BrassRing on Cloud The IBM Kenexa Talent BrassRing on Cloud SaaS offering is made up of the following components: a. IBM Kenexa BrassRing on Cloud b. IBM Kenexa BrassRing on Cloud is a scalable, online tool that helps employers and recruiters centralize and manage the Talent Acquisition process across multiple company divisions or locations. Base offering features include: ● Creating and posting job requisitions ● Sourcing ● Talent Gateways for candidates to search jobs and submit interest ● Tracking applications and work flow ● Screening candidates ● Approval levels to facilitate the selection processes ● Standard and ad-hoc reporting capabilities ● Social media interfaces and mobile technology c. The IBM Kenexa BrassRing on Cloud will be provided in both a staging and production environments. The staging environment will be provided through the life of the contract for testing purposes. d. The IBM Kenexa BrassRing on Cloud Onboard can be branded to Client’s company logo and colors. 2. IBM Kenexa Talent Acquisition BrassRing Onboard The IBM Kenexa Talent Acquisition BrassRing Onboard SaaS offering is made up of the following components: a. IBM Kenexa BrassRing on Cloud IBM Kenexa BrassRing on Cloud is a scalable, online tool that helps employers and recruiters centralize and manage the Talent Acquisition process across multiple company divisions or locations. Base offering features include: ● Creating and posting job requisitions ● Sourcing ● Talent Gateways for candidates to search jobs and submit interest ● Tracking applications and work flow ● Screening candidates ● Approval levels to facilitate the selection processes ● Standard and ad-hoc reporting capabilities ● Social media interfaces and mobile technology b. -

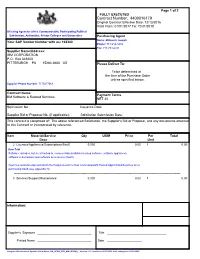

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

Michael Mcgeein, CPA, CA September 2018

IBM Cognos Analytics Data Prep. and Modelling Working with your data Michael McGeein, CPA, CA September 2018 IBM Business Analytics :: IBM Confidential :: © 2016 IBM Corporation Notices and disclaimers Copyright © 2018 by International Business Machines Corporation (IBM). as illustrations of how those customers have used IBM products and No part of this document may be reproduced or transmitted in any form without the results they may have achieved. Actual performance, cost, savings or other written permission from IBM. results in other operating environments may vary. U.S. Government Users Restricted Rights — use, duplication or disclosure References in this document to IBM products, programs, or services does not restricted by GSA ADP Schedule Contract with IBM. imply that IBM intends to make such products, programs or services available in all countries in which IBM operates or does business. Information in these presentations (including information relating to products that have not yet been announced by IBM) has been reviewed for accuracy as Workshops, sessions and associated materials may have been prepared by of the date of initial publication and could include unintentional technical or independent session speakers, and do not necessarily reflect the typographical errors. IBM shall have no responsibility to update this information. views of IBM. All materials and discussions are provided for informational This document is distributed “as is” without any warranty, either express or purposes only, and are neither intended to, nor shall constitute legal or other implied. In no event shall IBM be liable for any damage arising from the use of guidance or advice to any individual participant or their specific situation. -

Java and Z/OS (And Rdz)

® IBM Software Group Java and z/OS (and RDz) Jon Sayles – [email protected] © 2016 IBM Corporation IBM Software Group | Rational software Merrill Class . They’ll have RDz exposure . Terms & Concepts & Vocabulary Remove fear of Java Analogies – Procedural vocabulary 20 – 30 students - mix of young + old (mostly old) dudes . Call COBOL from Java Java doesn’t create an .exe Objects . z/OS Java Standard z/OS environment JCL – pointing to Unix Aware of JVM – can call COBOL http://www.s390java.com/index.htm IBM Software Group | Rational software Trademarks Trademarks The following are trademarks of the International Business Machines Corporation in the United States and/or other countries. For a complete list of IBM Trademarks, see www.ibm.com/legal/copytrade.shtml: AS/400, DBE, e-business logo, ESCO, eServer, FICON, IBM, IBM Logo, iSeries, MVS, OS/390, pSeries, RS/6000, S/30, VM/ESA, VSE/ESA, Websphere, xSeries, z/OS, zSeries, z/VM The following are trademarks or registered trademarks of other companies Lotus, Notes, and Domino are trademarks or registered trademarks of Lotus Development Corporation Java and all Java-related trademarks and logos are trademarks of Sun Microsystems, Inc., in the United States and other countries LINUX is a registered trademark of Linux Torvalds UNIX is a registered trademark of The Open Group in the United States and other countries. Microsoft, Windows and Windows NT are registered trademarks of Microsoft Corporation. SET and Secure Electronic Transaction are trademarks owned by SET Secure Electronic Transaction LLC. Intel is a registered trademark of Intel Corporation * All other products may be trademarks or registered trademarks of their respective companies. -

Clarion Alumni July 2001

Volume 48 No. 2 July 2001 Clarion University of Pennsylvania Alumni News Surrogate Parenting... Animal Refuge Style -See Page 15- Clarion Grads Lighting a Fire at Scholarship Auction Raises $55,000 Zippo -See Page 8- -See Page 9- Alumni Association Announces Recipients of ‘Distinguished Awards’ See Pages 6 & 7 www.clarion.edu/news 2-CLARION ALUMNI NEWS A L U M N I A S S O C I A T I O N CLARION ALUMNI NEWS Clarion Alumni News is published Stay in Touch three times a year by the Clarion University Alumni Association and remember the day I earned my undergraduate the Office of University Relations. degrees. It was in December of 1997 and even then Tippin Send comments to: University Iwas hot. The speakers were inspirational, my Relations Department, Clarion friends and family were there to cheer and I had an University, 974 E. Wood St., Clarion, PA 16214-1232; 814-393-2334; FAX overwhelming feeling of accomplishment. I 814-393-2082; or e-mail remember sitting in the gym next to my good [email protected]. friend Jen Founds and other communication majors, the people I had been in classes with for ALUMNI ASSOCIATION Alumni Events Calendar four years. It was an incredible day, the day that BOARD OF DIRECTORS you think about from the time you’re in junior Larry W. Jamison ’87,President Saturday, July 28 - Saturday, September 2001 high school. This was the payoff for all my hard John R. Mumford ’73 &’75, Pres.-elect August 4 Saturday, September 8 Wendy A. Clayton, ’85, secretary State System of Higher Alpha Sigma Alpha Gamma work. -

Software Withdrawal and Service Discontinuance: IBM Middleware, IBM Security, IBM Analytics, IBM Storage Software, and IBM Z

IBM United States Withdrawal Announcement 916-117, dated September 13, 2016 Software withdrawal and service discontinuance: IBM Middleware, IBM Security, IBM Analytics, IBM Storage Software, and IBM z Systems select products - Some replacements available Table of contents 1 Overview 107Replacement program information 10 Withdrawn programs 210Corrections Overview Effective on the dates shown, IBM(R) will withdraw support for the following program's VRM licensed under the IBM International Program License Agreement: VRM (V3.2.1) Note: V= All means all versions Note: V#.x means all releases of the version # listed Note: V#.#.x means all mods of the version release # listed For Advanced Administration System (AAS) Systems products Program number Program release VRM Withdrawal from name support date 5608-W07 IBM Tivoli(R) 3.2.x September 30, Storage 2017 (See Note FlashCopy(R) SUPT below) Manager For Passport Advantage(R) (PPA) On Premises products IBM Analytics products Program number Program release VRM Withdrawal from name support date 5639-I80 IBM Content 2.3.x September 30, Manager 2018 ImagePlus(R) Workstation program 5722-VI1 IBM DB2(R) 5.3.x September 30, Content Manager 2018 for iSeries 5724-B35 IBM InfoSphere(R) 5.5.x September 30, OptimTM 2016 Application Repository Analyzer 5724-B35 IBM InfoSphere 6.x September 30, Optim Application 2016 Repository Analyzer IBM United States Withdrawal Announcement 916-117 IBM is a registered trademark of International Business Machines Corporation 1 Program number Program release VRM Withdrawal -

Oral History Interview with Sam Wyly

An Interview with SAM WYLY OH 374 Conducted by David Allison on 6 December 2002 Smithsonian National Museum of American History Washington, D.C. Charles Babbage Institute Center for the History of Information Technology University of Minnesota, Minneapolis Copyright 2004, Charles Babbage Institute Sam Wyly Interview 6 December 2002 Abstract Wyly begins by recounting his childhood, and education prior to going to work for IBM’s Service Bureau Corporation, and then joining Honeywell as an area sales manager. He discusses how he left Honeywell to form University Computer Corporation (UCC), a firm that sold computer time, but transitioned into a software services business. Wyly explains his growing focus on computing and telecommunications, his formation of Datran, and his unsuccessful attempt to acquire Western Union. Much of the interview focuses on ongoing developments at UCC, the eventual sale of this firm to Computer Associates, his formation of Sterling Software, its acquisition of Informatics, the sale of Sterling, and his ideas on the future of information technology. Throughout Wyly’s discussion of UCC and Sterling, he elucidates upon his leadership philosophy, and the strategic, technical, operational, and financial management of these firms. This oral history was sponsored by the Software History Center in conjunction with the Center's ADAPSO reunion (3 May 2002). Preface As part of its preservation activities, the Software History Center (SHC) worked with Dr. David Allison of the Smithsonian Institution’s National Museum of American History and Dr. Jeffrey Yost of the Charles Babbage Institute to plan and conduct a number of oral history interviews of early software company founders and other key industry contributors. -

Annual Report 2011

ANNUAL REPORT 2011 TO OUR STOCKHOLDERS: I am pleased to report that KLA-Tencor performed at record levels on several fronts in fi scal year 2011. We achieved company records in our most critical fi nancial metrics, including revenues, net income, earnings per share and profi t margins, and our year-over-year revenue growth signifi cantly exceeded that of our peer group and our industry. At the same time, we generated record free cash fl ow and continued to deliver meaningful returns to our stockholders in the form of dividends and stock repurchases. This performance was the result of our unwavering focus on develop- ing market-leading technology, addressing our customers’ most critical needs and driving operational effi ciency. Though our industry has seen a recent slowdown in demand, we remain very excited about KLA-Tencor’s prospects for the future. The long-term demand drivers for KLA-Tencor and our industry remain intact, and we are well positioned to grow as demand for semiconductor capital equipment recovers. Our record results in fi scal year 2011 demonstrate that our strategies are working. Looking back over our 35-year history, we have established a pattern of achievement and leadership, which has enabled us to create the strong foundation from which we now look ahead to the future. Our accomplishments during fi scal year 2011 in each of our four strategic objectives (Customer Focus, Growth, Operational Excellence and Talent Development) are highlighted below: CUSTOMER FOCUS: MARKET LEADERSHIP Our customer focus strategic objective is measured in customer satisfaction and market share. We maintained our market leadership positions among our foundry and logic customers in fi scal year 2011 and improved our market position in memory, as evidenced by achieving record new order levels across all our end markets during the year.