Nafa Asset Allocation Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prospectus, Especially the Risk Factors Given at Para 4.11 of This Prospectus Before Making Any Investment Decision

ADVICE FOR INVESTORS INVESTORS ARE STRONGLY ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS PROSPECTUS, ESPECIALLY THE RISK FACTORS GIVEN AT PARA 4.11 OF THIS PROSPECTUS BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FALSE AND FICTITIOUS APPLICATIONS ARE PROHIBITED AND SUCH APPLICATIONS’ MONEY MAY BE FORFEITED UNDER SECTION 87(8) OF THE SECURITIES ACT, 2015. SONERI BANK LIMITED PROSPECTUS THE ISSUE SIZE OF FULLY PAID UP, RATED, LISTED, PERPETUAL, UNSECURED, SUBORDINATED, NON-CUMULATIVE AND CONTINGENT CONVERTIBLE DEBT INSTRUMENTS IN THE NATURE OF TERM FINANCE CERTIFICATES (“TFCS”) IS PKR 4,000 MILLION, OUT OF WHICH TFCS OF PKR 3,600 MILLION (90% OF ISSUE SIZE) ARE ISSUED TO THE PRE-IPO INVESTORS AND PKR 400 MILLION (10% OF ISSUE SIZE) ARE BEING OFFERED TO THE GENERAL PUBLIC BY WAY OF INITIAL PUBLIC OFFER THROUGH THIS PROSPECTUS RATE OF RETURN: PERPETUAL INSTRUMENT @ 6 MONTH KIBOR* (ASK SIDE) PLUS 2.00% P.A INSTRUMENT RATING: A (SINGLE A) BY THE PAKISTAN CREDIT RATING COMPANY LIMITED LONG TERM ENTITY RATING: “AA-” (DOUBLE A MINUS) SHORT TERM ENTITY RATING: “A1+” (A ONE PLUS) BY THE PAKISTAN CREDIT RATING AGENCY LIMITED AS PER PSX’S LISTING OF COMPANIES AND SECURITIES REGULATIONS, THE DRAFT PROSPECTUS WAS PLACED ON PSX’S WEBSITE, FOR SEEKING PUBLIC COMMENTS, FOR SEVEN (7) WORKING DAYS STARTING FROM OCTOBER 18, 2018 TO OCTOBER 26, 2018. NO COMMENTS HAVE BEEN RECEIVED ON THE DRAFT PROSPECTUS. DATE OF PUBLIC SUBSCRIPTION: FROM DECEMBER 5, 2018 TO DECEMBER 6, 2018 (FROM: 9:00 AM TO 5:00 PM) (BOTH DAYS INCLUSIVE) CONSULTANT TO THE ISSUE BANKERS TO THE ISSUE (RETAIL PORTION) Allied Bank Limited Askari Bank Limited Bank Alfalah Limited** Bank Al Habib Limited Faysal Bank Limited Habib Metropolitan Bank Limited JS Bank Limited MCB Bank Limited Silk Bank Limited Soneri Bank Limited United Bank Limited** **In order to facilitate investors, United Bank Limited (“UBL”) and Bank Alfalah Limited (“BAFL”) are providing the facility of electronic submission of application (e‐IPO) to their account holders. -

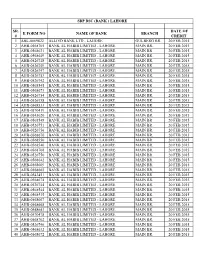

Sr. # E Form No Name of Bank Branch Date of Credit 1 Abl-0069822 Allied Bank

SBP BSC (BANK ) LAHORE SR. DATE OF E FORM NO NAME OF BANK BRANCH # CREDIT 1 ABL-0069822 ALLIED BANK LTD - LAHORE GULBERG BR. 20 FEB 2015 2 AHB-0568705 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 3 AHB-0568631 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 4 AHB-0568649 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 5 AHB-0526748 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 6 AHB-0526749 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 7 AHB-0526747 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 8 AHB-0526753 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 9 AHB-0526742 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 10 AHB-0568545 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 11 AHB-0568673 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 12 AHB-0526754 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 13 AHB-0526758 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 14 AHB-0568533 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 15 AHB-0570419 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 16 AHB-0543020 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 17 AHB-0568548 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 18 AHB-0526751 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 19 AHB-0526756 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 20 AHB-0568670 BANK AL HABIB LIMITED - LAHORE MAIN BR. -

WHY SILK? 111-007-455 2009 Inspiration for the Name Silkbank Comes from the Silk Route - a Trade Corridor Connecting Asia to Europe and the Rest of the World

Silkbank Building ANNUAL I.I. Chundrigar Road, Karachi REPORT www.silkbank.com.pk WHY SILK? 111-007-455 2009 Inspiration for the name Silkbank comes from the Silk Route - a trade corridor connecting Asia to Europe and the rest of the world. Silk, known for its distinctive properties and characteristics, symbolizes Silkbank’s brand beliefs. Premium & Upscale Silk is known for class and premium quality. Silkbank is positioned as an upscale bank providing its customers with premium banking experience. Talent & Innovation Silk embodies talent and timeless innovation. Silkbank promises its customers innovative products delivered through talented staff. Strong & Reliable Silk is amongst the strongest fibres known to mankind. Silkbank derives its strength from its strong international institutional sponsors giving it credibility and reliability. Dependable Silk through the times has held its value. Silkbank driven by a team of professionals provides an optimal experience that you can depend on. Contents Vision & Mission 02 Chairman's Message 03 Silkbank Products President & CEO's Message 05 Senior Management Committee 07 Assets Corporate Information 11 Directors’ Report 15 Statement of Compliance with the Code of Liabilities Corporate Governance 23 Statement of Internal Control 25 Notice of AGM 29 Review Report to the Members on Statement of Compliance with the Best Practices of Code of Corporate Governance 30 Independent Auditors’ Report 33 Balance Sheet 37 Profit and Loss Account 38 Statement of Comprehensive Income 39 Cash Flow Statement -

Snapshot of Results of Banks in Pakistan Snapshot of Results of Banks in Pakistan Six Months Period Ended 30 June 2016

KPMG Taseer Hadi & Co. Chartered Accountants Snapshot of results of Banks in Pakistan Snapshot of results of banks in Pakistan Six months period ended 30 June 2016 This snapshot has been prepared by KPMG Taseer Hadi & Co. and summarizes the performance of selected banks in Pakistan for the 6 months period ended 30 June 2016. The information contained in this snapshot has been obtained from the published consolidated financial statements of the banks and where consolidated financial statements were not available, standalone financials have been used. Reference should be made to the published financial statements of the banks to enhance the understanding of ratios and analysis of performance of a particular bank. We have tried to provide relevant financial analysis of the banks which we thought would be useful for benchmarking and comparison. However, we welcome any comments, which would facilitate in improving the contents of this document. The comments may be sent on [email protected] Dated: 23 September 2016 Karachi © 2016 KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistan and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2 Document Classification: KPMG Public HBL NBP UBL MCB ABL BAF 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 Ranking By total assets 1 1 2 2 3 3 4 4 5 5 6 6 By net assets 1 1 2 2 3 3 4 4 5 5 7 7 By profit before tax 1 1 4 4 2 3 3 2 5 5 7 8 Profit before tax * 28,298 -

The Road to Inclusion 2015 FINCA ANNUAL REPORT the FINCA Journey: Founder’S Letter

The Road to Inclusion 2015 FINCA ANNUAL REPORT The FINCA Journey: Founder’s Letter From its birth, FINCA’s purpose has The very scope and rapidity of FINCA’s growth, and that been inclusion: to serve the world’s most of the global microfinance movement, is testimony to how large was the exclusion that existed around the disadvantaged citizens. world, particularly with regard to women’s access to credit. Today, millions of mothers and fathers in the When FINCA launched its first “Village Banks” in the developing world have not one but several microfinance 1980s, our purpose was to assist illiterate, unemployed, providers who will give a small loan of working capital— and poverty-stricken families—especially mothers— often accessed by cellphone within a matter of minutes. with $50 loans to create businesses capable of generating $2–$3 of extra income per day. This result, Inclusion of women, and rapid access to working we trusted, would be just enough to improve their capital (or savings), is just the start of another process children’s nutrition, keep them in school and still set of inclusion. A growing business enables a FINCA aside a few cents per day in savings. borrower to improve her family’s nutrition and health, to keep her children in school, to buy a solar-powered This was a revolutionary proposition at the time. lamp and to simply hope and plan for the future. A child Throughout the underdeveloped world, 80% of citizens, who stays in school long enough to become numerate women in particular, were excluded from access to and literate will be able to earn a wage five times greater credit from the commercial banking system. -

Pace (Pakistan) Limited

PACE (PAKISTAN) LIMITED UNCONSOLIDATED FINANCIAL STATEMENTS FOR THE PERIOD ENDED 30 SEPTEMBER 2020 Pace (Pakistan) Limited Company Information Board of Directors Shehryar Ali Taseer (Chairman) Non-Executive Aamna Taseer (CEO) Executive Shahbaz Ali Taseer Executive Shehrbano Taseer Non-Executive Mian Ehsan Ul Haq Non-Executive Kanwar Latafat Ali Khan Independent Shavez Ahmad Independent Chief Financial Officer Amir Hafeez Audit Committee Shavez Ahmad (Chairman) Mian Ehsan Ul Haq Kanwar Latfat Ali Khan Human Resource and Remuneration (HR&R) Committee Shavez Ahmad (Chairman) Aamna Taseer Kanwar Latafat Ali Khan Company Secretary Sajjad Ahmad Auditors KPMG Taseer Hadi & Co. Chartered Accountants Legal Advisers M/s. Imtiaz Siddiqui & Associates Bankers Allied Bank Limited Albaraka Bank (Pakistan) Limited Askari Bank Limited Bank Alfalah Limited Faysal Bank Limited Habib Bank Limited KASB Bank Limited MCB Bank Limited National Bank of Pakistan NIB Bank Limited Silkbank Limited Soneri Bank Limited Pair Investment Company Limited The Bank of Punjab United Bank Limited Registrar and Shares Transfer Office Corplink (Pvt.) Limited Wings Arcade, 1-K Commercial Model Town, Lahore Tele: + 92-42-5839182 Registered Office/Head Office 2nd Floor, Pace Shopping Mall Fortress Stadium, Lahore Cantt Lahore, Pakistan (042)-36623005/6/8 Fax: (042) 36623121, 36623122 DIRECTOR’S REPORT TO THE SHAREHOLDERS The Directors of Pace (Pakistan) Limited (“the Company”) take pleasure in presenting to its shareholders the Unconsolidated Interim Financial Statements of the Company for the quarter ended September 30, 2020. Operating Results: During period under review, the sales of the Company showed a decrease of Rs 51.85 million to come at Rs 89.57 million as compared to Rs. -

The Relative Efficiency of Commercial Banks in Pakistan with Respect to Size and Ownership Structure During and After Global Financial Crisis

Journal of Accounting and Finance in Emerging Economies Vol 4, No 2, December 2018 Volume and Issues Obtainable at Center for Sustainability Research and Consultancy Journal of Accounting and Finance in Emerging Economies ISSN: 2519-0318ISSN (E) 2518-8488 Volume 4: Issue 2 December 2018 Journal homepage: publishing.globalcsrc.org/jafee The Relative Efficiency of Commercial Banks in Pakistan with Respect to Size and Ownership Structure During and After Global Financial Crisis 1Allah Bakhsh khan, 2Syed Zulfiqar Ali Shah, 3Muhammad Abbas, 4Qaiser Maqbool khan 1 Asst Professor (Commerce) Bahauddin Zakariya University, Multan, and PhD Scholar at International Islamic University, Islamabad. Pakistan. Email: [email protected] 2 Associate Professor, Faculty of Management Sciences, International Islamic University, Islamabad. Pakistan. 3 Assistant Professor, Air University, Multan Campus. Email: [email protected] 4 PhD Scholar at Department of Commerce, Bahauddin Zakariya University, Multan. Pakistan. Email:[email protected] ARTICLE DETAILS ABSTRACT History Purpose: This study has been carried out to find out the relative efficiency Revised format: Nov2018 of the commercial banks in Pakistan over a five- year period from 2006 to Available Online: Dec 2018 year 2010 using Frontier Approach of efficiency. The commercial banks included in this research paper are public sector banks, privatized banks, Keywords domestic private banks, and foreign banks. In addition to overall efficiency Efficiency, Banks, comparison of the commercial banks, this study has also tested the effect of Financial Intermediation, size and ownership structure of the commercial banks in Pakistan on their Moral Hazard, Data efficiency. Data/Design/Methodology/Approach: Out of 44 banks, 21 commercial JEL Classification: banks have been chosen, which, in terms of deposits, account for about 94 D61,E58,E44,Y10 percent of total deposits of the banking sector (Rs.5,124,308 million) as on December, 2010. -

Annual Report for the Year Ended December 31, 2012 Cover Concept

Annual Report for the year ended December 31, 2012 Cover Concept In today’s challenging environment, we face unprecedented uncertainties across a range of issues. Yet, we still believe that real success lies in always moving ahead; in the relentless pursuit of solutions. At Askari Bank, we believe in leading the way forward. Our fundamental aim is to integrate our offerings with the changing lifestyles of our valued customers – so that we can better assist in their banking needs and also help in shaping their future. On our cover this year, we express our long- standing conviction – of thinking ahead and banking forward. Annual Report of Askari Bank Limited for 2012 Contents 02 21 Years of Banking Unconsolidated Financial Consolidated Financial 04 Vision & Mission Statements of Askari Bank Statements of Askari Bank 06 Our Thinking 08 Products & Services Limited Limited and its Subsidiaries 12 Corporate Philosophy 16 Corporate Information 63 Statement of Compliance 131 Auditors’ Report to the 17 Entity Ratings 65 Review Report to the Members 18 Directors’ Profile Members 132 Consolidated Statement of Financial 22 Board Committees 66 Auditors’ Report to the Position 24 Management Committees Members 133 Consolidated Profit and Loss 26 Notice of 21st Annual General Meeting 68 Unconsolidated Statement of Financial Account 28 Management Position 134 Consolidated Statement of 69 Unconsolidated Profit and Loss Account Comprehensive Income 29 Organogram 70 Unconsolidated Statement of 135 Consolidated Cash Flow 30 Corporate Social Comprehensive -

A Case of NIB Bank Pakistan

SEISENSE Journal of Management Vol. 1. Issue 4. September 2018 DOI: 10.5281/zenodo.1344127 Post-Merger Corporate Performance: A Case of NIB Bank Pakistan. Fariha Batool Hailey College of Banking and Finance, University of the Punjab, Pakistan Misaal Naeem Hailey College of Banking and Finance, University of the Punjab, Pakistan Abstract This study measures whether the mergers generate efficient, trustworthy and wide- ranging capital base for the bank that completely comprised mergers and to what range mergers of banks increase the confidence of the investors, the customers, the shareholders and capacity to finance the real time sector. For the purpose total 9 ratios under profitability ratios and other ratios applied on key financial figures to analyze the selected bank performance. Key figures were taken from the website of the NIB bank. Data was taken from 2004-07 before merger and 2008-12 after the merger. Keywords Merger, Banks, Pakistan, Post Merger Corporate Performance Introduction Over the years the Pakistani banking sector has experienced extraordinary change, in ownership composition, provisions of a number of organizations, along with the depth of operations. These alterations have been prejudiced commonly by challenges invented by deregulation in rules of the financial sector, globalization of processes, procedural inventions and acceptance of managerial and prudential requirements that kneel to global codes. After the declaration by the state bank of Pakistan, that banks in Pakistan should strengthen their minimum capital adequacy ratio in relation to the bank risk weighted assets or set by SBP, the trend of merger and acquisitions that now swept through the banking sector has been started. -

Camels Rating System for Banking Industry in Pakistan

CAMELS RATING SYSTEM FOR BANKING INDUSTRY IN PAKISTAN Does CAMELS system provide similar rating as PACRA system in assessing the performance of banks in Pakistan? Authors: Haseeb Zaman Babar Gul Zeb Supervisor: Catherine Lions Students Umea School of Business Spring Semester 2011 Master Thesis, One-Year, 15hp II Abstract Financial sector of an economy plays an important role in its economic development and prosperity of the country. Banking industry serves as the backbone of the financial sector that accumulates saving from surplus economic units in the form of deposits and provides it to deficit economic units in the form of advances. Banking industry provides support to economy and industries in specific in the time of recessions and economic crisis. But when banks are at the heart of economic recession or banks are the cause of financial crisis like the recent past financial crisis 2007-09, it makes the situation worst for economic recovery. So it is of great importance to keenly observe the performance of the banks and their compliance with the regulatory requirements. Performance of the banks is measured at two levels, one is at the management and regulatory level of the banks and another is at external rating agencies. Purpose of regulatory and supervisory rating systems is to measure the bank performance at internal level and its compliance with regulatory requirements to keep the bank on right track. These ratings are highly confidential and are only available to the bank management. External credit rating agencies examine and evaluate the banks and issue ratings for the general public and investors in particulars. -

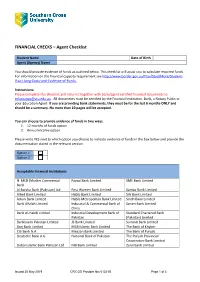

FINANCIAL CHECKS – Agent Checklist

FINANCIAL CHECKS – Agent Checklist Student Name Date of Birth Agent (Agency) Name You should provide evidence of funds as outlined below. This checklist will assist you to calculate required funds. For information on the financial capacity requirement see http://www.border.gov.au/Trav/Stud/More/Student- Visa-Living-Costs-and-Evidence-of-Funds. Instructions: Please complete this checklist and return it together with bank/agent certified financial documents to [email protected] . All documents must be certified by the Financial Institution, Bank, a Notary Public or your Education Agent. If you are providing bank statements, they must be for the last 6 months ONLY and should be a summary. No more than 10 pages will be accepted. You can choose to provide evidence of funds in two ways. 1. 12 months of funds option 2. Annual income option Please write YES next to which option you choose to indicate evidence of funds in the box below and provide the documentation stated in the relevant section. Option 1 Option 2 Acceptable Financial Institutions N MCB (Muslim Commercial Faysal Bank Limited SME Bank Limited Bank Al Baraka Bank (Pakistan) Ltd First Women Bank Limited Samba Bank Limited Allied Bank Limited Habib Bank Limited Silk Bank Limited Askari Bank Limited Habib Metropolitan Bank Limited Sindh Bank Limited Bank Alfalah Limited Industrial & Commercial Bank of Soneri Bank Limited China Bank Al-Habib Limited Industrial Development Bank of Standard Chartered Bank Pakistan (Pakistan) Limited BankIslami Pakistan Limited JS Bank Limited Summit -

Audited Financial Statements 2007

Askari Bank Limited Financial Statements 2007 53 Financial Statements of Askari Bank Limited (formerly Askari Commercial Bank Limited) for the year ended December 31, 2007 Askari Bank Limited Annual Report 2007 54 Financial Statements 2007 55 Statement of Compliance with the Code of Corporate Governance for the year ended December 31, 2007 This statement is being presented to comply with the Prudential Regulation No.XXIX, responsibilities of the Board of Directors, issued vide BSD Circular No.15, dated June 13, 2002 and the Code of Corporate Governance as contained in Listing Regulations of the stock exchanges where the Bank’s shares are listed for the purpose of establishing a framework of good governance, whereby a listed company is managed in compliance with the best practices of corporate governance. The Bank has applied the principles contained in the Code in the following manner: 1. The Bank encourages representation of independent non-executive directors and directors representing minority interests on its Board of Directors. At present the Board includes at least 11 non-executive Directors of which 3 independent Directors represent minority shareholders. 2. The Directors have confirmed that none of them is serving as a director in more than ten listed companies, including Askari Bank Limited (formerly, Askari Commercial Bank Limited), except Mr. Tariq Iqbal Khan who has been exempted for the purpose of this clause by the Securities and Exchange Commission of Pakistan (SECP). 3. All the resident directors of the Bank are registered as taxpayers and none of them has defaulted in payment of any loan to a banking company, a DFI or an NBFI or, being a member of a stock exchange, has been declared as a defaulter by that stock exchange.