Audited Financial Statements 2007

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Askari Bank Limited List of Shareholders (W/Out Cnic) As of December 31, 2017

ASKARI BANK LIMITED LIST OF SHAREHOLDERS (W/OUT CNIC) AS OF DECEMBER 31, 2017 S. NO. FOLIO NO. NAME OF SHAREHOLDERS ADDRESSES OF THE SHAREHOLDERS NO. OF SHARES 1 9 MR. MOHAMMAD SAEED KHAN 65, SCHOOL ROAD, F-7/4, ISLAMABAD. 336 2 10 MR. SHAHID HAFIZ AZMI 17/1 6TH GIZRI LANE, DEFENCE HOUSING AUTHORITY, PHASE-4, KARACHI. 3280 3 15 MR. SALEEM MIAN 344/7, ROSHAN MANSION, THATHAI COMPOUND, M.A. JINNAH ROAD, KARACHI. 439 4 21 MS. HINA SHEHZAD C/O MUHAMMAD ASIF THE BUREWALA TEXTILE MILLS LTD 1ST FLOOR, DAWOOD CENTRE, M.T. KHAN ROAD, P.O. 10426, KARACHI. 470 5 42 MR. M. RAFIQUE B.R.1/27, 1ST FLOOR, JAFFRY CHOWK, KHARADHAR, KARACHI. 9382 6 49 MR. JAN MOHAMMED H.NO. M.B.6-1728/733, RASHIDABAD, BILDIA TOWN, MAHAJIR CAMP, KARACHI. 557 7 55 MR. RAFIQ UR REHMAN PSIB PRIVATE LIMITED, 17-B, PAK CHAMBERS, WEST WHARF ROAD, KARACHI. 305 8 57 MR. MUHAMMAD SHUAIB AKHUNZADA 262, SHAMI ROAD, PESHAWAR CANTT. 1919 9 64 MR. TAUHEED JAN ROOM NO.435, BLOCK-A, PAK SECRETARIAT, ISLAMABAD. 8530 10 66 MS. NAUREEN FAROOQ KHAN 90, MARGALA ROAD, F-8/2, ISLAMABAD. 5945 11 67 MR. ERSHAD AHMED JAN C/O BANK OF AMERICA, BLUE AREA, ISLAMABAD. 2878 12 68 MR. WASEEM AHMED HOUSE NO.485, STREET NO.17, CHAKLALA SCHEME-III, RAWALPINDI. 5945 13 71 MS. SHAMEEM QUAVI SIDDIQUI 112/1, 13TH STREET, PHASE-VI, DEFENCE HOUSING AUTHORITY, KARACHI-75500. 2695 14 74 MS. YAZDANI BEGUM HOUSE NO.A-75, BLOCK-13, GULSHAN-E-IQBAL, KARACHI. -

12. BANKING 12.1 Scheduled Banks Operating in Pakistan Pakistani Banks

12. BANKING 12.1 Scheduled Banks Operating in Pakistan Pakistani Banks Public Sector Banks Nationalized Banks 1. First Women Bank Limited 2. National Bank of Pakistan Specialized Banks 1. Industrial Development Bank of Pakistan (IDBP) 2. Punjab Provincial Co-operative Bank Limited (PPCB) 3. Zarai Traqiati Bank Limited 4. SME Bank Ltd. Provincial Banks 1. The Bank of Khyber 2. The Bank of Punjab Private Domestic Banks Privatized Bank 1. Allied Bank of Pakistan Limited 2. Muslim Commercial Bank Limited 3. United Bank Limited 4. Habib Bank Ltd. Private Banks 1. Askari Commercial Bank Limited 2. Bank Al-Falah Ltd. 3. Bank Al-Habib Ltd. 4. Bolan Bank Ltd. 5. Faysal Bank Ltd. 6. KASB Bank Limited 7. Meezan Bank Ltd. 8. Metropolitan Bank Ltd 9. Prime Commercial Bank Ltd. 10. PICIC Commercial Bank Ltd. 11. Saudi-Pak Commercial Bank Limited 12. Soneri Bank Ltd. 13. Union Bank Ltd. Contd. 139 12.1 Scheduled Banks Operating in Pakistan Private Banks 14. Crescent Commercial Bank Ltd. 15. Dawood bank Ltd. 16. NDLC - IFIC Bank Ltd. Foreign Banks 1. ABN AMRO Bank NV 2. Al-Baraka Islamic Bank BSC 3. American Express Bank Ltd. 4. Citi Bank NA 5. Deutsche Bank AE 6. Habib Bank AG Zurich 7. Oman International Bank SAOG 8. Rupali Bank Ltd 9. Standard Chartered Bank Ltd. 10. The Bank of Tokyo-Mitsubishi Ltd. 11. The Hong Kong & Shanghai Banking Corporation Ltd. Source: SBP Note: Banks operating as on 30th June, 2004 140 12.2 State Bank of Pakistan - Assets of the Issue Department (Million Rupees) Last Day of June Particulars 2003 2004 2005 Total Assets 522,891.0 611,903.7 705,865.7 1. -

S# BRANCH CODE BRANCH NAME CITY ADDRESS 1 24 Abbottabad

BRANCH S# BRANCH NAME CITY ADDRESS CODE 1 24 Abbottabad Abbottabad Mansera Road Abbottabad 2 312 Sarwar Mall Abbottabad Sarwar Mall, Mansehra Road Abbottabad 3 345 Jinnahabad Abbottabad PMA Link Road, Jinnahabad Abbottabad 4 131 Kamra Attock Cantonment Board Mini Plaza G. T. Road Kamra. 5 197 Attock City Branch Attock Ahmad Plaza Opposite Railway Park Pleader Lane Attock City 6 25 Bahawalpur Bahawalpur 1 - Noor Mahal Road Bahawalpur 7 261 Bahawalpur Cantt Bahawalpur Al-Mohafiz Shopping Complex, Pelican Road, Opposite CMH, Bahawalpur Cantt 8 251 Bhakkar Bhakkar Al-Qaim Plaza, Chisti Chowk, Jhang Road, Bhakkar 9 161 D.G Khan Dera Ghazi Khan Jampur Road Dera Ghazi Khan 10 69 D.I.Khan Dera Ismail Khan Kaif Gulbahar Building A. Q. Khan. Chowk Circular Road D. I. Khan 11 9 Faisalabad Main Faisalabad Mezan Executive Tower 4 Liaqat Road Faisalabad 12 50 Peoples Colony Faisalabad Peoples Colony Faisalabad 13 142 Satyana Road Faisalabad 585-I Block B People's Colony #1 Satayana Road Faisalabad 14 244 Susan Road Faisalabad Plot # 291, East Susan Road, Faisalabad 15 241 Ghari Habibullah Ghari Habibullah Kashmir Road, Ghari Habibullah, Tehsil Balakot, District Mansehra 16 12 G.T. Road Gujranwala Opposite General Bus Stand G.T. Road Gujranwala 17 172 Gujranwala Cantt Gujranwala Kent Plaza Quide-e-Azam Avenue Gujranwala Cantt. 18 123 Kharian Gujrat Raza Building Main G.T. Road Kharian 19 125 Haripur Haripur G. T. Road Shahrah-e-Hazara Haripur 20 344 Hassan abdal Hassan Abdal Near Lari Adda, Hassanabdal, District Attock 21 216 Hattar Hattar -

MONEY and CREDIT HIGHLIGHTS Stock As on End June (Rs Million) Items / Years 2006 2007 A

MONEY AND CREDIT HIGHLIGHTS Stock as on end June (Rs million) Items / Years 2006 2007 A. Components of Monetary Assets Currency in Circulation 740,390 840,181 Demand Deposits 1,085,665 2,643,778 Other Deposits 4,931 7,012 (M1)a 1,830,986 3,490,971 Time Deposits 1,380,418 366,872 Foreign Currency Deposits 195,501 207,312 Total Monetary Assets (M2)b 3,406,905 4,065,155 I. Public Sector Borrowing (Net) 833,686 926,530 - Budgetary Support 708,037 810,053 - Commodity Operation 107,762 98,552 - Effect of Zakat etc. (14,308) (14,269) - Privatization proceeds 37,657 37,657 II. Non-Government Sector 2,190,769 2,576,474 - Autonomous Bodies 36,979 58,148 - Private Sector (Net) 2,153,790 2,518,326 a. Private Sector 2,113,890 2,479,608 b. Public Sector Corporation 47,237 46,010 c. PSEs Special Accounts Debt (23,225) (23,478) Repayment with SBP d. Organization Institution 15,889 16,187 (SBP credit to NBFIs) III. Other Item (Net) (327,346) (422,223) IV. Domestic Credit 2,696,564 3,080,263 V. Foreign Assets (Net) 710,341 984,892 VI. Monetary Assets (M2)b 3,406,905 4,065,155 TABLE 5.1 COMPONENTS OF MONETARY ASSETS (Rs million) Stocks at end June (a) 2000 2001 2002 2003 2004 2005 2006 2007 (P) 1. Currency Issued 376,997 396,548 462,095 527,557 617,508 712,480 791,834 901,401 2. Currency held by SBP 1,851 1,905 1,865 2,565 2,960 3,107 3,005 3,148 3. -

Faysal Funds

Accounts forthe Quarter Ended September 30, 2008 FAYSAL BALANCED GROWTH FUND The Faysal Balanced Growth Fund (FBGF) is an open-ended mutual fund. The units of FBGF are listed on the Karachi Stock Exchange and were initially offered to the public on April 19, 2004. FBGFseeks to provide long-term capital appreciation with a conservative risk profile and a medium to long-term investment horizon. FBGF's investment philosophy is to provide stable returns by investing in a portfolio balanced between equities and fixed income instruments. Fund Information Management Company Faysal Asset Management Limited Board of Directors of the Management Company Mr. Khalid Siddiq Tirmizey, Chairman Mr. Salman Haider Sheikh, Chief Executive Officer Mr. Sanaullah Qureshi, Director Mr. Syed Majid AIi, Director Mr. Feroz Rizvi, Director CFO of the Management Company Mr. Abdul Razzak Usman Company Secretary of the Management Company Mr. M. Siddique Memon Audit Committee Mr. Feroz Rizvi, Chairman Mr. Sanaullah Qureshi, Member Mr. Syed Majid Ali, Member Trustee Central Depository Company of Pakistan Limited Suit #. M-13, 16, Mezzanine Floor, Progressive Plaza, Beaumont Road, Near PIDC House, Karachi. Bankers to the Fund Faysal Bank Limited MCB Bank Limited Bank Alfalah Limited Atlas Bank Limited The Bank of Punjab Auditors Ford Rhodes Sidat Hyder & Co., Chartered Accountants Legal Advisor Mohsin Tayebely & Co., 2nd Floor, Dime Centre, BC-4, Block-9, KDA-5, Clifton, Karachi. Registrars Gangjees Registrar Services (Pvt) Limited Room # 506, 5th Floor, Clifton Centre, Kehkashan Clifton - Karachi. Distributors Access Financial Services (Pvt.) Ltd. AKD Securities (Pvt.) Limited Faysal Asset Management Limited Faysal Bank Limited PICIC Commercial Bank Limited Reliance Financial Products (Pvt.) Limited Invest Capital & Securities (Pvt.) Limited Flow(Private) Limited IGI Investment Bank Limited Pak Oman Investment Bank Limited Alfalah Securities (Pvt) Limited JS Global Capital Limited t"''' e , FAYSAL BALANCED ~ . -

Prospectus, Especially the Risk Factors Given at Para 4.11 of This Prospectus Before Making Any Investment Decision

ADVICE FOR INVESTORS INVESTORS ARE STRONGLY ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS PROSPECTUS, ESPECIALLY THE RISK FACTORS GIVEN AT PARA 4.11 OF THIS PROSPECTUS BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FALSE AND FICTITIOUS APPLICATIONS ARE PROHIBITED AND SUCH APPLICATIONS’ MONEY MAY BE FORFEITED UNDER SECTION 87(8) OF THE SECURITIES ACT, 2015. SONERI BANK LIMITED PROSPECTUS THE ISSUE SIZE OF FULLY PAID UP, RATED, LISTED, PERPETUAL, UNSECURED, SUBORDINATED, NON-CUMULATIVE AND CONTINGENT CONVERTIBLE DEBT INSTRUMENTS IN THE NATURE OF TERM FINANCE CERTIFICATES (“TFCS”) IS PKR 4,000 MILLION, OUT OF WHICH TFCS OF PKR 3,600 MILLION (90% OF ISSUE SIZE) ARE ISSUED TO THE PRE-IPO INVESTORS AND PKR 400 MILLION (10% OF ISSUE SIZE) ARE BEING OFFERED TO THE GENERAL PUBLIC BY WAY OF INITIAL PUBLIC OFFER THROUGH THIS PROSPECTUS RATE OF RETURN: PERPETUAL INSTRUMENT @ 6 MONTH KIBOR* (ASK SIDE) PLUS 2.00% P.A INSTRUMENT RATING: A (SINGLE A) BY THE PAKISTAN CREDIT RATING COMPANY LIMITED LONG TERM ENTITY RATING: “AA-” (DOUBLE A MINUS) SHORT TERM ENTITY RATING: “A1+” (A ONE PLUS) BY THE PAKISTAN CREDIT RATING AGENCY LIMITED AS PER PSX’S LISTING OF COMPANIES AND SECURITIES REGULATIONS, THE DRAFT PROSPECTUS WAS PLACED ON PSX’S WEBSITE, FOR SEEKING PUBLIC COMMENTS, FOR SEVEN (7) WORKING DAYS STARTING FROM OCTOBER 18, 2018 TO OCTOBER 26, 2018. NO COMMENTS HAVE BEEN RECEIVED ON THE DRAFT PROSPECTUS. DATE OF PUBLIC SUBSCRIPTION: FROM DECEMBER 5, 2018 TO DECEMBER 6, 2018 (FROM: 9:00 AM TO 5:00 PM) (BOTH DAYS INCLUSIVE) CONSULTANT TO THE ISSUE BANKERS TO THE ISSUE (RETAIL PORTION) Allied Bank Limited Askari Bank Limited Bank Alfalah Limited** Bank Al Habib Limited Faysal Bank Limited Habib Metropolitan Bank Limited JS Bank Limited MCB Bank Limited Silk Bank Limited Soneri Bank Limited United Bank Limited** **In order to facilitate investors, United Bank Limited (“UBL”) and Bank Alfalah Limited (“BAFL”) are providing the facility of electronic submission of application (e‐IPO) to their account holders. -

IBFT- Account Number Formats

IBFT- Account Number Formats Allied Bank Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 9 Digit Account Number, AAAAAAAAAAAAAAAA = 16 Digit Account Number Apna Microfinance Bank Please enter Apna Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 12 Digits Askari Bank Please enter Askari Bank Account Number by following the layout below: Total Digits of Bank Account Number: 14 Digits Format Example: BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Branchless Banking Account # Always consist of 11 digits Mobile Number. Al-Baraka Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Bank Alfalah Please enter Bank Alfalah Account Number by following the layout below: Conventional A/C#: Total Digits of Account Number: 14 Format Example: BBBBAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Islamic A/C#: Total Digits of Account Number: 18 Digit Format Example: BBBBAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAAAAAA = 14 Digit Account Number Branchless Banking Account # : Always consist of 11 digits Mobile Number. Bank Al-Habib Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digit Format -

18-12-2018.Pdf

SUPREME COURT OF PAKISTAN AND PRIME MINISTER OF PAKISTAN'S DIAMER BHASHA AND MOHMAND DAM FUND ACCOUNT LIST OF DONOR FOR 19 DEC-18 RECEIPT Bank Depositor Name Amount AL BARAKA BANK (PAKISTAN) LTD MUHAMMAD FAROOQ 200 AL BARAKA BANK (PAKISTAN) LTD Total 200 Allied Bank Limited JAVID AHMED 100,000 Allied Bank Limited TARIQ 50,000 Allied Bank Limited MNA FARRUKH KHAN 50,000 Allied Bank Limited GHULAM MUHAMMAD 35,000 Allied Bank Limited KHALIDA MEMON 30,000 Allied Bank Limited AASIM 25,000 Allied Bank Limited IMRAN 20,000 Allied Bank Limited AHSAN MEHMOOD CHUGHTAI 20,000 Allied Bank Limited QASWAR AZAM 20,000 Allied Bank Limited NADIA IQBAL DAR 20,000 Allied Bank Limited MIRZA ADEED ALI BAIG 20,000 Allied Bank Limited SHAHRYAR 15,000 Allied Bank Limited SAADSHARIF 13,180 Allied Bank Limited muhammad ud din 13,000 Allied Bank Limited RASHID 11,000 Allied Bank Limited AMIR USMAN 10,000 Allied Bank Limited M IMRAN 10,000 Allied Bank Limited ABDUL HAMEED KHAN 10,000 Allied Bank Limited SAHIR MEHMOOD 9,200 Allied Bank Limited MUHAMMAD AYAZ 6,500 Allied Bank Limited KALIM BIN RAFIQUE 6,000 Allied Bank Limited MUHAMMAD ASGHAR 5,000 Allied Bank Limited adnan 5,000 Allied Bank Limited TOBA MALIK 5,000 Allied Bank Limited MUNAWARSULTANA 5,000 Allied Bank Limited ASHRAF ALI 5,000 Allied Bank Limited BILAL 3,500 Allied Bank Limited ABDUL GHAFOOR 3,000 Allied Bank Limited SHAHIDHUSSAINQURESHI 3,000 Allied Bank Limited SAEEDA NASREEN 3,000 Allied Bank Limited ANSAR MEHMOOOD 2,000 Allied Bank Limited AFTAB SAB 2,000 Allied Bank Limited IDRESS 2,000 Allied -

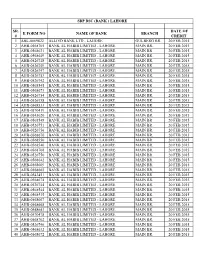

Sr. # E Form No Name of Bank Branch Date of Credit 1 Abl-0069822 Allied Bank

SBP BSC (BANK ) LAHORE SR. DATE OF E FORM NO NAME OF BANK BRANCH # CREDIT 1 ABL-0069822 ALLIED BANK LTD - LAHORE GULBERG BR. 20 FEB 2015 2 AHB-0568705 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 3 AHB-0568631 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 4 AHB-0568649 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 5 AHB-0526748 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 6 AHB-0526749 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 7 AHB-0526747 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 8 AHB-0526753 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 9 AHB-0526742 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 10 AHB-0568545 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 11 AHB-0568673 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 12 AHB-0526754 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 13 AHB-0526758 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 14 AHB-0568533 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 15 AHB-0570419 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 16 AHB-0543020 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 17 AHB-0568548 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 18 AHB-0526751 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 19 AHB-0526756 BANK AL HABIB LIMITED - LAHORE MAIN BR. 20 FEB 2015 20 AHB-0568670 BANK AL HABIB LIMITED - LAHORE MAIN BR. -

Lt Gen Tariq Khan, HI (M) (Retd), Is Chief Executive & Managing

Lt Gen Tariq Khan, HI (M) (Retd) Lt Gen Tariq Khan, HI (M) (Retd), is Chief Executive & Managing Director of Fauji Fertilizer Company Limited, FFC Energy Limited and Fauji Fresh n Freeze Limited and also holds directorship on the Boards of following: Fauji Fertilizer Bin Qasim Limited Askari Bank Limited Fauji Foods Limited Philip Morris (Pakistan) Limited Fauji Meat Limited FFBL Foods Limited FFBL Power Company Limited Thar Energy Limited Pakistan Maroc Phosphore S.A. He is Chairman of Sona Welfare Foundation (SWF) and Fertilizer Manufacturers of Pakistan Advisory Council (FMPAC) and member of the Board of Governors of Foundation University, Islamabad. The General was commissioned in Pakistan Army in April1977 with the coveted Sword of Honour. During his illustrious service in the Army, he had been employed on various prestigious command, staff and instructional assignments including command of a Strike Corps. He is a graduate of Command and Staff College Quetta and National Defence University Islamabad. He also holds Master Degree in War Studies. He has served on the faculty of Command and Staff College Quetta and National Defence University Islamabad. Since his retirement, he is on the honorary faculty of renowned institutions including National Defence University as a senior mentor. The General possesses vast experience as adviser to the leading corporate entities. He has been awarded Hilal-e-Imtiaz (Military) and is also the first Pakistan Army General who has been conferred upon the U.S ‘Legion of Merit’ by the U.S Government for his meritorious services as a senior representative at U.S CENTCOM in Tampa, Florida. -

Annual REPORT 2011 SILKBANKT

ANNUAl REPORT 2011 SILKBANKT Notice of AGM & Auditors' Review 35 Auditors' Report 39 Financial Statements 43 Six Years' Rnancial Highlights 44 Statement of Financial Position 50 Profit & Loss Account 51 Statement of Comprehensive Income 52 Vision & Mission 02 Cash Row Statement 53 Message from Chairman 04 Statement of Changes in Equity 54 President & CEO's Review 06 Notes to the Financial Statements 55 Senior Management Committee 09 Statement of Written-off Loans 100 Profiles of Board of Directors 13 Achievements & CSR 103 Corporate Information 17 Additional Shareholders' Information 110 Directors' Report 21 Pattern of Share Holdings CDC & Physical 111 Statement of Compliance with 29 Branch Network 114 the Code of Corporate Governance Foreign Correspondents 116 & Statement of Internal Control Proxy Form 119 To be the leader in premier banking, trusted by customers for accessibility, service and innovation; be an employer of choice creating value for all stakeholders In the aftermath of the economic slowdown since 2008, Non-Performing Loans (NPLs) have dampened the profitability dynamics of commercial banks. I am pleased to advise you that contrary to the banking industry trend, your Bank managed to register a significant reduction in NPLs, in each consecutive year since the takeover by the new management. An NPL reduction by the Special Assets Management team of Rs. 3.398 billion and a Provision Reversal of Rs. 1.829 billion was recorded for the year 2011. The Real Estate Asset Management team (REAM) also supported the Special Assets Management team by successfully selling off various properties held as OREO (Other Real Estate Owned), during the year. -

WHY SILK? 111-007-455 2009 Inspiration for the Name Silkbank Comes from the Silk Route - a Trade Corridor Connecting Asia to Europe and the Rest of the World

Silkbank Building ANNUAL I.I. Chundrigar Road, Karachi REPORT www.silkbank.com.pk WHY SILK? 111-007-455 2009 Inspiration for the name Silkbank comes from the Silk Route - a trade corridor connecting Asia to Europe and the rest of the world. Silk, known for its distinctive properties and characteristics, symbolizes Silkbank’s brand beliefs. Premium & Upscale Silk is known for class and premium quality. Silkbank is positioned as an upscale bank providing its customers with premium banking experience. Talent & Innovation Silk embodies talent and timeless innovation. Silkbank promises its customers innovative products delivered through talented staff. Strong & Reliable Silk is amongst the strongest fibres known to mankind. Silkbank derives its strength from its strong international institutional sponsors giving it credibility and reliability. Dependable Silk through the times has held its value. Silkbank driven by a team of professionals provides an optimal experience that you can depend on. Contents Vision & Mission 02 Chairman's Message 03 Silkbank Products President & CEO's Message 05 Senior Management Committee 07 Assets Corporate Information 11 Directors’ Report 15 Statement of Compliance with the Code of Liabilities Corporate Governance 23 Statement of Internal Control 25 Notice of AGM 29 Review Report to the Members on Statement of Compliance with the Best Practices of Code of Corporate Governance 30 Independent Auditors’ Report 33 Balance Sheet 37 Profit and Loss Account 38 Statement of Comprehensive Income 39 Cash Flow Statement