The $1 Billion Question: Do the Tax

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pocket Calendar & Stakes Schedule

2020-2021 POCKET SCHEDULE 149th THOROUGHBRED RACING SEASON NOVEMBER 2020 DECEMBER 2020 JANUARY 2021 SS M T W TH F SS SS MM TT WW TH F S S SS M TT WW THTH FF SS * * * * * * * * * 3 4 5 1 2 * * * * * * * 6 * * * 10 11 12 3 * * 6 7 8 9 * * * * * * * 13 * * 16 17 18 19 10 * * * 14 15 16 * * * * 26 27 28 20 * * * * * 26 17 18 * * 21 22 23 29 * 27 28 * * 31 24 * * * 28 29 30 31 FEBRUARY 2021 MARCH 2021 PROGRAMMING S M T W TH F S S M T TH F S NOVEMBER 26 S M T W TH F S S M T W TH F S THANKSGIVING CLASSIC DECEMBER 12 * * 3 4 5 6 * * * 4 5 6 LOUISIANA CHAMPIONS DAY (LA) 7 * * * 11 12 13 7 * * * 11 12 13 DECEMBER 19 SANTA SUPER SATURDAY * 15 16 * 18 19 20 14 * * * 18 19 20 JANUARY 16 ROAD TO THE DERBY KICKOFF DAY 21 * * * 25 26 27 21 * * * 25 26 27 FEBUARY 13 LOUISIANA DERBY PREVIEW DAY 28 28 * * * MARCH 20 LOUISIANA DERBY DAY POST TIME 1PM UNLESS STATED BELOW: POST TIME - 11:00 AM POST TIME - 12:00 PM \ GRADED STAKES DAYS (DEC. 12, JAN. 16, FEB. 13 & MAR. 20) POST TIMES ARE SUBJECT TO CHANGE. 2020-2021 THOROUGHBRED RACING SEASON STAKES SCHEDULE DATE PURSE STAKES RUNNING CONDITIONS DISTANCE / SURFACE NOV 26 125,000 THANKSGIVING CLASSIC 96th 3YO/UP 6 FURLONGS DEC 5 75,000 PAN ZARETA STAKES 55th 3YO/UP FILLIES & MARES 5 1/2 FURLONGS* (T) DEC 11 50,000 THE MAGIC CITY CLASSIC 10th 3YO/UP ONE MILE DEC 12 LOUISIANA CHAMPIONS DAY (LA) 100,000 LA CHAMPIONS DAY QH JUVENILE STAKES - GRADE II 30th 2YO 350 YARDS 100,000 LA CHAMPIONS DAY QH DERBY - GRADE III 30th 3YO 400 YARDS 100,000 LA CHAMPIONS DAY QH CLASSIC - GRADE II 30th 4YO/UP 440 YARDS 100,000 LA CHAMPIONS -

Midwest Non-Deal Roadshow

Midwest Non-Deal Roadshow Prepared For: Investor Relations (NASDAQ: CHDN) October 7-8, 2014 Bill Mudd, President and CFO Mike Anderson, VP Finance & IR / Treasurer Forward-Looking Statements This document contains various “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The Private Securities Litigation Reform Act of 1995 (the “Act”) provides certain “safe harbor” provisions for forward-looking statements. All forward-looking statements are made pursuant to the Act. The reader is cautioned that such forward-looking statements are based on information available at the time and/or management’s good faith belief with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the statements. Forward-looking statements speak only as of the date the statement was made. We assume no obligation to update forward-looking information to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information. Forward-looking statements are typically identified by the use of terms such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “predict,” “project,” “hope,” “should,” “will,” and similar words, although some forward-looking statements are expressed differently. Although we believe that the expectations reflected in such forward-looking statements are reasonable, -

The Big Easy and All That Jazz

©2014 JCO, Inc. May not be distributed without permission. www.jco-online.com The Big Easy and All that Jazz fter Hurricane Katrina forced a change of A venue to Las Vegas in 2006, the AAO is finally returning to New Orleans April 25-29. While parts of the city have been slow to recover from the disastrous flooding, the main draws for tourists—music, cuisine, and architecture—are thriving. With its unique blend of European, Caribbean, and Southern cultures and styles, New Orleans remains a destination city for travelers from around the United States and abroad. Transportation and Weather The renovated Ernest N. Morial Convention Center opened a new grand entrance and Great Hall in 2013. Its location in the Central Business District is convenient to both the French Quarter Bourbon Street in the French Quarter at night. Photo © Jorg Hackemann, Dreamstime.com. to the north and the Garden District to the south. Museums, galleries, and other attractions, as well as several of the convention hotels, are within Tours walking distance, as is the Riverfront Streetcar line that travels along the Mississippi into the Get to know popular attractions in the city French Quarter. center by using the hop-on-hop-off double-decker Louis Armstrong International Airport is City Sightseeing buses, which make the rounds about 15 miles from the city center. A shuttle with of a dozen attractions and convenient locations service to many hotels is $20 one-way; taxi fares every 30 minutes (daily and weekly passes are are about $35 from the airport, although fares will available). -

Living Blues 2021 Festival Guide

Compiled by Melanie Young Specific dates are provided where possible. However, some festivals had not set their 2021 dates at press time. Due to COVID-19, some dates are tentative. Please contact the festivals directly for the latest information. You can also view this list year-round at www.LivingBlues.com. Living Blues Festival Guide ALABAMA Foley BBQ & Blues Cook-Off March 13, 2021 Blues, Bikes & BBQ Festival Juneau Jazz & Classics Heritage Park TBA TBA Foley, Alabama Alabama International Dragway Juneau, Alaska 251.943.5590 2021Steele, Alabama 907.463.3378 www.foleybbqandblues.net www.bluesbikesbbqfestival.eventbrite.com jazzandclassics.org W.C. Handy Music Festival Johnny Shines Blues Festival Spenard Jazz Fest July 16-27, 2021 TBA TBA Florence, Alabama McAbee Activity Center Anchorage, Alaska 256.766.7642 Tuscaloosa, Alabama spenardjazzfest.org wchandymusicfestival.com 205.887.6859 23rd Annual Gulf Coast Ethnic & Heritage Jazz Black Belt Folk Roots Festival ARIZONA Festival TBA Chandler Jazz Festival July 30-August 1, 2021 Historic Greene County Courthouse Square Mobile, Alabama April 8-10, 2021 Eutaw, Alabama Chandler, Arizona 251.478.4027 205.372.0525 gcehjazzfest.org 480.782.2000 blackbeltfolkrootsfestival.weebly.com chandleraz.gov/special-events Spring Fling Cruise 2021 Alabama Blues Week October 3-10, 2021 Woodystock Blues Festival TBA May 8-9, 2021 Carnival Glory Cruise from New Orleans, Louisiana Tuscaloosa, Alabama to Montego Bay, Jamaica, Grand Cayman Islands, Davis Camp Park 205.752.6263 Bullhead City, Arizona and Cozumel, -

5555 Bullard Ave New Orleans, LA Investment Advisors

JDS Real Estate Services Bullard Corporate Center 5555 Bullard Ave New Orleans, LA Investment Advisors ENRI PINTO VP of National Sales CONFIDENTIALITY Miami Office AND DISCLOSURE Phone: 305-924-3094 [email protected] The information contained in the following Offering Memorandum (“OM”) is proprietary and strictly confidential. It is intended to be reviewed only by the party receiving it from Apex Capital Realty and should not be made available to any other person, entity, or affiliates without the written consent of Apex Capital Realty. By taking possession of and reviewing STEVEN VANNI the information contained herein the recipient agrees to hold and treat all such information Managing Director in the strictest confidence. The recipient further agrees that recipient will not photocopy or Miami Office duplicate any part of the offering memorandum. If you have no interest in the subject prop- Phone: 305-989-7854 erty at this time, please return this offering memorandum to Apex Capital Realty. This OM has been prepared to provide summary, unverified information to prospective purchasers, [email protected] and to establish only a preliminary level of interest in the subject property. The information contained herein is not a substitute for a thorough due diligence investigation. Apex Capital Realty has not made any investigation, and makes no warranty or representation, with respect to the income or expenses for the subject property, the future projected financial per- TONY SOTO formance of the property, the size and square footage of the property, the physical condition of the improvements thereon, or the financial condition or business prospects of any tenant, Commercial Advisor or any tenant’s plans or intentions to continue its occupancy of the subject property. -

2017 Continuing Disclosure Report

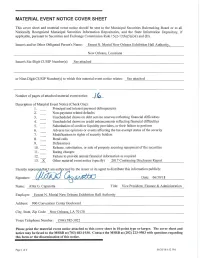

MATERIAL EVENT NOTICE COVER SHEET This cover sheet and material event notice should be sent to the Municipal Securities Rulemaking Board or to all Nationally Recognized Municipal Securities Information Repositories, and the State Information Depository, if applicable, pursuant to Securities and Exchange Commission Rule 15c2-12(b)(5)(i)8) and (D). Issuer's and/or Other Obligated Person's Name: Ernest N. Moria! New Orleans Exhibition Hall Authority, New Orleans, Louisiana Issuer's Six-Digit CUSIP Number(s): See attached --------------------------------------------------------- or Nine-Digit CUSIP Number(s) to which this material event notice relates: ---=-S-=-ee=--=att=ac::..:.h.:...:e-=d______ _____________ Number of pages of attached material event notice: ~ Description of Material Event Notice (Check One): 1. Principal and interest payment delinquencies 2. Non-payment related defaults 3. Unscheduled draws on debt service reserves reflecting financial difficulties 4. Unscheduled draws on credit enhancements reflecting financial difficulties 5. Substitution of credit or liquidity providers, or their failure to perform 6. Adverse tax opinions or events affecting the tax-exempt status of the security 7. Modifications to ri ghts of security holders 8. Bond calls 9. Defeasances 10. Release, substitution, or sale of property securing repayment of the securities 11. Rating changes 12. Failure to provide annual financial information as required 13. X Other material event notice (spec ifY) 20 17 Continuing Disclosure Report that,. I am authorized by the issuer or its agent to distribute this information publicly: Signature: Date: 06/3 0118 Name: Alita G. Caparotta Title: Vice President, Finance & Administration Employer: Ernest N. Moria! New Orleans Exhibition Hall Authority Address: 900 Convention Center Boulevard City, State, Zip Code New Orleans, LA 701 30 Voice Telephone Number: ----'-'(5'--'0'--'4.L)-=-- 5-=--82__ --=--3-=--02 _2_____________ ___ ___ _______ Please print the material event notice attached to this cover sheet in 10-point type or larger. -

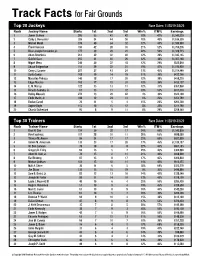

Track Facts for Fair Grounds

Track Facts for Fair Grounds Top 20 Jockeys Race Dates: 11/28/19-3/5/20 Rank Jockey Name Starts 1st 2nd 3rd Win% ITM% Earnings 1 James Graham 295 55 42 42 18% 47% $1,543,020 2 Colby J. Hernandez 326 54 44 50 16% 45% $1,636,320 3 Mitchell Murrill 379 49 64 52 12% 43% $1,590,880 4 Florent Geroux 194 42 28 31 21% 52% $1,750,236 5 Brian Joseph Hernandez, Jr. 177 39 29 21 22% 50% $1,328,715 6 Adam Beschizza 261 32 32 40 12% 39% $1,045,165 7 Gabriel Saez 255 31 40 26 12% 38% $1,007,148 8 Miguel Mena 240 30 22 18 12% 29% $832,810 9 Shaun Bridgmohan 151 29 22 21 19% 47% $1,193,920 10 Corey J. Lanerie 207 27 43 24 13% 45% $1,014,440 11 Santo Sanjur 168 19 14 19 11% 30% $422,700 12 Marcelino Pedroza 140 18 17 20 12% 39% $459,220 13 Edgar Morales 165 17 12 31 10% 36% $453,157 14 E. M. Murray 122 15 13 11 12% 31% $367,960 15 Ricardo Santana, Jr. 67 13 11 12 19% 53% $817,510 16 Robby Albarado 272 13 29 42 4% 30% $624,180 17 Eddie Martin, Jr. 188 12 24 14 6% 26% $354,790 18 Declan Carroll 70 11 5 4 15% 28% $263,700 19 Sophie Doyle 115 10 15 12 8% 32% $311,790 20 Chantal Sutherland 95 8 9 11 8% 29% $259,540 Top 30 Trainers Race Dates: 11/28/19-3/5/20 Rank Trainer Name Starts 1st 2nd 3rd Win% ITM% Earnings 1 Brad H. -

CDI Promotes Austin Miller to President of Fair Grounds Race Course & Slots

October 27, 2008 CDI Promotes Austin Miller to President of Fair Grounds Race Course & Slots Churchill Downs Incorporated (NASDAQ: CHDN) (“CDI”or “Company”) today announced that Austin Miller has been named president of Fair Grounds Race Course & Slots (“Fair Grounds”) in New Orleans. In addition, CDI announced that Eric Halstrom will join Fair Grounds as vice president and general manager of racing. Miller previously served as vice president and general manager of slots and OTB operations at Fair Grounds. In September 2008, he absorbed responsibility for the facility’s racing operation after the departure of former president Randy Soth. “This is a wonderful opportunity for me, and I am both honored and excited to continue my leadership of the outstanding employees of Fair Grounds Race Course and Slots,”said Miller. “With the start of our 2008-09 racing season and the opening of our permanent slots facility near, there’s a great deal to anticipate, and I’m looking forward to being a part of it and continuing my work with the leadership team at Churchill Downs Incorporated.” Miller joined CDI in May 2007 from Harrah’s New Orleans, where he served as vice president of gaming operations. He has also held management and senior executive positions with Grand Casinos, Harrah’s and Caesars, and worked in entertainment and professional sports through affiliations with Mid-America Festivals, Champps Entertainment and the Minnesota Strikers of the Major Indoor Soccer League. Miller holds a bachelor’s degree from the University of Minnesota. Halstrom comes to his new position with 15-plus years of experience in the racing business, including the previous nine years with Canterbury Park in Shakopee, Minn., where he most recently served as vice president of racing and simulcasting operations. -

The Louisiana Futurity Entry Or the Acceptance of a Transfer of an Entry for Any Cause and Without Notice to the Subscriber

FAIR GROUNDS RACE COURSE NEW ORLEANS, LOUISIANA NOTICE The rules of racing adopted by the Louisiana State Racing Commission in effect at the time the race is run, govern all races run under the auspices of the Fair Grounds Corporation. Entries to these stakes are received only with the understanding that the officers of the Corporation reserve the right to refuse the The Louisiana Futurity entry or the acceptance of a transfer of an entry for any cause and without notice to the subscriber. Such entries will on the agreement of the subscriber that they be received only with the understanding and 2020 provisions that the Racing Rules form a part of and govern the contract. No entry will be received except upon this condition: That all disputes, claims and objections arising out of the racing or with respect to the interpretation of the conditions of any stake shall be decided by the Stewards of this Corporation, or those whom they may appoint, and their decision upon all points shall be final. In all stakes, acceptance must be made through entry box at usual time of closing entries. Fair Grounds Corporation reserves the right to divide this race including both the added monies and all nominating and starting fees in the event there is a greater number of starters than the track can ac- commodate. If the race is divided, the Fair Grounds Corporation reserves the right to divide this race by sexes if the number in each group warrants it, and the divisions may be run on separate days, if the corporation desires. -

Still on the Road Venue Index 1956 – 2016

STILL ON THE ROAD VENUE INDEX 1956 – 2016 STILL ON THE ROAD VENUE INDEX 1956-2016 2 Top Ten Concert Venues 1. Fox Warfield Theatre, San Francisco, California 28 2. The Beacon Theatre, New York City, New York 24 3. Madison Square Garden, New York City, New York 20 4. Nippon Budokan Hall, Tokyo, Japan 15 5. Hammersmith Odeon, London, England 14 Royal Albert Hall, London, England 14 Vorst Nationaal, Brussels, Belgium 14 6. Earls Court, London, England 12 Jones Beach Theater, Jones Beach State Park, Wantagh, New York 12 The Pantages Theater, Hollywood, Los Angeles, California 12 Wembley Arena, London, England 12 Top Ten Studios 1. Studio A, Columbia Recording Studios, New York City, New York 27 2. Studio A, Power Station, New York City, New York 26 3. Rundown Studios, Santa Monica, California 25 4. Columbia Music Row Studios, Nashville, Tennessee 16 5. Studio E, Columbia Recording Studios, New York City, New York 14 6. Cherokee Studio, Hollywood, Los Angeles, California 13 Columbia Studio A, Nashville, Tennessee 13 7. Witmark Studio, New York City, New York 12 8. Muscle Shoals Sound Studio, Sheffield, Alabama 11 Skyline Recording Studios, Topanga Park, California 11 The Studio, New Orleans, Louisiana 11 Number of different names in this index: 2222 10 February 2017 STILL ON THE ROAD VENUE INDEX 1956-2016 3 1st Bank Center, Broomfield, Colorado 2012 (2) 34490 34500 30th Street Studio, Columbia Recording Studios, New York City, New York 1964 (1) 00775 40-acre North Forty Field, Fort Worth Stockyards, Fort Worth, Texas 2005 (1) 27470 75th Street, -

Ronnie Virgets Papers

RONNIE VIRGETS PAPERS 6 Linear Feet Special Collections & Archives Loyola University Library Collection 30 RONNIE VIRGETS PAPERS Ronnie Virgets is the quintessential "New Orleans original" - a native with the ability to see, appreciate and poke gentle fun at the quirky qualities that embody the Crescent City. For decades, he has, with well-chosen words and a distinctive voice. evoked images ofhis hometown to inspire new appreciations offamiliar surroundings. His columns and scripts present glimpses ofhis boyhood in Mid-City New Orleans where he was born at Mercy Hospital on April 16, 1942 and attended Catholic schools. While a student at Sl Aloysius High School, he was encouraged by a teacher to develop his writing talents and after high school graduation in 1961 to enroll as a Jownalism student at Loyola University. His first column, "00 the Virg," was published in the Maroon and with other Loyola students. he worked as a "stringer" at the Times-Picayune. He was graduated from Loyola in 1965. After a 1965-1968 U.S. Army tour which took him to Vietnam, Virgets returned to New Orleans and a variety ofjobs, including owning a pool hall. tending bar and working at a small public relations finn. In the mid-70s he returned to journalism, covering sports for the Times-Picayune and eventually writing free-lance sports features. As a child, VirgelS was introduced by his family to the world ofhorse racing and remembers his first visit to the stables where he "even liked the way it smelled," so he was particularly suited to become a columnist for the Racing Form. -

Introduction to Horse Racing Perhaps You've Been to the Track Before, Or

Introduction to Horse Racing Perhaps you’ve been to the track before, or have dabbled in on-line wagering without ever taking it seriously or maximizing the enjoyment. Sure, you can play the races by betting on your favorite horse names, numbers or colors and get lucky, but what most people don’t understand is there is a method to the madness, and figuring out the results of a race based on the information provided, and processed, is fun and rewarding. The premise of a race is simple -- the first horse to the finish line wins, but if you make a wager, predicting the outcome ahead of time is what gets you paid. Horse racing is a fascinating game. At first glance, the information in the past performances of a race can be quite intimidating, but one you get a feel for how it works, and appreciate the majesty of the animals, horse racing can quickly develop into a hobby, or even a passion. With knowledge comes interest and with understanding comes intrigue. As an on-air racing analyst for Churchill Downs, the home of the Kentucky Derby, and currently at Fair Grounds, I am emphasizing “new fan friendly” analysis on the air through the remainder of the season, so if you’re new to the game and/or feel like you have a lot to learn, please tune in via twinspires.com, the Twin Spires App, or the Churchill Downs’ Roku channel, where you can access both live racing and a full-day replays. In the meantime, here is some fundamental information to get you started.