Investor Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2018/19 (PDF)

JAGUAR LAND ROVER AUTOMOTIVE PLC Annual Report 2018/19 STRATEGIC REPORT 1 Introduction THIS YEAR MARKED A SERIES OF HISTORIC MILESTONES FOR JAGUAR LAND ROVER: TEN YEARS OF TATA OWNERSHIP, DURING WHICH WE HAVE ACHIEVED RECORD GROWTH AND REALISED THE POTENTIAL RATAN TATA SAW IN OUR TWO ICONIC BRANDS; FIFTY YEARS OF THE EXTRAORDINARY JAGUAR XJ, BOASTING A LUXURY SALOON BLOODLINE UNLIKE ANY OTHER; AND SEVENTY YEARS SINCE THE FIRST LAND ROVER MOBILISED COMMUNITIES AROUND THE WORLD. TODAY, WE ARE TRANSFORMING FOR TOMORROW. OUR VISION IS A WORLD OF SUSTAINABLE, SMART MOBILITY: DESTINATION ZERO. WE ARE DRIVING TOWARDS A FUTURE OF ZERO EMISSIONS, ZERO ACCIDENTS AND ZERO CONGESTION – EVEN ZERO WASTE. WE SEEK CONSCIOUS REDUCTIONS, EMBRACING THE CIRCULAR ECONOMY AND GIVING BACK TO SOCIETY. TECHNOLOGIES ARE CHANGING BUT THE CORE INGREDIENTS OF JAGUAR LAND ROVER REMAIN THE SAME: RESPONSIBLE BUSINESS PRACTICES, CUTTING-EDGE INNOVATION AND OUTSTANDING PRODUCTS THAT OFFER OUR CUSTOMERS A COMPELLING COMBINATION OF THE BEST BRITISH DESIGN AND ENGINEERING INTEGRITY. CUSTOMERS ARE AT THE HEART OF EVERYTHING WE DO. WHETHER GOING ABOVE AND BEYOND WITH LAND ROVER, OR BEING FEARLESSLY CREATIVE WITH JAGUAR, WE WILL ALWAYS DELIVER EXPERIENCES THAT PEOPLE LOVE, FOR LIFE. The Red Arrows over Solihull at Land Rover’s 70th anniversary celebration 2 JAGUAR LAND ROVER AUTOMOTIVE PLC ANNUAL REPORT 2018/19 STRATEGIC REPORT 3 Introduction CONTENTS FISCAL YEAR 2018/19 AT A GLANCE STRATEGIC REPORT FINANCIAL STATEMENTS 3 Introduction 98 Independent Auditor’s report to the members -

Tata Motors Annual Report

68th Annual Report 2012-13 CONTENTS FINANCIAL HIGHLIGHTS FINANCIAL STATEMENTS 36 Financial Performance Standalone Financial Statements 40 Summarised Balance Sheet 116 Independent Auditors’ Report and Statement of Profit and 120 Balance Sheet Loss Standalone 121 Profit and Loss Statement 42 Summarised Balance Sheet and Statement of Profit and 122 Cash Flow Statement Loss Consolidated 124 Notes to Accounts 44 Fund Flow Statement Consolidated Financial Statements 160 Independent Auditors’ Report STATUTORY REPORTS 162 Balance Sheet 45 Notice 163 Profit and Loss Statement 52 Directors’ Report 164 Cash Flow Statement 66 Management Discussion and 166 Notes to Accounts Analysis CORPORATE OVERVIEW Subsidiary Companies 98 Report on Corporate 02 Corporate Information Governance 197 Financial Highlights 03 Mission, Vision and Values 115 Secretarial Audit Report 200 Listed Securities 04 Chairman’s Statement 201 Financial Statistics 08 Board of Directors 12 Delivering Experiences Attendance Slip & Proxy Form 14 Key Performance Indicators 16 Products and Brands 18 Global Presence 20 Milestones 22 Driving Accountability 24 Focusing on Customers & Products 26 Emphasising Excellence 28 Delivering with Speed 30 Sustainability 34 Awards and Achievements ANNUAL GENERAL MEETING Date: Wednesday, August 21, 2013 Time: 3.00 p.m. Venue: Birla Matushri Sabhagar, 19, Sir Vithaldas Thackersey Marg, Mumbai 400 020 ANTICIPATING NEEDS. DELIVERING EXCITEMENT. At Tata Motors, we believe that our Our renewed commitment to these mobility needs of our customers. We are strengths stem from an organisation- pillars drives us to achieve our mission engaging with them at our dealerships wide culture which rests on four of anticipating and providing the best and adopting processes to ensure that pillars – Accountability, Customer & vehicles and experiences to excite our industry-leading practices form a key part Product Focus, Excellence and customers. -

European Car and Light Commercial Vehicle Production Outlook

European Car and Light Commercial Vehicle Production Outlook November 2012 SMMT, the 'S' symbol and the ‘Driving the motor industry’ brandline are trademarks of SMMT Ltd Contents Introduction and analysis overviews: Individual vehicle manufacturer reviews: About this report 3 BMW 61 Key Highlights 4 Daimler 68 Economic Background 10 Fiat (incl. Chrysler) 74 Automotive Market Overview 17 Ford 80 Overcapacity & Restructuring 22 GM 85 Demand Side Perspective 29 Honda 91 UK VM Summary 30 Hyundai-Kia 93 Production Outlook Overview 34 PSA 96 Country Rankings 48 Renault-Nissan-Dacia 102 Alternative Scenarios 52 Suzuki 111 Disclaimer 59 Tata – Jaguar Land Rover 112 Toyota 116 Volkswagen (incl. Porsche) 119 Aston Martin 128 Geely Volvo 129 Mitsubishi 132 SAIC MG 132 Saab-Spyker 132 Other Chinese – Chery and Great Wall 133 EUROPEAN CAR AND LCV PRODUCTION OUTLOOK REPORT November 2012 | Page 2 About this report This is the sixth 2012 Production Outlook report from AutoAnalysis. The next report will appear in January 2013. The views and projections contained in this report are those of the author, Ian Henry of AutoAnalysis. They do not represent an official SMMT view. The projections regarding new model timings, changes in production locations and the associated production volumes shown here have been compiled on the basis of information from a variety of sources. In most cases, the vehicle companies do not provide official information on which models will be made at which plants, nor do they provide detailed information on future volumes and timings. They have been prepared on the basis of judgments made by AutoAnalysis, taking into account the information, opinion and inside from a range of industry, press and analyst sources available at the time of compiling this report. -

Musk Urges Tesla Workers to Meet Customer Demand

CHINA DAILY | HONG KONG EDITION Monday, March 25, 2019 MOTORING | 19 NEW ARRIVALS Musk urges Tesla workers Sagitar stretching out with longer model FAW-Volkswagen launched its height, with a wheelbase stretch- all-new Sagitar Long-Wheelbase ing 2,731 mm. This is to optimize on Mar 18, in Sanya, South China’s interior space and offer a more to meet customer demand Hainan province. The sedan offers comfortable driver and passenger eight variants with two power- experience. The model has four train options at prices ranging kinds of driving modes: normal, Chinese and European buyers behind massive surge in company’s orders book from 131,800 yuan to 196,800 economic, sporty and individual- yuan ($19,620-$29,300). The ized, which can be tailored by the model sees upgrades in design, driver. Coupled with an advanced SAN FRANCISCO — On Thurs- performance, comfort and safety automatic driving system, includ- day, Tesla chief Elon Musk urged to target customers born in the ing an active lane keeping assist workers to make the “biggest 1980s and 1990s, who are believed system, emergency braking and wave” of deliveries in the electric to have higher requirements adaptive cruise control, the latest- carmaker’s history their top prior- for quality of life. The sedan is generation Sagitar not only rein- ity, Business Insider reported. 4,753 millimeters in length, 1,800 forces its driving safety, but also The news website posted a copy mm in width and 1,462 mm in improves its artificial intelligence. of an internal email from Musk rallying Tesla troops to pitch in with deliveries throughout Europe, China and North America. -

Printmgr File

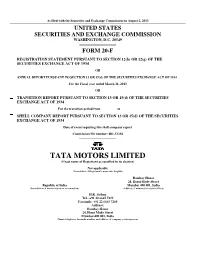

As filed with the Securities and Exchange Commission on August 2, 2013 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ⌧ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal year ended March 31, 2013 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report Commission file number: 001-32294 TATA MOTORS LIMITED (Exact name of Registrant as specified in its charter) Not applicable (Translation of Registrant’s name into English) Bombay House 24, Homi Mody Street Republic of India Mumbai 400 001, India (Jurisdiction of incorporation or organization) (Address of principal executive offices) H.K. Sethna Tel.: +91 22 6665 7219 Facsimile: +91 22 6665 7260 Address: Bombay House 24, Homi Mody Street Mumbai 400 001, India (Name, telephone, facsimile number and address of company contact person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Ordinary Shares, par value Rs.2 per share * The New York Stock Exchange, Inc Securities registered or to be registered pursuant to Section 12(g) of the Act: None (Title of Class) Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None (Title of Class) Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. -

JAGUAR LAND ROVER AUTOMOTIVE Plc RESULTS for the PERIOD ENDED 30 JUNE 2020 31St July 2020 Adrian Mardell, CFO - 2 - Disclaimer

JAGUAR LAND ROVER AUTOMOTIVE plc RESULTS FOR THE PERIOD ENDED 30 JUNE 2020 31st July 2020 Adrian Mardell, CFO - 2 - Disclaimer Statements in this presentation describing the objectives, projections, estimates and expectations of Jaguar Land Rover Automotive plc and its direct and indirect subsidiaries (the “Company”, “Group” or “JLR”) may be “forward-looking statements” within the meaning of applicable securities laws and regulations. Actual results could differ materially from those expressed or implied. Important factors that could make a difference to the Company’s operations include, among others, economic conditions affecting demand / supply and price conditions in the domestic and overseas markets in which the Company operates, changes in Government regulations, tax laws and other statutes and incidental factors. - Q1 represents the 3 month period from 1 April to 30 June - Q2 represents the 3 month period from 1 July to 30 September - Q3 represents the 3 month period from 1 October to 31 December - Q4 represents the 3 month period from 1 January to 31 March - FY represents the 12 month period from 1 April to 31 March of the following year Unless stated otherwise sales volumes are expressed in thousand units, financial values are in GBP millions. Consolidated results of Jaguar Land Rover Automotive plc and its subsidiaries contained in the presentation are unaudited and presented under IFRS as approved in the EU. Retail volume data includes sales from the Company’s unconsolidated Chinese joint venture (“CJLR”), these are excluded from Wholesale volume data. EBITDA is defined as profit before income tax expense, exceptional items, finance expense (net of capitalised interest), finance income, gains/losses on unrealised derivatives and debt, gains/losses on realised derivatives entered into for the purpose of hedging debt, gains/losses on equity investments held at fair value, share of profit/loss from equity accounted investments and depreciation and amortisation. -

Takata Allocation Schedule V3 (01.30.2018).Xlsx

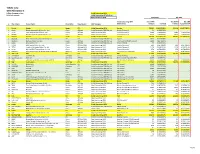

2:16-cr-20810-GCS-EAS Doc # 60-2 Filed 02/01/18 Pg 1 of 3 Pg ID 514 EXHIBIT B 2:16-cr-20810-GCS-EAS Doc # 60-2 Filed 02/01/18 Pg 2 of 3 Pg ID 515 Takata Corp OEM Allocation % Initial Consenting OEM Inflator shipping volume Initial Consenting OEM Roll‐up Units in thousands Joining OEM Non‐Consenting OEM Shipments ALL OEM Initial Consenting OEM Total PSAN Total PSAN ALL OEM # Short Name Formal Name Head office OEM Category Relationship Inflators % of total Inflators ALLOCATION % 1 Honda Honda Japan Initial Consenting OEM Honda 53,397 14.8215192% 53,419 14.8277907% 2CHAC Honda Automobile (China) Co., Ltd. China Initial Consenting OEM Roll‐up Honda Chinese JV 23 0.0062715% ‐ ‐ 3GHAC GAC Honda Automobile Co., Ltd. China Joining OEM Honda Chinese JV 3,682 1.0220562% 3,682 1.0220562% 4WDHAC Dongfeng Honda Automobile Co., Ltd. China Joining OEM Honda Chinese JV 4,323 1.2000105% 4,323 1.2000105% 5 Toyota Toyota Japan Initial Consenting OEM Toyota 44,018 12.2181997% 48,881 13.5681391% 6 NUMMI New United Motor Manufacturing, Inc. US Initial Consenting OEM Roll‐up Toyota 1,922 0.5335676% ‐ ‐ 7Daihatsu Daihatsu Motor Co., Ltd. Japan Initial Consenting OEM Roll‐up Toyota owned (100% owned) 2,908 0.8072901% ‐ ‐ 8HINO Hino Motors, Ltd. Japan Initial Consenting OEM Roll‐up Toyota affiliate 33 0.0090817% ‐ ‐ 9GTMC GAC Toyota Motor Co., Ltd. China Joining OEM Toyota Chinese JV 602 0.1671380% 602 0.1671380% 10 TFTM Tianjin FAW Toyota Motor Co., Ltd. China Joining OEM Toyota Chinese JV 3,069 0.8517936% 3,069 0.8517936% 11 SFTMCF Changchun Fengyue Company of Sichuan FAW Toyota Motor Co., Ltd. -

NEWS RELEASE Vibrant Group Acquires a 8.89 Hectares High Tech

VIBRANT GROUP LIMITED (formerly known as Freight Links Express Holdings Limited) Company Registration Number: 198600061G NEWS RELEASE Vibrant Group acquires a 8.89 hectares High Tech Industrial Park Development Site in Changshu for RMB 28,849,120 SINGAPORE, 19 March 2014 – Vibrant Group Limited (the “Company”) and together with its subsidiaries (the “Group”) today announced that its 50:50 joint venture company, Fervent Industrial Development (Suzhou) Co., Ltd (飞煌工业设施发展(苏州)有限公司) (“Fervent”), through its 60%-owned subsidiary company, Vibrant Properties Pte. Ltd., has acquired a 88,917 square metre (“sqm”) (approximately 8.89 hectares) prime High Tech Industrial Park development site with a total estimated gross floor area of approximately 67,405.04 sqm in Changshu High Tech Industrial Park, CEDZ, Jiangsu for RMB 28,849,120 or an average purchase price of RMB 324.45 per sqm in a public land auction (the “Project”). The Group has an effective 30% shareholding interest in this project. The development site (“Changshu Fervent Industrial Park” or “CFIP”) is located on the north west of the Changshu town centre, approximately 12 kilometers away, enjoying excellent highway connectivity: half an hour drive to Suzhou, Wuxi, Kunshan, Zhangjiagang and Taicang; one hour drive to Shanghai; and two hour drive to Nanjing and Hangzhou. The first phase of CFIP involves six blocks of standard light industrial factory and one block of 5- storey multi-purpose facility, which may house cafes and eateries, ATMs etc. The six blocks of light industrial facilities will be generally of part 3-storey ancillary office and a single storey factory of either semi-detached or terraced configuration. -

2018第四届汽车先进制造技术峰会 the 4Th Automotive Advanced Manufacturing Technology Summit 2018

2018第四届汽车先进制造技术峰会 The 4th Automotive Advanced Manufacturing Technology Summit 2018 Sponsors for 2018 Summit: Diamond Sponsor: Golden Sponsor: Silver Sponsor: Booth Sponsor: Banner Sponsor: Organizer: 2018第四届汽车先进制造技术峰会 The 4th Automotive Advanced Manufacturing Technology Summit 2018 Conference background Who should attend We have sucessufully held the annual event-3rd Automotive Advanced Manufacturing Technology Summit in April 2017. For this l OEMs (Passenger car & Commercial vehicle) year, we will hold the event in Guangzhou, which will traget more l Other vehicle manufactures / Auto parts manufactures than 1100 participants. The event will be the largest one in China and l stumping、welding、printing system integrators highest technical level automotive technology summit that will l Metallic material、non-metallic material、coating material attracts the industry professionals and enterprises. and other suppliers This year's summit will continue to discuss the hot topics of l Press machine enterprises/ Mold enterprises / Robotics three major processes of the vehicle manufacturing ( Stamping, enterprises Welding, Painting), like the latest workshop planning, new l Spraying equipment enterprises/ Testing equipments technology application, new process, new equipment and so on. At enterprises/ Tooling equipment enterprises the same time, we will add “Smart Factory” session for the needs l Welding equipment enterprises / Electric integrated of participants in previous events, discussing intelligent enterprises manufacturing in automobile production -

Tata Motors Annual Report

68th Annual Report 2012-13 WorldReginfo - 82692955-67e3-4e65-9aba-f325bd0e9d58 CONTENTS FINANCIAL HIGHLIGHTS FINANCIAL STATEMENTS 36 Financial Performance Standalone Financial Statements 40 Summarised Balance Sheet 116 Independent Auditors’ Report and Statement of Profit and 120 Balance Sheet Loss Standalone 121 Profit and Loss Statement 42 Summarised Balance Sheet and Statement of Profit and 122 Cash Flow Statement Loss Consolidated 124 Notes to Accounts 44 Fund Flow Statement Consolidated Financial Statements 160 Independent Auditors’ Report STATUTORY REPORTS 162 Balance Sheet 45 Notice 163 Profit and Loss Statement 52 Directors’ Report 164 Cash Flow Statement 66 Management Discussion and 166 Notes to Accounts Analysis CORPORATE OVERVIEW Subsidiary Companies 98 Report on Corporate 02 Corporate Information Governance 197 Financial Highlights 03 Mission, Vision and Values 115 Secretarial Audit Report 200 Listed Securities 04 Chairman’s Statement 201 Financial Statistics 08 Board of Directors 12 Delivering Experiences Attendance Slip & Proxy Form 14 Key Performance Indicators 16 Products and Brands 18 Global Presence 20 Milestones 22 Driving Accountability 24 Focusing on Customers & Products 26 Emphasising Excellence 28 Delivering with Speed 30 Sustainability 34 Awards and Achievements ANNUAL GENERAL MEETING Date: Wednesday, August 21, 2013 Time: 3.00 p.m. Venue: Birla Matushri Sabhagar, 19, Sir Vithaldas Thackersey Marg, Mumbai 400 020 WorldReginfo - 82692955-67e3-4e65-9aba-f325bd0e9d58 ANTICIPATING NEEDS. DELIVERING EXCITEMENT. At Tata Motors, we believe that our Our renewed commitment to these mobility needs of our customers. We are strengths stem from an organisation- pillars drives us to achieve our mission engaging with them at our dealerships wide culture which rests on four of anticipating and providing the best and adopting processes to ensure that pillars – Accountability, Customer & vehicles and experiences to excite our industry-leading practices form a key part Product Focus, Excellence and customers. -

JAGUAR LAND ROVER AUTOMOTIVE PLC Annual Report2018/19 =

JAGUAR LAND ROVER AUTOMOTIVE PLC Annual Report2018/19 = (Registered number 06477691) Iu| "8 #101 WEDNESDAY ‘ba)09/20" COMPANIES HOUSE The Red ArrowsoverSolihull at Land Rover's 70th anniversary celebration STRATEGIC REPORT Introduction THIS YEAR MARKED A SERIES OF HISTORIC MILESTONES FOR JAGUAR LAND ROVER: TEN YEARS OF TATA OWNERSHIP, DURING WHICH WE HAVE ACHIEVED RECORD GROWTH AND REALISED THE POTENTIAL RATAN TATA SAW IN OUR TWO ICONIC BRANDS; FIFTY YEARS OF THE EXTRAORDINARY JAGUAR XJ, BOASTING A LUXURY SALOON BLOODLINE UNLIKE ANY OTHER; AND SEVENTY YEARS SINCE THE FIRST LAND ROVER MOBILISED COMMUNITIES AROUND THE WORLD. TODAY, WE ARE TRANSFORMING FOR TOMORROW. OUR VISION IS A WORLD OF SUSTAINABLE, SMART MOBILITY: DESTINATION ZERO. WE ARE DRIVING TOWARDS A FUTURE OF ZERO EMISSIONS, ZERO ACCIDENTS AND ZERO CONGESTION —- EVEN ZERO WASTE. WE SEEK CONSCIOUS REDUCTIONS, EMBRACING THE CIRCULAR ECONOMY AND GIVING BACK TO SOCIETY. TECHNOLOGIES ARE CHANGING BUT THE CORE INGREDIENTS OF JAGUAR LAND ROVER REMAIN THE SAME: RESPONSIBLE BUSINESS PRACTICES, CUTTING-EDGE INNOVATION AND OUTSTANDING PRODUCTS THAT OFFER OUR CUSTOMERS A COMPELLING COMBINATION OF THE BEST BRITISH DESIGN AND ENGINEERING INTEGRITY. CUSTOMERS ARE AT THE HEART OF EVERYTHING WE DO. WHETHER GOING ABOVE AND BEYOND WITH LAND ROVER, OR BEING FEARLESSLY CREATIVE WITH JAGUAR, WE WILL ALWAYS DELIVER EXPERIENCES THAT PEOPLE LOVE, FOR LIFE. JAGUAR LAND ROVER AUTOMOTIVE PLC ANNUAL REPORT 2018/19 CONTENTS STRATEGIC REPORT FINANCIAL STATEMENTS 3. Introduction 98 Independent Auditor's report -

OEM PSAN Inflator Sales Data Schedule

Takata Corp OEM Allocation % Inflator shipping volume Initial Consenting OEM Units in thousands Initial Consenting OEM Roll-up Non-Consenting OEM Shipments ALL OEM Initial Consenting OEM Total PSAN Total PSAN ALL OEM # Short Name Formal Name Head office Classification OEM Category Relationship Inflators % of total Inflators ALLOCATION % 1 Honda Honda Japan CG Initial Consenting OEM Honda 53,397 14.8215192% 53,419 14.8277907% 2 CHAC Honda Automobile (China) Co., Ltd. China Affiliate Initial Consenting OEM Roll-up Honda Chinese JV 23 0.0062715% - - 3 GHAC GAC Honda Automobile Co., Ltd. China Affiliate Non-Consenting OEM Honda Chinese JV 3,682 1.0220562% 3,682 1.0220562% 4 WDHAC Dongfeng Honda Automobile Co., Ltd. China Affiliate Non-Consenting OEM Honda Chinese JV 4,323 1.2000105% 4,323 1.2000105% 5 Toyota Toyota Japan CG Initial Consenting OEM Toyota 44,018 12.2181997% 48,881 13.5681391% 6 NUMMI New United Motor Manufacturing, Inc. US CG Initial Consenting OEM Roll-up Toyota 1,922 0.5335676% - - 7 Daihatsu Daihatsu Motor Co., Ltd. Japan Affiliate Initial Consenting OEM Roll-up Toyota owned (100% owned) 2,908 0.8072901% - - 8 HINO Hino Motors, Ltd. Japan Affiliate Initial Consenting OEM Roll-up Toyota affiliate 33 0.0090817% - - 9 GTMC GAC Toyota Motor Co., Ltd. China Affiliate (KSS) Non-Consenting OEM Toyota Chinese JV 602 0.1671380% 602 0.1671380% 10 TFTM Tianjin FAW Toyota Motor Co., Ltd. China Affiliate (KSS) Non-Consenting OEM Toyota Chinese JV 3,128 0.8683364% 3,128 0.8683364% 11 SFTM Sichuan FAW Toyota Motor Co., Ltd.