Car Title Loans $700 Loan $1,500 Loan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation

U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities A Financial System That T OF EN TH M E A Financial System T T R R A E P A E S That Creates Economic Opportunities D U R E Y H T Nonbank Financials, Fintech, 1789 and Innovation Nonbank Financials, Fintech, and Innovation Nonbank Financials, Fintech, TREASURY JULY 2018 2018-04417 (Rev. 1) • Department of the Treasury • Departmental Offices • www.treasury.gov U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation Report to President Donald J. Trump Executive Order 13772 on Core Principles for Regulating the United States Financial System Steven T. Mnuchin Secretary Craig S. Phillips Counselor to the Secretary T OF EN TH M E T T R R A E P A E S D U R E Y H T 1789 Staff Acknowledgments Secretary Mnuchin and Counselor Phillips would like to thank Treasury staff members for their contributions to this report. The staff’s work on the report was led by Jessica Renier and W. Moses Kim, and included contributions from Chloe Cabot, Dan Dorman, Alexan- dra Friedman, Eric Froman, Dan Greenland, Gerry Hughes, Alexander Jackson, Danielle Johnson-Kutch, Ben Lachmann, Natalia Li, Daniel McCarty, John McGrail, Amyn Moolji, Brian Morgenstern, Daren Small-Moyers, Mark Nelson, Peter Nickoloff, Bimal Patel, Brian Peretti, Scott Rembrandt, Ed Roback, Ranya Rotolo, Jared Sawyer, Steven Seitz, Brian Smith, Mark Uyeda, Anne Wallwork, and Christopher Weaver. ii A Financial System That Creates Economic -

Adjustable-Rate Mortgage (ARM) Is a Loan with an Interest Rate That Changes

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Board of Governors of the Federal Reserve System www.federalreserve.gov 0412 Consumer Handbook on Adjustable-Rate Mortgages | i Table of contents Mortgage shopping worksheet ...................................................... 2 What is an ARM? .................................................................................... 4 How ARMs work: the basic features .......................................... 6 Initial rate and payment ...................................................................... 6 The adjustment period ........................................................................ 6 The index ............................................................................................... 7 The margin ............................................................................................ 8 Interest-rate caps .................................................................................. 10 Payment caps ........................................................................................ 13 Types of ARMs ........................................................................................ 15 Hybrid ARMs ....................................................................................... 15 Interest-only ARMs .............................................................................. 15 Payment-option ARMs ........................................................................ 16 Consumer cautions ............................................................................. -

Overdraft: Payment Service Or Small-Dollar Credit?

March 16, 2020 Overdraft: Payment Service or Small-Dollar Credit? Funding Gaps in Consumer Finances Figure 1. Annual Interest and Noninterest Income One of the earliest documented cases of bank overdraft U.S. Commercial Banks, 1970-2018 ($ millions) dates back to 1728, when a Royal Bank of Scotland customer requested a cash credit to allow him to withdraw more money from his account than it held. Three centuries later, technologies, such as electronic payments (e.g., debit cards) and automated teller machines (ATMs), changed the way consumers use funds for retail purchases, transacting more frequently and in smaller denominations. Accordingly, today’s financial institutions commonly offer point-of-sale overdraft services or overdraft protection in exchange for a flat fee around $35. Although these fees can be large relative to the transaction, alternative sources of short-term small-dollar funding, such as payday loans, deposit advances, and installment loans, can be costly as well. Congress has taken an interest in the availability and cost of providing consumers funds to meet Source: Federal Deposit Insurance Corporation (FDIC). their budget shortfalls. Legislation introduced in the 116th Congress (H.R. 1509/S. 656 and H.R. 4254/S. 1595) as well Banks generate noninterest income in a number of ways. as the Federal Reserve’s real-time payments initiative could For example, a significant source of noninterest income impact consumer use of overdraft programs in various comes from collecting fees for deposit accounts services, ways. (See “Policy Tools and Potential Outcomes” below such as maintaining a checking account, ATM withdrawals, for more information.) The policy debate around this or covering an overdraft. -

LOAN RATES America First Credit Union Offers Members Competitive Loan Rates, Listed Below

LOAN RATES America First Credit Union offers members competitive loan rates, listed below. The annual percentage rates (APR) quoted are based on approved credit. Rates may be higher, depending on your credit history and other underwriting factors. Our loan offices will discuss your application and available rates with you. Variable APRs may increase or decrease monthly. Go to americafirst.com or call 1-800-999-3961 for more information. EFFECTIVE: OCTOBER 1, 2021 VARIABLE APR FIXED APR FEE DISCLOSURES VEHICLE 2.99% - 18.00% 2.99% - 18.00% ANNUAL PERCENTAGE RATE (APR) FOR PURCHASES 60-MONTH DECLINING RATE AUTO N/A 3.24% - 18.00% When you open your account, the applicable APR is based on creditworthiness. SMALL RV LOAN 4.49% - 15.24% 5.49% - 16.24% After that, your APR will vary with the market based on the Prime Rate. RV LOAN 4.49% - 15.74% 5.49% - 16.74% APR FOR CASH ADVANCES & BALANCE TRANSFERS When you open your account, the applicable APR is based on creditworthiness. RV BALLOON N/A 5.49% - 6.74% After that, your APR will vary with the market based on the Prime Rate. PERSONAL 8.49% - 18.00% 9.49% - 18.00% HOW TO AVOID PAYING INTEREST ON PURCHASES LINE OF CREDIT 15.24% - 18.00% Your due date is the 28th day of each month. We will not charge any interest on the portion of the purchases balance that you pay by the due date each month. SHARE-SECURED LINE OF CREDIT 3.05% FOR CREDIT CARD TIPS FROM THE CONSUMER FINANCIAL PROTECTION CONSUMER SHARE LOAN + 3.00% BUREAU CREDIT BUILDER PLUS 10.00% To learn more about factors to consider when applying for or using a credit card, visit the Consumer Financial Protection Bureau at CERTIFICATE ACCOUNT * 3.00% consumerfinance.gov/learnmore. -

Stopping the Payday Loan Trap Alternatives That Work, Ones That Don’T

Stopping the payday Loan trap AlternAtives thAt Work, ones thAt Don’t NCLC® NATIONAL CONSUMER June 2010 L AW C E N T E R® © Copyright 2010, National Consumer Law Center, Inc. All rights reserved. About the Authors Lauren K. Saunders is the Managing Attorney of NCLC’s Washington, DC office, where she handles legislative, administrative and other advocacy efforts on behalf of low income consumers. She contributes to several NCLC publications, including Fair Credit Reporting, Fair Debt Collection and Consumer Banking and Payments Law. She graduated magna cum laude from Harvard Law School where she was an Executive Editor of the Harvard Law Review, and holds a Masters in Public Policy from Harvard’s Kennedy School of Government and a B.A., Phi Beta Kappa, from Stanford University. Leah A. Plunkett is a staff attorney at NCLC, where she focuses on predatory small dollar loans, auto policy, protection of exempt funds, and the consumer needs of domestic violence survivors. Before coming to NCLC, Leah clerked in the United States District Court for the District of Maryland and established the Youth Law Project at New Hampshire Legal Assistance. Leah is a cum laude graduate of Harvard Law School, where she was on the board of both the Harvard Legal Aid Bureau and HLS for Choice. Carolyn Carter is NCLC’s Deputy Director for Advocacy. She is a contributing author to Cost of Credit, Truth in Lending, Unfair and Deceptive Acts and Practices and several other NCLC treatises. Prior to joining NCLC, she worked for legal services programs in Ohio and Pennsylvania. -

Payday Lending in America

An overview from Oct 2013 Report 3 in the Payday Lending in America series Payday Lending in America: Policy Solutions Overview About 20 years ago, a new retail financial product, the payday loan, began to spread across the United States. It allowed a customer who wanted a small amount of cash quickly to borrow money and pledge a check dated for the next payday as collateral. Twelve million people now use payday loans annually, spending an average of $520 in interest to repeatedly borrow an average of $375 in credit. In the 35 states that allow this type of lump-sum repayment loan, customers end up having to borrow again and again—paying a fee each time. That is because repaying the loan in full requires about one-third of an average borrower’s paycheck, not leaving enough money to cover everyday living expenses without borrowing again. In Colorado, lump-sum payday lending came into use in 1992. The state was an early adopter of such loans, but the situation is now different. In 2010, state lawmakers agreed that the payday loan market in Colorado had failed and acted to correct it. Legislators forged a compromise designed to make the loans more affordable while granting the state’s existing nonbank lenders a new way to provide small-dollar loans to those with damaged credit histories. The new law changed the terms for payday lending from a single, lump-sum payment to a series of installment payments stretched out over six months and lowered the maximum allowable interest rates. As a result, borrowers in Colorado now pay an average of 4 percent of their paychecks to service the loans, compared with 36 percent under a conventional lump-sum payday loan model. -

MLA Faqs 08.22

Frequently Asked Questions about the Defense Department’s Military Lending Act Regulations The following is intended to help pawnbrokers prepare for the October 3, 2016 mandatory compliance date for the expanded Military Lending Act (MLA) regulations. This information is not intended as, and should not be used as, a substitute for guidance from your local lawyer. What is the Military Lending Act? The MLA was enacted by Congress in 2006, and the DOD adopted a regulation to implement it in 2007, but did not cover pawn transactions. The DOD expanded the scope of the regulation to cover additional consumer credit products on July 22, 2015 (“2015 regulation”), and specifically mentioned pawn transactions. When does compliance with the DOD’s 2015 regulation become mandatory for pawn transactions? October 3, 2016, unless extended by the DOD or otherwise by Congress or a court of law. What types of transactions does DOD’s expanded regulation govern? The 2015 regulation applies to pawns if the borrowers or pledgers are active duty service members, their spouse or other dependent who receives 51% or more of their support from the service member. These consumers are “covered borrowers”. No traditional non-recourse pawn transaction entered into before October 3, 2016 is affected by the 2015 regulation. The 2015 regulation does not affect pawns entered into before your customer became an active duty service member or dependent of one. What are the key requirements of DOD’s regulation? The 2015 regulation: • caps the maximum Annual Percentage Rate -

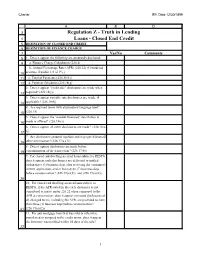

Regulation Z - Truth in Lending 4 Loans - Closed End Credit 5 DEFINITION of CLOSED END CREDIT 6 DEFINITION of FINANCE CHARGE 7 Yes/No Comments 8 1

Charter Eff. Date 12/30/1899 A B D 3 Regulation Z - Truth in Lending 4 Loans - Closed End Credit 5 DEFINITION OF CLOSED END CREDIT 6 DEFINITION OF FINANCE CHARGE 7 Yes/No Comments 8 1. Does it appear the following are accurately disclosed: 9 a. Finance Charge Calculation (226.4) b. Annual Percentage Rate (APR) (226.22) (Considered 10 accurate if within 1/8 of 1%.) 11 c. Total of Payments (226.18(h)) 12 d. Payment Schedules (226.18(g) 2. Does it appear "credit sale" disclosures are made when 13 required? (226.18(j)) 3. Does it appear variable-rate disclosures are made, if 14 applicable? (226.18(f)) 4. Are required terms with explanatory language used? 15 (226.18) 5. Does it appear the “amount financed” itemization is 16 made or offered? (226.18(c)) 6. Does it appear all other disclosures are made? (226.18(a- 17 r)) 7. Are disclosures grouped together and segregated from all 18 other information? (226.17(a)(1)) 8. Does it appear disclosures are made before 19 consummation of the transaction? (226.17(b)) 9. For closed end dwelling-secured loans subject to RESPA, does it appear early disclosures are delivered or mailed within three (3) business days after receiving the consumer's written application, and at least seven (7) business days before consummation? (226.19(a)(1)) and (226.19(a)(2)) 20 10. For closed end dwelling-secured loans subject to RESPA, if the APR stated in the early disclosure is not considered accurate under 226.22 when compared to the APR at consumation, does it appear corrected disclosures of all changed terms, including the APR, are provided no later than three (3) business days before consummation? 21 (226.19(a)(2)) 11. -

Putting Microfinance to the Test 18-Month Impacts of the Grameen America Program

Putting Microfinance to the Test 18-Month Impacts of the Grameen America Program September 2020 M. Victoria Quiroz Becerra Kelsey Schaberg Daron Holman Richard Hendra Dissemination of MDRC publications is supported by the following organizations and individuals that help finance MDRC’s public policy outreach and expanding efforts to communicate the results and implications of our work to policymakers, practitioners, and others: The Annie E. Casey Foundation, Arnold Ventures, Charles and Lynn Schusterman Family Foundation, The Edna McConnell Clark Foundation, Ford Foundation, The George Gund Foundation, Daniel and Corinne Goldman, The Harry and Jeanette Weinberg Foundation, Inc., The JPB Foundation, The Joyce Foundation, The Kresge Foundation, and Sandler Foundation. In addition, earnings from the MDRC Endowment help sustain our dissemination efforts. Contributors to the MDRC Endowment include Alcoa Foundation, The Ambrose Monell Foundation, Anheuser- Busch Foundation, Bristol-Myers Squibb Foundation, Charles Stewart Mott Foundation, Ford Foundation, The George Gund Foundation, The Grable Foundation, The Lizabeth and Frank Newman Charitable Foundation, The New York Times Company Foundation, Jan Nicholson, Paul H. O’Neill Charitable Foundation, John S. Reed, Sandler Foundation, and The Stupski Family Fund, as well as other individual contributors. The findings and conclusions in this report do not necessarily represent the official positions or policies of the funders. For information about MDRC and copies of our publications, see our website: www.mdrc.org. Copyright © 2020 by MDRC®. All rights reserved. Putting Microfinance to the Test 18-Month Impacts of the Grameen America Program M. Victoria Quiroz Becerra Kelsey Schaberg Daron Holman Richard Hendra September 2020 OVERVIEW his report summarizes 18-month findings from the evaluation of the Grameen America pro- gram, a microfinance institution that provides loans to low-income women in the United States who are seeking to start or expand a small business. -

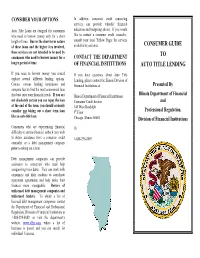

Consumer Guide to Auto Title Lending

CONSIDER YOUR OPTIONS In addition, consumer credit counseling services can provide valuable financial Auto Title Loans are designed for consumers education and budgeting advice. If you would who need to borrow money only for a short like to contact a consumer credit counselor, length of time. Due to the short-term nature consult your local Yellow Pages for services of these loans and the higher fees involved, available in your area. CONSUMER GUIDE these services are not intended to be used by TO consumers who need to borrow money for a CONTACT THE DEPARTMENT longer period of time. OF FINANCIAL INSTITUTIONS AUTO TITLE LENDING If you need to borrow money you should If you have questions about Auto Title explore several different lending options. Lending, please contact the Illinois Division of Contact various lending institutions and Financial Institutions at: Presented By compare fees to find the most economical loan that best suits your financial needs. If you are Illinois Department of Financial Institutions Illinois Department of Financial not absolutely certain you can repay the loan Consumer Credit Section and at the end of the term, you should seriously 100 West Randolph consider not taking out a short term loan 9th Floor Professional Regulation, like an auto title loan Chicago, Illinois 60601 Division of Financial Institutions Consumers who are experiencing financial Or difficulty or serious financial setback may wish to obtain assistance from a consumer credit 1-888-298-8089 counselor or a debt management company prior to taking out a loan. Debt management companies can provide assistance to consumers who need help reorganizing their debts. -

Payday Loans = Costly Cash

Payday Loans = Costly Cash Payday lenders lure consumes with messages like “Get cash until payday! $100 or more…fast!” These ads are on the radio, television, the Internet and even in the mail. These types of loans go by a variety of names: payday loans, cash advance loans, check advance loans, post-dated check loans or deferred deposit check loans – and they come at a very high price. How payday loans work • Usually, a borrower writes a personal check payable to the lender for the amount he or she wishes to borrow plus a fee. The company gives the borrower the amount of the check minus the fee. • Fees charged for payday loans are usually a percentage of the face value of the check or a fee charged per amount borrowed - say, for every $50 or $100 loaned. • If you extend or "roll-over" the loan - say for another two weeks - you will pay the fees for each extension. • Payday lenders create a cycle of debt, encourage chronic borrowing and hold annual interest rates as high at 400%. • Under the Truth in Lending Act, the cost of payday loans - like other types of credit - must be disclosed. Among other information, you must receive, in writing, the finance charge (a dollar amount) and the annual percentage rate or APR (the cost of credit on a yearly basis). • Let's say you write a personal check for $115 to borrow $100 for up to 14 days. The check casher or payday lender agrees to hold the check until your next payday. At that time, depending on the particular plan, the lender deposits the check, you redeem the check by paying the $115 in cash, or you roll-over the check by paying a fee to extend the loan for another two weeks. -

Easy Money, Impossible Debt How Predatory Lending Traps Alabama’S Poor

EASY MONEY, IMPOSSIBLE DEBT How Predatory Lending traPs aLabama’s Poor EASY MONEY, IMPOSSIBLE DEBT How Predatory Lending traPs aLabama’s Poor © southern poverty law center | february 2013 www.splcenter.org CONTENTS executive summary 5 tricks of tHe trade 7 victimized 17 buyer beware 27 safeguards needed 31 wHat next? 35 4 Easy Money, Impossible Debt EXecUTIVE SUmmARY Alabama has four times as many payday lenders as McDonald’s restaurants. and it has more title loan lenders, per capita, than any other state.1 this should come as no surprise. with the nation’s third highest poverty rate and a shamefully lax regulatory environment, alabama is a paradise for predatory lenders. by advertising “easy money” and no credit checks, they prey on low-income individuals and families during their time of greatest financial need – intentionally trapping them in a cycle of high-interest, unaf- fordable debt and draining resources from impoverished communities. although these small-dollar loans are explained to lawmakers as short- term, emergency credit extended to borrowers until their next payday, this is only part of the story. the fact is, the profit model of this industry is based on lending to down- on-their-luck consumers who are unable to pay off loans within a two-week (for payday loans) or one-month (for title loans) period before the lender offers to “roll over” the principal into a new loan. as far as these lenders are concerned, the ideal customer is one who cannot afford to pay down the prin- cipal but rather makes interest payments month after month – often paying far more in interest than the original loan amount.