Annual Report Corporate Information

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SUNAC CHINA HOLDINGS LIMITED 融創中國控股有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 01918)

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt about any aspect of this circular or as to the action to be taken, you should consult your licensed securities dealer or registered institution in securities, bank manager, solicitor, professional accountant or other professional advisers. If you have sold or transferred all your shares in Sunac China Holdings Limited, you should at once hand this circular together with the enclosed form of proxy to the purchaser(s) or transferee(s) or to the bank, licensed securities dealer or registered institution in securities or other agent through whom the sale or transfer was effected for transmission to the purchaser(s) or transferee(s). Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. This circular appears for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for any securities. SUNAC CHINA HOLDINGS LIMITED 融創中國控股有限公司 (incorporated in the Cayman Islands with limited liability) (Stock Code: 01918) (1) CONNECTED TRANSACTION — PROPOSED SHARE ISSUANCE UNDER SPECIFIC MANDATE AND (2) APPLICATION FOR WHITEWASH WAIVER Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders Capitalised terms used on this cover shall have the same meanings as those defined in the section headed “Definition” in this circular, unless the context requires otherwise. -

Three Red Lines” Policy

Real Estate Developers with High Leverage to See Inventory Quality Tested Under Broader “Three Red Lines” Policy October 28, 2020 In our view, the widening of regulations aimed at controlling real estate developers’ interest- ANALYSTS bearing debt would further reduce the industry’s overall credit risk in the long term. However, the nearer term may see less headroom for highly leveraged developers to finance in the capital Xiaoliang Liu, CFA market, pushing them to sell off inventory to ease liquidity pressure. Beijing +86-10-6516-6040 The People’s Bank of China said in September that measures aimed at monitoring the funding [email protected] and financial management of key real estate developers will steadily be expanded. Media reports suggest that the new regulations would see a cap of 15% on annual growth of interest-bearing Jin Wang debt for all property developers. Developers will be assessed against three indicators, which are Beijing called “red lines”: whether asset liability ratios (excluding advance) exceeded 70%; whether net +86-10-6516-6034 gearing ratio exceeded 100%; whether cash to short-term debt ratios went below 1.0. Developers [email protected] which breached all three red lines won’t be allowed to increase their debt. If only one or two of the red lines are breached, such developers would have their interest-bearing debt growth capped at 5% and 10% respectively. The first half of the year saw debt grow rapidly among developers. In a sample of 87 real estate developers that we are monitoring, more than 40% saw their interest-bearing debt grow at a faster rate than 15% year over year as of the end of June (see the chart below). -

Gemdale Properties and Investment Corporation Limited 金地商置集團有限公司* (Incorporated in Bermuda with Limited Liability) (Stock Code: 535)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Gemdale Properties and Investment Corporation Limited * 金地商置集團有限公司 (Incorporated in Bermuda with limited liability) (Stock Code: 535) DISCLOSEABLE TRANSACTION DISPOSAL OF 74% OF A SUBSIDIARY DISPOSAL OF 74% OF A SUBSIDIARY The Board announces that, on 12 July 2018, One Polaris, Shenzhen Weixin, Fainmark and Nanjing Jiqingfeng (all of which are indirect wholly-owned subsidiaries of the Company, as the Vendors) and Perfect Area, Shanghai Hongxing, Xuzhou Vanke and Charm Silver (collectively, as the Purchasers) entered into the Agreement in relation to the Disposal. Upon completion of the Disposal, the Group’s effective equity interest in the Target Company will be reduced from 100% to 26% and the Target Company will be under the joint control of the parties to the Agreement. Therefore, the Target Company will cease to be accounted for as a subsidiary of the Company and will be accounted for as a joint venture of the Group. The financial results of the Target Company will no longer be consolidated into the consolidated financial statements of the Group. LISTING RULES IMPLICATIONS As one the applicable percentage ratios (as defined under the Listing Rules) exceed 5% but are less than 25%, the entering into of the Agreement and the transactions contemplated thereunder (including the consideration) constitutes a discloseable transaction of the Company and is subject to the reporting and announcement requirements under Chapter 14 of the Listing Rules. -

China Reits Property Landlords to Shine 19

SECTOR BRIEFING number DBS Asian Insights DBS Group59 Research • May 2018 China REITs Property Landlords to Shine 19 DBS Asian Insights SECTOR BRIEFING 59 02 China REITs Property Landlords to Shine Ken HE Equity Analyst DBS (Hong Kong) [email protected] Carol WU Head of Greater China Research DBS (Hong Kong) [email protected] Danielle WANG CFA Equity Analyst DBS (Hong Kong) [email protected] Derek TAN Equity Analyst DBS Group Research [email protected] Jason LAM Equity Analyst DBS (Hong Kong) [email protected] Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights [email protected] Goh Chien Yen Editor-in-Chief Jean Chua Managing Editor Martin Tacchi Art Director 19 DBS Asian Insights SECTOR BRIEFING 59 03 04 Executive Summary 08 China REITs Are Lagging Edging Towards Onshore REITs Major Obstacles in Fostering 18 an Onshore REIT Regime CMBS/CMBNs Are Growing Faster C-REITs Are Imminent Which Asset Type Will Benefit 28 More? Modern Logistics Properties The Rise of Active Property Asset Management Which Developer Will Benefit From the Establishment of C-REITs? 49 Appendix DBS Asian Insights SECTOR BRIEFING 59 04 Executive Summary No REIT regime yet he real estate investment trust (REIT) has become an important investment vehicle as evidenced by its separation from the financial sector in the Global Industry Classification Standard as a sector on its own. Major Asian countries/regions have joined western countries to kickstart local versions of REITs, leaving China the last Tbig economy that has yet to have such an investment vehicle. Two major technical In our view, removing legislative obstacles (publicly traded funds are not allowed to obstacles hold commercial properties) is the first step that the government needs to take towards establishing a modern REIT regime. -

U.S. Investors Are Funding Malign PRC Companies on Major Indices

U.S. DEPARTMENT OF STATE Office of the Spokesperson For Immediate Release FACT SHEET December 8, 2020 U.S. Investors Are Funding Malign PRC Companies on Major Indices “Under Xi Jinping, the CCP has prioritized something called ‘military-civil fusion.’ … Chinese companies and researchers must… under penalty of law – share technology with the Chinese military. The goal is to ensure that the People’s Liberation Army has military dominance. And the PLA’s core mission is to sustain the Chinese Communist Party’s grip on power.” – Secretary of State Michael R. Pompeo, January 13, 2020 The Chinese Communist Party’s (CCP) threat to American national security extends into our financial markets and impacts American investors. Many major stock and bond indices developed by index providers like MSCI and FTSE include malign People’s Republic of China (PRC) companies that are listed on the Department of Commerce’s Entity List and/or the Department of Defense’s List of “Communist Chinese military companies” (CCMCs). The money flowing into these index funds – often passively, from U.S. retail investors – supports Chinese companies involved in both civilian and military production. Some of these companies produce technologies for the surveillance of civilians and repression of human rights, as is the case with Uyghurs and other Muslim minority groups in Xinjiang, China, as well as in other repressive regimes, such as Iran and Venezuela. As of December 2020, at least 24 of the 35 parent-level CCMCs had affiliates’ securities included on a major securities index. This includes at least 71 distinct affiliate-level securities issuers. -

China Jinmao (817 HK) China Jinmao

China Financials 26 July 2016 China Jinmao (817 HK) China Jinmao Target price: HKD2.97 Share price (25 Jul): HKD2.26 | Up/downside: +31.4% Initiation: access to prime assets Cynthia Chan (852) 2773 8243 One of the few to have exposure to primary development in tier-2 cities [email protected] A proven brand in high-end housing; growing rentals in tier-1 cities Jonas Kan, CFA (852) 2848 4439 [email protected] Initiating with Buy (1) rating and 12-month target price of HKD2.97 Investment case: We initiate coverage of China Jinmao, the real estate Share price performance flagship of stated-owned Sinochem Corporation, with a Buy (1) call. We (HKD) (%) see China Jinmao as one of the few China developers with a differentiated 2.7 120 2.5 110 and sustainable business model, proven expertise in the primary land 2.2 100 development business in major tier-2 cities (Nanjing and Changsha), and a 2.0 90 sound reputation for high-end residential projects in upper-tier cities 1.7 80 (especially Beijing and Shanghai). Moreover, earnings should be backed by Jul-15 Oct-15 Jan-16 Apr-16 solid and growing recurrent income from several prime rental properties Franshion (LHS) Relative to HSI (RHS) and hotels, many of which are located in core areas of tier-1 cities. 12-month range 1.74-2.66 We believe China Jinmao’s primary development business differentiates it Market cap (USDbn) 3.10 3m avg daily turnover (USDm) 1.49 from other developers, especially at a time when property development Shares outstanding (m) 10,672 margins are shrinking and profitability is becoming harder to maintain. -

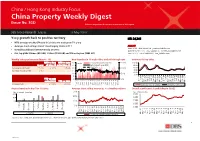

China Property Weekly Digest (Issue No

China / Hong Kong Industry Focus China Property Weekly Digest (Issue No. 302) Refer to important disclosures at the end of this report DBS Group Research . Equity 13 May 2020 Y-o-y growth back to positive territory HSI: 24,246 • MTD average weekly GFA sold in 29 cities we track grew 7% y-o-y • Average short-selling interest stood largely stable at 11% ANALYST Jason LAM +852 36684179 [email protected] • Overall southbound interest steady at 5.65% Danielle WANG CFA, +852 36684176 [email protected] • Our top picks: Shimao (813 HK), Yuzhou (1628 HK) and China Aoyuan (3883 HK) Ken HE CFA, +86 2138968221 [email protected] Weekly sales performance (May 4 – 10) New launches in 10 major cities and sell-through rate Inventory in key cities MTD vs Avg MTD vs same 30 k units Total units launched (LHS) 150% 100.0 w-o-w of May -19 period May-19 25 Sell-through rate (RHS) 80.0 Avg weekly GFA sold ↑ 1.4% ↓ 1.1% ↑ 7.0% 20 26w avg 100% 60.0 Inventory (no. of weeks) ↑ 3.7 15 40.0 20.0 10 50% 0.0 5 YTD vs same 0 0% Jul-13 Jul-18 Jan-11 Jan-16 Jun-11 Jun-16 Feb-13 Oct-14 Feb-18 Oct-19 Apr-12 Sep-12 Apr-17 Sep-17 Dec-13 Dec-18 Nov-11 Nov-16 Mar-15 Mar-20 Aug-15 May-14 period 2019 YTD vs 2019 May-19 7W17 2W18 1W19 YTD GFA sold ↓ 21.3% ↓ 35.0% 9W19 51W16 15W17 23W17 31W17 39W17 47W17 12W18 20W18 28W18 36W18 45W18 17W19 25W19 33W19 41W19 49W19 12W20 Inventory (no. -

Emerging Markets Core Equity Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

Emerging Markets Core Equity Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms -

Investment Savills Research

Beijing – October 2019 MARKET IN MINUTES Investment Savills Research Savills team Please contact us for further information RESEARCH James Macdonald Senior Director China +8621 6391 6688 james.macdonald@ savills.com.cn Vincent Li Associate Director Beijing +8610 5925 2044 vincentx.li@ savills.com.cn CENTRAL MANAGEMENT Investment market sees significant activity Anthony Mcquade Several transactions were completed during the quarter, marking a significant Managing Director Northern China pickup in activity compared to the same period last year. +8610 5925 2002 anthony.mcquade@ savills.com.cn • The first-hand strata-title office market received 185,600 • A total of 14 land plots were transacted during Q3/2019 for a sq m of new supply in Q3/2019, up 6.1% quarter-on-quarter combined consideration of RMB29 billion, marking a 12.4% INVESTMENT (QoQ). Total transaction area reached 235,700 sq m, up QoQ decline. Out of the total transacted land plots, eight Spring Cao 15.3% QoQ. were designated for residential and two for commercial Senior Director usage. Beijing • New supply in the first-hand strata-title retail market +8610 5925 2048 reached 127,400 sq m in Q3/2019, up a significant 144.6% spring.cao@ savills.com.cn QoQ. Total transaction area reached 117,700 sq m, down 36.1% QoQ. Savills plc Savills is a leading global real “ The investment market in estate service provider listed on • Activity in the en-bloc investment market was brisk in the London Stock Exchange. The company established in 1855, has Q3/2019. A total of nine deals were concluded during the Beijing saw several a rich heritage with unrivalled growth. -

Tracker Fund of Hong Kong

LIPPO FUND SERIES LIPPO SELECT HK & MAINLAND PROPERTY ETF SEMI-ANNUAL FINANCIAL STATEMENTS (UNAUDITED) FOR THE SIX MONTHS ENDED 30 SEPTEMBER 2018 LIPPO FUND SERIES LIPPO SELECT HK & MAINLAND PROPERTY ETF Contents Pages Administration and management 1 Report of the Manager 2 Statement of net assets (Unaudited) 3 Investment limitations and prohibitions under the SFC Code (Unaudited) 4 Investment portfolio (Unaudited) 5 - 6 Statement of movements in investment portfolio (Unaudited) 7 - 8 IMPORTANT: Any opinion expressed herein reflects the Manager’s view only and is subject to change. For more information about the Lippo Fund Series, please refer to the prospectus of the Lippo Fund Series which is available at our website: http://lippoetf.com/index.php/fund-info/. Investors should not rely on the information contained in this report for their investment decisions. LIPPO FUND SERIES LIPPO SELECT HK & MAINLAND PROPERTY ETF ADMINISTRATION AND MANAGEMENT Manager Service Agent Lippo Investments Management Limited HK Conversion Agency Services Limited 40/F, Tower Two 1/F, One & Two Exchange Square Lippo Centre, 89 Queensway 8 Connaught Place Hong Kong Central, Hong Kong Website: http://www.lippo-im.com Legal Adviser to the Manager Directors of the Manager King & Wood Mallesons Bruce Cheung Heung Wing 13th Floor, Gloucester Tower David Ng Tai Chiu The Landmark, 15 Queen’s Road Central, Hong Kong Trustee Cititrust Limited Participating Dealers 50th Floor, Champion Tower Goldman Sachs (Asia) Securities Limited Three Garden Road 68th Floor, Cheung Kong Center Central, Hong Kong 2 Queen’s Road (prior to 1 November 2017) Central, Hong Kong BOCI-Prudential Trustee Limited Credit Suisse Securities (Hong Kong) Limited 12/F & 25/F, Citicorp Centre 88th Floor, International Commerce Centre 18 Whitfield Road 1 Austin Road West Causeway Bay, Hong Kong Kowloon, Hong Kong (with effect from 1 November 2017) Auditor Custodian and Administrator PricewaterhouseCoopers Citibank N.A. -

Shimao Property Holdings 0813.HK, 813 HK in Search of the Next Growth Driver Price: HK$11.98 ▼ Price Target: HK$15.20 Previous: HK$16.00

Asia Pacific Equity Research 31 March 2016 Overweight Shimao Property Holdings 0813.HK, 813 HK In search of the next growth driver Price: HK$11.98 ▼ Price Target: HK$15.20 Previous: HK$16.00 Shimao’s FY2015 results came in broadly in line. Core net profit was down 20% China Y/Y driven by margin deterioration, which is likely stabilizing thanks to recent China / Hong Kong Property market rebound. We believe Shimao’s management is logical enough to preserve AC Ryan Li, CFA cash and is not aggressive in land-banking when land price is rising significantly, (852) 2800-8529 hence net gearing on total equity basis stayed low. Shimao is patiently waiting for [email protected] land-banking opportunity, and they have slowly demonstrated their ability in Bloomberg JPMA RLI <GO> seeking and closing deals in the secondary market, including a piece in Shanghai Karl Chan in 2015 and recently a piece in Beijing. Should Shimao be able to buy cheap (852) 2800-8513 landbank in top tier cities using low-cost capital, we believe Shimao will resume [email protected] its growth pace soon, which is a free option attaching to today’s stock price at 5x Jevon Jim 2016E P/E. We believe the lack of growth is fully priced in, and with potential (852) 2800-8538 chairman buyback in the near term, together with strong sales momentum from [email protected] J.P. Morgan Securities (Asia Pacific) Limited YRD, we stay OW with Dec-2016 PT of HK$15.2, based on 6.5x 2016E P/E. -

Premium Asia Property Fund

Premium Asia Property Fund Top 10 Portfolio Holdings as at 30 September 2020 China Resources Land (Real Estate) Market Cap: USD 32.1 Billion • China Resources Land is a comprehensive real estate company with a presence in more than 50 cities across mainland China. The company has over 110 ongoing projects and a land bank exceeding 20 million square metres. • It mainly, operates in the development, investment, management and sale of property; as well as hotel operations and decoration services. • The company stands out with its best-in-class expertise and track record of building residential, shopping and office complexes in the urban cores of China’s megacities. CapitaLand Retail China Trust (REITs) Market Cap: USD 1.0 Billion • CapitaLand Retail China Trust invests in a portfolio of shopping malls located in mainland China. The malls within the portfolio are positioned as a one-stop family-oriented shopping, dining and entertainment destination. This portfolio is supported by a sizeable population in the area. As a result the company is set to benefit from China’s consumption upgrade cycle. • Tenants include global international and domestic retailers such as Wal-Mart, Carrefour, Nike, Sephora, Starbucks, UNIQLO and Zara, most of which are under master or long-term leases. This has allowed them to maintain a resilient portfolio with an occupancy rate of 97.7% (September 2018), further supporting the financial growth of the company into the future. Yuexiu Real Estate Investment Trust (REITs) Market Cap: USD 1.5 Billion • Yuexiu Real Estate Investment Trust focuses on offices, retail and other commercial properties that are able to provide considerable cash flows and returns.