A Case of Davis & Shirtliff Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Factors Affecting Effective Implementation of E-Procurement in Supermarkets' Supply Chain Management in Nairobi and Its Enviro

FACTORS AFFECTING EFFECTIVE IMPLEMENTATION OF E-PROCUREMENT IN SUPERMARKETS’ SUPPLY CHAIN MANAGEMENT IN NAIROBI AND ITS ENVIRONS, KENYA BY ANNE NANZALA ONGOLA A DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF MASTER OF BUSINESS ADMINISTRATION (PROCUREMENT AND SUPPLIES MANAGEMENT) IN THE SCHOOL OF BUSINESS AT KCA UNIVERSITY SEPTEMBER 2017 DECLARATION I declare that this proposal is my original work and has not been previously published or submitted elsewhere for award of a degree. I also declare that this contains no material written or published by other people except where due reference is made and author duly acknowledged. Sign………………………………… Date……………………………… Anne Nanzala Ongola Reg No:13/00859 I do hereby confirm I have examined the master’s Proposal of Anne Nanzala Ongola And have approved it for examination Sign…………………………… Date………………………………… Dr. Brigitt Okonga Proposal supervisor ii ABSTRACT All organizations around the globe seek to identify strategies that will improve their performance as far as their day to day activities are concerned. Businesses such as Supermarkets that engage customers and suppliers alike thrive when they are based on up-to- date supply chain management strategies that keep up with the needs of both parties. One such strategy that is based on Information Technology is E-procurement. This study was set out to investigate the Factors Affecting Effective Implementation of E-Procurement in Supply Chain Management in Supermarkets in Nairobi and its environs. In order to achieve this, the study aimed to identify the effect of employee competence, cost of implementation, management involvement and management commitment on effective management of supply chains of Supermarkets in Nairobi and its environs. -

Generic Strategies Adopted Towards Creation of Competitive Advantage Among Supermarkets in Kenya

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668. Volume 19, Issue 7. Ver. V. (July 2017), PP 64-97 www.iosrjournals.org Generic Strategies Adopted Towards Creation Of Competitive Advantage Among Supermarkets In Kenya. A Case Study of Tier 1 Supermarkets in Kenya. * Martin Kathurima Mwirigi A Thesis Submitted in Partial Fulfilment for the Degree of Master of Business Administration at Kenya Methodist University Corresponding Author: Martin Kathurima Mwirigi Abstract: This study sought to establish the generic strategies and their relationship towards competitive advantage among Tier one supermarkets in Kenya based on Neven and Reardon, 2004 in Kenya namely Nakumatt, Tuskys and Uchumi. An organization can achieve competitive advantagerelative to its rivals through lower cost, best cost, broad differentiation, focused differentiation and focused low cost allowing an organization to outperform its competition by securing a superior market position, paramount skills, quality and adequate resources. There was a great knowledge gap, especially owing to the fact that a big supermarket chain like Uchumi had experienced management shakeup, declared losses, closed stores and lost huge market share unlike competitors Nakumatt and Tuskys continued to expansion footprint in and beyond Kenya as well as other international giants entry to Kenyan retail market. The objective was to establish the relationship between generic strategies adopted and the performance of Supermarkets in Kenya. The respondents came from the three tier one supermarkets. A descriptive design and a historical research design were used in the implementation of the research and analysis of the acquired data. The data was collected using questionnaires. -

East Africa's Family-Owned Business Landscape

EAST AFRICA’S FAMILY-OWNED BUSINESS LANDSCAPE 500 LEADING COMPANIES ACROSS THE REGION PREMIUM SPONSORS: 2 TABLE OF CONTENTS EAST AFRICA’S FAMILY-OWNED BUSINESS CONTENTS LANDSCAPE Co-Founder, CEO 3 Executive Summary Rob Withagen 4 Methodology Co-Founder, COO Greg Cohen 7 1. MARKET LANDSCAPE Project Director 8 Regional Heavyweight: East Africa Leads Aicha Daho Growth Across the Continent Content Director 10 Come Together: Developing Intra- Jennie Forcier Patterson Regional Trade Opens Markets of Data Director Significant Scale Yusra Khadra 11 Interview: Banque du Caire Editorial Manager Lauren Mellows 13 2. FOB THEMES Research & Data Team Alexandria Akena 14 Stronger Together: Private Equity Jerome Amedo Offers Route to Growth for Businesses Laban Bore Prepared to Cede Some Ownership Jessen Chiniven Control Woyneab Habte Mayowa Hambolu 15 Interview: Centum Investment Milkiyas Lekeleh Siyum 16 Interview: Nairobi Securities Exchange Omololu Adeniran 17 A Hire Calling: Merit is Becoming a Medina Mamadou Stronger Factor in FOB Employment Kuringe Masao Melina Matabishi Practices Ivan Matoowa 18 Interview: Anjarwalla & Khanna Sweetness Mathew 21 Interview: CDC Group Plc Paige Arhaus Theodore Angwenyi 22 Interview: Melvin Marsh International Design 23 Planning for the Future: Putting Next- Nuno Caldeira Generation Leaders at the Helm 24 Interview: Britania Allied Industries 25 3. COUNTRY DEEPDIVES 25 Kenya 45 Ethiopia 61 Uganda 77 Tanzania 85 Rwanda 91 4. FOB DIRECTORY EAST AFRICA’S FAMILY-OWNED BUSINESS LANDSCAPE EXECUTIVE SUMMARY 3 EXECUTIVE -

Effect of Internal Control Practices on Financial

EFFECT OF INTERNAL CONTROL PRACTICES ON FINANCIAL PERFORMANCE OF SUPERMARKET CHAINS IN NAIROBI CENTRAL BUSINESS DISTRICT BY ROSELYN N. GITAU MASTER OF SCIENCE IN COMMERCE (FINANCE AND ACCOUNTING) KCA UNIVERSITY 2018 EFFECT OF INTERNAL CONTROL PRACTICES ON FINANCIAL PERFORMANCE OF SUPERMARKET CHAINS IN NAIROBI CENTRAL BUSINESS DISTRICT BY ROSELYN N. GITAU REG: 17/00549 A DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF THE DEGREE OF MASTER OF SCIENCE IN COMMERCE (FINANCE AND ACCOUNTING) IN THE SHOOL OF BUSINESS AND PUBLIC MANAGEMENT, KCA UNIVERSITY NOVEMBER, 2018 DECLARATION I declare that this dissertation is my original work and has not been published or submitted elsewhere for the award of the degree of Master of Science in Commerce (Finance and Accounting). I also declare that this dissertation contains no material written or published by other people except where due reference is made and the author duly acknowledged. Roselyn N. Gitau Registration Number 17/00549 Sign: ____________________ Date: __________________________ I do hereby confirm that I have examined the Masters dissertation of Roselyn N. Gitau And have certified that all revisions that the dissertation panel and examiners recommended have been adequately addressed Sign: ____________________ Date: __________________________ Dr. Brigitte W. Okonga Supervisor ACKNOWLEDGEMENT It is with great pleasure that I would like to express my appreciation to the support system that stood by me as I undertook this dissertation. It is because of their great support that the completion of this research project was made possible. First and foremost, I thank the Almighty God for empowering me to undertake this dissertation, without Him it would have been impossible. -

Influence of Marketing Strategies on Competitiveness of PZ Cussons East Africa Limited

INFLUENCE OF MARKETING STRATEGIES ON COMPETITIVENESS OF PZ CUSSONS EAST AFRICA LIMITED OMWENGA ANITA MAGOMA A RESEARCH PROJECT SUBMITED IN PARTIAL FULFILMENT FOR THE AWARD OF DEGREE OF MASTER OF BUSINESS ADMINISTRATION, SCHOOL OF BUSINESS, UNIVERSITY OF NAIROBI 2019 DECLARATION I declare this study project is my original work and has not been presented for educational purposes in University of Nairobi or any other higher learning institution. Signature…………………………………… Date…………………………… ANITA MAGOMA OMWENGA D61/ 79093/2015 This research project has been submitted for examination with my approval as the university supervisor Signature ………………………………………. Date ……………………………………… PROFESSOR JUSTUS MUNYOKI DEPARTMENT OF BUSINESS ADMINISTRATION UNIVERSITY OF NAIROBI i ACKNOWLEDGEMENT I would like to acknowledge my supervisor Professor Justus Munyoki, for his dedication and interest during the process of this entire research. His guidance, encouragement and constructive counsels made this research come to an end. I am also grateful to PZ Cussons East Africa Limited managers who created time to answer to my interview queries. ii DEDICATION I dedicate this research to my parents Mr and Mrs Omwenga for their unwavering love and support always. I dedicate this study to my siblings who have never failed to give me moral support. Last but not least, I dedicate this research to my beloved family. To them, I say thank you. iii ABBREVIATIONS & ACRONYMS FMCG Fast Moving Consumer Goods COMESA Common Market for East and Southern Africa KPMG Klynveld Peat Marwick Goerdeler PZ Paterson Zochonis RBV Resource Based View iv ABSTRACT The objective of this research was to establish influence of marketing strategies on competiveness of PZ Cussons East Africa Limited. -

Effect of Inventory Control Strategies on Performance of Retail Chains in Kenya

EFFECT OF INVENTORY CONTROL STRATEGIES ON PERFORMANCE OF RETAIL CHAINS IN KENYA. A CASE OF NAIVAS SUPERMARKET Ndigwa, D. M., & Moronge, M. Vol. 6, Iss. 3, pp 343 - 355, August 4, 2019. www.strategicjournals.com, ©Strategic Journals EFFECT OF INVENTORY CONTROL STRATEGIES ON PERFORMANCE OF RETAIL CHAINS IN KENYA. A CASE OF NAIVAS SUPERMARKET Ndigwa, D. M.,1* & Moronge, M.2 1*Msc. Candidate, Jomo Kenyatta University of Agriculture & Technology [JKUAT], Kenya 2Ph.D, Lecturer, Jomo Kenyatta University of Agriculture & Technology [JKUAT], Kenya Accepted: July 25, 2019 ABSTRACT This study pursued to evaluate the effect of inventory control strategies on the performance of Kenyan retail industry. Retail business is vital in any growing nation and account for over 65% of the GDP. This is why nations must continually invest in this industry. Over the previous two eras there had remained a steady growth of retail chains and most companies were fighting to be market leaders. Amid all this competition retail organizations continued to experience allot of challenges which includes but not limited to; looking for new markets, unplanned rapid expansion, poor governance and weak controls. All this was as a result of poor inventory control strategies. The broad purpose of this study was to analyze inventory control strategies effect on performance of retail chain in Kenya. Primary and secondary Data collection was done. Questionnaires were used to collect primary data and secondary data by use of journal, reports, books and the internet. This study examined the effect of consignment inventory and electronic data interchange (EDI) on the performance of retail organizations in Kenya with a keen interest on the employees of Naivas supermarket with a target population of 125. -

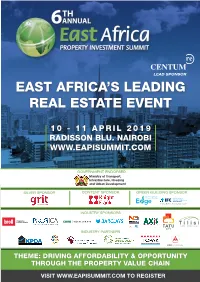

EAPI Summit Brochure

LEAD SPONSOR EAST AFRICA’S LEADING REAL ESTATE EVENT 10 - 11 APRIL 2019 RADISSON BLU. NAIROBI WWW.EAPISUMMIT.COM GOVERNMENT ENDORSED Ministry of Transport, Infrastructure, Housing and Urban Development SILVER SPONSOR CONTENT SPONSOR GREEN BUILDING SPONSOR INDUSTRY SPONSORS INDUSTRY PARTNERS A S S A L O C R I A U T T I C O E N T I O H F C K R E A N E Y A H T PROMOTING EXCELLENCE AAK IN THE BUILT ENVIRONMENT THEME: DRIVING AFFORDABILITY & OPPORTUNITY THROUGH THE PROPERTY VALUE CHAIN VISIT WWW.EAPISUMMIT.COM TO REGISTER AN OVERVIEW OF EAPI 2018 20 COUNTRIES 100 62 239 SPEAKERS MEDIA CCOMPANIES 33.5% 66.5% INTERNATIONAL LOCAL 513 DELEGATES 14 INDUSTRIES REPRESENTED Property Investment 11.81% Consulting and Advisory 12.29% Property Management and Support Services 14.90% Retail 3.10% Hoteliers 2.62% Construction and Engineering Services 5.24% Finance and Banking 8.10% Property Development 16.67% Legal 3.57% Architect 2.86% Quantity Surveying Services 3.57% Pension Fund 0.71% Government 4.05% Media and Other 7.52% 0% 5% 10% 15% 20% 25% 30% 35% 40% ABOUT THE EAPI SUMMIT In its sixth year, the East Africa Property Investment (EAPI) Summit has become the leading property event for the entire region’s real estate market. Driven by passionate professionals, fast growing economies and exciting projects; the real estate sector provides potential and opportunity for the educated and savvy investor or developer. Designed by property professionals to provide insight, debate, deal-making and networking opportunities through an intensive and collaborative two-day agenda; the EAPI Summit plays a pivotal role in deconstructing the regional markets and providing transparency and insight for the industry for both private sector and public-sector stakeholders. -

Download Venture Magazine

TRENDS INTEL INDUSTRY COUNTRY PURSUITS HOUSING FUND CONCERTS E-COMMERCE KENYA TRAVEL GEMS NOT FOR SALE NOT Corporate Magazine | October - December, 2018 E-COMMERCE REPORT Thanks to the Internet and Mobile the power of smart phones, entrepreneurs are taking advantage of opportunities created by e-commerce and are commerce scaling their small businesses revolution into success stories Regulated2 by| the Central Bank of Kenya 37 KCB Bank’s Simba Points program Through the Simba Points program, the bank is rewarding its customers for transactions they make. 6 Housing pillar and the opportunities for investors The government has prioritised housing as one of the pillars that will drive growth in the next five years. 42 Hidden gems for tourists It is the holiday season again, a time when people are planning to go on holiday. To help you choose, we have curated some of Africa’s best hidden gems. 24 8 Making of a memorable concert From dukawallas to Jumia There are many factors Over the years, Kenya’s retail sector has that take place behind-the- experienced tremendous growth. Corner shops, scenes which determine if the which were the norm, are being replaced by audience get value for money. mega shopping malls and virtual stores. Nairobi’s ‘kibanda’ traders make a big splash online Marketers are leveraging on the power 18 of social media to advertise and sell their products and services. | 3 WORDFROM THEEDITOR Latching onto the digital platforms few of years ago one would have been quick to dismiss the suggestion that e-commerce would one day kill “brick and mortar” retail as lazy thinking. -

FMCG and Retail Sector in Africa SECTOR REPORT Corporate Guide for the Packaged Food Sector in African Countries and Possible Synergies with Turkey

2020 FMCG and Retail Sector in Africa SECTOR REPORT Corporate guide for the packaged food sector in African countries and possible synergies with Turkey 1 2 About Istanbul Africa Trade Company Istanbul Africa Trade Company aims to improve economic relations between Turkey and African countries. Through our international trade services, businesses reach better products and deliver services to large areas. In addition to international trade services, we proudly provide product investigation, trade strategy development, contract manufacturing services. Disclaimer Copyright © 2020 Istanbul Africa Trade Company This business report was developed to provide information about current economic outlook in Africa from our perspective. This guide does not constitute legal or regulatory advice, nor guidance or advice regarding the preparation of policies and procedures. The practices and standards described in this report may not be sufficient under applicable law or for another financial institution with which the user seeks to do business. All rights reserved. Istanbul Africa Trade Company accepts no liability whatsoever for the actions of third parties in the distribution of the report. The data, analysis and insights in this report were prepared by Istanbul Africa Trade Company. This report is not a business and trade advice. Istanbul Africa Trade Company is not liable to update the information or conclusions in this report. Istanbul Africa Trade Company does not accept any liability for any loss arising from information contained in this report. -

Information Memorandum

UCHUMI SUPERMARKETS LIMITED Incorporated in Kenya under the Companies Act (Cap. 486, Laws of Kenya) (Registration Number C.6/92) INFORMATION MEMORANDUM The Rights Issue of 99,534,980 New Ordinary Shares Fully Paid At An Offer Price of KShs 9.00 In The Ratio Of 3 New Ordinary Shares For Every 8 Ordinary Shares Held Lead Transaction Advisor Faida Investment Bank Limited Sponsoring Stock Brokers Faida Investment Bank Ltd(Kenya), Faida Securities Rwanda (Rwanda), UAP Financial Services Ltd (Uganda), Rasilimali Ltd (Tanzania) Legal Advisor Hamilton Harrison & Mathews Reporting Accountant Ernst & Young Receiving Bank Equity Bank Limited Share Registrars Funguo Registrars Limited PR and Advertising Consultant Hill & Knowlton Strategies The date of this Information Memorandum is 7 November 2014 1 TRANSACTION ADVISORS LEAD TRANSACTION ADVISOR SPONSORING STOCK BROKERS LEAD LEGAL ADVISOR REPORTING ACCOUNTANT RECEIVING BANK REGISTRARS PR & COMMUNICATION AND ADVERTISING CONSULTANT 2 TABLE OF CONTENTS 1 CONTACT INFORMATION..................................................................................................................................... 4 2 IMPORTANT NOTICE ............................................................................................................................................ 7 3 DEFINITIONS AND INTERPRETATIONS............................................................................................................ 10 4 CHAIRPERSON’S STATEMENT......................................................................................................................... -

Impax Company Profile

COMPANY PROFILE Solutions in time, meeting your every need. 1 IMPAX BUSINESS SOLUTIONS LTD mpax Business Solutions Limited (Impax) is an information VISION systems and business consultancy company based in Nairobi, Kenya but with operations in Uganda and Nigeria. To be the premier IT business solutions company in Africa. IWe provide business solutions and consultancy services in the areas of business process automation and MISSION mobile solutions. To provide leading IT solutions tailored to meet the client’s specific needs including business improvement and value Impax was founded in August 2003 and has so far undertaken adding systems and at the same time ensuring a quick a wide range of consultancy assignments across Africa. We return on investment through a combination of continuous endeavour to provide world-class business management technological advancement and dedicated, highly skilled systems and support services to solve business problems and motivated professionals committed to the delivery of and enhance business performance in organizations. This timely and quality services. has been attained through partnering with strategic market leaders ensuring that our clients acquire solutions that OUR CORE VALUES efficiently satisfy their business needs. • Excellence Impax is the Microsoft Partner of the year 2017 – Public • Quality Sector: Government for West, East and Central African • Trust (WECA) region. We have also previously received awards in • Respect CRM & RMS and continuously featured in the Top 100 Mid- Sized Companies Awards since 2014. 2 OUR PRINCIPLE STATEMENT INNOVATIVE PRODUCTS Impax continues to identify and make available to its clients the most innovative and cutting edge technologies that will deliver the highest value to the clients. -

The Sub-Sharan Africa Organized Mass Grocery

+44 20 8123 2220 [email protected] I&R - The Sub-Sharan Africa Organized Mass Grocery Retail Market Report 2016 https://marketpublishers.com/r/I44CE95D7BBEN.html Date: April 2017 Pages: 133 Price: US$ 1,400.00 (Single User License) ID: I44CE95D7BBEN Abstracts The retailing market in Africa is expected to record a stronger positive value performance over the next decade. Major drivers will include population growth and the projected positive economic growth across many African countries, as well as heightened marketing activities and investing from international players. In addition, growth is set to be driven by the increasing rate of urbanization, the rapidly-growing middle class and increased local and international retail investment by players in the African market, which is expected to boost retailing in the region. Driven by “one-stop- shopping”, in addition to offering consumer convenience, grocery retailers across the continent have used retail floor space to accommodate a variety of products aimed at growing sales revenues and maintaining customer loyalty. Increased international interest in the African market, through direct investment by players, such as Walmart Game, Carrefour and continental players especially from Southern Africa Such as South Africa’s Shoprite, Botswana’s Choppies, and Kenya’s Nakumatt have played a key role in expanding mass grocery retail and promoting consumer confidence and spending. As incomes rise and all of the usual emerging market dynamics are in play, such as urbanization, more hectic lifestyles, many people in Africa are also gaining access to mass grocery retail services. However, while Africa continent is prime for investment‚ this must be tempered with knowledge of the trading risks such as the lack of formalized retail infrastructure, power shortages and poor supply and logistics chains.