Voya Secure Index Opportunities Plus Annuity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Operative Facts in Surrenders (Concluded)

University of Missouri Bulletin Law Series Volume 38 April 1928 Article 9 1928 Operative Facts in Surrenders (concluded) Merrill I. Schnebly Follow this and additional works at: https://scholarship.law.missouri.edu/ls Part of the Law Commons Recommended Citation Merrill I. Schnebly, Operative Facts in Surrenders (concluded), 38 Bulletin Law Series. (1928) Available at: https://scholarship.law.missouri.edu/ls/vol38/iss1/9 This Article is brought to you for free and open access by the Law Journals at University of Missouri School of Law Scholarship Repository. It has been accepted for inclusion in University of Missouri Bulletin Law Series by an authorized editor of University of Missouri School of Law Scholarship Repository. For more information, please contact [email protected]. OPERATIVE FACTS IN SURRENDERS CREATION IN THE LESSEE OF A NEW INTEREST IN THE SAME PREMISES Where the lessee has accepted a new interest in the premises embraced in the original demise, and such new interest is incapable of existing along with the old, the latter is extinguished through a surrender "by act and operation of law." When a new interest of this kind has been created in the lessee, a problem arises which offers but two possibilities of solution. Either it must be held that the new interest is valid and the former interest extinguished, or else that the new interest is invalid and the original lease still in full effect. If the parties think in creating the new interest of its effect upon the original lease, it would seem that they must regard the old leasehold interest as ex- tinguished. -

What Is Your Client's

Strength Since 1906 Midland National Midland National’s story is a classic example of American perseverance and ingenuity. Since 1906, Midland National has survived and thrived through two world wars, the Great Depression, the Dust Bowl, Products At-A-Glance and multiple recessions. Now with over 100 years under its belt, Midland National holds over one million life insurance and annuity policies with assets of over $44 billion. Source: Midland National 2015 Annual Report. • A+ (Superior) A.M. Best A.M. Best is a large third‐party independent reporting and rating company that rates an insurance company on the basis of the company’s financial strength, operating performance and ability to meet its obligations What is your client’s to policyholders. A+ is the second highest rating out of 15 categories and was affirmed for Midland National Life Insurance Company as part of Sammons Financial Group on July 14, 2016. For the latest rating, access www.ambest.com. • A+ (Strong) Standard & Poor’s Standard and Poor’s awarded its “A+” (Strong) rating for insurer financial strength on February 26, 2009 and affirmed on July 2, 2015 to Midland National Life Insurance Company, as part of Sammons Financial Group. The “A+” (Strong) rating is the fifth highest out of 22 available ratings. FOCUS? Questions? Need illustration help? Call our Sales Support team at 800-843-3316 ext. 32150. Protection...Growth...Flexibility... Midland National has a product for every focus. Administrative Office • One Sammons Plaza • Sioux Falls, SD 57193 MidlandNational.com -

Quarterly CPS1 Performance Flier

Take a look at Horace Mann's Capital Premier Series I An annuity offers some significant features and guarantees. As life expectancies increase, a key retirement concern is outliving your money. With an annuity you have the opportunity to choose lifetime income options, which would supply you with income you are guaranteed not to outlive. In addition, if you die before you retire, the guaranteed minimum death benefit provides some safeguards for your family. With Horace Mann Life Insurance Company's Capital Premier Series 1 (CPS 1) group variable annuity you get that and more. Horace Mann has partnered with a number of well-known investment firms to provide educators a full range of investment options that span a wide spectrum of investment styles. From large company growth to bond options, we can help match your personal investment comfort level with the appropriate investment options. You can re-allocate your money, use dollar-cost-averaging, or use systematic rebalancing to maintain your desired investment strategy. You can also allocate contributions to a fixed account with a guaranteed interest rate. Keep a long-range outlook A variable annuity is an insurance product designed to help meet retirement needs and should be seen as part of a long-term retirement plan. However, we understand investors may want to monitor the performance results of the investment options available within our variable annuities. Therefore, we provide these monthly performance updates. Take a few minutes to review the results; we caution you to not make a purchase or allocation decision based solely on the numbers in the following tables. -

Will of Dame Anne Packington.Pdf

TNA PROB/11/47 Will of Dame Anne Packington In the name of the father and of the sonne and of the holy ghoste The xxvjth daie of the monneth of Aprell in the yere of incarnacion of our Lorde Jesus Christe 1563. I Dame Anne Packington Widdow late the wief of Sir John Pakington knight deceased being in the hole mynde and in health of boddie blessed be almightie god remembringe and calling to mynde the mutablitie of this transitory lief knowing my selfe mortall and subiecte to death whereunto every creature is borne. Doe make ordeine and declare this my present Testament and last will in manner and fourme followinge ffirst and principally I bequeath my soule to the blissed Trinitie and the holly company of heaven my bodie to be buried in that parishe churche Where it shall please god to ende my lief or where my executors shall thinke mete at thende of the highe aulter Wheras the sepulture was vsed moste commonly to stande if the rome and place maie be suffered or els at thother ende of the high alter And I will that my executors shall cause a Tombe of marble to be made and sett over my bodie for the making Wherof I bequeath twenty markes or more if it come to more/ And I bequethe to xxti poore men and women every one a blacke gowne of an honest clothe or good frise Wherof xij of them shall beare at my buriall xij torches and iiij of them shall beare forever greate tapers if the lawes of this Realme will so permitt and suffer Item I bequeath amonge the poore househoulders dwelling in that parrish where I shalbe buried twelve pennce a pece/ And among all other people comming to my buriall ij d. -

What Amounts to a Surrender by Operation of Law?

September 2010 Review Property @ction Welcome to the Fifth Edition of the Quarterly Review from Hammonds’ Property@ction Team. In this issue we will look at the following: (i) What amounts to a surrender by operation of law; (ii) Does it do what it says on the tin? - full repairing and insuring leases; (iii) Double trouble; (iv) Compulsory purchase orders; (v) Adverse possession; We welcome all contributions to this review and if you would like to discuss this further please contact any of the editorial team. What amounts to a surrender by operation of law? Where a landlord and tenant bring a lease to an end, they usually do so by completing a deed of surrender. However, sometimes, it may be implied that a surrender has occurred. The term commonly used for an implied surrender is a surrender “by operation of law”. In a recent case, QFS Scaffolding v Sable1 , the court considered some of the relevant principles for a surrender by operation of law to take place. Facts The landlord (Mr and Mrs Sable) granted a lease to a tenant company which eventually entered into administration. Prior to the administration, a new company (QFS) was formed with a view to taking over the tenant’s business. The Sables negotiated terms for a new lease with QFS who, in fact, went into occupation. However, the negotiations faltered and no new lease was entered into. Instead, QFS asked the administrator of the tenant to assign the lease to it and, as a result of this request, a deed of assignment was executed. -

Understanding the Religious Terrorism of Boko Haram in Nigeria

African Study Monographs, 34 (2): 65–84, August 2013 65 NO RETREAT, NO SURRENDER: UNDERSTANDING THE RELIGIOUS TERRORISM OF BOKO HARAM IN NIGERIA Daniel Egiegba AGBIBOA Oxford Department of International Development, University of Oxford ABSTRACT Boko Haram, a radical Islamist group from northeastern Nigeria, has caused severe destruction in Nigeria since 2009. The threat posed by the extremist group has been described by the present Nigerian President as worse than that of Nigeria’s civil war in the 1960s. A major drawback in the Boko Haram literature to date is that much effort has been spent to remedy the problem in lieu of understanding it. This paper attempts to bridge this important gap in existing literaure by exploring the role of religion as a force of mobilisation as well as an identity marker in Nigeria, and showing how the practice and perception of religion are implicated in the ongoing terrorism of Boko Haram. In addition, the paper draws on the relative deprivation theory to understand why Boko Haram rebels and to argue that religion is not always a sufficient reason for explaining the onset of religious terrorism. Key Words: Boko Haram; Nigeria; Religious terrorism; Identity; Relative deprivation theory. INTRODUCTION Since 2009, bombings and shootings by the Nigerian extremist group Boko Haram have targeted Nigeria’s religious and ethnic fault lines in an apparently escalating bid to hurt the nation’s stability. A spate of increasingly coordinated and sophisticated attacks against churches from December 2011 through July 2012 suggests a strategy of provocation through which the group seeks to spark wide- scale sectarian violence that will strike at the foundations of the country (Forest, 2012). -

MSME) During COVID 19 Outbreak in South Sulawesi Province Indonesia

May – June 2020 ISSN: 0193-4120 Page No. 26707 - 26721 Factors Influencing Resilience of Micro Small and Medium Entrepreneur (MSME) during COVID 19 Outbreak in South Sulawesi Province Indonesia Muhammad Hidayat¹, Fitriani Latief², DaraAyu Nianty³ ShandraBahasoan⁴AndiWidiawati⁵ ¹²³⁴⁵STIE Nobel Indonesia Article Info Abstract: Volume 83 Aim: To find out factors influencing resilience of Micro Small and Medium Page Number: 26707 – 26721 Entrepreneur MSME entrepreneurs during the worlwide spread of COVID-19 Publication Issue: pandemic, this study aims at empirically examine the influence of entrepreneurial May - June 2020 personality in utilizing technology and government support for business resilience through crisis management as an intervening variable. Research design, data and method:This research is a quantitative study analyzing sample of 97 small and medium enterprisesactors in South Sulawesi, Indonesia, chosen by using purposive sampling. The main data in this study is results of questionnaires distributed to respondents which is analyzed by using Partial Least Square (PLS analysis). Results and Findings: This study proves a positive and significant relationship between entrepreneurship personlity and crisis management. Thereis no significant relationship between utilizing of technology toward crisis management. There is a Article History positive and significant relationship between government supporttoward crisis Article Received: 11 May 2020 management. This research also proves a positive and significant influence between Revised: 19 May 2020 crisis management on business resilience. Accepted: 29 May 2020 Publication: 12 June 2020 Keywords: Entrepreneurship Characteristic, Technology Utilization, Government Support , Business Resilience I. INTRODUCTION viruses that infect the respiratory system. This viral infection is called covid-19. The world has been being troubled by the Coronavirus causes common cold,amild to appearance of corona virus. -

GOLD Package Channel & VOD List

GOLD Package Channel & VOD List: incl Entertainment & Video Club (VOD), Music Club, Sports, Adult Note: This list is accurate up to 1st Aug 2018, but each week we add more new Movies & TV Series to our Video Club, and often add additional channels, so if there’s a channel missing you really wanted, please ask as it may already have been added. Note2: This list does NOT include our PLEX Club, which you get FREE with GOLD and PLATINUM Packages. PLEX Club adds another 500+ Movies & Box Sets, and you can ‘request’ something to be added to PLEX Club, and if we can source it, your wish will be granted. ♫: Music Choice ♫: Music Choice ♫: Music Choice ALTERNATIVE ♫: Music Choice ALTERNATIVE ♫: Music Choice DANCE EDM ♫: Music Choice DANCE EDM ♫: Music Choice Dance HD ♫: Music Choice Dance HD ♫: Music Choice HIP HOP R&B ♫: Music Choice HIP HOP R&B ♫: Music Choice Hip-Hop And R&B HD ♫: Music Choice Hip-Hop And R&B HD ♫: Music Choice Hit HD ♫: Music Choice Hit HD ♫: Music Choice HIT LIST ♫: Music Choice HIT LIST ♫: Music Choice LATINO POP ♫: Music Choice LATINO POP ♫: Music Choice MC PLAY ♫: Music Choice MC PLAY ♫: Music Choice MEXICANA ♫: Music Choice MEXICANA ♫: Music Choice Pop & Country HD ♫: Music Choice Pop & Country HD ♫: Music Choice Pop Hits HD ♫: Music Choice Pop Hits HD ♫: Music Choice Pop Latino HD ♫: Music Choice Pop Latino HD ♫: Music Choice R&B SOUL ♫: Music Choice R&B SOUL ♫: Music Choice RAP ♫: Music Choice RAP ♫: Music Choice Rap 2K HD ♫: Music Choice Rap 2K HD ♫: Music Choice Rock HD ♫: Music Choice -

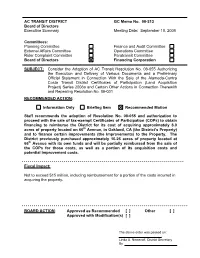

Resolution No

AC TRANSIT DISTRICT GC Memo No. 08-213 Board of Directors Executive Summary Meeting Date: September 10, 2008 Committees: Planning Committee Finance and Audit Committee External Affairs Committee Operations Committee Rider Complaint Committee Paratransit Committee Board of Directors Financing Corporation SUBJECT: Consider the Adoption of AC Transit Resolution No. 08-055 Authorizing the Execution and Delivery of Various Documents and a Preliminary Official Statement in Connection With the Sale of the Alameda-Contra Costa Transit District Certificates of Participation (Land Acquisition Project) Series 2008a and Certain Other Actions in Connection Therewith and Repealing Resolution No. 08-031 RECOMMENDED ACTION: Information Only Briefing Item Recommended Motion Staff recommends the adoption of Resolution No. 08-055 and authorization to proceed with the sale of tax-exempt Certificates of Participation (COPs) to obtain financing to reimburse the District for its cost of acquiring approximately 8.0 acres of property located on 66th Avenue, in Oakland, CA (the District’s Property) and to finance certain improvements (the Improvements) to the Property. The District previously purchased approximately 16.26 acres of property located at 66th Avenue with its own funds and will be partially reimbursed from the sale of the COPs for those costs, as well as a portion of its acquisition costs and potential improvement costs. Fiscal Impact: Not to exceed $15 million, including reimbursement for a portion of the costs incurred in acquiring the property. BOARD ACTION: Approved as Recommended [ ] Other [ ] Approved with Modification(s) [ ] The above order was passed on: . Linda A. Nemeroff, District Secretary By GC Memo No. 08-213 Meeting Date: September 10, 2008 Page 2 of 4 Background/Discussion: The Special Meeting This is a special joint meeting of the AC Transit Board of Directors and the Finance Corporation Board of Directors. -

Page 1 of 279 FLORIDA LRC DECISIONS

FLORIDA LRC DECISIONS. January 01, 2012 to Date 2019/06/19 TITLE / EDITION OR ISSUE / AUTHOR OR EDITOR ACTION RULE MEETING (Titles beginning with "A", "An", or "The" will be listed according to the (Rejected / AUTH. DATE second/next word in title.) Approved) (Rejectio (YYYY/MM/DD) ns) 10 DAI THOU TUONG TRUNG QUAC. BY DONG VAN. REJECTED 3D 2017/07/06 10 DAI VAN HAO TRUNG QUOC. PUBLISHER NHA XUAT BAN VAN HOC. REJECTED 3D 2017/07/06 10 POWER REPORTS. SUPPLEMENT TO MEN'S HEALTH REJECTED 3IJ 2013/03/28 10 WORST PSYCHOPATHS: THE MOST DEPRAVED KILLERS IN HISTORY. BY VICTOR REJECTED 3M 2017/06/01 MCQUEEN. 100 + YEARS OF CASE LAW PROVIDING RIGHTS TO TRAVEL ON ROADS WITHOUT A APPROVED 2018/08/09 LICENSE. 100 AMAZING FACTS ABOUT THE NEGRO. BY J. A. ROGERS. APPROVED 2015/10/14 100 BEST SOLITAIRE GAMES. BY SLOANE LEE, ETAL REJECTED 3M 2013/07/17 100 CARD GAMES FOR ALL THE FAMILY. BY JEREMY HARWOOD. REJECTED 3M 2016/06/22 100 COOL MUSHROOMS. BY MICHAEL KUO & ANDY METHVEN. REJECTED 3C 2019/02/06 100 DEADLY SKILLS SURVIVAL EDITION. BY CLINT EVERSON, NAVEL SEAL, RET. REJECTED 3M 2018/09/12 100 HOT AND SEXY STORIES. BY ANTONIA ALLUPATO. © 2012. APPROVED 2014/12/17 100 HOT SEX POSITIONS. BY TRACEY COX. REJECTED 3I 3J 2014/12/17 100 MOST INFAMOUS CRIMINALS. BY JO DURDEN SMITH. APPROVED 2019/01/09 100 NO- EQUIPMENT WORKOUTS. BY NEILA REY. REJECTED 3M 2018/03/21 100 WAYS TO WIN A TEN-SPOT. BY PAUL ZENON REJECTED 3E, 3M 2015/09/09 1000 BIKER TATTOOS. -

Lower for Even Longer: What Does the Low Interest Rate Economy Mean for Insurers?

September 2020 Lower for even longer: what does the low interest rate economy mean for insurers? 01 Executive summary 02 Key takeaways 03 Lower interest rates for even longer 07 Non-life insurers unable to offset low interest rates pre COVID-19 11 Low for longer: very negative for life insurers 17 Managing interest rate risks 20 Conclusion Executive summary Unconventional monetary policy and The fallout from the COVID-19 crisis has put new pressure on already low interest negative interest rates are here to stay. rates, which were facing a structural decline even before pandemic outbreak. The massive monetary and fiscal response to the ensuing lockdown measures has further pressured yields. The rise of implicit or explicit yield curve control and also redesigns of monetary policy frameworks suggest that low interest rates are set to stay, for even longer. In this environment, we forecast that US 10-year yields will be at 1%, and German yields at around –0.4% by year-end 2020 and 2021. Lower for longer is the new norm that insurers will need to cope with. Non-life insurers need to improve their Empirical analysis across the major markets shows a strong long-term relationship underwriting margins significantly to between the combined ratio in non-life insurance and nominal interest rates. During cope with ultra-low interest rates. periods of lower rates, weaker investment returns need to be offset by stronger underwriting results. Before COVID-19, most major markets were already in a prolonged phase of below-average profitability. In the last decade, the average ROE of the G7 markets in our analysis was relatively low at around 7%, reflecting a prolonged period of soft underwriting conditions, weak investment performance, and a high level of capital funds. -

The General Public License Version 3.0: Making Or Breaking the FOSS Movement Clark D

Michigan Telecommunications and Technology Law Review Volume 14 | Issue 2 2008 The General Public License Version 3.0: Making or Breaking the FOSS Movement Clark D. Asay Follow this and additional works at: http://repository.law.umich.edu/mttlr Part of the Computer Law Commons, and the Science and Technology Law Commons Recommended Citation Clark D. Asay, The General Public License Version 3.0: Making or Breaking the FOSS Movement, 14 Mich. Telecomm. & Tech. L. Rev. 265 (2008). Available at: http://repository.law.umich.edu/mttlr/vol14/iss2/1 This Article is brought to you for free and open access by the Journals at University of Michigan Law School Scholarship Repository. It has been accepted for inclusion in Michigan Telecommunications and Technology Law Review by an authorized editor of University of Michigan Law School Scholarship Repository. For more information, please contact [email protected]. THE GENERAL PUBLIC LICENSE VERSION 3.0: MAKING OR BREAKING THE FOSS MOVEMENT? Clark D. Asay* Cite as: Clark D. Asay, The GeneralPublic License Version 3.0: Making or Breaking the Foss Movement? 14 MICH. TELECOMM. TECH. L. REV. 265 (2008), available at http://www.mttlr.org/volfourteen/asay.pdf I. INTRODUCTION ......................................................................... 266 II. FREE SOFTWARE V. OPEN SOURCE ........................................... 268 A. The FSF's Vision of Free Software..................................... 268 B. The OSI's Vision: A Different Movement? ......................... 270 C. PracticalDifferences? ....................................................... 271 III. G PLv3: ITS T ERM S................................................................... 274 A. GPLv3 's Anti-DRM Section ............................................... 274 1. Its C ontents ................................................................. 274 2. FSF's Position on DRM .............................................. 276 3. The Other Side of the Coin? OSI Sympathizers ........