Lower for Even Longer: What Does the Low Interest Rate Economy Mean for Insurers?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What Is Your Client's

Strength Since 1906 Midland National Midland National’s story is a classic example of American perseverance and ingenuity. Since 1906, Midland National has survived and thrived through two world wars, the Great Depression, the Dust Bowl, Products At-A-Glance and multiple recessions. Now with over 100 years under its belt, Midland National holds over one million life insurance and annuity policies with assets of over $44 billion. Source: Midland National 2015 Annual Report. • A+ (Superior) A.M. Best A.M. Best is a large third‐party independent reporting and rating company that rates an insurance company on the basis of the company’s financial strength, operating performance and ability to meet its obligations What is your client’s to policyholders. A+ is the second highest rating out of 15 categories and was affirmed for Midland National Life Insurance Company as part of Sammons Financial Group on July 14, 2016. For the latest rating, access www.ambest.com. • A+ (Strong) Standard & Poor’s Standard and Poor’s awarded its “A+” (Strong) rating for insurer financial strength on February 26, 2009 and affirmed on July 2, 2015 to Midland National Life Insurance Company, as part of Sammons Financial Group. The “A+” (Strong) rating is the fifth highest out of 22 available ratings. FOCUS? Questions? Need illustration help? Call our Sales Support team at 800-843-3316 ext. 32150. Protection...Growth...Flexibility... Midland National has a product for every focus. Administrative Office • One Sammons Plaza • Sioux Falls, SD 57193 MidlandNational.com -

Quarterly CPS1 Performance Flier

Take a look at Horace Mann's Capital Premier Series I An annuity offers some significant features and guarantees. As life expectancies increase, a key retirement concern is outliving your money. With an annuity you have the opportunity to choose lifetime income options, which would supply you with income you are guaranteed not to outlive. In addition, if you die before you retire, the guaranteed minimum death benefit provides some safeguards for your family. With Horace Mann Life Insurance Company's Capital Premier Series 1 (CPS 1) group variable annuity you get that and more. Horace Mann has partnered with a number of well-known investment firms to provide educators a full range of investment options that span a wide spectrum of investment styles. From large company growth to bond options, we can help match your personal investment comfort level with the appropriate investment options. You can re-allocate your money, use dollar-cost-averaging, or use systematic rebalancing to maintain your desired investment strategy. You can also allocate contributions to a fixed account with a guaranteed interest rate. Keep a long-range outlook A variable annuity is an insurance product designed to help meet retirement needs and should be seen as part of a long-term retirement plan. However, we understand investors may want to monitor the performance results of the investment options available within our variable annuities. Therefore, we provide these monthly performance updates. Take a few minutes to review the results; we caution you to not make a purchase or allocation decision based solely on the numbers in the following tables. -

Will of Dame Anne Packington.Pdf

TNA PROB/11/47 Will of Dame Anne Packington In the name of the father and of the sonne and of the holy ghoste The xxvjth daie of the monneth of Aprell in the yere of incarnacion of our Lorde Jesus Christe 1563. I Dame Anne Packington Widdow late the wief of Sir John Pakington knight deceased being in the hole mynde and in health of boddie blessed be almightie god remembringe and calling to mynde the mutablitie of this transitory lief knowing my selfe mortall and subiecte to death whereunto every creature is borne. Doe make ordeine and declare this my present Testament and last will in manner and fourme followinge ffirst and principally I bequeath my soule to the blissed Trinitie and the holly company of heaven my bodie to be buried in that parishe churche Where it shall please god to ende my lief or where my executors shall thinke mete at thende of the highe aulter Wheras the sepulture was vsed moste commonly to stande if the rome and place maie be suffered or els at thother ende of the high alter And I will that my executors shall cause a Tombe of marble to be made and sett over my bodie for the making Wherof I bequeath twenty markes or more if it come to more/ And I bequethe to xxti poore men and women every one a blacke gowne of an honest clothe or good frise Wherof xij of them shall beare at my buriall xij torches and iiij of them shall beare forever greate tapers if the lawes of this Realme will so permitt and suffer Item I bequeath amonge the poore househoulders dwelling in that parrish where I shalbe buried twelve pennce a pece/ And among all other people comming to my buriall ij d. -

What Amounts to a Surrender by Operation of Law?

September 2010 Review Property @ction Welcome to the Fifth Edition of the Quarterly Review from Hammonds’ Property@ction Team. In this issue we will look at the following: (i) What amounts to a surrender by operation of law; (ii) Does it do what it says on the tin? - full repairing and insuring leases; (iii) Double trouble; (iv) Compulsory purchase orders; (v) Adverse possession; We welcome all contributions to this review and if you would like to discuss this further please contact any of the editorial team. What amounts to a surrender by operation of law? Where a landlord and tenant bring a lease to an end, they usually do so by completing a deed of surrender. However, sometimes, it may be implied that a surrender has occurred. The term commonly used for an implied surrender is a surrender “by operation of law”. In a recent case, QFS Scaffolding v Sable1 , the court considered some of the relevant principles for a surrender by operation of law to take place. Facts The landlord (Mr and Mrs Sable) granted a lease to a tenant company which eventually entered into administration. Prior to the administration, a new company (QFS) was formed with a view to taking over the tenant’s business. The Sables negotiated terms for a new lease with QFS who, in fact, went into occupation. However, the negotiations faltered and no new lease was entered into. Instead, QFS asked the administrator of the tenant to assign the lease to it and, as a result of this request, a deed of assignment was executed. -

Understanding the Religious Terrorism of Boko Haram in Nigeria

African Study Monographs, 34 (2): 65–84, August 2013 65 NO RETREAT, NO SURRENDER: UNDERSTANDING THE RELIGIOUS TERRORISM OF BOKO HARAM IN NIGERIA Daniel Egiegba AGBIBOA Oxford Department of International Development, University of Oxford ABSTRACT Boko Haram, a radical Islamist group from northeastern Nigeria, has caused severe destruction in Nigeria since 2009. The threat posed by the extremist group has been described by the present Nigerian President as worse than that of Nigeria’s civil war in the 1960s. A major drawback in the Boko Haram literature to date is that much effort has been spent to remedy the problem in lieu of understanding it. This paper attempts to bridge this important gap in existing literaure by exploring the role of religion as a force of mobilisation as well as an identity marker in Nigeria, and showing how the practice and perception of religion are implicated in the ongoing terrorism of Boko Haram. In addition, the paper draws on the relative deprivation theory to understand why Boko Haram rebels and to argue that religion is not always a sufficient reason for explaining the onset of religious terrorism. Key Words: Boko Haram; Nigeria; Religious terrorism; Identity; Relative deprivation theory. INTRODUCTION Since 2009, bombings and shootings by the Nigerian extremist group Boko Haram have targeted Nigeria’s religious and ethnic fault lines in an apparently escalating bid to hurt the nation’s stability. A spate of increasingly coordinated and sophisticated attacks against churches from December 2011 through July 2012 suggests a strategy of provocation through which the group seeks to spark wide- scale sectarian violence that will strike at the foundations of the country (Forest, 2012). -

MSME) During COVID 19 Outbreak in South Sulawesi Province Indonesia

May – June 2020 ISSN: 0193-4120 Page No. 26707 - 26721 Factors Influencing Resilience of Micro Small and Medium Entrepreneur (MSME) during COVID 19 Outbreak in South Sulawesi Province Indonesia Muhammad Hidayat¹, Fitriani Latief², DaraAyu Nianty³ ShandraBahasoan⁴AndiWidiawati⁵ ¹²³⁴⁵STIE Nobel Indonesia Article Info Abstract: Volume 83 Aim: To find out factors influencing resilience of Micro Small and Medium Page Number: 26707 – 26721 Entrepreneur MSME entrepreneurs during the worlwide spread of COVID-19 Publication Issue: pandemic, this study aims at empirically examine the influence of entrepreneurial May - June 2020 personality in utilizing technology and government support for business resilience through crisis management as an intervening variable. Research design, data and method:This research is a quantitative study analyzing sample of 97 small and medium enterprisesactors in South Sulawesi, Indonesia, chosen by using purposive sampling. The main data in this study is results of questionnaires distributed to respondents which is analyzed by using Partial Least Square (PLS analysis). Results and Findings: This study proves a positive and significant relationship between entrepreneurship personlity and crisis management. Thereis no significant relationship between utilizing of technology toward crisis management. There is a Article History positive and significant relationship between government supporttoward crisis Article Received: 11 May 2020 management. This research also proves a positive and significant influence between Revised: 19 May 2020 crisis management on business resilience. Accepted: 29 May 2020 Publication: 12 June 2020 Keywords: Entrepreneurship Characteristic, Technology Utilization, Government Support , Business Resilience I. INTRODUCTION viruses that infect the respiratory system. This viral infection is called covid-19. The world has been being troubled by the Coronavirus causes common cold,amild to appearance of corona virus. -

GOLD Package Channel & VOD List

GOLD Package Channel & VOD List: incl Entertainment & Video Club (VOD), Music Club, Sports, Adult Note: This list is accurate up to 1st Aug 2018, but each week we add more new Movies & TV Series to our Video Club, and often add additional channels, so if there’s a channel missing you really wanted, please ask as it may already have been added. Note2: This list does NOT include our PLEX Club, which you get FREE with GOLD and PLATINUM Packages. PLEX Club adds another 500+ Movies & Box Sets, and you can ‘request’ something to be added to PLEX Club, and if we can source it, your wish will be granted. ♫: Music Choice ♫: Music Choice ♫: Music Choice ALTERNATIVE ♫: Music Choice ALTERNATIVE ♫: Music Choice DANCE EDM ♫: Music Choice DANCE EDM ♫: Music Choice Dance HD ♫: Music Choice Dance HD ♫: Music Choice HIP HOP R&B ♫: Music Choice HIP HOP R&B ♫: Music Choice Hip-Hop And R&B HD ♫: Music Choice Hip-Hop And R&B HD ♫: Music Choice Hit HD ♫: Music Choice Hit HD ♫: Music Choice HIT LIST ♫: Music Choice HIT LIST ♫: Music Choice LATINO POP ♫: Music Choice LATINO POP ♫: Music Choice MC PLAY ♫: Music Choice MC PLAY ♫: Music Choice MEXICANA ♫: Music Choice MEXICANA ♫: Music Choice Pop & Country HD ♫: Music Choice Pop & Country HD ♫: Music Choice Pop Hits HD ♫: Music Choice Pop Hits HD ♫: Music Choice Pop Latino HD ♫: Music Choice Pop Latino HD ♫: Music Choice R&B SOUL ♫: Music Choice R&B SOUL ♫: Music Choice RAP ♫: Music Choice RAP ♫: Music Choice Rap 2K HD ♫: Music Choice Rap 2K HD ♫: Music Choice Rock HD ♫: Music Choice -

Resolution No

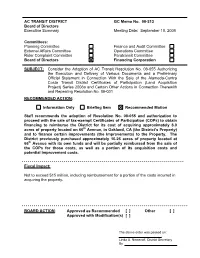

AC TRANSIT DISTRICT GC Memo No. 08-213 Board of Directors Executive Summary Meeting Date: September 10, 2008 Committees: Planning Committee Finance and Audit Committee External Affairs Committee Operations Committee Rider Complaint Committee Paratransit Committee Board of Directors Financing Corporation SUBJECT: Consider the Adoption of AC Transit Resolution No. 08-055 Authorizing the Execution and Delivery of Various Documents and a Preliminary Official Statement in Connection With the Sale of the Alameda-Contra Costa Transit District Certificates of Participation (Land Acquisition Project) Series 2008a and Certain Other Actions in Connection Therewith and Repealing Resolution No. 08-031 RECOMMENDED ACTION: Information Only Briefing Item Recommended Motion Staff recommends the adoption of Resolution No. 08-055 and authorization to proceed with the sale of tax-exempt Certificates of Participation (COPs) to obtain financing to reimburse the District for its cost of acquiring approximately 8.0 acres of property located on 66th Avenue, in Oakland, CA (the District’s Property) and to finance certain improvements (the Improvements) to the Property. The District previously purchased approximately 16.26 acres of property located at 66th Avenue with its own funds and will be partially reimbursed from the sale of the COPs for those costs, as well as a portion of its acquisition costs and potential improvement costs. Fiscal Impact: Not to exceed $15 million, including reimbursement for a portion of the costs incurred in acquiring the property. BOARD ACTION: Approved as Recommended [ ] Other [ ] Approved with Modification(s) [ ] The above order was passed on: . Linda A. Nemeroff, District Secretary By GC Memo No. 08-213 Meeting Date: September 10, 2008 Page 2 of 4 Background/Discussion: The Special Meeting This is a special joint meeting of the AC Transit Board of Directors and the Finance Corporation Board of Directors. -

DNA Test Report: DNA - HC-HSF4

Health - DNA Test Report: DNA - HC-HSF4 Pastoral - Australian Shepherd Dog Name Reg No DOB Sex Sire Dam Test Date Test Result ABODANDY NIKO JACAROO BOO AK02001703 26/05/2009 Bitch YULIA EVEREADY DANDY OF SHEPALIAN BAJIMBA AT ABODANDY 26/08/2014 Clear ABODANDY ACCRA BLU LIGHTENING AH04474501 08/10/2007 Bitch HEATHERHILL SHOCK N AWE (IMP ACCRA IMNO MUGGLE 04/03/2010 Clear USA) ACCRA WISHES N'SPELLS AS02712504 23/06/2015 Bitch LISKARN NO SECRET WE LOVE BLEUROYAL BEWITCHING BELLE 12/03/2019 Clear YOU WITH ACCRA (IMP CHL) ALADDIN'S VIVA LA FRANCE Bitch MEDALIONS FIRE BY ALADDIN ALADDIN'S HOT EVENT 08/06/2009 Clear ALLMARK CARELESS WHISPER AH00498001 09/10/2006 Bitch BAYSHORE'S TEARS OF A CLOWN OZZYPOOL MOLLY MALONE AT 27/08/2010 Clear ALLMARK ALLMARK DON'T STOP ME NOW AQ01809410 06/04/2013 Dog BAYSHORE STONEHAVEN CAT ALLMARK CARELESS WHISPER 25/08/2017 Clear BURGLAR (IMP USA) ALLMARK FOREIGN AFFAIR AM00615702 05/11/2010 Bitch DAZZLE'S BILL-A-BING BILL-A- ALLMARK CARELESS WHISPER 08/08/2013 Clear BONG ALLMARK GRACE JONES AK01434908 01/04/2009 Bitch HEATHERHILL SHOCK N AWE (IMP OZZYPOOL MOLLY MALONE AT 19/03/2012 Clear USA) ALLMARK ALLMARK ITALIAN KISSES FOR APPLEFIRE AP01167601 03/02/2012 Bitch GOD'S GREAT BANANA SKIN ALLMARK CARELESS WHISPER 14/08/2013 Clear ALLMARK JOIN THE CLAN AT MISTYHOLLY AQ01809407 06/04/2013 Bitch BAYSHORE STONEHAVEN CAT ALLMARK CARELESS WHISPER 07/07/2015 Clear BURGLAR (IMP USA) ALLMARK MASERATI AT MEITZA AP01167605 03/02/2012 Dog GOD'S GREAT BANANA SKIN ALLMARK CARELESS WHISPER 27/08/2015 Clear ALLMARK MUFFIN MUNCHER -

THE WHEN Like the Had Aavsd from the Geiser

V A INDIANAPQMS JOUBMA PRICE FIVE CENTS. INDIANAPOLIS, FRIDAY MORNING, AUGUST 17, 1888. SUBSGEISEH MHCI3 ITVE CENTS. WHEN" INDICATIONS. COLLIDED IN A DENSE FOG Copenhagen. Those that were saved lost all yold, Ole Christoffsen, Carolina, Carl and Fritz NO SURRENDER TO FRANCE their effects, and even all tneir clothing, except Christensen, Annie and Oscar Wieicer. Jens NO PALAVER FRIDAY Kaln and local storms; clearing their night-wea- r. Hansen. Hilda Soldberg. Louise Andersen, In the northsrn part of tha State; generally CdDt A. Albers. of the Wieland. tells the fol- Laritz Kummendahl, Annie Thompson, Mads cooler. lowing story: 'At 10 o'clock on the morning of Hansen, Gust Adler, Paul Taulsen, Annie and The Steamers Geiser and Thinvalla Aug. 14 we passed some wreckage floating in the Kirsten Sovensen and Miss E. Peterson. Plain Speech by Germany's Emperor at sea and suspected that an accident had hap- When one offers what any Crash Together Rear Sable Island. pened somewhere sear us. A little later we A 1.1st uf th Lost. a Mon"ent Unveiling at Frankfort. WE.RISE TO REMARK sailed through a sea of oil and sighted a broken New York, Aug. lG.-- Tho following is the of buyer can see is an absolute boat the Geiser. About 11:30 we sighted a which can be obtained to- ateemer to the northward, about eight miles off, best list of the lost and seeing night is made by striking off the names of "bargain the greatest bargain So does tho thermometer. It re- the had a flag of distress up we ran It The Armies oi'tbe Empire Will Perish cn the The Vessels Collide with Great Force, a Hnza down to her. -

Mpandla, 20 Cents and My- Self Nave Been Co-Ordinating MK Actions in the Durban Area Since the Beginning of the Year. Tna- Bane

We reached Umlazi at 0600hrs and decided that the material left in KwaMashu would be NO SURRENDER fetched that afternoon. When Mpandla came to collect me and The 'Citizen' of September 9 1986 reported: "Weapons ... were found in a car in which four suspected ANC terrorists were killed in a shootout with police Thabane to fetch the material in Durban on Sunday night. The men were shot dead in a firefight with the I was somehow occupied at police after being cornered... At the time the police, including members of the home and could not come with reaction unit of the security police, were investigating an incident in which a them. They then decided to take KwaMashu house was fired upon and attacked with three hand grenades . ." 20 cents and Mbongeni. True, four MK combatants fell heroically that Sunday. What the "Citizens" deliberately forgets to mention is that they did not die alone. They took many boer soldiers and policemen with them. This is the battle in which Thabane SPOTTED MemeJa, alias Bridge Thwala, lost his life. Below follows the story as related by When leaving KwaMashu the one member of the unit. blue cressida they were riding in was spotted by the police. That Mpandla, 20 cents and my could have been due to the fact self nave been co-ordinating MK that the area was heavily patrol actions in the Durban area since led by the police following the the beginning of the year. Tna- bane is one of the comrades attack on Shabalala's house or who were trained outside the some people could have seen the country and sent to Durban. -

“Aware-Settler” Biblical Studies: Breaking Claims of Textual Ownership Matthew R

“Aware-Settler” Biblical Studies: Breaking Claims of Textual Ownership Matthew R. Anderson [email protected] ABSTRACT “Aware-Settler” is a term coined here to describe the various hermeneutics that arise as increasingly, non-Indigenous biblical scholars take seriously that their research is done on colonized Land. Paying special attention to the principle of possessiveness, the article suggests breaking stubborn Settler-scholar hid- den-default assumptions of ownership, proposing instead that biblical texts might be understood as another form of “Treaty territory.” Indigenous scholars’ common emphases on Landedness, relationality, spirituality, and community good, can inform methodologies employed by Settler biblical scholars. These hermeneutical principles, learned in a contact zone characterized by attention to reciprocity and respect, are employed in a brief look at Matthew 28:25–28. The so-called Great Commission is a foundational text of colonialism; many Indigenous scholars have judged it as “unreadable.” For that reason it provides a particularly appropri- ate test-case for applying Aware-Settler hermeneutics focussed on breaking claims of identity and owner- ship. KEYWORDS aware-settler, Indigenous, settler, hermeneutics, biblical scholarship or her Presidential address at the 2018 meeting of the Canadian Society of Biblical Studies, FChristine Mitchell spoke on “Reading Biblical Conquest Stories on Treaty 4 Land: Working To- wards Reconciliation.”1 She noted that already thirty years before, Robert Warrior, an Indigenous