CTA AC NO. 182 Page 2 of 21

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

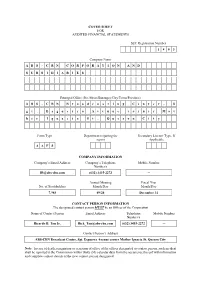

COVER SHEET for AUDITED FINANCIAL STATEMENTS SEC Registration Number 1 8 0 3 Company Name A

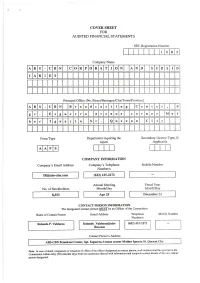

COVER SHEET FOR AUDITED FINANCIAL STATEMENTS SEC Registration Number 1 8 0 3 Company Name A B S - C B N C O R P O R A T I O N A N D S U B S I D I A R I E S Principal Office (No./Street/Barangay/City/Town/Province) A B S - C B N B r o a d c a s t i n g C e n t e r , S g t . E s g u e r r a A v e n u e c o r n e r M o t h e r I g n a c i a S t . Q u e z o n C i t y Form Type Department requiring the Secondary License Type, If report Applicable A A F S COMPANY INFORMATION Company’s Email Address Company’s Telephone Mobile Number Number/s [email protected] (632) 3415-2272 ─ Annual Meeting Fiscal Year No. of Stockholders Month/Day Month/Day 7,985 09/24 December 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Mobile Number Number/s Ricardo B. Tan Jr. [email protected] (632) 3415-2272 ─ Contact Person’s Address ABS-CBN Broadcast Center, Sgt. Esguerra Avenue corner Mother Ignacia St. Quezon City Note: In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

Philippines in View Philippines Tv Industry-In-View

PHILIPPINES IN VIEW PHILIPPINES TV INDUSTRY-IN-VIEW Table of Contents PREFACE ................................................................................................................................................................ 5 1. EXECUTIVE SUMMARY ................................................................................................................................... 6 1.1. MARKET OVERVIEW .......................................................................................................................................... 6 1.2. PAY-TV MARKET ESTIMATES ............................................................................................................................... 6 1.3. PAY-TV OPERATORS .......................................................................................................................................... 6 1.4. PAY-TV AVERAGE REVENUE PER USER (ARPU) ...................................................................................................... 7 1.5. PAY-TV CONTENT AND PROGRAMMING ................................................................................................................ 7 1.6. ADOPTION OF DTT, OTT AND VIDEO-ON-DEMAND PLATFORMS ............................................................................... 7 1.7. PIRACY AND UNAUTHORIZED DISTRIBUTION ........................................................................................................... 8 1.8. REGULATORY ENVIRONMENT .............................................................................................................................. -

Cr07671 Abs 17Q 3Q 2020 Abs-Cbn

COVER SHEET SEC Registration Number 1 8 0 3 Company Name A B S - C B N C O R P O R A T I O N A N D S U B S I D I A R I E S Principal Office (No./Street/Barangay/City/Town/Province) A B S - C B N B r o a d c a s t C e n t e r , S g t . E s g u e r r a A v e n u e c o r n e r M o t h e r I g n a c i a S t . Q u e u z o n C i t y Form Type Department requiring the report Secondary License Type, If Applicable 1 7 Q COMPANY INFORMATION Company’s Email Address Company’s Telephone Number/s Mobile Number 415-2272 Annual Meeting Fiscal Year No. of Stockholders Month/Day Month/Day 6,547 September 24 September 30 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number Aldrin M. Cerrado [email protected] 415-2272 Contact Person’s Address ABS-CBN Broadcast Center, Sgt. Esguerra Avenue corner Mother Ignacia St. Quezon City Note: In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

ABS-CBN Broadcasting Corporation Sgt

ABS-CBN Broadcasting Corporation Sgt. Esguerra Avenue, Quezon City, Philippines April 19, 2010 Philippine Stock Exchange, Inc. Exchange Road, Ortigas Center Pasig City Attention: Ms. Janet A. Encarnacion Head, Disclosure Department Dear Ms. Encarnacion, We hereby submit to the Philippine Stock Exchange (PSE) the Definitive Information Statement of ABS- CBN Broadcasting Corporation (ABS-CBN or the Company). Based on the Securities and Exchange Commission’s (SEC) letter dated April 16, 2010, which provided a list of prescribed amendments to the Preliminary Information Statement the Company submitted to the SEC and the PSE last April 13, 2010, we made the following revisions: 1. Updated to March 31, 2010 the following information: a. Number of Shares Outstanding on page 7. b. Security Ownership of Certain Record and Beneficial Owners of more than 5% on page 7. c. Security Ownership of Directors and Management on page 8. d. List of Directors and Executive Officers on pages 9 to 18. e. Top 20 Shareholders on page 50. 2. Disclosure of any relationship of Mr. Oscar M. Lopez with any of the nominees for Independent Director on page 9. 3. Compliance with the five year rotation requirement of external auditor on page 20. 4. Brief reason(s) for and the general effect of the proposed amendment of the Company’s Articles of Incorporation on page 22. 5. Submission of 1st Quarter 2010 report on page 42. 6. Share price information as of the latest practicable trading date (April 19, 2010) on page 49. 7. Disclosure on dividend policy and restrictions on page 49. Thank you. -

SKY Cable Corporation Implements TCS HOBSTM Platform to Drive Digital Transformation

SKY Cable Corporation implements TCS HOBSTM platform to drive digital transformation Abstract Client SKY Cable Corporation Digital transformation is imperative in the media and entertainment industry as consumers demand a wider portfolio of products and services, backed by Industry personalized unified customer experiences across channels and touchpoints. Media and Entertainment SKY Cable Corporation wanted to support both traditional and new age digital Offering services across all its business processes, enable automation to drive operational Implementation of efficiency and rapidly introduce changes without hampering agility. SKY Cable TCS HOBS open partnered with Tata Consultancy Services to implement TCS HOBSTM on Azure. platform on cloud for the client’s DTH The solution’s catalog-centric architecture provided SKY Cable with a one stop prepaid line of business solution to manage business processes across product portfolio management, and for driving their customer management, order management, partner management, wallet digital transformation management, voucher management and inventory management. journey “The TCS HOBS platform has not only provided SKY Cable with a stable platform to support our DTH service product growth which we could never achieve on our old one, but also given its breadth and depth of features has provided us the base for all of our prepaid and postpaid products and services going forward.” Chief Information Officer, SKY Cable About the Client Business Challenge SKY Cable Corporation is the pay SKY Cable needed to increase its business agility and maintain its market television and broadband arm of leadership in the rapidly evolving communications service provider landscape of ABS-CBN, Philippines’ leading DTH, broadband and cable TV services. -

Accs Cfs1218 Abscbn Corporation and Subs Filed.Pdf

ABS-CBN CORPORATION ANNUAL REPORT PART I - BUSINESS AND GENERAL INFORMATION 3 1. Business Overview 3 1.1. Historical Background 3 1.2. Lines of Business 3 1.3. Subsidiaries 6 1.4. Significant Philippine Associates and Affiliates 8 1.5. Competition 8 1.6. Patents, Trademarks, Licenses, Franchises, Concessions, Royalty 12 1.7. Corporate Social Responsibility 16 1.8. Principal Competitive Strengths of the Company 18 1.9. Key Strategies and Objectives 21 1.10. Transactions with Related Parties 19 1.11. Risks Relating to the Company 20 2. Properties 20 2.1. Head Office 20 2.2. Local and Regional Properties 23 2.3. Leased Properties: 25 3. Legal Proceedings 207 4. Submission of Matters to a Vote of Security Holders 28 PART II - OPERATIONAL AND FINANCIAL INFORMATION 30 5. Market for Issuer’s Common Equity and Related Stockholder Matters 28 6. Management’s Discussion and Analysis of Financial Condition and Results of Operations 284 7. Financial Statements 34 8. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure 34 PART III - CONTROL AND COMPENSATION INFORMATION Error! Bookmark not defined. 9. Directors and Executive Officers of the Issuer 35 9.1. Board of Directors 35 9.2. Executive / Corporate Officers 39 10. Executive Compensation 44 11. Security Ownership of Certain Beneficial Owners and Management 46 12. Certain Relationships and Related Transactions 49 PART IV - CORPORATE GOVERNANCE 52 13. Corporate Governance 52 PART V - EXHIBITS and SCHEDULES 65 14. Exhibits and Reports on SEC Form 17-C 65 SIGNATURES 65 PART I - BUSINESS AND GENERAL INFORMATION 1. -

Philippines US$28.7M Revenue in 2018, Accumulated Loss Tops $378M

9-22 September C NTENT 2019 www.contentasia.tv l www.contentasiasummit.com NBC orders Sky Castle pilot U.S. breakthrough for Korea’s JTBC U.S. network NBC has ordered a pilot based on Korean series Sky Castle from Korean network JTBC/Drama House and local indie production company HB Entertainment. A network spokesman in the U.S. said the pilot was in develop- ment under the auspices of Berlanti Pro- ductions in association with Warner Bros Television, and was not a series order. The full story is on page 2 Singapore’s Toggle ups short-form Flix Snip deal adds 29 titles, pushes domestic content barriers Nine-month old global short-form con- tent service, Flix Snip, has rolled out in Asia in partnership with Singapore’s Me- diacorp, streaming 29 international titles with themes that put Mediacorp among the country’s most progressive broad- casters. The full story is on page 3 ContentAsia Summit Thanks to our partner StarHub Ch 434 Who said what... NOW AVAILABLE & who was there FOR ALL ASIAN TERRITORIES! The 11th ContentAsia Summit wrapped at the end of August with one clear mes- sage: Life has never been better for Asian storytellers. Here’s some of what was said. There’s more in our Mipcom issue, out in gustoworldwidemedia.com gustotv.tv [email protected] early October. C NTENTASIA 9-22 September 2019 9-22 September 2019 Page 2. Page 2. NBC orders Sky Castle pilot U.S. breakthrough for Korea’s JTBC NBCUniversal has ordered a pilot based on Korean series Sky Castle from Korean network JTBC/Drama House and local in- die production company HB Entertainment. -

Philippines in View Cc

PHILIPPINES IN VIEW 2021 Table of Contents Chapter 1: Overall TV Market Environment ........................................................................ 2 Chapter 2: Online Curated Content (OCC) Market Environment ....................................... 13 Chapter 3: Traditional Pay TV Market Environment ......................................................... 45 Chapter 4: Piracy in the Philippines: Piracy and Unauthorized Distribution for Online and Traditional TV .................................................................................................................. 97 Chapter 5: Regulatory Environment for Digital Content ........................................................ 102 References ..................................................................................................................... 113 Annex A: Top TV Programs ............................................................................................. 121 Annex B: Glossary of Acronyms ...................................................................................... 125 1 Chapter 1: Overall TV Market Environment The disruptions to the Philippine television (TV) industry over recent years are many and the most recent of them, the 2019 coronavirus pandemic (COVID-19), has not made things easier. In June 2020, the World Economic Forum cited the myriad ways the pandemic has affected the media industry from content creators to distributors, saying that while consumer demand for content has skyrocketed due to lockdowns and the prevalence of remote -

Lopezlink April 2019

APRIL 2019 www.lopezlink.ph Happy birthday, OML! http://www.facebook.com/lopezlinkonline www.twitter.com/lopezlinkph Isang milyong kwento na puno ng saya, aksyon, kilig at pag-asa mula sa SKYdirect Story on page 6 Seeds of WSummer…page 12 First Gen recurring Hope: Pillow skin care earnings up 51%…page 2 talk…page 9 tips…page 12 Lopezlink April 2019 FPH attributable First Gen recurring RNI up by 53% earnings up 51% FIRST Gen Corporation re- (P17.8 billion), or 16% to $2.0 “2018 was an exceptional FOR the year ended December FPH also increased by P4.4 primarily driven by higher sale ported recurring net income billion (P103.8 billion) from year for First Gen as we con- 31, 2018, recurring net income billion or 76%, from P5.9 bil- of electricity following favor- attributable to equity holders $1.7 billion (P86.0 billion) in cretized value from the sizable (RNI) attributable to First Phil- lion to P10.3 billion, reflect- able spot market prices and the of the parent of $243 million 2017. The natural gas portfo- investment made for the mod- ippine Holdings Corporation ing the growth in RNI slightly effectivity of the San Gabriel (P12.8 billion) in 2018. This was lio accounted for $1,240 mil- ern 420-MW San Gabriel nat- (FPH) reached P10.4 billion, reduced by net nonrecurring plant’s power supply agreement a 51%- or an $82-million (P4.6 lion (P65.1 billion), or 63% of ural gas-fired power plant. This higher by P3.6 billion or 53% losses booked during the year with Meralco; higher comple- billion) surge from $161 million First Gen’s total consolidated was made in anticipation of the compared to last year’s P6.8 largely on account of unfavor- tion and sales booking of (P8.1 billion) in 2017, mainly revenues. -

Communication

Media - In general, "media" refers to various means of communication. Channels of communication that serve many diverse functions, such as offering a variety of entertainment with either mass or specialized appeal, communicating news and information, or displaying advertising messages. The media carry the advertisers' messages and serve as the vital link between the seller of a product or service and the consumer. Communication: "Any act by which one person gives to or receives from another person information about that person's needs, desires, perceptions, knowledge, or affective states. Communication may be intentional or unintentional, may involve conventional or unconventional signals, may take linguistic or nonlinguistic forms, and may occur through spoken or other modes." The Sender in the Communication Process "Two essential elements in every communication situation are the sender and the receiver. Thesender is anyone who wishes to convey an idea or concept to others, seek information, or express a thought or emotion. The receiver is the person to whom the message is sent. The sender encodes the idea by selecting symbols with which to compose a message. The message is the tangible formulation of the idea that is sent to the receiver. The message is sent through a channel, which is the communication carrier. The channel can be a formalreport, a telephone call, an e-mail message, or a face-to-face meeting. The receiver decodes the symbols to interpret the meaning of the message." "In the communication process, the role of receiveris, I believe, as important as that of sender. There are five receiver steps in the process of communication--Receive, Understand, Accept, Use, and Give a Feedback. -

20 MAR-4 P3«L

' ^'©KiCf of t|)r ferrrrtflrp EIGHTEENTH CONGRESS OF THE ) REPUBLIC OF THE PHILIPPINES ) First Regular Session ) 20 MAR-4 P3«l SENATE Introduced by Senators MANUEL "LUO" M. LAPID, SHERWIN GATCHALIAN, JOEL VILLANUEVA, MARIA LOURDES NANCY S. BINAY, JUAN MIGUEL F. ZUBIRI, SONNY ANGARA, RALPH G. RECTO, GRACE POE, and EMMANUEL "MANNY" PACQUIAO CONCURRENT RESOLUTION EXPRESSING THE SENSE OF THE CONGRESS TO ALLOW ABS-CBN BROADCASTING CORPORATION AND SKY CABLE CORPORATION TO OPERATE PENDING THE FINAL DETERMINATION OF THE RENEWAL OF THEIR RESPECTIVE FRANCHISES BY THE EIGHTEENTH CONGRESS THROUGH THE ISSUANCE OF THE APPROPRIATE PROVISIONAL AUTHORITY BY THE NATIONAL TELECOMMUNICATIONS COMMISSION 1 WHEREAS, by virtue of Republic Act No. 7966, ABS-CBN Broadcasting 2 Corporation was "granted a franchise to construct, operate and maintain, for 3 commercial purposes and in the public interest, television and radio broadcasting 4 stations in and throughout the Philippines, through microwave, satellite or whatever 5 means including the use of any new technologies in television and radio systems, 6 with the corresponding technological auxiliaries or facilities, special broadcast and 7 other broadcast distribution services and relay stations" for twenty-five (25) years 8 or until May 4, 2020; 9 WHEREAS, under Republic Act No. 7969, SKY Cable Corporation (formerly 10 Central CATV, Inc.), was granted a franchise "to construct, establish, install, 11 operate and maintain for commercial purposes and in the public interest, 12 community antennae television systems" for twenty-five (25) years or until May 4, 13 2020. 14 WHEREAS, as early as the 16th Congress, an attempt had been made to 15 renew the franchise of ABS-CBN through the filing of House Bill No. -

September 2018: SKYBIZ: Seizing the Momentum

SEPTEMBER 2018 www.lopezlink.ph Lopez Group celebrates 12 healthful years of Walk the Talk. Story on page 10. http://www.facebook.com/lopezlinkonline www.twitter.com/lopezlinkph SKYBIZ: Seizing theSKYBIZ Enterprise and MSME head Dickymomentum Liwanag, SKY Cable Regional Business Group head Ed Patron and National Sales head Kenneth Orlanes are men on a mis- sion. The three of them are key figures in the company’s objective to earn P2 billion in revenues by 2020. Turn to page 6 First Gen leads way The sound values Get help with your …page 2 of Devin Lopez …page 12 …page 9 to-do list! Lopezlink September 2018 Lopezlink September 2018 Biz News JANUARY TO JUNE 2018 FINANCIAL RESULTS (UNAUDITED, CONSOLIDATED) Net income attributable to equity ANC brings billionaire investor Lopez Holdings attributable Total revenues holders of the parent company net income at P.174B 2017 2018 % change 2017 2018 % change Kevin O’Leary to Manila By Carla Paras-Sison VENTURE capitalist and ABS-CBN P19.344B P18.936B -2 P1.455B P849.882M -42 entrepreneur Kevin O’Leary, EDC P17.747B P17.135B -3 P4.615B P3.366B -27 LOPEZ Holdings Corpora- ate First Philippine Holdings net income during the period. known as “Mr. Wonderful” in tion reported P2.174 billion in Corporation (FPH) accounted Unfavorable forex movement First Gen $853.995M $932.850M +10 $57.993M $84.861M +46 the business-themed program net income attributable to eq- for the results. during the period partially off- FPH P51.482B P58.674B +14 P2.516B P4.048B +61 “Shark Tank,” will be coming to uity holders of the parent for Unaudited consolidated rev- set the effect of growth in the Lopez Holdings P51.482B P58.674B +14 P1.763B P2.174B +23 Manila for the ANC Leader- the first six months of 2018.