Greece: Logistics & Industrial Market Snapshot

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Department Town Address Postcode Telephone Etoloakarnania Agrinio

Department Town Address Postcode Telephone Etoloakarnania Agrinio 1, Eirinis square, Dimitrakaki street 301 00 2641046346 Etoloakarnania Mesologgi 45, Charilaou Trikoupi street 302 00 2631022487 Etoloakarnania Nafpaktos 1, Athinon street 303 00 2634038210 Etoloakarnania Amfilohia Vasileos Karapanou street 305 00 2642023302 Argolida Argos 12, Danaou street 212 00 2751069042 Argolida Nafplio 35, Argous street 211 00 2752096478 Argolida Porto Heli Porto Heli Argolidas 210 61 2754052102 Arkardia Megalopoli 15, Kolokotroni street 222 00 2791021131 Arkardia Tripoli 48, Ethinikis Antistaseos street 221 00 2710243770 Arta Arta 129, Skoufa street 471 00 2681077020 Attica Athens 316, Acharnon street & 26 Atlantos street 112 52 2102930333 Attica Agios Dimitrios 54, Agiou Dimitriou street 173 41 2109753953 Attica Agios Dimitrios 276, Vouliagmenis avenue 173 43 2109818908 Attica Agios Dimitrios 9 - 11, Agiou Dimitriou street 173 43 2109764322 Attica Agia Paraskevi 429, Mesogeion avenue 153 43 2106006242 Attica Athens - Piraeus 153, Piraeus Avenue 118 53 2104815333 Attica Athens - Aristeidou 1, Aristeidou street 105 59 2103227778 Attica Athens 79, Alexandras avenue 114 74 2106426650 Attica Athens - Plateia Viktorias 2, Victoria square 104 34 2108220800 Attica Athens - Stadiou 7, Stadiou street 105 62 2103316892 Attica Egaleo 266, Iera Odos street 122 42 2105316671 126, Vasilissis Sofias street & 2, Feidippidou Attica Abelokipoi street 115 27 2106461200 Attica Amfiali 32, Pavlou Fissa street 187 57 2104324300 Attica Palaio Faliro 82, Amfitheas avenue -

Greek Energy Directory 2 0 1 6

) ENERGIA•gr Greek Energy Directory 2 0 1 6 t n e m Business The Oil Sector Natural Gas The Electricity SectorRenewable EnergyEnergy Sources Efficiency &The Co Genera2on Legal FrameworkResearch & DevelopDirectory TERNA ENERGY is a major player in the Renewable Energy Market and specifically in the development of Wind Parks, in Hydroelectric Projects, Solar Energy Plants as well as Waste to Energy and Biomass Projects, with presence in Greece, Europe and the USA. The total installed capacity of the Group accounts for 664 MW: 394 MW in Greece, 138 MW in the USA, 102 MW in Poland and 30 MW in Bulgaria, while 274 more MW are currently under development in Greece and abroad. Overall, the company operates, is constructing or has fully licensed 938 MW of RES installations in Europe and the USA. The company is targeting to reach almost 1,000 MW of RES projects in operation in all countries where it is active, over the following years. T A B L E O F C O N T E N T S Publisher’s Foreword 9 Preface by the Minister of Environment and Energy, Mr. PANOS SKOURLETIS M.P. 11 1. An introduction to Greece’s Energy Sector by COSTIS STAMBOLIS, Execu=ve Director, IENE and Managing Editor of Energia.gr 14 2. The Oil Sector Overview of Greece’s Oil Sector by COSTIS STAMBOLIS 40 Hellenic Petroleum, A Market Leader in SE Europe by GRIGORIS STERGIOULIS, CEO, HELPE 49 Hydrocarbon E &P sector: When the Vision Becomes a Reality by Professor SOFIA STAMATAKI, ex - Chairman, Hellenic Hydrocarbons Managements Company (ΕΔΕΥ) 53 A New Era for Greece’s Upstream Sector by MATHIOS RIGAS, CEO, Energean Oil & Gas 61 Greece’s Oil Retail Market by DIMITRIS MEZARTASOGLOU, Research Associate, IENE 67 3. -

La Metamorfosi Di Dioniso E L'inno Omerico

Cornelia Isler-Kerényi La metamorfosi di Dioniso e l’inno omerico VII Abstract The Homeric hymn VII, of which the date is controversial, tells of the kidnapping of Dionysus in the guise of an adolescent by a band of Tyrrenian pirates and their punishment. In his ceramic iconography in the Archaic age the God is always represented as a mature man. Only from 430 B.C. is he presented as an adolescent like he is at the East pediment of the Parthenon. Analysing the form of Dionysus in the works of the most important and productive Athenian vase-painters during this period helps us to understand the meaning of such a transformation. These works highlight the divinity of the Bacchic mysteries more than the official patron of the city and reflect the political and cultural climate which changed in Athens in the last decade of the 5th Century B.C. The iconographic situation makes it difficult to imagine that it was possible to sing about an adolescent Dionysus before 430 B.C. L’inno omerico VII, di datazione controversa, racconta il sequestro di Dioniso nelle sembianze di un efebo da parte di pirati tirreni e il loro castigo. Nella sua iconografia vascolare in età arcai- ca il dio si presenta invece sempre in età matura. In forme giovanili, come nel frontone est del Partenone, viene raffigurato solo a partire dal 430 a.C. circa. Nel prendere in esame l’immagine di Dioniso nell’opera dei ceramografi ateniesi più importanti attivi in quel periodo si cerca di definire meglio il significato di tale metamorfosi. -

21, El. Venizelou Ave., 102 50 ATHENS SECTION Tel.: 2103202049, Fax: 2103226371

LIST OF BANK BRANCHES (BY HEBIC) 30/06/2015 BANK OF GREECE HEBIC BRANCH NAME AREA ADDRESS TELEPHONE NUMBER / FAX 0100001 HEAD OFFICE SECRETARIAT ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS SECTION tel.: 2103202049, fax: 2103226371 0100002 HEAD OFFICE TENDER AND ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS PROCUREMENT SECTION tel.: 2103203473, fax: 2103231691 0100003 HEAD OFFICE HUMAN ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS RESOURCES SECTION tel.: 2103202090, fax: 2103203961 0100004 HEAD OFFICE DOCUMENT ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS MANAGEMENT SECTION tel.: 2103202198, fax: 2103236954 0100005 HEAD OFFICE PAYROLL ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS MANAGEMENT SECTION tel.: 2103202096, fax: 2103236930 0100007 HEAD OFFICE SECURITY ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS SECTION tel.: 2103202101, fax: 210 3204059 0100008 HEAD OFFICE SYSTEMIC CREDIT ATHENS CENTRE 3, Amerikis, 102 50 ATHENS INSTITUTIONS SUPERVISION SECTION A tel.: 2103205154, fax: …… 0100009 HEAD OFFICE BOOK ENTRY ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS SECURITIES MANAGEMENT SECTION tel.: 2103202620, fax: 2103235747 0100010 HEAD OFFICE ARCHIVES ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS SECTION tel.: 2103202206, fax: 2103203950 0100012 HEAD OFFICE RESERVES ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS MANAGEMENT BACK UP SECTION tel.: 2103203766, fax: 2103220140 0100013 HEAD OFFICE FOREIGN ATHENS CENTRE 21, El. Venizelou Ave., 102 50 ATHENS EXCHANGE TRANSACTIONS SECTION tel.: 2103202895, fax: 2103236746 0100014 HEAD OFFICE SYSTEMIC CREDIT ATHENS CENTRE 3, Amerikis, 102 50 ATHENS INSTITUTIONS SUPERVISION SECTION B tel.: 2103205041, fax: …… 0100015 HEAD OFFICE PAYMENT ATHENS CENTRE 3, Amerikis, 102 50 ATHENS SYSTEMS OVERSIGHT SECTION tel.: 2103205073, fax: …… 0100016 HEAD OFFICE ESCB PROJECTS CHALANDRI 341, Mesogeion Ave., 152 31 CHALANDRI AUDIT SECTION tel.: 2106799743, fax: 2106799713 0100017 HEAD OFFICE DOCUMENTARY ATHENS CENTRE 21, El. -

Registration Certificate

1 The following information has been supplied by the Greek Aliens Bureau: It is obligatory for all EU nationals to apply for a “Registration Certificate” (Veveosi Engrafis - Βεβαίωση Εγγραφής) after they have spent 3 months in Greece (Directive 2004/38/EC).This requirement also applies to UK nationals during the transition period. This certificate is open- dated. You only need to renew it if your circumstances change e.g. if you had registered as unemployed and you have now found employment. Below we outline some of the required documents for the most common cases. Please refer to the local Police Authorities for information on the regulations for freelancers, domestic employment and students. You should submit your application and required documents at your local Aliens Police (Tmima Allodapon – Τμήμα Αλλοδαπών, for addresses, contact telephone and opening hours see end); if you live outside Athens go to the local police station closest to your residence. In all cases, original documents and photocopies are required. You should approach the Greek Authorities for detailed information on the documents required or further clarification. Please note that some authorities work by appointment and will request that you book an appointment in advance. Required documents in the case of a working person: 1. Valid passport. 2. Two (2) photos. 3. Applicant’s proof of address [a document containing both the applicant’s name and address e.g. photocopy of the house lease, public utility bill (DEH, OTE, EYDAP) or statement from Tax Office (Tax Return)]. If unavailable please see the requirements for hospitality. 4. Photocopy of employment contract. -

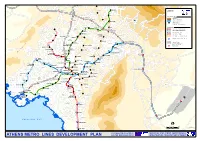

Athens Metro Lines Development Plan and the European Union Transport and Networks

Kifissia M t . P e Zefyrion Lykovrysi KIFISSIA n t LEGEND e l i Metamorfosi KAT METRO LINES NETWORK Operating Lines Pefki Nea Penteli LINE 1 Melissia PEFKI LINE 2 Kamatero MAROUSSI LINE 3 Iraklio Extensions IRAKLIO Penteli LINE 3, UNDER CONSTRUCTION NERANTZIOTISSA OTE AG.NIKOLAOS Nea LINE 2, UNDER DESIGN Filadelfia NEA LINE 4, UNDER DESIGN IONIA Maroussi IRINI PARADISSOS Petroupoli Parking Facility - Attiko Metro Ilion PEFKAKIA Nea Vrilissia Ionia ILION Aghioi OLYMPIAKO "®P Operating Parking Facility STADIO Anargyri "®P Scheduled Parking Facility PERISSOS Nea PALATIANI Halkidona SUBURBAN RAILWAY NETWORK SIDERA Suburban Railway DOUK.PLAKENTIAS Anthousa ANO Gerakas PATISSIA Filothei "®P Suburban Railway Section also used by Metro o Halandri "®P e AGHIOS HALANDRI l P "® ELEFTHERIOS ALSOS VEIKOU Kallitechnoupoli a ANTHOUPOLI Galatsi g FILOTHEI AGHIA E KATO PARASKEVI PERISTERI GALATSI Aghia . PATISSIA Peristeri P Paraskevi t Haidari Psyhiko "® M AGHIOS NOMISMATOKOPIO AGHIOS Pallini ANTONIOS NIKOLAOS Neo PALLINI Pikermi Psihiko HOLARGOS KYPSELI FAROS SEPOLIA ETHNIKI AGHIA AMYNA P ATTIKI "® MARINA "®P Holargos DIKASTIRIA Aghia PANORMOU ®P KATEHAKI Varvara " EGALEO ST.LARISSIS VICTORIA ATHENS ®P AGHIA ALEXANDRAS " VARVARA "®P ELEONAS AMBELOKIPI Papagou Egaleo METAXOURGHIO OMONIA EXARHIA Korydallos Glyka PEANIA-KANTZA AKADEMIA GOUDI Nera "®P PANEPISTIMIO MEGARO MONASTIRAKI KOLONAKI MOUSSIKIS KORYDALLOS KERAMIKOS THISSIO EVANGELISMOS ZOGRAFOU Nikea SYNTAGMA ANO ILISSIA Aghios PAGRATI KESSARIANI Ioannis ACROPOLI NEAR EAST Rentis PETRALONA NIKEA Tavros Keratsini Kessariani SYGROU-FIX KALITHEA TAVROS "®P NEOS VYRONAS MANIATIKA Spata KOSMOS Pireaus AGHIOS Vyronas s MOSCHATO Peania IOANNIS o Dafni t Moschato Ymittos Kallithea ANO t Drapetsona i PIRAEUS DAFNI ILIOUPOLI FALIRO Nea m o Smyrni Y o Î AGHIOS Ilioupoli DIMOTIKO DIMITRIOS . -

Networking UNDERGROUND Archaeological and Cultural Sites: the CASE of the Athens Metro

ing”. Indeed, since that time, the archaeological NETWORKING UNDERGROUND treasures found in other underground spaces are very often displayed in situ and in continu- ARCHAEOLOGICAL AND ity with the cultural and archaeological spaces of the surface (e.g. in the building of the Central CULTURAL SITES: THE CASE Bank of Greece). In this context, the present paper presents OF THE ATHENS METRO the case of the Athens Metro and the way that this common use of the underground space can have an alternative, more sophisticated use, Marilena Papageorgiou which can also serve to enhance the city’s iden- tity. Furthermore, the case aims to discuss the challenges for Greek urban planners regarding the way that the underground space of Greece, so rich in archaeological artifacts, can become part of an integrated and holistic spatial plan- INTRODUCTION: THE USE OF UNDERGROUND SPACE IN GREECE ning process. Greece is a country that doesn’t have a very long tradition either in building high ATHENS IN LAYERS or in using its underground space for city development – and/or other – purposes. In fact, in Greece, every construction activity that requires digging, boring or tun- Key issues for the Athens neling (public works, private building construction etc) is likely to encounter an- Metropolitan Area tiquities even at a shallow depth. Usually, when that occurs, the archaeological 1 · Central Athens 5 · Piraeus authorities of the Ministry of Culture – in accordance with the Greek Archaeologi- Since 1833, Athens has been the capital city of 2 · South Athens 6 · Islands 3 · North Athens 7 · East Attica 54 cal Law 3028 - immediately stop the work and start to survey the area of interest. -

Supplementary Materials

Supplementary Materials Figure S1. Temperature‐mortality association by sector, using the E‐OBS data. Municipality ES (95% CI) CENTER Athens 2.95 (2.36, 3.54) Subtotal (I-squared = .%, p = .) 2.95 (2.36, 3.54) . EAST Dafni-Ymittos 0.56 (-1.74, 2.91) Ilioupoli 1.42 (-0.23, 3.09) Kessariani 2.91 (0.39, 5.50) Vyronas 1.22 (-0.58, 3.05) Zografos 2.07 (0.24, 3.94) Subtotal (I-squared = 0.0%, p = 0.689) 1.57 (0.69, 2.45) . NORTH Aghia Paraskevi 0.63 (-1.55, 2.87) Chalandri 0.87 (-0.89, 2.67) Galatsi 1.71 (-0.57, 4.05) Gerakas 0.22 (-4.07, 4.70) Iraklio 0.32 (-2.15, 2.86) Kifissia 1.13 (-0.78, 3.08) Lykovrisi-Pefki 0.11 (-3.24, 3.59) Marousi 1.73 (-0.30, 3.81) Metamorfosi -0.07 (-2.97, 2.91) Nea Ionia 2.58 (0.66, 4.54) Papagos-Cholargos 1.72 (-0.36, 3.85) Penteli 1.04 (-1.96, 4.12) Philothei-Psychiko 1.59 (-0.98, 4.22) Vrilissia 0.60 (-2.42, 3.71) Subtotal (I-squared = 0.0%, p = 0.975) 1.20 (0.57, 1.84) . PIRAEUS Aghia Varvara 0.85 (-2.15, 3.94) Keratsini-Drapetsona 3.30 (1.66, 4.97) Korydallos 2.07 (-0.01, 4.20) Moschato-Tavros 1.47 (-1.14, 4.14) Nikea-Aghios Ioannis Rentis 1.88 (0.39, 3.39) Perama 0.48 (-2.43, 3.47) Piraeus 2.60 (1.50, 3.71) Subtotal (I-squared = 0.0%, p = 0.580) 2.25 (1.58, 2.92) . -

Generation 2.0 for Rights, Equality & Diversity

Generation 2.0 for Rights, Equality & Diversity Intercultural Mediation, Interpreting and Consultation Services in Decentralised Administration Immigration Office Athens A (IO A) January 2014 - now On 1st January 2014, the One Stop Shop was launched and all the services issuing and renewing residence permits for immigrants in Greece were moved from the municipalities to Decentralised Administrations. Namely, the 66 Attica municipalities were shared between 4 Immigration Offices of the Attic Decentralised Administration. a) Immigration Office for Athens A with territorial jurisdiction over residents of the Municipality of Athens, Address: Salaminias 2 & Petrou Ralli, Athens 118 55 b) Immigration Office for Central Athens and West Attica, with territorial jurisdiction over residents of the following Municipalities; i) Central Athens: Filadelfeia-Chalkidona, Galatsi, Zografou, Kaisariani, Vyronas, Ilioupoli, Dafni-Ymittos, ii) West Athens: Aigaleo Peristeri, Petroupoli, Chaidari, Agia Varvara, Ilion, Agioi Anargyroi- Kamatero, and iii) West Attica: Aspropyrgos, Eleusis (Eleusis-Magoula) Mandra- Eidyllia (Mandra - Vilia - Oinoi - Erythres), Megara (Megara-Nea Peramos), Fyli (Ano Liosia - Fyli - Zefyri). Address: Salaminias 2 & Petrou Ralli, Athens 118 55 c) Immigration Office for North Athens and East Attica with territorial jurisdiction over residents of the following Municipalities; i) North Athens: Penteli, Kifisia-Nea Erythraia, Metamorfosi, Lykovrysi-Pefki, Amarousio, Fiothei-Psychiko, Papagou- Cholargos, Irakleio, Nea Ionia, Vrilissia, -

Athens Metro Lines Development Plan and the European Union Infrastructure, Transport and Networks

AHARNAE Kifissia M t . P ANO Lykovrysi KIFISSIA e LIOSIA Zefyrion n t LEGEND e l i Metamorfosi KAT OPERATING LINES METAMORFOSI Pefki Nea Penteli LINE 1, ISAP IRAKLIO Melissia LINE 2, ATTIKO METRO LIKOTRIPA LINE 3, ATTIKO METRO Kamatero MAROUSSI METRO STATION Iraklio FUTURE METRO STATION, ISAP Penteli IRAKLIO NERATZIOTISSA OTE EXTENSIONS Nea Filadelfia LINE 2, UNDER CONSTRUCTION KIFISSIAS NEA Maroussi LINE 3, UNDER CONSTRUCTION IRINI PARADISSOS Petroupoli IONIA LINE 3, TENDERED OUT Ilion PEFKAKIA Nea Vrilissia LINE 2, UNDER DESIGN Ionia Aghioi OLYMPIAKO PENTELIS LINE 4, UNDER DESIGN & TENDERING AG.ANARGIRI Anargyri STADIO PERISSOS Nea "®P PARKING FACILITY - ATTIKO METRO Halkidona SIDERA DOUK.PLAKENTIAS Anthousa Suburban Railway Kallitechnoupoli ANO Gerakas PATISSIA Filothei Halandri "®P o ®P Suburban Railway Section " Also Used By Attiko Metro e AGHIOS HALANDRI l "®P ELEFTHERIOS ALSOS VEIKOU Railway Station a ANTHOUPOLI Galatsi g FILOTHEI AGHIA E KATO PARASKEVI PERISTERI . PATISSIA GALATSI Aghia Peristeri THIMARAKIA P Paraskevi t Haidari Psyhiko "® M AGHIOS NOMISMATOKOPIO AGHIOS Pallini NIKOLAOS ANTONIOS Neo PALLINI Pikermi Psihiko HOLARGOS KYPSELI FAROS SEPOLIA ETHNIKI AGHIA AMYNA P ATTIKI "® MARINA "®P Holargos DIKASTIRIA Aghia PANORMOU ®P ATHENS KATEHAKI Varvara " EGALEO ST.LARISSIS VICTORIA ATHENS ®P AGHIA ALEXANDRAS " VARVARA "®P ELEONAS AMBELOKIPI Papagou Egaleo METAXOURGHIO OMONIA EXARHIA Korydallos Glyka PEANIA-KANTZA AKADEMIA GOUDI Nera PANEPISTIMIO KERAMIKOS "®P MEGARO MONASTIRAKI KOLONAKI MOUSSIKIS KORYDALLOS ZOGRAFOU THISSIO EVANGELISMOS Zografou Nikea ROUF SYNTAGMA ANO ILISSIA Aghios KESSARIANI PAGRATI Ioannis ACROPOLI Rentis PETRALONA NIKEA Tavros Keratsini Kessariani RENTIS SYGROU-FIX P KALITHEA TAVROS "® NEOS VYRONAS MANIATIKA Spata KOSMOS LEFKA Pireaus AGHIOS Vyronas s MOSHATO IOANNIS o Peania Dafni t KAMINIA Moshato Ymittos Kallithea t Drapetsona PIRAEUS DAFNI i FALIRO Nea m o Smyrni Y o Î AGHIOS Ilioupoli DIMOTIKO DIMITRIOS . -

A Tale of Hidden Cities

Volume 4, Number 3, 2017, 19{38 journal homepage: region.ersa.org DOI: 10.18335/region.v4i3.189 A Tale of Hidden Cities Anastasia Panori1 1 Panteion University of Social and Political Sciences, Athens, Greece (email: [email protected]) Received: 8 February 2017/Accepted: 15 June 2017 Abstract. Hidden cities within a city? A large trending literature concerning urban and suburban poverty concentration patterns has been developed during the last decade. However, there are few cases where adequate data exist at a low spatial level, allowing the exploration of such socio-spatial phenomena. This paper seeks to investigate the structure and evolution of poverty within urban and suburban space, under a multidimensional framework, during a period of extended economic transformation. This paper uses the metropolitan area of Athens as its main case study, for which data at a municipal level exist, allowing the calculation of the Multidimensional Poverty Index (MPI) for the years 2006 and 2011. An extended cluster analysis, based on the calculated MPI values, results in the specification of three poverty clusters within Athens. The decomposition of the MPI index into its main dimensions highlights any existing differences between the structural and behavioural characteristics of each of them. The results indicate that there is a clear spatial concentration of poverty in the west suburban areas of Athens. The urban core of the city is characterised by middle-income municipalities, whilst the north-east and the south-east suburban areas experience low-poverty indicators. Finally, the results suggest that during the period under investigation more deprived areas were affected the most. -

List of Cities of Greece

SNo City Census 1991 Census 2001 Census 2011 Rank Region 1 Athens 772,072 745,514 664,046 1 Attica 2 Thessaloniki 383,967 363,987 315,196 2 Central Macedonia 3 Patras 152,570 160,400 168,034 3 West Greece 4 Piraeus 182,671 175,697 163,688 4 Attica 5 Larissa 112,777 124,394 144,651 5 Thessaly 6 Heraklion 115,270 130,914 140,730 6 Crete 7 Peristeri 137,288 137,918 139,981 7 Attica 8 Kallithea 114,233 109,609 100,641 8 Attica 9 Acharnes 61,052 75,329 99,346 9 Attica 10 Kalamaria 80,698 87,255 91,279 10 Central Macedonia 11 Nikaia 87,597 93,086 89,380 11 Attica 12 Glyfada 63,306 80,409 87,305 12 Attica 13 Volos 77,192 82,439 86,046 13 Thessaly 14 Ilio 78,326 80,859 84,793 14 Attica 15 Ilioupoli 75,037 75,904 78,153 15 Attica 16 Keratsini 71,982 76,102 77,077 16 Attica 17 Evosmos 28,821 52,624 74,686 17 Central Macedonia 18 Chalandri 66,285 71,684 74,192 18 Attica 19 Nea Smyrni 69,749 73,986 73,076 19 Attica 20 Marousi 64,092 69,470 72,333 20 Attica 21 Agios Dimitrios 57,574 65,173 71,294 21 Attica 22 Zografou 80,492 76,115 71,026 22 Attica 23 Egaleo 78,563 74,046 69,946 23 Attica 24 Nea Ionia 60,635 66,017 67,134 24 Attica 25 Ioannina 56,699 61,629 65,574 25 Epirus 26 Palaio Faliro 61,371 64,759 64,021 26 Attica 27 Korydallos 63,184 67,456 63,445 27 Attica 28 Trikala 45,835 48,686 61,653 28 Thessaly 29 Vyronas 58,523 61,102 61,308 29 Attica 30 Agia Paraskevi 47,463 56,836 59,704 30 Attica 31 Galatsi 57,230 58,042 59,345 31 Attica 32 Chalcis 51,646 53,584 59,125 32 Central Greece 33 Petroupoli 38,278 48,327 58,979 33 Attica 34 Serres 50,017