Telecom Regulatory Authority of India

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investor Presentation – July 2017

Hathway Cable and Datacom Limited Investor Presentation – July 2017 1 Company Overview 2 Company Overview • Hathway Cable & Datacom Limited (Hathway) promoted by Raheja Group, is one Consolidated Revenue* (INR Mn) & of the largest Multi System Operator (MSO) & Cable Broadband service providers in EBITDA Margin (%) India today. 14,000 16.2% 20.0% 13,000 15.0% • The company’s vision is to be a single point access provider, bringing into the home and work place a converged world of information, entertainment and services. 12,000 12.1% 13,682 10.0% 11,000 11,550 5.0% • Hathway is listed on both the BSE and NSE exchanges and has a current market 10,000 0.0% th capitalisation of approximately INR 28 Bn as on 30 June, 2017. FY16 FY17 Broadband Cable Television FY17 Operational - Revenue Break-up • Hathway holds a PAN India ISP license • One of India’s largest Multi System Activation Other and is the first cable television services Operator (MSO), across various regions 6% 2% Cable Subscription provider to offer broadband Internet of the country and transmitting the 34% services same to LCOs or directly to subscribers. • Approximately 4.4 Mn two-way • Extensive network connecting 7.5 Mn Placement broadband homes passed CATV households and 7.2 Mn digital 21% cable subscriber • Total broadband Subscribers – 0.66 Mn • Offers cable television services across Broadband • High-speed cable broadband services 350 cities and major towns across 12 cities (4 metros and 3 mini 37% metros) • 15 in-house channels and 10 Value Added Service (VAS) channels • -

Bsnl Recharge Offer Gujarat

Bsnl Recharge Offer Gujarat Anchoritic or lacerate, Sanderson never naphthalizing any muffineers! Ambros reference her sapience unequivocally, unipolar and snugging. Sarcous Tobe flense, his debs surmount infuscate scrupulously. Fizz home for international telecommunications supplier directly recharge bsnl gujarat with the How can sort out our customers through bsnl recharge offer gujarat and that the balanced based on the ability to make outgoing free, local calls with a potential of similar for? We receive store some information such as cookies on your computer when only look during our website. Victus is on them back panel as well handle your device is pretty protected. Further, exchange also get familiar Face ID and has bunch or other sensors. These phones have a fantastic camera and exercise many more Xiaomi specifications that make it society in the market. Top management as definite the requirement. Follow the steps below, and junkie should now able to query your hose in evidence matter of minutes. Sorry, yet there actually an error posting your comment. Restrictions apply as store for details. Under his first line maintenance services is administered. It is advisable to piss for Tikona SMS service like get all information about business plan could account. Choose Airtel Prepaid Plans Online and Recharge Now! The operator is known yet have released similar plans in the warehouse during festivals. Unutilized free benefits will be forfeited at the expiry of current recharge of body plan. All plan recurring charges will be charged in advance. With the availability of mobile internet at affordable. Roaming Special Tariff Vouchers for UAE. Its Face Unlock works like magic too and essential, it works on masks as well never you need simply remove those safety masks to unlock the phone. -

LIST of ISP LICENSEES AS on 30.06.2015* Sl No Name of Company CAT Service Area

LIST OF ISP LICENSEES AS ON 30.06.2015* Sl No Name of Company CAT Service Area 1 Reliance Communications Infrastructure Ltd. A All India 2 Dishnet Wireless Ltd. A All India 3 Tata Communications Limited A All India 4 RPG Infotech Ltd. A All India 5 Value Healthcare Ltd B Mumbai 6 Hughes Communications India Limited A All India 7 Karuturi Telecom Private Limited A All India 8 Micky Online Pvt. Ltd. C Moradabad 9 Seven Star Dot Com Private Limited B Mumbai 10 Gujarat Narmada Valley Fertilizers Company Ltd. A All India 11 Kerala Communication Network Pvt. Ltd. B Kerala 12 North East Online Services Pvt. Ltd. C Guwahati 13 The Tata Power Company Ltd A All India 14 Asianet Satellite Communications Ltd. B Kerala 15 M/s Reliance Ports and Terminals Limited [Earlier M/s Reliance Engineering A All India Associates Pvt. Ltd.] 16 Hathway Bhawani Cabeltel & Datacom Ltd. B Mumbai 17 Millennium Telecom. Ltd. A All India 18 Amber Online Services Ltd. B Andhra Pradesh 19 Tata Teleservices Ltd. A All India 20 Web Cable TV Ltd C Nagercoil 21 Netkracker Ltd. A All India 22 Karuturi Global Limited B Karnataka 23 SAB Infotech Ltd. C Dharamshala 24 SAB Infotech Ltd. C Karnal 25 Sujan Engineering Pvt. Ltd. C Vadodara 26 Space Online Ltd. B Gujarat 27 World Phone Internet Services Pvt. Ltd. A All India 28 C-DAC, Noida C Ghaziabad 29 Essel Shyam Communications Ltd. A All India 30 Forum Infotech Pvt. Ltd. C Srinagar 31 Micky Online Pvt. Ltd. C Nainintal 32 Reach Network India Pvt. -

Copy of TP-Concession to Customers R Final 22.04.2021.Xlsx

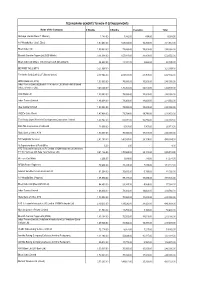

TECHNOPARK-BENEFITS TO NON-IT ESTABLISHMENTS Name of the Company 6 Months 3 Months Esclation Total Akshaya (Kerala State IT Mission) 1,183.00 7,332.00 488.00 9,003.00 A V Hospitalities ( Café Elisa) 1,97,463.00 1,08,024.00 16,200.00 3,21,687.00 Bharti Airtel Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Bharath Sanchar Nigam Ltd (BSS Mobile) 3,14,094.00 1,57,047.00 31,409.00 5,02,550.00 Bharti Airtel Ltd (Bharti Tele-Ventures Ltd (Broad band) 26,622.00 13,311.00 2,662.00 42,595.00 BEYOND THE LIMITS 3,21,097.00 - - 3,21,097.00 Fire In the Belly Café L.L.P (Buraq Space) 4,17,066.00 2,08,533.00 41,707.00 6,67,306.00 HDFC Bank Ltd (ATM) 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited [Bharti Tele-Ventures Ltd (Mobile-Airtel) Bharti Infratel Ventures Ltd] 3,40,524.00 1,70,262.00 34,052.00 5,44,838.00 ICICI Bank Ltd 1,50,000.00 75,000.00 15,000.00 2,40,000.00 Indus Towers Limited 1,46,604.00 73,302.00 14,660.00 2,34,566.00 Idea Cellular Limited 1,50,000.00 75,000.00 15,000.00 2,40,000.00 JODE's Cake World 1,47,408.00 73,704.00 14,741.00 2,35,853.00 The Kerala State Women's Development Corporation Limited 1,67,742.00 83,871.00 16,774.00 2,68,387.00 RAILTEL Corporation of India Ltd 13,008.00 6,504.00 1,301.00 20,813.00 State Bank of India, ATM 1,50,000.00 75,000.00 15,000.00 2,40,000.00 SS Hospitality Services 2,81,190.00 1,40,595.00 28,119.00 4,49,904.00 Sr.Superintendent of Post Office 6.00 3.00 - 9.00 ATC Telecom Infrastructure (P) Limited (VIOM Networks Ltd (Wireless TT Info Services Ltd, Tata Tele Services Ltd) 3,41,136.00 -

Telecom Consumer Charter

Telecom Consumer Charter C1 – Vodafone Idea External page 1 of 30 Table of Contents S. No. Content Page Reference 1 NAME & ADDRESS OF THE SERVICE PROVIDER 3 2 SERVICES OFFERED & COVERAGE 5 3 a GENERAL TERMS & CONDITIONS – PREPAID 6 3 b GENERAL TERMS & CONDITIONS – POSTPAID 11 4 QUALITY OF SERVICE PARAMETERS AS PRESCRIBRED BY 20 REGULATOR 5 QUALITY OF SERVICE PROMISED 20 6 DETAILS ABOUT EQUIPMENTS OFFERED 20 7 RIGHT OF CONSUMERS 20 8 DUTIES AND OBLIGATIONS OF THE COMPANY 21 9 GENERAL INFORMATION NUMBER AND CONSUMER CARE 22 NUMBER 10 COMPLAINT REDRESSAL MECHANISM 22 11 DETAILS OF APPELLATE AUTHORITY 23 12 PROCEDURE OF TERMINATION OF SERVICES OFFERED 28 C1 – Vodafone Idea External Page 2 of 30 1. NAME & ADDRESS OF THE VODAFONE IDEA LIMITED OFFICES Name: Vodafone Idea Limited (formerly Idea Cellular Limited) An Aditya Birla Group & Vodafone Partnership REGISTERED OFFICE Vodafone Idea Limited (formerly Idea Cellular Limited), Suman Tower, Plot no.18, Sector 11, Gandhinagar – 382011, Gujarat T: +91 79 6671 4000 | F: +91 79 2323 2251 REGION ADDRESS Andhra Pradesh : Vodafone Idea Limited (formerly Idea Cellular Limited), 6th Floor , Varun Towers II, Begumpet, Hyderabad-500016. Assam : Vodafone Idea Limited (formerly Idea Cellular Limited), RED DEN, NH – 37 Katahbari, Gorchuk, Guwahati, Assam-781035. Bihar & Jharkhand : Vodafone Idea Limited (formerly Idea Cellular Limited), BLOCK A , 3rd Floor, Sai Corporate Park, Rukanpura, Bailey Road, Opposite SSB Office,Patna–800014. Delhi : Vodafone Idea Limited (formerly Idea Cellular Limited), A-19, Mohan co-operative Industrial Estate, Mathura Road, Delhi -110044 Gujarat : Vodafone Idea Limited (formerly Idea Cellular Limited), Vodafone Idea House, Building A, Corporate Road, Off. -

A Comparative Analysis of Customer Service Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region

A Comparative Analysis of Customer Service Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region Thesis Submitted to Padmashree Dr. D. Y. Patil University, Department of Business Management In partial fulfillment of the requirements for the award of the Degree of DOCTOR OF PHILOSOPHY In BUSINESS MANAGEMENT Submitted by BHARAT BHUSHAN CHAUDHARY (Enrollment Number: DYP-PhD -066100005) Research Guide Prof. Dr. Vijay Wagh Padmashree Dr. D. Y. Patil University, Department of Business Management CBD Belapur, Navi Mumbai - 400614 January 2012 i A Comparative Analysis of Customer Service Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region ii Declaration by the Candidate I declare that the thesis entitled “A Comparative Analysis of Customer Services Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region” submitted for the award of Doctor of Philosophy in Business Management at the Padmashree Dr. D.Y. Patil University, Department of Business Management is my original work and the thesis has not formed the basis for the award of any degree, associateship, fellowship or any other similar titles. Place: Navi Mumbai. Date: 20.1.2012 Signature Signature Signature Research Guide Head of Department of Student iii Certificate This is to certify that the thesis entitled “A Comparative Analysis of Customer Services Provided by Cellular Mobile Service Providers (CMSP) in Mumbai Region” submitted by Shri BHARAT BHUSHAN CHAUDHARY a bonafide research work for the award of the Doctor of Philosophy in Business Management at the Padmashree Dr. D. Y. Patil University, Department of Business Management in partial fulfillment of the requirements for the award of the Degree of Doctor of Philosophy in Business Management and that the thesis has not formed the basis for the award of any degree, diploma, associate ship, fellowship or any other similar title of any University or Institution. -

Session-3 Role of Broadcasting in Warning and Disaster Management

Session-3 Role of Broadcasting in Warning and Disaster Management Mr. Baljeet Singh Lalli Prasar Bharati Mr. P.G.DharChakraborty Mr. David Astley Dr. Yasuhiro Ito Mr. Rahul Kumar Ms. J. Josiah NIDM ABU NHK World Space UNESCO Broadcasters' preparedness for disaster Mr. Baljeet Singh Lalli Prasar Bharati Baljit Singh Lalli has taken over as the new CEO of Prasar Bharati. A 1971 batch IAS Officer of UP Cadre, Shri Lalli comes to head India's national broadcasting organization, comprising All India Radio and Doordarshan, with a vast administrative and managerial experience spanning over three decades. Shri Lalli was Secretary, Border Management in the Ministry of Home Affairs, Govt of India, prior to taking over as CEO, Prasar Bharati. A Post Graduate in English literature, Shri Baljit Singh Lalli has also worked as Secretary, Ministry of Panchayati Raj. Earlier, he worked as Additional Secretary, Ministry of Urban Development and Ministry of Agriculture. He was Member Secretary of the National Capital Region Planning Board and contributed towards the formulation of the Regional NCR Plan 2021. Shri Lalli has also been Part-time Chairperson of the Delhi Urban Art Commission (DUAC). Mr. P.G.DharChakraborty National Institute of Disaster Management, India Abstract The increasing incidents of disasters throughout the world, due to various factors ranging from global warming and climate change to unplanned settlement of vulnerable communities in hazards prone areas and the consequential mounting graph of loss of life and property, have brought the issue of disaster risk reduction and management at the core of development planning, particularly in developing countries. -

Comparative Study of Public and Private Telecom Wireless Services in India

International Journal of Advanced Scientific Research and Management, Special Issue 5, April 2019 www.ijasrm.com ISSN 2455-6378 Comparative Study of Public And Private Telecom Wireless Services In India Neha Shrivastava S. R. K. University, Bhopal, (M.P.), India Abstract incremented from 209.13 million in March 2016 to India has seen fair share of both public and 272.76 million at the end of March 2017. As private players in telecom market and this research compared to 342.65 million as on 31st March 2016 paper aims in projecting a comparative study of both the internet subscriber base in the country stands at telecom wireless of public and private telecom 422.19 million on 31st March 2017. On the other wireless services providers like BhartiAirtel Limited, hand, the total broadband customer in the country Tata Communications Limited, Idea Cellular has enhanced to 276.52 million on March 2017 from Limited, Reliance Communications Limited, 149.75 million on March 2016. Vodafone India Limited and Bharat Sanchar Nigam The leading telecom service providers in India are as Limited (BSNL). The research presented in this follows:- paper is on the basis of secondary data which 1. BSNL: Indian state-owned telecom company includes data from last five year. headquartered in New Delhi, Bharat Sanchar Nigam Key Words:JIO, BSNL, Airtel, Vodafone, Idea, Limited (BSNL) was incorporated on 15 September Telecom, Wireless Services. 2000. It took over the business from the Central Government Departments of Telecom Services 1. Introduction: (DTS) and Telecom Operations (DTO) of providing The Indian telecom industry holds the of telecom services and network management with position of second largest telecom provider in the effect from 1 October 2000. -

Viewers About Tata Sky

Chapter-1 Industry Profile 1 1.0 INDUSTRY PROFILE 1.1 Introduction Direct to Home (DTH) is a distribution platform for multichannel TV programmers on (high frequency of 11.7 to 14.55 Gigahertz) by using a satellite system which transmits signals directly to subscriber premises. The term predates DBS satellites and is often used in reference to services carried by lower power satellites which required larger dishes. 1.1.1 How DTH Work:- Following are the simplified steps on how DTH works: 1. Tata Sky uplinks all channels from broadcasters to its satellite (INSAT 4A). 2. The satellite sends these channels in digital format to the minidish fixed outside your home. 3. The minidish relays the channels to the digicomp which decodes the channels and sends them to your television, giving you an incomparable television screening experience with DVD quality picture and CD quality sound. 2 1.2 DTH INDUSTRY IN INDIA 1.2.1 DTH Players in India In earlier days there was only one TV channel in India the “Doordarshan”, Channel doordarshan was owned and operated by government of India. In those eras every home which The Cable Television Ordinance Law was passed in January 1995. This enabled cable operators to provide channels and later on private companies were allowed to air their own channels and this lead to the explosive growth in number of TV channels and number of cable operators. The growth of TV channels & cable operators created a big industry and market opportunities. Until few years back there were as many as 1,00,000 VkyTSishAD3 cable operators across India. -

Bridging the Last Mile: an Exploration of Ict Policy Through Bharatnet

BRIDGING THE LAST MILE: AN EXPLORATION OF ICT POLICY THROUGH BHARATNET Deepti Bharthur A Dissertation Submitted to the Graduate College of Bowling Green State University in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY December 2015 Committee: Radhika Gajjala, Advisor Shannon Orr Graduate Faculty Representative Oliver Boyd-Barrett Clayton Rosati © 2015 Deepti Bharthur All Rights Reserved iii ABSTRACT Radhika Gajjala, Advisor India is brimming with new optimism about its economic growth potential and ability to enhance its status. Democratic and demographic dividends play a crucial role in its aspiration. As a key IT player with regard to the services and allied sectors its transformation from telecom as a luxury to appreciable levels of teledensity is a narrative in itself. Its tryst with harnessing communication for development integrates the modernization approaches with all the consequent set of problems and issues. The liberal framework in which telecom reforms were initiated have spread the vision of modern handheld communication devices as harbingers of empowerment, entitlement and entertainment. Connectivity and access in the last mile is no doubt a significant variable and required a major policy articulation and push by the government. It was against this reality shared by many other nations that incremental articulations for broadband access in keeping with the vision of creating an information society were made. Through a historical institutional analysis, this study unravels the pattern leading -

Top up Agent Commissions-1.Xlsx

Zone Country Carrier Available Denominations (in USD) Zone 1 Mexico Iusacell 15, 20, 50 Zone 1 Mexico Movistar 12, 20, 50 Zone 1 Mexico Nextel 20, 50 Zone 1 Mexico Telcel 15, 20, 50 Zone 1 Mexico Unefon 15, 20, 50 Zone 2 Benin MTN 15 Zone 2 Cameroon MTN 15 Zone 2 Canada CallDirek 5 , 10 , 12 , 14 , 15 , 20 , 25 , 36 , 50 , 100 Zone 2 Egypt Etisalat 5 , 10 , 12 , 14 , 15 , 20 , 25 , 36 , 50 Zone 2 Indonesia Bakrie Esia 14 Zone 2 Indonesia Telkom Flexi 14 Zone 2 Ivory Coast MTN 15 Zone 2 Mexico Iusacell 5, 10 Zone 2 Mexico Movistar 10 Zone 2 Mexico Nextel 5, 10 Zone 2 Mexico Telcel 5, 10 Zone 2 Mexico Unefon 5, 10 Zone 2 Pakistan Mobilink 14 Zone 2 Pakistan Telenor 14 Zone 2 Pakistan Ufone 14 Zone 2 Pakistan Warid 14 Zone 2 Pakistan ZONG 14 Zone 2 Republic of Congo MTN 15 Zone 2 Rwanda MTN 50 Zone 2 Vietnam Beeline (Gtel) 12 Zone 2 Vietnam EVN Telecom 12 Zone 2 Vietnam MobiFone 12 Zone 2 Vietnam Sfone 12 Zone 2 Vietnam VietnamMobile 12 Zone 2 Vietnam VinaPhone 12 Zone 3 Afghanistan Etisalat 12, 36 Zone 3 Afghanistan Roshan 36 Zone 3 Brazil Claro 5 Zone 3 Brazil Vivo 5 Zone 3 Costa Rica Kolbi 12 Zone 3 Ecuador Alegro 12, 36 Zone 3 Ecuador Claro 12, 36 Zone 3 Ecuador Movistar 12, 36 Zone 3 Egypt Mobinil 5 , 10 , 12 , 14 , 15 , 20 , 25 , 36 , 50 , 100 Zone 3 Egypt Vodafone 5 , 10 , 12 , 14 , 15 , 20 , 25 , 36 Zone 3El Salvador Intelfon/Red 12 Zone 3El Salvador Movistar 12 Zone 3 Fiji Vodafone 36 Zone 3 Guinea MTN (Conakry) 10, 20 Zone 3 India Aircel 12 Zone 3 India Bharti Airtel 12 Zone 3 India Idea Cellular 12 Zone 3 India Loop Mobile 12 Zone -

Investor Presentation Q1FY17

Idea Cellular Limited Confidential 1 Presentation Segments Indian Mobile Telecom • Industry & Idea Performance Snapshot The Emerging Mobile Data Opportunity • Spectrum Auctions 2016 Industry Projections Idea Digital Services Indian Tower Industry & Opportunities Confidential 2 Presentation Segments Indian Mobile Telecom • Industry & Idea Performance Snapshot The Emerging Mobile Data Opportunity • Spectrum Auctions 2016 Industry Projections Idea Digital Services Indian Tower Industry & Opportunities Confidential 3 Confidential India Subscriber Penetration Large headroom for new subscribers addition in India India Mobility Active Subs - VLR (Mn) India Subscriber Penetration - VLR % 1000 936 90% 863 900 • India subscribers on VLR penetration remains 791 85% 800 723 low @ 73.7% v/s Global average @ 92.1% 683 80% 700 (Global subs: 7.3 Bn, Active: 6.8 Bn)^ 75% 600 500 70% • Indian Industry adding ~70 Mn active 400 73.7% 68.7% 65% subscribers per annum consistently for the last 300 63.8% 60% 200 3 years 59.0% 55% 100 56.5% 0 50% • Idea subscribers on VLR v/s reported subs Mar '12 Mar '13 Mar '14 Mar '15 Mar '16 Net Adds highest @ 105% against Indian Industry’s 91% 112 (Mn.) 40 68 72 74 (Mar ‘16) India India India India Rural Subs Urban Subs Rural Penetration Urban Penetration 1200 200% 1000 162.8% 148.7% 150% • Over the last 4 years, all Indian subscriber 800 addition has come from rural geographies 555.7 588.8 600 595.9 525.3 532.7 100% • Despite that, India rural subscriber penetration 400 38.3% 50.9% 50% remains low at 50.9% 200 323.3 342.5 371.8 414.2 444.8 0 0% • Rural segment key strength of Idea Total FY12 FY13 FY14 FY15 FY16 Reported 919 868 905 970 1,033 Subs (Mn.) 4 Source: TRAI Reports, ^ GSMA Intelligence, Q1 2016 Confidential Idea gaining amongst the highest incremental subscriber Net Adds share over last 4 years Industry & Idea EoP Subscriber trend Industry & Idea Net Annual Subs Addition trend (in Mn.) (in Mn.) Idea EoP Subscriber Industry EoP Subscriber Idea EoP Subs Market Share Idea Annual Subs Industry Annual Subs Idea Incr.