HSBC Bank Egypt S.A.E

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Sub-Custodians Used for Safekeeping of Financial Instruments

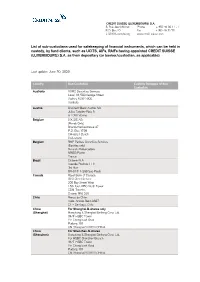

CREDIT SUISSE (LUXEMBOURG) S.A. 5, Rue Jean Monnet Phone + 352 46 00 11 - 1 P.O. Box 40 Fax + 352 46 32 70 L-2010 Luxembourg www.credit-suisse.com List of sub-custodians used for safekeeping of financial instruments, which can be held in custody, by fund clients, such as UCITS, AIFs, RAIFs having appointed CREDIT SUISSE (LUXEMBOURG) S.A. as their depositary (or banker/custodian, as applicable) Last update: June 30, 2020 Country Sub-Custodian Custody Delegate of Sub- Custodian Australia HSBC Securities Services Level 13, 580 George Street Sydney NSW 2000 Australia Austria UniCredit Bank Austria AG Julius Tandler-Platz 3 A-1090 Vienna Belgium SIX SIS AG (Bonds Only) Brandschenkestrasse 47 P.O. Box 1758 CH-8021 Zurich Switzerland Belgium BNP Paribas Securities Services (Equities only) 9 rue du Débarcadère 93500 Pantin France Brazil Citibank N.A. Avenida Paulista 1111 3rd floor BR-01311-290 Sao Paulo Canada Royal Bank of Canada GSS Client Service 200 Bay Street West 15th floor, RBC North Tower CDN-Toronto, Ontario M5J 2J5 Chile Banco de Chile Avda. Andrés Bello 2687 CL – Santiago, Chile China For Shanghai-B-shares only (Shanghai) Hongkong & Shanghai Banking Corp. Ltd. 34/F HSBC Tower Yin Cheng East Road Pudong 101 CN-Shanghai 200120 CHINA China For Shenzhen-B-shares (Shenzhen) Hongkong & Shanghai Banking Corp. Ltd. For HSBC Shenzhen Branch 34/F HSBC Tower Yin Cheng East Road Pudong 101 CN-Shanghai 200120 CHINA Colombia Cititrust Colombia S.A. Sociedad Fiduciaria Carrera 9A No. 99-02 First Floor Santa Fé de Bogotá D.C. -

Annual Review Show Major International Network Comprises Some 6,500 Offices in Developments in the HSBC Group Last Year

The HSBC Group Headquartered in London, HSBC Holdings plc is one Illustrative Theme of the largest banking and financial services Managing for Value organisations in the world. The HSBC Group’s The photographs in this Annual Review show major international network comprises some 6,500 offices in developments in the HSBC Group last year. They illustrate 79 countries and territories in Europe, the Asia- the progress we have made in implementing our five-year strategic plan, ‘Managing for Value’, launched in 1998. Pacific region, the Americas, the Middle East and Africa. The picture spreads are grouped around these initiatives. They reflect the breadth and scope of our operations, and With listings on the London, Hong Kong, New our international character. York and Paris stock exchanges, shares in HSBC Building our ‘wealth management’ (personal financial Holdings plc are held by around 190,000 shareholders services) business is a cornerstone of our plan. It was seen in in some 100 countries and territories. The shares are our acquisitions during 2000, notably CCF, and in the launch traded on the New York Stock Exchange in the form of our first truly global service for personal customers, HSBC Premier. To provide essential back office support, we of American Depositary Receipts. invested more resources in the global processing of banking operations. We focused on e-business to bring customers a Through a global network linked by advanced range of new services via new delivery channels, such as technology, including a rapidly growing e-commerce internet and mobile phone banking. We joined forces with capability, HSBC provides a comprehensive range of Merrill Lynch in a joint venture offering online investment and banking services. -

Brown Brothers Harriman Global Custody Network Listing

BROWN BROTHERS HARRIMAN GLOBAL CUSTODY NETWORK LISTING Brown Brothers Harriman (Luxembourg) S.C.A. has delegated safekeeping duties to each of the entities listed below in the specified markets by appointing them as local correspondents. The below list includes multiple subcustodians/correspondents in certain markets. Confirmation of which subcustodian/correspondent is holding assets in each of those markets with respect to a client is available upon request. The list does not include prime brokers, third party collateral agents or other third parties who may be appointed from time to time as a delegate pursuant to the request of one or more clients (subject to BBH's approval). Confirmations of such appointments are also available upon request. COUNTRY SUBCUSTODIAN ARGENTINA CITIBANK, N.A. BUENOS AIRES BRANCH AUSTRALIA CITIGROUP PTY LIMITED FOR CITIBANK, N.A AUSTRALIA HSBC BANK AUSTRALIA LIMITED FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) AUSTRIA DEUTSCHE BANK AG AUSTRIA UNICREDIT BANK AUSTRIA AG BAHRAIN* HSBC BANK MIDDLE EAST LIMITED, BAHRAIN BRANCH FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) BANGLADESH* STANDARD CHARTERED BANK, BANGLADESH BRANCH BELGIUM BNP PARIBAS SECURITIES SERVICES BELGIUM DEUTSCHE BANK AG, AMSTERDAM BRANCH BERMUDA* HSBC BANK BERMUDA LIMITED FOR THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED (HSBC) BOSNIA* UNICREDIT BANK D.D. FOR UNICREDIT BANK AUSTRIA AG BOTSWANA* STANDARD CHARTERED BANK BOTSWANA LIMITED FOR STANDARD CHARTERED BANK BRAZIL* CITIBANK, N.A. SÃO PAULO BRAZIL* ITAÚ UNIBANCO S.A. BULGARIA* CITIBANK EUROPE PLC, BULGARIA BRANCH FOR CITIBANK N.A. CANADA CIBC MELLON TRUST COMPANY FOR CIBC MELLON TRUST COMPANY, CANADIAN IMPERIAL BANK OF COMMERCE AND BANK OF NEW YORK MELLON CANADA RBC INVESTOR SERVICES TRUST FOR ROYAL BANK OF CANADA (RBC) CHILE* BANCO DE CHILE FOR CITIBANK, N.A. -

HSBC Bank Egypt Personal Finance Terms and Conditions

HSBC Bank Egypt Personal Finance Terms and Conditions. ﻫﺬه اﻟﺸﺮوط واﻷﺣﻜﺎم ﺗﻄﺒﻖ ﻣﻦ ٧ ﺳﺒﺘﻤﺒﺮ ٢٠١٤ These Terms and conditions apply from 7 September 2014 © بــنــك إتــش إس بــي ســي مــصــر. ش.م.م. 2020 جميع الحقوق محفوظة. ﻻ يجوز استنساخ أي جزء من هذا المنشور أو تخزينه في أي Copyright. HSBC Bank Egypt S.A.E. 2020 ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in © جهاز لخزن المعلومات أو تحويله، في أي شكل أو وسيلة إلكترونية، مــيــكـــانيكية، الــتصــوير، الــتســجــيــل، أو غـيــر ذلـــــك، دون الــحــصول ,a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without the prior written permission of HSBC Bank Egypt S.A.E. عــلى إذن خــطي مسبق من بنك إتش إس بي سي مصر. ش.م.م. Issued by HSBC Bank Egypt S.A.E, 306 Corniche El Nil Street, PO Box 124, Maadi, Cairo, Egypt. CRN 20075. .CRN 20075 صدر عن بنك إتش إس بي سي مصر. ش.م.م. 306 كورنيش النيل، ص.ب. 124، المعادي، القاهرة، مصر. 1 HSBC Bank Egypt Personal Finance Terms and Conditions ﻫﺬه اﻟﺸﺮوط واﻷﺣﻜﺎم ﺗﻄﺒﻖ ﻣﻦ ٧ ﺳﺒﺘﻤﺒﺮ ٢٠١٤ .These Terms and conditions apply from 7 September 2014 Definitions In these Terms, the following words and expressions shall have the following : meanings: ﻧﺤﻦ ﻧﺎ “we”, “us” and “our” refer to HSBC Bank Egypt. Our “branches” means those branches of HSBC Bank Egypt situated in the Country. » “account” means each and every personal current, savings & term deposit, saving certificate, finance, overdraft and/or credit/debit card account which we operate for you at your request/instruction through one of our branches (or electronically) as may be applicable in the context in which it appears in these Terms. -

List of Subcustodians - Nomura Bank (Luxembourg) S.A

List of Subcustodians - Nomura Bank (Luxembourg) S.A. Some markets may be restricted for AIF / UCITS funds Investment - Please contact your dedicated Account Manager Market Currency Sub-custodian Cash correspondent bank Argentina ARS CITIBANK N.A. Argentina Branch (via The Bank of New York Mellon, Brussels) Australia AUD NATIONAL AUSTRALIA BANK LIMITED, Melbourne Austria EUR EUROCLEAR BANK SA/NV, Brussels Bangladesh BDT THE HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED, Bangladesh Branch, Dhaka Belgium EUR EUROCLEAR BANK SA/NV, Brussels Bermuda BMD HSBC BANK BERMUDA LIMITED, Hamilton (via The Bank of New York Mellon, Brussels) Brazil BRL BANCO BNP PARIBAS BRASIL S.A., São Paulo CITIBANK EUROPE PLC, Bulgarian Branch (via The Bank of New Bulgaria BGN York Mellon, Brussels) Canada CAD CIBC MELLON TRUST COMPANY, Toronto CANADIAN IMPERIAL BANK OF COMMERCE, Toronto Chile CLP BANCO DE CHILE, Santiago (via The Bank of New York Mellon, Brussels) China (Shanghai) USD HSBC BANK (CHINA) COMPANY LIMITED, Shanghai China (Shenzen) HKD HSBC BANK (CHINA) COMPANY LIMITED, Shenzhen China CNY INDUSTRIAL COMMERCIAL BANK OF CHINA, Beijing* Colombia COP CITITRUST S.A., Bogota (via The Bank of New York Mellon, Brussels) PRIVREDNA BANKA, Zagreb (via The Bank of New York Mellon, Croatia HRK Brussels) Czech Republic CZK UNICREDIT BANK CZECH REPUBLIC AND SLOVAKIA, Prague Denmark DKK NORDEA BANK ABP, DENMARK BRANCH Egypt EGP HSBC BANK EGYPT S.A.E., Cairo (via The Bank of New York Mellon, Brussels) Estonia EUR SEB PANK AS, Tallin (via the Bank of New York Mellon, -

Unterverwahrung Die Informationen Dieser Anlage Hat Die Gesellschaft Von Der Verwahrstelle Mitgeteilt Bekommen

Unterverwahrung Die Informationen dieser Anlage hat die Gesellschaft von der Verwahrstelle mitgeteilt bekommen. Die Gesellschaft hat diese Informationen nur auf Plausibilität geprüft. Sie ist auf die Zulieferung der Information durch die Verwahrstelle angewiesen und kann die Richtigkeit und Vollständigkeit im Einzelnen nicht überprüfen. Die Verwahrstelle hat verschiedene Zwischen-Unterverwahrer mit der Verwahrung der Vermögensgegenstände beauftragt. Die Zwischen-Unterverwahrer wiederum haben die Verwahraufgaben auf verschiedene weitere Unterverwahrer übertragen, die in den in der Unterverwahrliste jeweils aufgeführten Ländern ansässig sind, um die jeweiligen Vermögensgegenstände in den jeweiligen Ländern zu verwahren. Folgende Interessenkonflikte könnten sich aus der Unterverwahrung ergeben: Fallgruppe 1 Sofern in der von der Verwahrstelle zur Verfügung gestellten Unterverwahrliste Gesellschaften mit der Bezeichnung „Deutsche Bank …“ genannt sind, handelt es sich um Niederlassungen oder Tochtergesellschaften der Deutsche Bank Gruppe und um ein mit der Verwaltungsgesellschaft verbundenes Unternehmen. Fallgruppe 2 Mit Unterverwahrern, die nicht unter die Fallgruppe 1 fallen, werden keine Interessenskonflikte gesehen. Potentielle Interessenkonflikte würden durch die Gestaltung des Verwahrstellen-/ Unterverwahrervertrags gesteuert werden. Die Verwahrstelle geht nach eigenen Angaben mit den Interessenkonflikten wie folgt um: Die Verwahrstelle hat angemessene und wirksame interne Regelwerke eingeführt, um eigene potentielle Interessenkonflikte -

HSBC Bank Middle East Limited Annual Report and Accounts 2020

HSBC Bank Middle East Limited Annual Report and Accounts 2020 Contents Presentation of Information Page This document comprises the Annual Report and Accounts 2020 Report of the Directors 2 for HSBC Bank Middle East Limited (‘the bank’) and its subsidiary Independent Auditor’s Report to the Shareholder of HSBC Bank undertakings (together ‘the group’). It contains the Report of the Middle East Limited 3 Directors, Financial Statements together with the Auditor’s report Financial Statements 8 and Additional information. References to ‘HSBC’ or ‘the HSBC Consolidated income statement 8 Group ’or 'the Group' within this document mean HSBC Holdings Consolidated statement of comprehensive income 9 plc together with its subsidiaries. Consolidated statement of financial position 10 Consolidated statement of cash flows 11 Consolidated statement of changes in equity 12 Notes on the Financial Statements 13 1 Legal status and principal activities 13 2 Basis of preparation and significant accounting policies 13 3 Net fee income 22 4 Changes in fair value of designated debt and related derivatives 22 5 Operating profit/(loss) 23 6 Employee compensation and benefits 23 7 Auditors’ remuneration 24 8 Tax 24 9 Dividends 25 10 Segment analysis 26 11 Trading assets 27 12 Fair values of financial instruments carried at fair value 27 13 Fair values of financial instruments not carried at fair value 31 14 Derivatives 32 15 Financial investments 34 16 Assets charged as security for liabilities, and collateral accepted as security for assets 34 17 Interests in -

HSBC Entity Giinsdownload

HSBC Counterparties - Common Reporting Standard legal entity information Updated: 10 May 2019 The Common Reporting Standard (CRS) affects both business and individuals, from the smallest account holder to the largest of corporations. Therefore, as well as requiring our customers to provide CRS related information to us, HSBC should also provide its tax residency information to those financial institutions (referred to as "counterparties") that count us as their customer, when those financial institutions are required to carry out their CRS due diligence obligations. To fulfil our CRS requirements, HSBC has provided the following data for each of its entities: -Entity Name -Registered Address -Country of Incorporation -Entity Type -Jurisdiction of Tax Residency -Global Intermediary Identification Number (GIIN) (if relevant) -Taxpayer Identification Number (TIN) To access this information, simply search below by any of these fields. If you cannot find the information you are looking for, please speak to your main point of contact at HSBC. Global Intermediary Identification Number Taxpayer Identification Number (TIN) Entity Name Registered Address Country of Incorporation Entity Type Jurisdiction of Tax Residency (GIIN) HSBC Administradora de Inversiones S.A. Bouchard 557, Piso 18° , Cdad. Autónoma de Buenos Aires, Argentina, 1106 Argentina REPORTING FI Argentina IN8MB5.99999.SL.032 30-58408672-2 HSBC Argentina Holdings S.A. 557 Bouchard, Level 22 , Ciudad de Buenos Aires, Capital federal, Argentina, C1106ABG Argentina REPORTING FI Argentina HFH4AU.00001.ME.032 30-54054626-2 HSBC Bank Argentina S.A. 557 Bouchard, Level 22 , Ciudad de Buenos Aires, Capital federal, Argentina, C1106ABG Argentina REPORTING FI Argentina HFH4AU.00000.LE.032 33537186009 HSBC Seguros de Retiro (Argentina) S.A. -

Central Bank of Egypt Control & Supervision Sector Sr. No. Banks

Central Bank of Egypt Control & Supervision Sector Banks Registered with the Central Bank of Egypt Sr. Registration Banks Address of Head Office No. Date 1 Banque Misr 18/1/1958 151, Mohamed Farid St., Cairo . 2 National Bank of Egypt 1/1/1961 1187, Cornich El Nile St., Cairo . 3 Egyptian Arab Land Bank 18/1/1958 78 Gameat El Dewal El Arabia St., Mohandessin, Giza . 4 Agricultural Bank of Egypt 11/8/1977 1,El Seid Club St., Dokki, Giza . 5 Industrial Development Bank 27/5/1976 2 Abdel Kader Hamza street, Cairo Centre Building, Garden City, Cairo 6 Banque Du Caire 18/1/1958 6, Dr. Moustafa Abu Zahra St., Nasr city, Cairo . 7 The United Bank 25/6/2006 106, El Kasr El Einy St.,(Cairo Center Tower),Cairo . 8 Bank of Alexandria 18/1/1958 49, Kasr El Nile St., Cairo . 9 MIDBank S.A.E 26/6/1975 21/23 Charles De Gaulle St., (ex Giza st.,), Nile Tower, Giza . 10 Commercial International Bank (Egypt) 13/8/1975 21/23, Charles Du Gaulle St., (ex Giza St.,), Nile Tower, Giza . 11 Attijariwafa bank Egypt S.A.E 13/8/1975 Star Capital A1 Tower,City Stars, 2 Ali Rashed St., Nasr City, Cairo. 12 Societe Arabe Internationale de Banque 9/9/1976 56, Gameat El Dewal Al Arabia St., Mohandessin, Giza . 13 Blom Bank - Egypt 24/3/1977 Block No.61 , 1st District, 90 St., The Fifth Compound, New Cairo . 14 Credit Agricole Egypt S.A.E 12/5/1977 Touristic area No. (9/10/11/12/13) Fifth Settlement , Cairo. -

Egypt Facts & Figures 2016

EGYPT FACTS & FIGURES 2016 EGYPT FACTS AND FIGURES 2016 Geography Surface (in sqkm) 1,001,450 o.w. Land area 995,450 o.w. Water area 6,000 Land boundaries' length (in km) 2,665 Coastline length (in km) 2,450 Maximum altitude: Mount Catherine (in m) 2,629 Demography Population (in millions) 90.2 Population annual growth rate (2006-2016) 2.2% Population under 15 years (% of total population) 33% Population density (per sqkm) 90 Urban population (% of total population) 43% Unemployment rate 13% Life expectancy at birth 71 Infant mortality rate (per 1,000 live births) 20 Human Development Index (UNDP) 0.691 Education Adult literacy rate Male 83% Female 67% Number of students in pre-university education (000s) 20,641 Number of schools 52,664 Number of teachers 992,797 Health Number of hospital beds (per 1,000 people) 0.5 Number of physicians (per 1,000 people) 2.8 Health expenditures/GDP 5.6% Technology Diffusion Number of telephone mainlines (per 100 people) 7.4 Number of cellular subscribers (per 100 people) 111.0 Number of internet users (per 100 people) 35.9 Number of broadband subscribers (per 100 people) 4.5 Infrastructure (in Km) Roadway length (paved) 137,430 Railway length 5,085 Ports and terminals Ayn Sukhnah, Alexandria, Damietta, El Dekheila, Sidi Kurayr, Suez General Currency Egyptian Pound Official language Arabic Fiscal year July 1 - June 30 Number of governorates 26 Fiscal Year 2014 2015 2016 Macroeconomic Indicators GDP (US$ billion) 312.3 336.6 329.1 o.w. Agriculture, irrigation and fishing 11.1% 11.3% 11.9% o.w. -

HSBC Bank Plc, London and Hong Kong and Shanghai Banki

The below is a list sub delegates appointed by the Global Sub-Custodians (HSBC Bank plc, London and Hong Kong and Shanghai Banking Corporation Limited, Hong Kong) of the Depositary Bank, HSBC Bank Plc, Luxembourg Branch as at 1 March 2018 and will be updated should any changes take place. Country Sub‐custodian/Agent Argentina HSBC Bank Argentina S.A. Australia HSBC Bank Australia Limited Austria UniCredit Bank Austria AG Bahrain HSBC Bank Middle East Ltd Bangladesh The Hongkong & Shanghai Banking Corporation Ltd (Bangladesh) Belgium BNP Paribas Securities Services Belgium Euroclear Bank SA/NV Bermuda HSBC Bank of Bermuda Ltd Bosnia‐Herzegovina UniCredit Bank d.d. Botswana Standard Chartered Bank Botswana Ltd Brazil Bradesco‐Kirton Corretora de Títulos e Valores Mobiliários S.A. Bulgaria UniCredit Bulbank AD Canada Royal Bank of Canada Chile Banco Santander Chile China HSBC Bank (China) Company Limited Colombia Itau Securities Services Colombia S.A. Sociedad Fuduciaria Croatia Privredna Banka Zagreb d.d. Cyprus HSBC France, Athens Branch Czech Republic Ceskoslovenska obchodni banka, a. s. Denmark Skandinaviska Enskilda Banken AB Egypt HSBC Bank Egypt Ltd Estonia SEB Pank Finland Skandinaviska Enskilda Banken AB France CACEIS Bank Germany HSBC Trinkaus & Burkhardt AG Ghana Standard Chartered Bank Ghana Ltd Greece HSBC France, Athens Branch Hong Kong The Hongkong & Shanghai Banking Corporation Ltd (Hong Kong) Hungary UniCredit Bank Hungary Zrt. India The Hongkong & Shanghai Banking Corporation Ltd (India) Indonesia PT Bank HSBC Indonesia Ireland HSBC Bank plc Israel Bank Leumi le‐Israel BM Italy BNP Paribas Securities Services Japan The Hongkong & Shanghai Banking Corporation Ltd (Japan) Jordan Bank of Jordan Plc Kazakhstan JSC Citibank Kazakhstan Kenya Standard Chartered Bank Kenya Ltd HSBC Bank plc, Luxembourg Branch 16, Boulevard d’Avranches, B.P. -

HSBC Holdings

Competing in the New Normal Michael Geoghegan 29 September 2009 Forward-looking statements This presentation and subsequent discussion may contain certain forward- looking statements with respect to the financial condition, results of operations and business of the Group. These forward-looking statements represent the Group’s expectations or beliefs concerning future events and involve known and unknown risks and uncertainty that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Additional detailed information concerning important factors that could cause actual results to differ materially is available in our Interim Report. Past performance cannot be relied on as a guide to future performance. 2 Strong Core Foundations A diversified business By customer group Profit before tax1 1H08 US$10,774m 2H08 US$9,097m 1H09 US$5,019m 8,346 6,298 4,611 2,840 2,690 2,583 2,432 822 793 625 632 (189) (1,249) (3,250) (3,094) Personal Financial Services Commercial Banking Global Banking and Markets Private Banking Other Note: (1) Excluding goodwill impairment on North American PFS business 4 A diversified business By geography Profit before tax1 1H08 US$10,774m 2H08 US$9,097m 1H09 US$5,019m 5,692 5,177 3,073 2,976 2,634 2,388 2,501 2,088 2,022 1,266 990 771 756 643 580 (2,366) (2,598) (3,703) Hong Kong RoAP Middle East Latin America Europe North America Note: (1) Excluding goodwill impairment on North American PFS business 5 Financial strength Capital Movement in Tier 1 capital,