CONNECTING LIVES in OUR DIGITAL WORLD Humanising Financial Services

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Raoul Named Brand of the Year at the World Branding Awards

Raoul named Brand of the Year at the World Branding Awards LONDON, October 28, 2014 – Raoul was named “Brand of the Year” in the “Fashion – Singapore” category at the 2014 World Branding Awards. 68 brands from 25 countries were honoured at a glittering awards ceremony at the prestigious One Whitehall Place in London over the weekend. Global winners include Apple, Coca-Cola, Del Monte, Heinz, HSBC, Louis Vuitton, McDonald’s, Samsung, Sony PlayStation and VISA. Other national tier winners from Singapore include Singtel and Marina Bay Sands. The awards was organised by the World Branding Forum, a global non-profit organisation which produces, manages and supports a wide range of programmes covering research, development, education, recognition, networking and outreach. It is also involved with research and development, the implementation of standards, best practice guidelines and tools, as well as other relevant branding initiatives. Richard Rowles, chairman of the World Branding Forum said, “It takes years to build a strong brand, and brands that make the list at these awards deserve recognition. Their work inspire those who work in the branding industry, and these are also brands that have a strong relationship with consumers. In addition to a brand valuation, voting by consumers show that connection that winning brands have with the general public.” The awards recognised some of the best global and national brands for their work and achievements. Uniquely, winners were judged through four streams: brand valuation, consumer market research, public online voting, as well voting by the World Branding Forum Advisory Council, which is made up of luminaries from the world of branding. -

Dato' Fam Lee Ee

55 AIRASIA BERHAD Annual Report 2015 Dato’ Fam Lee Ee, Malaysian, aged 55, was appointed an Independent Non-Executive Director of the Company on 8 October 2004. He was re-designated as Senior Independent Non-Executive Director on 20 August 2014. He is a member of the Audit Committee and Chairman of the Nomination and Remuneration Committee of the Board. He received his BA (Hons) from the University of Malaya in 1986 and LLB (Hons) from the University of Liverpool, England in 1989. Upon obtaining his Certificate of Legal Practice in 1990, he has been practising law since 1991 and is currently a senior partner at Messrs YF Chun, Fam & Yeo. Dato’ Fam used to sit on the Board of Trustees of Yayasan PEJATI from 1996 to 2007. Since 2001, he has served as a legal advisor to the Chinese Guilds and Association and charitable organisations such as Yayasan SSL Haemodialysis Centre in PJ. Dato’ Fam is also a Non-Independent Non-Executive Director of AirAsia X Berhad. dato’ fam lee ee Senior Independent Non-Executive Director Malaysian Leadership 55 AIRASIA BERHAD Annual Report 2015 DATO’ ABDEL AZIZ@@ABDUL AZIZ BIN ABU BAKAR Non-Independent Non-Executive Director Malaysian Dato’ Abdel Aziz @ Abdul Aziz Bin Abu Bakar, Malaysian, aged 62, was appointed a Non-Executive Director of the Company on 20 April 2005. On 16 June 2008, he was re-designated as Non-Executive Chairman and, subsequently, as a Non-Independent Non-Executive Director in November 2013. He is also a member of the Audit Committee and Nomination and Remuneration Committee. -

2015 WORLD BRANDING AWARDS: TANDUAY BAGS BRAND of the YEAR HONORS by ARGIE C

THE PHILIPPINE STAR I-4 F EATURES MONDAY, OCTOBER 19, 2015 2015 WORLD BRANDING AWARDS: TANDUAY BAGS BRAND OF THE YEAR HONORS By ARGIE C. AGUJA TDI-VP for Distillery Operations Gerry Tee n recognition of the Filipino spirit of receives the “Brand of the resiliency, dedication, and tradition of Year” award for Tanduay excellence, the World Branding Forum in the recently concluded I(WBF) recently named Tanduay as its “Brand World Brand Awards of the Year” in the Spirits - Rum category during held last September 24 the recently concluded World Branding Awards at The State Apartments, last September 24 at The State Apartments, Kensington Palace in Kensington Palace in London. London. From a pool of 2,600 brands from 35 countries, Tanduay was among the 118 brands selected to receive the prestigious award where some of the world’s best brands are recognized for their work (From left) National and achievements. Consequently, Tanduay is the marketing manager Garry only brand in the Spirits - Rum category from the Ong, AVP for Marketing Philippines to be selected for this year’s Awards. Paul Lim, and Tee The delegation, composed of Tanduay Distillers, representing Tanduay Inc. (TDI) VP for Distillery Operations Gerry during the awards night. Tee, AVP for Marketing Paul Lim and national manager Garry Ong, represented the brand and received the award. The winners National winners from the Philippines include Ayala Land, Jollibee and Puregold. Meanwhile, national tier winners from around the world to the voice of at least 65,000 consumers across include Barclays, BBC, British Airways, Thomas the world. -

AAX AR 2016 AR B.Pdf

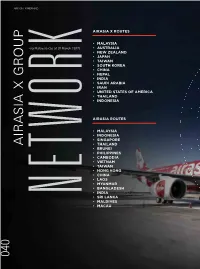

AIRASIA X BERHAD AIRASIA X ROUTES • MALAYSIA via Malaysia (as at 31 March 2017) • AUSTRALIA • NEW ZEALAND • JAPAN • TAIWAN • SOUTH KOREA • CHINA • NEPAL • INDIA • SAUDI ARABIA • IRAN • UNITED STATES OF AMERICA • THAILAND • INDONESIA AIRASIA ROUTES • MALAYSIA • INDONESIA • SINGAPORE AIRASIA X GROUP AIRASIA • THAILAND • BRUNEI • PHILIPPINES • CAMBODIA • VIETNAM • TAIWAN • HONG KONG • CHINA • LAOS • MYANMAR • BANGLADESH NETWORK • INDIA • SRI LANKA • MALDIVES • MACAU 040 SOUTH KOREA JAPAN CHINA IRAN NEPAL UNITED STATES OF AMERICA BANGLADESH SAUDI ARABIA HONG KONG MYANMAR TAIWAN LAOS MACAU INDIA THAILAND VIETNAM CAMBODIA PHILIPPINES SRI LANKA BRUNEI MALAYSIA MALDIVES SINGAPORE INDONESIA AUSTRALIA NEW ZEALAND AIRASIA ROUTES AIRASIA X ROUTES Creating opportunity through leasing With 90 customers in 50 countries, Macquarie AirFinance has the breadth and expertise to help any airline seize opportunities. Let us discuss how we can help you. Asia Europe, the Middle East and Africa Americas Singapore Dublin San Francisco +65 6601 0051 +353 1 238 3200 +1 415 829 6600 To learn more, contact us or visit www.macquarie.aero macquarie.com Except for Macquarie Bank Limited (Australian Credit Licence (ACL) 237502) ABN 46 008 583 542 (MBL), any Macquarie entity referred to on this page is not an authorised deposit-taking institution for the purposes of the Banking Act 1959 (Cth). That entity’s obligations do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of that entity, unless noted otherwise. Before making a decision about whether to acquire a credit or lending product, a person should obtain and review the terms and conditions relating to that product and also seek independent financial, legal and taxation advice. -

Coco, Heinz, LEGO , Neutrogena and Spotify Amongst 318 Winners At

CoCo, Heinz, LEGO®, Neutrogena® and Spotify Amongst 318 Winners at the 2019 World Branding Awards at Kensington Palace November 14, 2019 03:00 PM Eastern Standard Time LONDON--(BUSINESS WIRE)--The prestigious World Branding Awards, the ultimate global brand recognition accolade – now in its 10th edition, saw 318 brands from 41 countries named “Brand of the Year” in a glittering ceremony held at the State Apartments of Kensington Palace today. The brands were nominated by over 230,000 consumers across the globe. Beijing Tong Ren Tang, CHAI LI WON, CoCo, Heinz, IKEA, JinkoSolar, LEGO®, Netflix, Neutrogena®, Spotify and Yakult were proudly announced as this year’s Global Tier winners. Regional Tier winners included Aramex (United Arab Emirates); Elkjøp (Norway); H&M (Sweden); Lancôme (France); Naturgy (Spain); Optical 88 (Hong Kong); LuLu (United Arab Emirates); Isetan (Japan); and ZALORA (Singapore). National Tier winners included Airland (Hong Kong), Amarula (South Africa), Aqua Gulf (Kuwait), Bango (Indonesia), BreadTalk (Singapore), Cadbury (United Kingdom), De’Longhi (Italy), FERN-D (Philippines), Glo (Nigeria), Gourmet (Pakistan), Grandiosa (Norway), Java House (Kenya), Kaspersky (Russia), Media Markt (Germany), Milton (India), MR D.I.Y. (Malaysia), Nahdi (Saudi Arabia), Natural Aqua Gel Cure (Japan), Özdilek (Turkey), Thai Airways (Thailand), The Lost Paradise of Dilmun Water Park (Bahrain), THOMY (Switzerland), and Yelmo Cines (Spain). Winners are uniquely judged through three streams: brand valuation, consumer market research, and public online voting. Seventy percent of the scoring process comes from consumer votes. There can only be one winner in each category per country. “The Awards are an acknowledgement to the tireless effort of the teams that build and maintain their brand presence in an ever-changing market,” said Richard Rowles, Chairman of the World Branding Forum. -

Kuwaittimes 5-11-2018.Qxp Layout 1

SAFAR 27,1440 AH MONDAY, NOVEMBER 5, 2018 27º 28 Pages Max 150 Fils Established 1961 Min 22º ISSUE NO: 17675 The First Daily in the Arabian Gulf www.kuwaittimes.net Roche opens new diagnostic Sacked Lanka PM residence Pakistani porters: Unsung Unseeded Khachanov stuns 3 center in Symphony complex 9 a symbol of power struggle 22 masters of the mountains 28 Djokovic to win Paris Masters Election of Assembly legislative panel chief leads to resignations Controversy continues over membership of Harbash, Tabtabaei By B Izzak and reviews all proposed laws to establish if they are in line with the constitution, before sending them to the KUWAIT: Two opposition members of the National concerned Assembly committees. But like other Assembly’s legal and legislative committee resigned from Assembly panels, its decisions are not final as the the panel yesterday, barely a few days after their elec- Assembly can change them. tion, after the panel elected a pro-government lawmaker Meanwhile, controversy over the membership of to lead it. The seven members of the panel were elected opposition MPs Waleed Al-Tabtabaei and Jamaan Al- during the new Assembly term’s opening day on Tuesday Harbash continued, with new constitutional and legal - four members were pro-government, including three opinions. In an unprecedented decision, the Assembly Shiites, and three others were opposition Islamists. on Tuesday voted to keep the membership of the two On the day of the election, Islamist MP Mohammad lawmakers even after they were jailed in a final ruling Hayef said he is quitting the panel and did not attend its by the court of cassation for storming the Assembly first meeting yesterday when the panel met and elected building in Nov 2011. -

African Business

The Bestselling Pan-African Business Magazine Our Top 100 Who, where, why and how much? Interview Thebe Ikalafeng, Founder, Brand Africa Ecobank Building an iconic brand MTN Taking Africa global African Why local brands need to own the African space INSIDE Breakdown of Africa’s favourite brands BUSINESSAn IC Publication 48th Year Special Edition November 2015 by category, and how much they’re worth The definitive ranking of Africa’s most admired and most valuable brands An independent African Business Brand Africa 100 report supported by MTN TopBrandsCover.indd 2 21/10/2015 09:42 EVERY DAY, OUR ENERGY KEEPS THE WHEELS OF BUSINESS TURNING AND TURNING We set businesses free. Free from worrying about the We have been investing and innovating in sub-Saharan quality and supply of the fuels, lubricants and LPG they Africa for over 25 years. Asking businesses, large and rely on day after day. Free to focus on what they do best. small, what they need most. We then provide the energy solutions that keep them moving and growing. We master every stage of the process from sourcing, blending and storage to distribution, on-site management Our integrated energy platform is simple yet remarkable. and waste disposal. So you can rest assured that we can Our energy keeps the wheels of your business turning help your business run smoothly and reliably. and turning. So you can devote your energy to making it a success. oryxenergies.com TopBrandsCover.indd 4 20/10/2015 15:36 in association with UNITED KINGDOM IC PUBLICATIONS 7 Coldbath Square London EC1R 4LQ Tel: +44 20 7841 3210 Fax: Admin +44 20 7713 7898 Editorial: +44 20 7841 3211 [email protected] www.africanbusinessmagazine. -

News Release Raffleseducationcorp

NEWS RELEASE RAFFLESEDUCATIONCORP BAGGED TWO PRESTIGIOUS AWARDS IN 2015 Best Company for Leadership in Private Education in the Asia Pacific Brand of the Year 2015 National Award Singapore, 11 May 2015 - Raffles Education Corporation Limited (“RafflesEducationCorp”) received two prestigious awards in March 2015, namely the IAIR Awards in Hong Kong and World Branding Awards in Paris, France. The IAIR Awards held at the Conrad Hong Kong Hotel on 10 March recognised more than 50 companies for their leadership in strategic fields across sectors such as Corporate, Property Sustainability and Finance in the Asia Pacific and worldwide. RafflesEducationCorp was recognised as the Best Company for Leadership in Private Education in the Asia Pacific under IAIR Corporate Awards 2015. From left to right: Mr Scott Chew, Executive Director and Deputy CEO of RafflesEducationCorp, received the prestigious Award from Mr. Guido Giommi, President of IAIR Group. The World Branding Awards 2015 organised by the World Branding Forum (WBF), a global non-profit organisation dedicated to advancing branding standards for the good of the branding community and consumers, was held at the iconic Hilton Paris Opera on 24 March. Page 1 of 4 The awards ceremony honoured 50 international brands in luxury, fashion, lifestyle, hospitality, service, food and beverage from 22 countries. Some notable global winners included Cartier, Gucci, Hermes, Prada, IKEA, Nike and many more. The Awards recognised the best global and national brands for their work and achievements. Uniquely, winners were judged through four streams: brand valuation, consumer market research, public online voting, as well as voting by the World Branding Forum Advisory Council. -

Club Med Named « Brand of the Year » at the World Branding Awards

Press Release, October 26, 2017 Club Med named « Brand of the Year » at the World Branding Awards Club Med, the global leader of all-included luxury holidays, received for the 2nd time “Brand of the Year” award in the “Resorts” category during a ceremony which took place at Kensington Palace on October, 11th. For the second time, Club Med stands out during the World Branding Awards from among more than 3000 nominees. This ceremony, during which 245 companies from 32 countries around the world received awards, rewarded Club Med as “Brand of the Year” in the “Resorts” category. This fourth instalment of the World Branding Awards put forwards brands from the food, luxury, lifestyle, hotel and services industries as major French and international brands such as L’Oréal, Cartier, Facebook, Google, Samsung, Qatar Airways and more all received awards. Club Med is proud to receive this distinction which honors the efforts of its 23.000 collaborators working in 30 countries around the brand value and specifically all their actions for the brand platform “Amazing You / Vous Etonnez” and their actions on social medias. This award is an appreciation from professionals and the reflect of Club Med’s awareness as 70% of votes come from consumers. The World Branding Awards: recognizing businesses The World Branding Forum (WBF) is an international non-profit organization that aims to advance branding standards for the benefit of brands and consumers. It organizes and sponsors a range of educational programs and collaborates with leading universities and museums. Seen as the best international reward, brands are evaluated based on three criteria: brand valuation, consumer market research, and public online voting. -

Board of Directors' Profile

Annual Report 2016 BOARD OF DIRECTORS’ PROFILE TAN SRI DATO’ MEGAT ZAHARUDDIN BIN MEGAT MOHD NOR DATUK ABDUL FARID BIN ALIAS Non-Independent Non-Executive Director Non-Independent Executive Director (Chairman) (Group President & Chief Executive Officer) Nationality / Age / Gender: Malaysian / 68 / Male Malaysian / 49 / Male Date of Appointment: 1 October 2009 2 August 2013 Academic / Professional • Associate of the Royal School of Mines, UK • Master of Business Administration (Finance), University of Denver, USA Qualification(s): • Bachelor of Science (Hons) in Mining Engineering, Imperial College of Science & • Bachelor of Science in Accounting, Pennsylvania State University, University Park, USA Technology, University of London, UK • Advanced Management Programme, Harvard Business School, Harvard University, USA Working Present: Present: Experience: Within Maybank Group Within Maybank Group • Chairman/Director of Maybank • Group President & Chief Executive Officer/Executive Director of Maybank • Chairman/Director of Maybank Ageas Holdings Berhad • Director of Maybank Investment Bank Berhad • President Commissioner of PT Bank Maybank Indonesia Tbk • Director of Maybank Ageas Holdings Berhad • Commissioner of PT Bank Maybank Indonesia Tbk Other Companies/Bodies • Director of Etiqa International Holdings Sdn Bhd • Director of The ICLIF Leadership and Governance Centre, Malaysia Other Companies/Bodies Past: • Chairman of The Association of Banks in Malaysia • Chairman of PADU Corporation from August 2013 to September 2016 • Vice Chairman -

Demand for Spanish Food Exports to Qatar on the Rise, Says Envoy

US BLOW | Page 2 GROWING TIES | Page 4 Iran sanctions Pakistan and move hits China sign 15 Europe fi rms deals, MoUs Sunday, November 4, 2018 Safar 26, 1440 AH TOURIST ATTRACTIONS: Page 20 GULF TIMES Nepal is off ering ‘huge potential’ for BUSINESS Qatari investors Demand for Spanish food exports to Qatar on the rise, says envoy By Peter Alagos ers and their engagement with our excellent quality, country the chance to sample Spanish cuisine.” from the supply side, participating in exhibitions Business Reporter but very competitive supply of food and beverage, As Spain’s new ambassador to Qatar, Alfaro said under the Spanish pavilion, such as Hospitality make them a close partner for the Spanish provid- she is looking forward to further strengthening the Qatar. The Spanish technology on agriculture pro- ers,” the ambassador said. Alfaro ties between Qatar and Spain, in- duction is also contributing to the local manufac- eading food distributors in the country are pointed out that more companies More companies in Qatar cluding “co-operation relations turing,” Alfaro said. importing more products from Spain, a trend in the Qatari market are eliminat- are eliminating the “middle in all fi elds – political, economic, Earlier, former Spanish ambassador to Qatar, Ig- Lthe Spanish embassy in Doha is determined ing the “middle man” by import- man” by importing products cultural, and educational.” She nacio Escobar, had told Gulf Times that plans are to maintain, according to Spanish ambassador Be- ing the products directly from directly from Spanish food added that the embassy is work- underway for a greenhouse project in Qatar, which len Alfaro. -

Vietnam Could Give Tech Companies One Year to Comply with Cyberlaw

SUNDAY, NOVEMBER 4, 2018 11 Lulu ‘Brand of the Year’ The only hypermarket brand to win this top honour at World Branding Awards 2018 World Branding The fact that Awards• are the top this award is recognition given to an primarily based organization or brand on public survey and customer TDT | London feedback, makes this recognition uLu hypermarket & shop- much more valuable Lping won the ‘Brand of the for us Year’ award in the Retail cate- ASHRAF ALI MUSLIAM gory at the 2018 World Branding Award Ceremony yesterday. World Branding Awards are the top recognition given to an organisation or brand for their Kensington Palace. path-breaking and innovative “We are obviously very de - branding, marketing & com - lighted and proud to be chosen munication initiatives over the as the top global brand and the years and are regarded as the fact that this award is primar- top benchmark in the industry. ily based on public survey and Ashraf Ali Musliam, Exec- customer feedback, makes this utive Director of Lulu Group, recognition much more valua- received the award from Rich- ble for us,” said Ashraf Ali after ard Rowles, the Chairman of receiving the award. World Branding Forum, in the Other global brands awarded presence of top business leaders Ashraf Ali Musliam, Executive Director of LuLu Group along with Adeeb Ahamed, MD of LuLu Financial Group, Shafeena Yusuffali, CEO of Tablez, Mohammed Althaf at the ceremony included Brit- and dignitaries from around the Director and V. Nandakumar, CCO of LuLu Group with the Brand of The Year Trophy at the World Branding Award Ceremony yesterday at the Kensington Palace in ish Airways, Nescafe, Omantel, world at a function held at the London Nippon, etc.