Power Finance Corporation Ltd.: Change in Limits

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

India Capital Markets Experience

Dorsey’s Indian Capital Markets Capabilities March 2020 OVERVIEW Dorsey’s capital markets team has the practical wisdom and depth of experience necessary to help you succeed, even in the most challenging markets. Founded in 1912, Dorsey is an international firm with over 600 lawyers in 19 offices worldwide. Our involvement in Asia began in 1995. We now cover Asia from our offices in Hong Kong, Shanghai and Beijing. We collaborate across practice areas and across our international and U.S. offices to assemble the best team for our clients. Dorsey offers a full service capital markets practice in key domestic and international financial centers. Companies turn to Dorsey for all types of equity offerings, including IPOs, secondary offerings (including QIPs and OFSs) and debt offerings, including investment grade, high-yield and MTN programs. Our capital markets clients globally range from emerging companies, Fortune 500 seasoned issuers, and venture capital and private equity sponsors to the underwriting and advisory teams of investment banks. India has emerged as one of Dorsey’s most important international practice areas and we view India as a significant market for our clients, both in and outside of India. Dorsey has become a key player in the Indian market, working with major global and local investment banks and Indian companies on a range of international securities offerings. Dorsey is recognized for having a market-leading India capital markets practice, as well as ample international M&A and capital markets experience in the United States, Asia and Europe. Dorsey’s experience in Indian capital markets is deep and spans more than 15 years. -

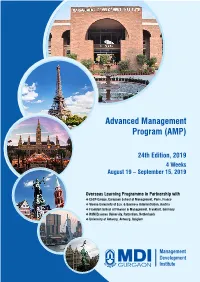

Advanced Management Program (AMP)

Advanced Management Program (AMP) 24th Edition, 2019 4 Weeks August 19 – September 15, 2019 Overseas Learning Programme in Partnership with ESCP-Europe, European School of Management, Paris, France Vienna University of Eco. & Business Administration, Austria Frankfurt School of Finance & Management, Frankfurt, Germany RSM Erasmus University, Rotterdam, Netherlands University of Antwerp, Antwerp, Belgium Advanced Management Program (AMP) 24th Edition, 2019 STRATEGIC LEADERSHIP TRANSFORMATION IN THE DIGITAL AGE With the advent of digital technology, the concept of doing business has completely transformed. The agile, dynamic and hyper-linked work environment requires organizations to redefine the competencies of an effective leader in the digital era. Everyday communication is rapidly changing to virtual domains, based on continuously evolving social media platforms like Linkedin, twitter, instagram, pinterest and so on. Organizations have started realizing that the increased uses of internet applications, and social media has made today’s employees and customer more aware than ever. The traditional market place has taken a shape of digital platforms. Suppliers and customers meet directly, and the middle layers are disappearing. Manufacturing organizations earn a large part of their revenue from services. Therefore, focus on cost and process control is becoming as important as sales. The entire supply chain including suppliers and customers are becoming global. In order to understand the cross cultural issues and the best practices across the globe, global benchmarking is becoming essential. Rapid changing business environment has increased the pressure on the key performance measures of an organization. An organization cannot merely remain competitive only in one of the few dimensions of business performances such as cost, quality, service, agility, or speed. -

Press Release REC Limited

Press Release REC Limited March 30, 2021 Ratings Amount Facilities/Instruments Rating1 Rating Action (Rs. crore) Long term Market Borrowing CARE AAA; Stable 1,00,000.00 Assigned Programme for FY22 (Triple A; Outlook: Stable) 1,00,000.00 Total Long Term Instruments (Rs. One Lakhs Crore Only) CARE A1+ Commercial Paper issue for FY22 5,000.00 Assigned (A One Plus) Short term Market Borrowing CARE A1+ 5,000.00 Assigned Programme for FY22 (A One Plus) 10,000.00 Total Short Term Instruments (Rs. Ten Thousand Crore Only) Details of instruments/facilities in Annexure-1 Detailed Rationale & Key Rating Drivers The rating assigned to the market borrowing programme of REC Limited continues to factor in REC’s parentage as well as its strategic importance to Government of India (GoI) in the development of power sector in India. The rating factors in REC’s parentage as well as its strategic importance to Government of India (GoI) in the development of power sector in India. The rating also draws comfort from REC’s quasi-sovereign status that allows it to have a diversified resource profile, adequate profitability and comfortable capitalization levels. However the rating factors in risks associated with weakness in REC’s asset quality in exposure to private sector, high exposure to weak state power utilities and high sector-wise as well as borrower concentration risk. With respect to the acquisition of Government of India’s (GoI) existing 52.63% equity shareholding in REC Limited by Power Finance Corporation Limited (PFC; rated CARE AAA; Stable/ CARE A1+), the acquisition transaction was completed on March 28, 2019. -

Companhia De Saneamento De Minas Gerais GAIL (India) Limited

Vote Summary Report Date range covered: 07/01/2020 to 06/30/2021 Location(s): All Locations Institution Account(s): NBI Diversified Emerging Markets Equity Dino Polska SA Meeting Date: 07/02/2020 Country: Poland Primary Security ID: X188AF102 Record Date: 06/16/2020 Meeting Type: Annual Ticker: DNP Shares Voted: 12,894 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction Management Proposals Mgmt 1 Open Meeting Mgmt 2 Elect Meeting Chairman Mgmt For For For 3 Acknowledge Proper Convening of Meeting Mgmt 4 Approve Agenda of Meeting Mgmt For For For 5 Receive Management Board Report on Mgmt Company's and Group's Operations, Financial Statements, and Management Board Proposal on Allocation of Income and Dividends 6 Receive Supervisory Board Reports on Board's Mgmt Work, Management Board Report on Company's and Group's Operations, Financial Statements, and Management Board Proposal on Allocation of Income and Dividends 7 Receive Supervisory Board Requests on Mgmt Approval of Management Board Report on Company's and Group's Operations, Financial Statements, Management Board Proposal on Allocation of Income and Dividends, and Discharge of Management Board Members 8.1 Approve Management Board Report on Mgmt For For For Company's Operations 8.2 Approve Financial Statements Mgmt For For For 9 Approve Allocation of Income and Omission of Mgmt For For For Dividends 10.1 Approve Management Board Report on Group's Mgmt For For For Operations 10.2 Approve Consolidated Financial Statements Mgmt For For For 11.1 Approve -

Revision in Market Lot of Derivative Contracts on Individual Stocks

Department : FUTURES & OPTIONS Download Ref No: NSE/FAOP/45895 Date : September 30, 2020 Circular Ref. No: 87/2020 All Members, Revision in Market Lot of Derivative Contracts on Individual Stocks In pursuance of SEBI guidelines for periodic revision of lot sizes for derivatives contracts specified in the SEBI circular CIR/MRD/DP/14/2015 dated July 13, 2015, the market lots of derivatives contracts shall be revised as follows: Sr. Underlying whose Derivative Count of Annexure No Effective date contract size shall be Underlying Number October 30, 2020 (for Nov 1 Revised Downwards 15 1 2020 & later expiries) 2 Revised Upwards 12 October 30, 2020 (for Jan 2 2021 & later expiries) 3 Unchanged 108 - 3 Revised Downwards but new October 30, 2020 (for Jan 4 lot size is not a multiple of old 1 4 2021 & later expiries) lot size To avoid operational complexities, in case of Annexure 2 and 4 above, following will be applicable: 1. Only the far month contract i.e. January 2021 expiry contracts will be revised for market lots. Contracts with maturity of November 2020 and December 2020 would continue to have the existing market lots. All subsequent contracts (i.e. January 2021 expiry and beyond) will have revised market lots. 2. The day spread order book will not be available for the combination contract of Dec 2020 – Jan 2021 expiry. For the purpose of the computation, the average of the closing price of the underlying has been taken for one month period of September 1st – September 30th 2020. This circular shall come into effect from October 30, 2020. -

Executive Director in REC Limited, New Delhi.PDF

awl* f9fi*t. I REC Limited (Formerly Rural Electrification Corporation Limited) (TI-Va 1-1-tebi-1 Th-t 's e) / (A Government of India Enterprise) REC Regd. Office: Core•4, SCOPE Complex, 7, Lodhi Road, New Delhi 110 003 t:trilft-tx Endless enemy. Infinite possibilities. Tel: +91-11-4309 1500 I Fax: +91-11-2436 0644 I Website: www.recindia.com CIN : L4010101.1969001005095 l GST No.: 07AAACR4512R123 No.CMD/SM/REC/2021/22 To, The Chief Secretaries of all States Sir, Subject: Filling up of the post of Executive Director in REC Limited, New Delhi on deputation - reg. REC Limited, a Navaratna CPSE under the administrative control of the Ministry of Power, Government of India, is the nodal agency for implementation of several programs of the Government of India such as the Rajiv Gandhi Gramin Vidyut Yojana (RGGVY), Saubhagya (Pradhanmantri Sahaj Bijli Har Ghar Yojana), DDUGJY (Deendayal Upadhyaya Gram Jyoti Yojana), UDAY (Ujwal Discom Assurance Yojana) among many others. The Company is also poised to be a Nodal Agency for the proposed 'Revamped Distribution Scheme' targeted at improving the performance of the Discoms in the country. 2. To execute these programs, we have two posts of Executive Directors to be tilled by senior officers from the government on deputation. One IAS officer of Director rank is already working as Executive Director on deputation in the Company. We intend to fill the other vacant post of Executive Director on deputation basis. This is to request you to kindly forward names of suitable IAS officers at Deputy Secretary/Director rank for the post by 05th March, 2021. -

Calendar of Interest and Redemption for FY 2021-22- 24.08.2021

Calendar of Interest/Redemptions Due/Paid for FY 2021-22 Interest Due Interest Payment Redemption Due Redemption Sr No Issuer Name ISIN Number Date Date Remarks Date Payment Date Remarks 1North Eastern Electric Power Corporation Ltd INE636F07183 4/1/2021 3/31/2021 Paid 2 National Highways Authority of India INE906B07EJ8 01-04-2021 01-04-2021 Paid 3 National Highways Authority of India INE906B07EF6 01-04-2021 01-04-2021 Paid 4 National Highways Authority of India INE906B07EG4 01-04-2021 01-04-2021 Paid 5 National Highways Authority of India INE906B07EL4 01-04-2021 01-04-2021 Paid 6 National Highways Authority of India INE906B07EK6 01-04-2021 01-04-2021 Paid 7 National Highways Authority of India INE906B07EE9 01-04-2021 01-04-2021 Paid 8 National Highways Authority of India INE906B07EH2 01-04-2021 01-04-2021 Paid 9 National Highways Authority of India INE906B07EI0 01-04-2021 01-04-2021 Paid AP - Paid TS- Delay in receiving the funds from 10 Andhra Pradesh Power Finance Corporation Ltd INE847E08DL4 01-04-2021 3/31/2021 Telangana Govt. AP - Paid TS- Delay in receiving the funds from 11 Andhra Pradesh Power Finance Corporation Ltd INE847E08DM2 01-04-2021 3/31/2021 Telangana Govt. AP - Paid TS- Delay in receiving the funds from 12 Andhra Pradesh Power Finance Corporation Ltd INE847E09029 01-04-2021 3/31/2021 Telangana Govt. AP - Paid TS- Delay in receiving the funds from 13 Andhra Pradesh Power Finance Corporation Ltd INE847E08DK6 01-04-2021 3/31/2021 Telangana Govt. AP - Paid TS- Delay in receiving the funds from 14 Andhra Pradesh Power Finance Corporation Ltd INE847E08DJ8 01-04-2021 3/31/2021 Telangana Govt. -

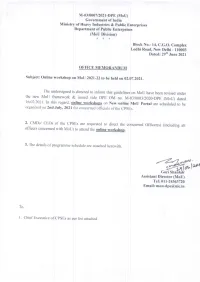

OM for Online Workshop on Mou 2021-22 to Be Held on 02.07

M-03/0007/2021-DPE (MoU) Government of India Ministry of Heavy Industries & Public Enterprises Department of Public Enterprises (MoU Division) * * * Block No.- 1 4 , C.G.O. Complex Lodhi Road, New Delhi - 110003 Dated: 29"" June 2021 OFFICE MEMORANDUM Subject: Online workshop on MoU 2021-22 t o be h e l d on 02.07.2021. The undersigned is directed to inform that guidelines o n MoU h a v e b e e n revised u n d e r t h e new MoU framework & issued vide DPE OM n o . M-03/0003/2020-DPE (MoU) dated 16.02.2021. I n t h i s regard, online workshops on New online MoU Portal a r e scheduled to b e organized on 2nd J u l y , 2021 f o r concerned officials of t h e CPSEs. 2. CMDs/ CEOs of t h e CPSEs a r e requested to d i r e c t t h e concerned O f f i c e r ( s ) ( including all officers concerned with MoU) to attend t h e online workshop. 3 . T h e d e t a i l s of programme schedule a r e attached herewith. Go ae: Fa). oto |2™ Gori Shankar Assistant Director (MoU) Tel: 011-24363720 Email: [email protected] To, 1 . C h i e f Executive of CPSEs as p e r list attached Department of Public Enterprises MoU 2021-22 Schedule of Online Workshop on New online MoU portal Venue: Conference Room No. -

A Journey Towards

A Journey Towards InfinityUnfolding the story through Panchatatva YEARS AND BEYOND... GLORIOUS PAST, INSPIRING FUTURE YEARS AND BEYOND... The journey continues The Konark Sun Temple, a thirteenth-century Sun Temple (also known as the Black Pagoda), built-in Orissa red sandstone (Khandolite) and black granite by King Narasimhadeva I (AD 1236-1264) of the Ganga dynasty. The Sun Temple was constructed towards the end of Odisha's temple-building phase in the 13th century by King Narasimha Deva I of the Eastern Ganga Dynasty (whose great grandfather renovated the Jagannath Temple in Puri). Dedicated to Surya the Sun God, it was made as his colossal cosmic chariot with 12 pairs of wheels pulled by seven horses (sadly, only one of the horses remains). ! fo'okfu nso lfornZqfjrkfu ijklqo! ;n~ HknzarUUk vk lqo!! Om. O God, the creator of the universe and the Giver of all happiness. Keep us far from bad habits, bad deeds, and calamities. May we attain everything that is auspicious. The Sun is the source of infinite energy. India has since time immemorial, celebrated the enormous power of “Surya” as a benevolent benefactor and a supreme nurturer. REC's logo is a tribute to the all-powerful Sun and its aspirations to tap the possibilities as endless as the Sun's energy, as reflected in the tagline “Endless Energy, Infinite Possibilities”. Kedarnath temple, Uttarakhand I am happy to know that REC Limited (RECL) is bringing out a publication celebrating 51 years of its service to the nation. REC Limited, since its inception in 1969, has been at the forefront of the electrification drive as the nodal agency for Ministry of Power’s rural electrification programs. -

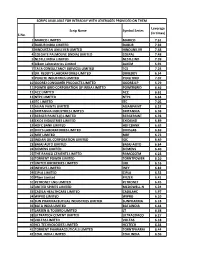

S.No. Scrip Name Symbol Series Leverage (In Times) 1 MARICO

SCRIPS AVAILABLE FOR INTRADAY WITH LEVERAGES PROVIDED ON THEM Leverage Scrip Name Symbol Series (in times) S.No. 1 MARICO LIMITED MARICO 7.61 2 DABUR INDIA LIMITED DABUR 7.92 3 HINDUSTAN UNILEVER LIMITED HINDUNILVR 7.48 4 COLGATE PALMOLIVE (INDIA) LIMITED COLPAL 7.48 5 NESTLE INDIA LIMITED NESTLEIND 7.39 6 Alkem Laboratories Limited ALKEM 6.91 7 TATA CONSULTANCY SERVICES LIMITED TCS 7.24 8 DR. REDDY'S LABORATORIES LIMITED DRREDDY 6.54 9 PIDILITE INDUSTRIES LIMITED PIDILITIND 7.07 10 GODREJ CONSUMER PRODUCTS LIMITED GODREJCP 5.79 11 POWER GRID CORPORATION OF INDIA LIMITED POWERGRID 6.46 12 ACC LIMITED ACC 6.61 13 NTPC LIMITED NTPC 6.64 14 ITC LIMITED ITC 7.05 15 ASIAN PAINTS LIMITED ASIANPAINT 6.52 16 BRITANNIA INDUSTRIES LIMITED BRITANNIA 6.98 17 BERGER PAINTS (I) LIMITED BERGEPAINT 6.78 18 EXIDE INDUSTRIES LIMITED EXIDEIND 6.89 19 HDFC BANK LIMITED HDFCBANK 6.63 20 DIVI'S LABORATORIES LIMITED DIVISLAB 6.69 21 MRF LIMITED MRF 6.73 22 INDIAN OIL CORPORATION LIMITED IOC 6.49 23 BAJAJ AUTO LIMITED BAJAJ-AUTO 6.64 24 SIEMENS LIMITED SIEMENS 6.40 25 THE RAMCO CEMENTS LIMITED RAMCOCEM 6.23 26 TORRENT POWER LIMITED TORNTPOWER 6.10 27 UNITED BREWERIES LIMITED UBL 6.16 28 INFOSYS LIMITED INFY 6.82 29 CIPLA LIMITED CIPLA 6.52 30 Pfizer Limited PFIZER 6.41 31 PETRONET LNG LIMITED PETRONET 6.45 32 UNITED SPIRITS LIMITED MCDOWELL-N 6.24 33 CADILA HEALTHCARE LIMITED CADILAHC 5.97 34 WIPRO LIMITED WIPRO 6.10 35 SUN PHARMACEUTICAL INDUSTRIES LIMITED SUNPHARMA 6.18 36 BATA INDIA LIMITED BATAINDIA 6.44 37 LARSEN & TOUBRO LIMITED LT 6.38 38 ULTRATECH CEMENT -

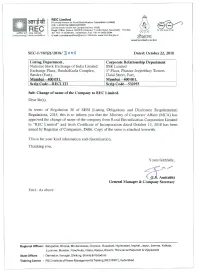

Change of Name of the Company to REC Limited

REC Limited (Formerly known as Rural Electrrficallon Corpomtlon Limited) cw : L40101DL195SGOIODEOSS (Incorporated underlhe Companles Act, 1956) Raga. omce: Core-4, SCOPE Complex, 7 Learn Road, New new r 110 003 W $741,311? mam Tel +9141724365161 43091500 l Fax ~51711-2436 0644 a ndless energy 24mg gosslbilmes E-msil- complianceomoer®recl m l Website www reclndla gov m SEC-l/187(2)/2018/ 3 O O 6 Dated: October 22, 2018 Listing Department, Corporate Relationship Department National Stock Exchange of India Limited BSE Limited Exchange Plaza, BandraKurla Complex, 1‘l Floor, Phiroze J eejeebhoy Towers Bandra (East), Dalal Street, Fort, Mumbai — 400 051. Mnmhai 7 400 001. Scrip Code—RECLTD Scrip Code—532955 Sub: Change of name of the Company to REC Limited. Dear Sir(s), In terms of Regulation 30 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, this is to inform you that the Ministry of Corporate Affairs (MCA) has approved the change of name of the Company from Rural Electrification Corporation Limited to “REC Limited" and fresh Certificate of Incorporation dated October 13, 2018 has been issued by Registrar of Companies, Delhi Copy of the same is attached herewith This is for your kind information and dissemination. Thanking you, Yours faithfully, // . Amitabh) General Manager & Company Secretary Encl.‘ As above Regional Offices: Bangalore, Bhopal, Bhubaneswar, Chennal, Guwehati, Hyderabad, Imphal, Jaipur. Jammu, Kolkala, Lucknow, Mumbai, Panchkula, Patna, Raipur, Ranchi, Thiruvananthapuram &Vijayawada State Offices : Dehmdun, ltanagar. Shillong, Shlmla &Vadodara TrainingCentre : RECInsllluleofPowerManagement&Tralning(RECIPMT),Hyderabad 1132133 W3 GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS Office ofthe Registrar ofCompanies 4th Floor, IFCI Tower 61, New Delhi, Delhi, India, 110019 Certificate of Incorporation pursuant to change of name [Pursuant to rule 29 of the Companies (Incorporation) Rules. -

NSE Symbol NSE 6 Month Avg Total Market

Average Market Cap of 200 listed companies on BSE & NSE for the six months ended 30 June 2021 BSE 6 month Avg NSE 6 month Avg Average of BSE and NSE 6 Total Market Cap Total Market Cap month Avg Total Market Cap S.No. Company Name ISIN BSE SYMBOL (Rs. In Crs.) NSE Symbol (Rs. In Crs.) (Rs. in Crs.) 1 Reliance Industries Ltd INE002A01018 RELIANCE 1338017.01 RELIANCE 1355067.509 1346542.26 Tata Consultancy Services 2 Ltd. INE467B01029 TCS 1169783.56 TCS 1173068.166 1171425.86 3 HDFC Bank Ltd. INE040A01034 HDFCBANK 819037.95 HDFCBANK 818713.671 818875.81 4 Infosys Ltd INE009A01021 INFY 579784.19 INFY 579697.3885 579740.79 5 Hindustan Unilever Ltd., INE030A01027 HINDUNILVR 549336.78 HINDUNILVR 549358.908 549347.84 Housing Development 6 Finance Corp.Lt INE001A01036 HDFC 462288.58 HDFC 461373.1089 461830.84 7 ICICI Bank Ltd. INE090A01021 ICICIBANK 416645.51 ICICIBANK 416389.0234 416517.27 8 Kotak Mahindra Bank Ltd. INE237A01028 KOTAKBANK 361640.52 KOTAKBANK 361438.6361 361539.58 9 State Bank Of India, INE062A01020 SBIN 329767.32 SBIN 329789.268 329778.29 10 Bajaj Finance Limited INE296A01024 BAJFINANCE 324996.53 BAJFINANCE 324843.5005 324920.02 11 Bharti Airtel Ltd. INE397D01024 BHARTIARTL 299981.36 BHARTIARTL 299955.7729 299968.57 12 HCL Technologies Ltd INE860A01027 HCLTECH 261400.46 HCLTECH 261392.0109 261396.24 13 Wipro Ltd., INE075A01022 WIPRO 258617.45 WIPRO 261102.3994 259859.92 14 ITC Ltd INE154A01025 ITC 259423.16 ITC 259396.0648 259409.61 15 Asian Paints Ltd. INE021A01026 ASIANPAINT 253487.28 ASIANPAINT 253454.4536 253470.87 16 AXIS Bank Ltd.