M T a R T E C H N O L O G I E S Reaching for the Skies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

India Capital Markets Experience

Dorsey’s Indian Capital Markets Capabilities March 2020 OVERVIEW Dorsey’s capital markets team has the practical wisdom and depth of experience necessary to help you succeed, even in the most challenging markets. Founded in 1912, Dorsey is an international firm with over 600 lawyers in 19 offices worldwide. Our involvement in Asia began in 1995. We now cover Asia from our offices in Hong Kong, Shanghai and Beijing. We collaborate across practice areas and across our international and U.S. offices to assemble the best team for our clients. Dorsey offers a full service capital markets practice in key domestic and international financial centers. Companies turn to Dorsey for all types of equity offerings, including IPOs, secondary offerings (including QIPs and OFSs) and debt offerings, including investment grade, high-yield and MTN programs. Our capital markets clients globally range from emerging companies, Fortune 500 seasoned issuers, and venture capital and private equity sponsors to the underwriting and advisory teams of investment banks. India has emerged as one of Dorsey’s most important international practice areas and we view India as a significant market for our clients, both in and outside of India. Dorsey has become a key player in the Indian market, working with major global and local investment banks and Indian companies on a range of international securities offerings. Dorsey is recognized for having a market-leading India capital markets practice, as well as ample international M&A and capital markets experience in the United States, Asia and Europe. Dorsey’s experience in Indian capital markets is deep and spans more than 15 years. -

Dixon Technologies (India) Ltd. (Formerly Known As Dixon Technologies (India) Pvt

Dixon An ISO 9001 : 2008, 14001 : 2004 Company Dixon Technologies (India) Ltd. (Formerly Known as Dixon Technologies (India) Pvt. Ltd ) CIN : L32101UP1993PLC066581 Regd. Office: B-14 & 15, Phase-II, Noida-201305, (U.P.) India,Ph.: 0120-4737200 E-mail : [email protected]. Website : http://www.dixoninfo.com, Fax : 0120-4737263 5th July, 2018 To To Secretary �cretary Listing Department sting Department BSE Limited 'v National Stock Exchange of India Limited Department of Corporate Services Exchange Plaza, Bandra Kurla Complex Phiroze Jeejeebhoy Towers, Mumbai - 400 050 Dalal Street, Mumbai - 400 001 Scrip Code - 540699 Scrip Code- DIXON !SIN: INE935N01012 !SIN: INE935N01012 Subject: Appointment of President - Chief Operating Officer (COO) of the Company Dear Sir/Ma'am, We wish to inform you that Mr. Abhijit Kotnis has joined the Company as President - Chief Operating Officer (COO) of the Company. A detailed announcement in this respect is enclosed herewith. We request you to kindly take the same on record and oblige. Thanking you, Encl: as above Dixon Technologies appoints Mr. Abhijit Kotnis as President -Chief Operating Officer (COO) of the Company 5th July, Noida: Dixon Technologies (India) Limited (“Company”) has appointed Mr. Abhijit Kotnis as President- COO who shall be spearheading the Company’s LED Television division & New Projects. Mr. Kotnis has over 28 years of rich and extensive experience across Manufacturing, Technology Business Development and sourcing fields. His knowledge and expertise is proven in the areas of Strategic Planning & Executions, New Business Development, Supply Chain Management, Business transformations etc . Mr. Kotnis holds an MBA in Marketing & Operations & B.E. in Electronics & Telecommunications from Marathawada University, Aurangabad and has also completed his Post Graduate Programme in Management (MEP) from IIM, Ahmedabad. -

Advanced Management Program (AMP)

Advanced Management Program (AMP) 24th Edition, 2019 4 Weeks August 19 – September 15, 2019 Overseas Learning Programme in Partnership with ESCP-Europe, European School of Management, Paris, France Vienna University of Eco. & Business Administration, Austria Frankfurt School of Finance & Management, Frankfurt, Germany RSM Erasmus University, Rotterdam, Netherlands University of Antwerp, Antwerp, Belgium Advanced Management Program (AMP) 24th Edition, 2019 STRATEGIC LEADERSHIP TRANSFORMATION IN THE DIGITAL AGE With the advent of digital technology, the concept of doing business has completely transformed. The agile, dynamic and hyper-linked work environment requires organizations to redefine the competencies of an effective leader in the digital era. Everyday communication is rapidly changing to virtual domains, based on continuously evolving social media platforms like Linkedin, twitter, instagram, pinterest and so on. Organizations have started realizing that the increased uses of internet applications, and social media has made today’s employees and customer more aware than ever. The traditional market place has taken a shape of digital platforms. Suppliers and customers meet directly, and the middle layers are disappearing. Manufacturing organizations earn a large part of their revenue from services. Therefore, focus on cost and process control is becoming as important as sales. The entire supply chain including suppliers and customers are becoming global. In order to understand the cross cultural issues and the best practices across the globe, global benchmarking is becoming essential. Rapid changing business environment has increased the pressure on the key performance measures of an organization. An organization cannot merely remain competitive only in one of the few dimensions of business performances such as cost, quality, service, agility, or speed. -

Press Release REC Limited

Press Release REC Limited March 30, 2021 Ratings Amount Facilities/Instruments Rating1 Rating Action (Rs. crore) Long term Market Borrowing CARE AAA; Stable 1,00,000.00 Assigned Programme for FY22 (Triple A; Outlook: Stable) 1,00,000.00 Total Long Term Instruments (Rs. One Lakhs Crore Only) CARE A1+ Commercial Paper issue for FY22 5,000.00 Assigned (A One Plus) Short term Market Borrowing CARE A1+ 5,000.00 Assigned Programme for FY22 (A One Plus) 10,000.00 Total Short Term Instruments (Rs. Ten Thousand Crore Only) Details of instruments/facilities in Annexure-1 Detailed Rationale & Key Rating Drivers The rating assigned to the market borrowing programme of REC Limited continues to factor in REC’s parentage as well as its strategic importance to Government of India (GoI) in the development of power sector in India. The rating factors in REC’s parentage as well as its strategic importance to Government of India (GoI) in the development of power sector in India. The rating also draws comfort from REC’s quasi-sovereign status that allows it to have a diversified resource profile, adequate profitability and comfortable capitalization levels. However the rating factors in risks associated with weakness in REC’s asset quality in exposure to private sector, high exposure to weak state power utilities and high sector-wise as well as borrower concentration risk. With respect to the acquisition of Government of India’s (GoI) existing 52.63% equity shareholding in REC Limited by Power Finance Corporation Limited (PFC; rated CARE AAA; Stable/ CARE A1+), the acquisition transaction was completed on March 28, 2019. -

Dixon Technologies (India) Limited Corporate Presentation

Dixon Technologies (India) Limited Corporate Presentation October 2017 Company Overview Dixon Technologies (India) Limited Corporate Presentation 2 Dixon Overview – Largest Home Grown Design-Focused Products & Solutions Company Business overview Engaged in manufacturing of products in the consumer durables, lighting and mobile phones markets in India. Company also provide solutions in reverse logistics i.e. repair and refurbishment services of set top boxes, mobile phones and LED TV panels Fully integrated end-to-end product and solution suite to original equipment manufacturers (“OEMs”) ranging from global sourcing, manufacturing, quality testing and packaging to logistics Diversified product portfolio: LED TVs, washing machine, lighting products (LED bulbs &tubelights, downlighters and CFL bulbs) and mobile phones Leading Market position1: Leading manufacturer of FPD TVs (50.4%), washing machines (42.6%) and CFL and LED lights (38.9%) Founders: 20+ years of experience; Mr Sunil Vachani has been awarded “Man of Electronics” by CEAMA in 2015 Manufacturing Facilities: 6 state-of-the-art manufacturing units in Noida and Dehradun; accredited with quality and environmental management systems certificates Backward integration & global sourcing: In-house capabilities for panel assembly, PCB assembly, wound components, sheet metal and plastic moulding R&D capabilities: Leading original design manufacturer (“ODM”) of lighting products, LED TVs and semi-automatic washing machines Financial Snapshot: Revenue, EBITDA and PAT has grown at -

“Dixon Technologies India Limited 4QFY2020 Earnings Conference Call”

“Dixon Technologies India Limited 4QFY2020 Earnings Conference Call” June 11, 2020 ANALYST: MR. DHRUV JAIN – AMBIT CAPITAL MANAGEMENT: MR. ATUL B LALL – CHIEF EXECUTIVE OFFICER – DIXON TECHNOLOGIES LIMITED MR. SAURABH GUPTA – CHIEF FINANCIAL OFFICER – DIXON TECHNOLOGIES LIMITED Page 1 of 20 Dixon Technologies India Limited June 11 2020 Moderator: Ladies and gentlemen, good day and welcome to the Dixon Technologies India Limited 4QFY2020 Earnings Conference Call hosted by Ambit Capital. As a reminder, all participant lines will be in the listen-only mode and there will be an opportunity for you to ask questions after the presentation concludes. Should you need assistance during the conference call, please signal an operator by pressing “*” then “0” on your touchtone phone. Please note that this conference is being recorded. I would now like to hand the conference over to Mr. Dhruv Jain from Ambit Capital. Thank you and over to you Sir! Dhruv Jain: Thank you. Welcome to the 4QFY2020 Earnings call of Dixon Technologies. From the management, we have with us Mr. Atul Lall, CEO and Mr. Saurabh Gupta, CFO. Over to you Sir for your opening comments! Atul B. Lall: Thank you Dhruv. This is Atul Lall and we also have with us Saurabh Gupta, CFO. Good afternoon ladies and gentlemen, thanks for joining this call. Before I touch upon our 4QFY2020 results, I would like to update you on how we have fared during the lockdown and the latest update on the post relaxation. So we resumed our operations in all our factories in all the nine factories between May 4, 2020 and May 18, 2020. -

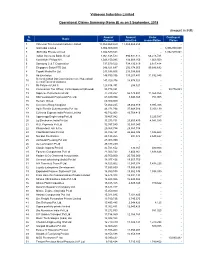

Videocon Industries Limited Operational Claims Summary (Form

Videocon Industries Limited Operational Claims Summary (Form B) as on 3 September, 2018 (Amount in INR) S. Amount Amount Under Contingent Name No. Claimed Admitted reconciliation Claims 1 Videocon Telecommunications Limited 17,869,469,659 17,869,469,659 - - 2 Gail India Limited 3,906,000,000 - - 3,906,000,000 3 IBM India Private Limited 1,352,539,824 - - 1,352,539,824 4 Indian Overseas Bank, Seoul 1,061,148,533 994,931,813 66,216,721 - 5 Koninklijke Philips N.V. 1,043,150,095 134,003,250 1,563,509 - 6 Samsung C & T Corporation 737,679,522 734,130,819 2,617,414 - 7 Singapore Satori PTE Ltd. 346,821,647 256,174,955 90,646,692 - 8 Topaki Media Pvt Ltd 233,598,606 233,598,606 - - 9 Ab Electrolux 148,790,336 137,257,491 11,532,845 - Secunderabad Gst Commissionerate Hyderabad 10 141,829,376 18,874,523 - - Central Tax And Customs 11 Rs Polymers Unit Ii 128,814,341 294,521 - - 12 Commercial Tax Officer, Circle Spaecial1,Bhiwadi 93,775,891 - - 93,775,891 13 Supreme Petrochemical Ltd 77,748,257 66,179,401 11,568,856 - 14 Shri Venkatesh Polymould Pvt. Ltd. 63,880,934 3,940,369 751,905 - 15 Hemant Group 60,300,000 - - - 16 Covestro (Hong Kong)Ltd 53,462,245 49,466,919 3,995,326 - 17 Agile Electric Sub Assembly Pvt Ltd 46,271,794 37,948,586 5,203,139 - 18 Cj Korea Express India Private Limited 42,782,958 16,768,416 - - 19 Approcopp Engineering Pvt Ltd 39,467,942 - 3,225,587 - 20 Lg Electronics India Pvt Ltd 33,273,731 23,653,430 4,541,580 - 21 R.G. -

Dixon Technologies (India) (DIXTEC)

March 29, 2021 S__tock___ TALES Stock Tales are concise, holistic stock reports across wider spectrum of sectors. Updates will not be periodical but based on significant events or change in price. Dixon Technologies (India) (DIXTEC) CMP: | 3624 Target: | 4270 (18%) Target Period: 15 months BUY March 29, 2021 Rising star in domestic manufacturing space... Dixon Technologies (DTL) is India’s leading electronic manufacturing service Stock Data (EMS) provider to various multinational/domestic companies in India. The company is one of the biggest beneficiaries of the government’s production Particular Amount linked incentive (PLI) scheme for mobile phones and other electronic Market Cap (| Crore) 21,222.1 products. We believe PLI benefits will start flowing in from Q4FY21E Total Debt (FY20) (| Crore) 82.8 onwards while in future DTL’s mobile revenue will grow multi-fold (~14x Cash & Inv (FY20) (| Crore) 100.1 jump) over FY20-23E. DTL has also applied for PLI in the lighting, electronic EV (| Crore) 21,204.8 wearables and other electronic products (laptop/notebooks). This opens up 52 week H/L 4588/ 624 a significant growth opportunity for DTL, going forward (we see 4x jump in Equity capital (| Crore) 11.6 Stock Tales Face value (|) 2.0 revenue FY20-23E). Further, prudent working capital management and Price Performance future expansion through internal accruals will keep balance sheet light and `f return ratios elevated (RoE: 39%, RoCE: 44%) for DTL, going forward. 5000 20000 Strong play in emergent domestic EMS industry 4000 15000 3000 10000 The Indian electronic manufacturing services (EMS) industry is likely to grow 2000 at a CAGR of 45% over the next five years to become a ~US$152 billion (bn) 1000 5000 industry. -

Companhia De Saneamento De Minas Gerais GAIL (India) Limited

Vote Summary Report Date range covered: 07/01/2020 to 06/30/2021 Location(s): All Locations Institution Account(s): NBI Diversified Emerging Markets Equity Dino Polska SA Meeting Date: 07/02/2020 Country: Poland Primary Security ID: X188AF102 Record Date: 06/16/2020 Meeting Type: Annual Ticker: DNP Shares Voted: 12,894 Proposal Voting Vote Number Proposal Text Proponent Mgmt Rec Policy Rec Instruction Management Proposals Mgmt 1 Open Meeting Mgmt 2 Elect Meeting Chairman Mgmt For For For 3 Acknowledge Proper Convening of Meeting Mgmt 4 Approve Agenda of Meeting Mgmt For For For 5 Receive Management Board Report on Mgmt Company's and Group's Operations, Financial Statements, and Management Board Proposal on Allocation of Income and Dividends 6 Receive Supervisory Board Reports on Board's Mgmt Work, Management Board Report on Company's and Group's Operations, Financial Statements, and Management Board Proposal on Allocation of Income and Dividends 7 Receive Supervisory Board Requests on Mgmt Approval of Management Board Report on Company's and Group's Operations, Financial Statements, Management Board Proposal on Allocation of Income and Dividends, and Discharge of Management Board Members 8.1 Approve Management Board Report on Mgmt For For For Company's Operations 8.2 Approve Financial Statements Mgmt For For For 9 Approve Allocation of Income and Omission of Mgmt For For For Dividends 10.1 Approve Management Board Report on Group's Mgmt For For For Operations 10.2 Approve Consolidated Financial Statements Mgmt For For For 11.1 Approve -

Revision in Market Lot of Derivative Contracts on Individual Stocks

Department : FUTURES & OPTIONS Download Ref No: NSE/FAOP/45895 Date : September 30, 2020 Circular Ref. No: 87/2020 All Members, Revision in Market Lot of Derivative Contracts on Individual Stocks In pursuance of SEBI guidelines for periodic revision of lot sizes for derivatives contracts specified in the SEBI circular CIR/MRD/DP/14/2015 dated July 13, 2015, the market lots of derivatives contracts shall be revised as follows: Sr. Underlying whose Derivative Count of Annexure No Effective date contract size shall be Underlying Number October 30, 2020 (for Nov 1 Revised Downwards 15 1 2020 & later expiries) 2 Revised Upwards 12 October 30, 2020 (for Jan 2 2021 & later expiries) 3 Unchanged 108 - 3 Revised Downwards but new October 30, 2020 (for Jan 4 lot size is not a multiple of old 1 4 2021 & later expiries) lot size To avoid operational complexities, in case of Annexure 2 and 4 above, following will be applicable: 1. Only the far month contract i.e. January 2021 expiry contracts will be revised for market lots. Contracts with maturity of November 2020 and December 2020 would continue to have the existing market lots. All subsequent contracts (i.e. January 2021 expiry and beyond) will have revised market lots. 2. The day spread order book will not be available for the combination contract of Dec 2020 – Jan 2021 expiry. For the purpose of the computation, the average of the closing price of the underlying has been taken for one month period of September 1st – September 30th 2020. This circular shall come into effect from October 30, 2020. -

Earnings Presentation Q3 & 9M,Fy 19-20

R I S E Research Innovation Scale Excellence EARNINGS PRESENTATION Q3 & 9M,FY 19 - 20 Disclaimer Certain statements in this communication may be ‘forward looking statements’ within the meaning of applicable laws and regulations. These forward-looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the forward-looking statements. Important developments that could affect the Company’s operations include changes in the industry structure, significant changes in political and economic environment in India and overseas, tax laws, import duties, competition, inflationary pressures, litigation and labour relations. Dixon Technologies (India) Limited and its subsidiaries and joint ventures will not be in any way responsible for any action taken based on such statements and undertakes no obligation to publicly update these forward-looking statements to reflect subsequent events or circumstances. 2 Table of contents Latest Business Updates 04 Highlights of Q3 & 9M,FY 19-20 05 Consolidated Results Summary 06 Segment Wise Performance 7-8 ODM Revenue Share & Segment wise ROCE 09 Expenditure Analysis 10 Balance Sheet 11 Cash Flow 12 Key Financial Ratios 13 3 Latest Business Updates Commenced production of Home appliances for Voltas Beko Commenced Production of Samsung Feature Phone from 1st Nov 2019 To commence production of LED TV’s for Samsung from Feb 2020 Commenced production of entire range of Lighting products for HPL Electric & Power Got order -

Executive Director in REC Limited, New Delhi.PDF

awl* f9fi*t. I REC Limited (Formerly Rural Electrification Corporation Limited) (TI-Va 1-1-tebi-1 Th-t 's e) / (A Government of India Enterprise) REC Regd. Office: Core•4, SCOPE Complex, 7, Lodhi Road, New Delhi 110 003 t:trilft-tx Endless enemy. Infinite possibilities. Tel: +91-11-4309 1500 I Fax: +91-11-2436 0644 I Website: www.recindia.com CIN : L4010101.1969001005095 l GST No.: 07AAACR4512R123 No.CMD/SM/REC/2021/22 To, The Chief Secretaries of all States Sir, Subject: Filling up of the post of Executive Director in REC Limited, New Delhi on deputation - reg. REC Limited, a Navaratna CPSE under the administrative control of the Ministry of Power, Government of India, is the nodal agency for implementation of several programs of the Government of India such as the Rajiv Gandhi Gramin Vidyut Yojana (RGGVY), Saubhagya (Pradhanmantri Sahaj Bijli Har Ghar Yojana), DDUGJY (Deendayal Upadhyaya Gram Jyoti Yojana), UDAY (Ujwal Discom Assurance Yojana) among many others. The Company is also poised to be a Nodal Agency for the proposed 'Revamped Distribution Scheme' targeted at improving the performance of the Discoms in the country. 2. To execute these programs, we have two posts of Executive Directors to be tilled by senior officers from the government on deputation. One IAS officer of Director rank is already working as Executive Director on deputation in the Company. We intend to fill the other vacant post of Executive Director on deputation basis. This is to request you to kindly forward names of suitable IAS officers at Deputy Secretary/Director rank for the post by 05th March, 2021.