Officestatus Summer // 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Savills Studley Report Boston Office Sector Q1 2018

Savills Studley Research Boston Savills Studley Report Boston office sector Q1 2018 SUMMARY Market Highlights LEASING DECLINES RENT RISES "Boston's economy and office market has taken Following a strong fourth quarter of activity, The average asking rent for the entire region a different route in this cycle, deviating from with 4.0 million square feet (msf) leased – increased by 0.7% to $32.38. The Class quarterly activity inched down to 2.6 msf. A asking rent was essentially flat, inching the weak population and job growth displayed Tenants have leased 11.6 msf in the four down by 0.4% to $40.33. in many older Northeast and Midwest metros most recent quarters, 29.5% below the - and locally during prior cycles. This time has long-term market average of 16.4 msf. SALES DOWN SHARPLY truly been different for Boston. The willingness As of March 2018, office sales volume in AVAILABILITY RATES PUSH LOWER Boston totaled $1.9 billion in the last six of many companies to pay top dollar for months, down sharply compared to the $4.9 Boston's expertise in a wide variety of high-tech The market's overall availability rate billion sold in the previous six months. decreased by 50 basis points from 12.7% sectors has been a game-changer." to 12.2%. The Class A availability rate fell by 60 basis points to 13.2%. Steve Woodworth, Managing Director Savills Studley Report | Boston Recovery Covers a Lot of Office-Using Employment Trends Ground, Region a FrontRunner for HQ2 Millions 0.60 5% The duration, magnitude and scope of 0.58 Boston’s expansion in this cycle has been 3% impressive. -

Boston Office Market Report

BOSTON OFFICE MARKET REPORT SECOND QUARTER 2018 NO SIGNS OF SUMMER SLOWDOWN Greater Boston's market showed no signs of weakening during the second quarter by recording strong growth from numerous industry types. The market continued receiving inbound demand as well as converting organic growth into significant expansion. Most notably, Amazon's commitment to nearly 430,000 square feet at Parcel L4 in the Seaport reflects inbound demand while Wayfair's torrid expansion into roughly 395,000 SF in the Back Bay at 222 Berkeley and 500 Boylston Street exemplifies organic growth. The region's demographics and economy have remained solid which has supported and promoted Boston's recent expansion. Firmly rooted in education, technology and life sciences, Boston's diverse economic base has submitted strong job growth through increased recruitment and skilled labor retention from the area’s leading universities and institutions. Looking forward, expect durable market conditions and a diversified economy to guide the region's commercial real estate market to a strong performance over the next several years. 3.5% 3.8% # $2.6B 2ND MAY MAY MA QUARTERLY NATIONALLY IN MASSACHUSETTS NATIONAL VC FUNDING (Q1) QUARTERLY (Q1) UNEMPLOYMENT UNEMPLOYMENT VC FUNDING CLASS A MARKET ASKING RATE VS. DIRECT VACANCY TRENDS $64.00 16.0% $61.00 14.0% $58.00 12.0% GLOBAL DESTINATION $55.00 10.0% World leader in medical innovation and $52.00 8.0% technological advancement $49.00 6.0% TOWER SALES RIPPLE $46.00 4.0% EFFECT Will recent Class A Tower sales push $43.00 2.0% rental rates even higher? $40.00 0.0% 201720162015201420132012201120102009200820072006 YTD2018 TECHNOLOGY & Average Asking Rate Direct Vacancy (%) INNOVATION HUB Fortune 500 leaders and 1,900 homegrown startups CLASS B BUILD TO SUIT AND ASKING RATE VS. -

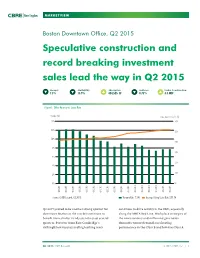

Speculative Construction and Record Breaking Investment Sales Lead the Way in Q2 2015

MARKETVIEW Boston Downtown Office, Q2 2015 Speculative construction and record breaking investment sales lead the way in Q2 2015 Vacancy Availability Absorption Sublease Under Construction 7.5% 13.9% 424,525 SF 0.75% 3.3 MSF Figure 1: Office Vacancy vs. Lease Rate Vacancy (%) Lease Rate Per Sq. Ft. ($) 14% $60 12% $50 10% $40 8% $30 6% $20 4% $10 2% 0% $0 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Source: CBRE Research, Q2 2015. Vacancy Rate 7.5% Average Asking Lease Rate $51.54 Q2 2015 proved to be another strong quarter for continues to drive activity in the CBD, especially downtown Boston as the market$60 continues to along the MBTA Red Line. Workplace strategies of benefit from similar trends seen the past several the new economy and millennial generation quarters. Pressure from East$50 Cambridge’s dominate tenant demand, accelerating strikingly low vacancy and high asking rents performance in the Class B and low-rise Class A $40 $30 Q2 2015 CBRE Research © 2015 CBRE, Inc. | 1 $20 $10 $0 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Sq. Ft. (000’s) 2,000 1,500 1,000 500 0 (5,000) (1,000) Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 MARKETVIEW BOSTON DOWNTOWN OFFICE markets. The investment sales market is red hot, contraction for the overall Boston market, the with record-breaking sales seen in all submarkets. -

Boston Market Viewpoint

Research & Forecast Report GREATER BOSTON MARKET VIEWPOINT Q4 2015 Boston Overview Large Requirements The downtown Boston office market was running on all cylinders in TENANT SF INDUSTRY 2015, posting over two million square feet of positive absorption Putnam Investments 250,000 Financial Services and an unprecedented seven million square feet for the five- Eze Castle 125,000 Technology year period 2011 to 2015. The Financial District was by far the Advent International 100,000 Financial Services largest contributor to the positive results in 2015. Occupancy in this core submarket increased by over 1.3 million square feet WeWork 90,000 Business Services with the majority (920,000 SF) recorded in the low-rise segment Rue LaLa 75,000 Retail of the Class A tower market. Nearly 400,000 square feet of Boston Globe 75,000 Media/Publishing positive absorption was recorded in the Seaport, largely due to the construction completion of 101 Seaport Square, a 420,000-square- Velocity foot office building anchored by PwC. > Velocity (signed lease activity) was healthy over the course of 2015, with approximately 4.6 million square feet of leases signed. Statistics in the core submarkets are as follows: > The largest transaction in 2015 was BNY Mellon’s Boston Market Statistics 250,000-square-foot renewal at One Boston Place. Although this represented a contraction of approximately 100,000 square 2015 MARKET SEGMENT SUPPLY (SF) VACANCY RATE* ABSORPTION feet for the financial services firm, market-wide tenants in Financial District – Class A 27,762,321 9.1% 1,192,196 growth mode far outnumbered those reducing their space requirements. -

TRENDS in the Real Estate Market

TRENDS IN the real estate market 2016 WELCOMING REMARKS Tom Hynes, Co-Chairman KEYNOTE ADDRESS Charlie Baker Governor of Massachusetts PLACEMAKING from concept to reality THE BOSTON MARKET Ron Perry, President 1.75M Rendering by Neoscape 3rd Tallest Building High End Rents Topping $80/RSF H “General Electric to select Boston as new global headquarters”. E “Boston’s biggest office sale this year just closed – for $1.3 billion [500 A Boylston & 222 Berkeley Street]”. D L “It’s official: Putnam Investments making big move to 100 Federal St. ” I “Boston Globe will move HQ to downtown office N [53 State Street]”. E “As Pier 4 develops, Tishman Speyer makes another South Boston S play [One Channel Center - $316.5M]”. K E Y S T vacancy net absorption A T 8.9% 2.1M RSF S K E Y rental rates S T $48-$80 $38-$52 $65-$85 A T S T Back Bay Financial District O W E R Vacancy 5.9% 20th Floor 5.6% S T 6.6% 3.1% U D Y V 5M RSF 30% E L O 250K RSF 250K RSF 250K RSF 200K RSF 175K RSF C One Boston Place 100 Federal Street Landmark Center 125 High Street Schrafft Center I T Y 85K RSF 150K RSF 125K RSF 120K RSF 110K RSF Innovation & Design 125 High Street 1325 Boylston Street 333 Summer Street Landmark Center Building T E N 4M RSF 7 options > 100K RSF A N T S 600K RSF 250K RSF 200K RSF 125K RSF 100K RSF I N M A R K 100K RSF 90K RSF 75K RSF 75K RSF 65K RSF E T =Committed Tenants suburban M 1M RSF I G R destination: boston A T suburban I O N N E W recently completed [office] D E 680K RSF V E L O P M E N 101 Seaport Boulevard 1325 Boylston Street T Skanska Samuels -

Esposito V. American Renal Associates Holdings, Inc., Et Al. 16-CV-11797-U.S. District Court Civil Docket

US District Court Civil Docket as of June 15, 2018 Retrieved from the court on June 15, 2018 United States District Court District of Massachusetts (Boston) CIVIL DOCKET FOR CASE #: 1:16-cv-11797-ADB Esposito v. American Renal Associates Holdings, Inc. et al Date Filed: 09/02/2016 Assigned to: Judge Allison D. Burroughs Date Terminated: 06/15/2018 related Case: 1:17-cv-12091-ADB Jury Demand: Plaintiff Cause: 15:78m(a) Securities Exchange Act Nature of Suit: 850 Securities/Commodities Jurisdiction: Federal Question Plaintiff Mary Esposito represented by Mark A. Delaney individually and on behalf of all other Berman DeValerio persons similarly situated One Liberty Square 8th Floor Boston, MA 02109 617-542-8300 Email: [email protected] ATTORNEY TO BE NOTICED V. Defendant American Renal Associates Holdings, represented by Antonia M. Apps Inc. Milbank Tweed Hadley & McCloy LLP 28 Liberty Street New York, NY 10005-1413 212-530-5357 Fax: 212-822-5357 Email: [email protected] LEAD ATTORNEY PRO HAC VICE ATTORNEY TO BE NOTICED Elise Kent Bernanke Milbank Tweed Hadley & McCloy LLP 28 Liberty Street New York, NY 10005-1413 212-530-5239 Fax: 212-822-5239 Email: [email protected] LEAD ATTORNEY PRO HAC VICE ATTORNEY TO BE NOTICED Gary R. Greenberg Greenberg Traurig, LLP One International Place 20th Floor Boston, MA 02110 617-310-6013 Fax: 617-310-6001 Email: [email protected] LEAD ATTORNEY ATTORNEY TO BE NOTICED Jed M. Schwartz Milbank Tweed Hadley McCloy LLP 24 Liberty Street New York, NY 10005-1413 212-530-5283 Fax: 212-822-5283 Email: [email protected] LEAD ATTORNEY PRO HAC VICE ATTORNEY TO BE NOTICED Katherine R. -

100Largest Law Firms in Massachusetts

100LARGEST LAW FIRMS IN MASSACHUSETTS 2020 THE BBA THANKS 135+ SPONSORS Supporting excellence in the profession, access to justice, diversity & inclusion, and service to the Boston community. LAW FIRMS GOVERNMENT 30+ Years of Sponsorship: Boston Planning & Development Agency | Committee Brown Rudnick LLP | Choate | Foley Hoag LLP | Goodwin | for Public Counsel Services | Massachusetts Commission Goulston & Storrs | Locke Lord LLP | Mintz | Ropes & Gray | Against Discrimination (MCAD) | Massachusetts WilmerHale Department of Energy Resources | Massachusetts Department of Environmental Protection | Office of Labor 20+ Years of Sponsorship: Relations of the City of Boston | Office of the Corporation Burns & Levinson | Conn Kavanaugh | Day Pitney | Donnelly, Counsel of the City of Boston | Office of the Massachusetts Conroy & Gelhaar, LLP | Hemenway & Barnes LLP | Hogan Attorney General | Suffolk County District Attorney’s Lovells | Murphy & King | Nixon Peabody | Nutter | Peabody & Office Arnold | Rackemann, Sawyer & Brewster | Robinson & Cole | Sherin and Lodgen | Sugarman Rogers | Sullivan | Todd & Weld LLP | Yurko, Salvesen & Remz, P.C. IN-HOUSE LEGAL DEPARTMENTS Blue Cross Blue Shield of Massachusetts | Coverys | Dell 10+ Years of Sponsorship: EMC | LPL Financial | Partners HealthCare | Spartan Race, Anderson & Kreiger | Casner & Edwards | Dain Torpy | Davis Inc. | State Street Corporation | UMASS Boston Office of Malm | DLA Piper | Duane Morris | Gesmer Updegrove General Counsel LLP | Greenberg Traurig | Hinckley Allen | Hirsch Roberts Weinstein | Holland & Knight | Morgan, Brown & Joy, LLP | Ogletree Deakins | Robins Kaplan LLP | Rose Law Partners LAW SCHOOLS Boston College Law School | Boston University School of LLP | Ruberto, Israel & Weiner | Skadden, Arps, Slate, Law | New England Law | Boston | Northeastern University Meagher & Flom LLP | SUGARMAN | Sunstein Kann Murphy & Timbers LLP | Verrill | Weil School of Law | Suffolk University Law School 5+ Years of Sponsorship: NON-PROFITS Arent Fox | Arrowood LLP | Atwood & Cherny, P.C. -

Weekly Digest 1.09.09

A B C D E F G Application Industry Employer Website Job/Internship Location Corporate Office Address Notes 1 Deadline 2 Advertising 24/7 Real Media http://www.24-7media.de/ NYC N/A 132 W. 31st Street, Floor 9, New York, NY 10001 N/A 360i produces integrated digital marketing campaigns for large brand advertisers with a foundation in Advertising 360i 3 http://www.360i.com/ NYC N/A 28 West 23rd St, 6th Floor, New York, NY 10010 search marketing. Each year, one student who shows promise and a desire to gain experience in the media aspect of advertising will be selected to complete a 10-week summer internship at Adweekmagazine's Advertising American Advertising Federation headquarters in New York. The intern will work in the marketing department and will be exposed to various projects that support advertising sales. The intern will be provided with a $4,500 stipend to 4 http://www.aaf.org/default.asp?id=148 DC 6-Feb 1101 Vermont Avenue NW, Suite 500, Washington DC 20005 cover transportation costs, food, lodging and other living expenses during the 10-week internship. The Ad Council of Rochester is a thriving, highly regarded, community-service organization that advocates for necessity of strategic marketing and communications to advance the work of social Advertising Ad Council of Rochester service and cultural organizations; creates innovative and strategic marketing and communications programs that improve the vitality of our community and partners with businesses, volunteers and 5 http://www.adcouncilroch.org/default.asp Rochester N/A 274 N. Goodman St., Suite B269, Rochester, NY 14607 nonprofits to achieve positive community impact. -

FEI Partner Program Financial Executives International (FEI) Is the Preeminent Professional Association of Financial Executives

FEI Partner Program Financial Executives International (FEI) is the preeminent professional association of financial executives. The Boston Chapter is one of the largest chapters with 600 members representing more than 500 organizations in Greater Boston and throughout New England. Who Are FEI Boston Members? Their Titles: Chief Financial Officer Vice President of Finance Audit Committee member Vice President of Chief Accounting Officer Senior Manager Planning and Analysis Vice President of Comptroller/Controller Vice President of Taxes Risk Management Vice President of Pension Director of Finance, Taxes, Treasurer Fund Investments Treasury or Accounting Their Companies: ▪ $2 million in net worth or $6 million in capital (combined net worth and long-term debt) or $10 million or more in annual revenues. ▪ $8 million in operating expenses ▪ $200 million in total assets (Financial Institutions) ▪ $40 million total assets (Government corporations /authorities) Their Connections: ▪ They come from all industries ▪ Our members are THE Financial leaders of Boston ▪ They have nationwide connections with 10,000 of their finance peers ▪ They have access to the C Suite in their companies FEI Boston Partners make BIG Things Happen. Be a Part of the Change We Make. KEY BENEFITS OF PARTNERSHIP FEI is truly vested in its partnerships being successful! Thanks to • On a rotating basis, chapter our partners' financial support and specialized expertise, we sponsors are profiled at our provide the highest quality programs and speakers, outstanding monthly Executive Events content for our professional development seminars, academic scholarships to the best and brightest, and assist our fellow • Partners are provided one members who are seeking their next opportunity. -

Largest Law Firms in Massachusetts 2021

1002021 LARGEST LAW FIRMS IN MASSACHUSETTS THE BBA THANKS 135+ SPONSORS Supporting excellence in the profession, access to justice, diversity & inclusion, and service to the Boston community. LAW FIRMS GOVERNMENT 30+ Years of Sponsorship: Boston Planning & Development Agency | Committee for Brown Rudnick LLP | Choate | Foley Hoag LLP | Goodwin | Public Counsel Services | Massachusetts Commission Goulston & Storrs | Locke Lord LLP | Mintz | Ropes & Gray Against Discrimination (MCAD) | Massachusetts | WilmerHale Department of Energy Resources | Massachusetts 20+ Years of Sponsorship: Department of Environmental Protection | Office of Labor Burns & Levinson | Conn Kavanaugh | Day Pitney | Relations of the City of Boston | Office of the Corporation Donnelly, Conroy & Gelhaar, LLP | Hemenway & Barnes Counsel of the City of Boston | Office of the Massachusetts LLP | Hogan Lovells | Murphy & King | Nixon Peabody | Attorney General | Suffolk County District Attorney’s Nutter | Peabody & Arnold | Rackemann, Sawyer & Office Brewster | Robinson & Cole | Sherin and Lodgen | Sugarman Rogers | Sullivan | Todd & Weld LLP | Yurko, IN-HOUSE LEGAL DEPARTMENTS Salvesen & Remz, P.C. Blue Cross Blue Shield of Massachusetts | Coverys | Dell EMC | LPL Financial | Mass General Brigham | State Street 10+ Years of Sponsorship: Corporation | UMASS Boston Office of General Counsel Anderson & Kreiger | Casner & Edwards | Dain Torpy | Davis Malm | DLA Piper | Duane Morris | Gesmer Updegrove LLP | Greenberg Traurig | Hinckley Allen | LAW SCHOOLS Boston College Law School -

Directory Of

LAWYERS WEEKLY LAWYERS DIRECTORY OF NEW ENGLAND 2014 - 2015 IN-HOUSE COUNSEL DIRECTORY OF NEW ENGLAND IN-HOUSE COUNSEL 2014-2015 DIRECTORY Martin M. Fantozzi business Litigation Partner BOSTON NEW YORK WASHINGTON, DC BEIJING goulstonstorrs.com Courtroom tested. Martin Fantozzi knows business. From the boardroom Client committed. to the courtroom, clients appreciate the practical, Case closed. solutions-oriented approach he delivers. Whether representing corporations, medical and educational facilities, LLCs or shareholders, Marty’s ability to distill what’s important is widely recognized. Marty cuts to the chase, and so can you with Goulston & Storrs. serious 1914 2014 Legal. Brief. A relationship so intuitive you’llyou’ll thitthinknk wewe’re’re rereadinga your mind. Corporate Social Responsibility and the Law Massachusetts Noncompete Law csrandthelaw.com massachusettsnoncompetelaw.com Energy & Cleantech Counsel Policyholder Counsel Blog energycleantechcounsel.com policyholdercounsel.com Infrastructure & Construction Law Security, Privacy and the Law infrastructureandconstructionlaw.com securityprivacyandthelaw.com Law & the Environment Trademark and Copyright Law At Bowditch & Dewey, our attorneys don’t use magic to solve lawandenvironment.com trademarkandcopyrightlawblog.com legal matters. They become a valuable member of your team. Some clients think of us a specialized boutique and other clients turn to us as a full-service solution. Either way, we take Foley Hoag blogs. Just a click away. the time to understand what the client wants to achieve and we work hard to make that happen. It’s no illusion. Ideas. Exchanged. Our blogs break down legal developments to inform, report on trends and initiate dialogue. Join the discussion. www.foleyhoag.com Attorney advertising. Prior results do not guarantee a similar outcome. -

Directory of Massachusetts

Directory of Massachusetts LOBBYISTS 2017 617.646.1000 - www.oneillandassoc.com BOSTON - WASHINGTON DC LEGISLATIVE & REGULATORY ADVOCACY STRATEGIC COMMUNICATIONS GOVERNMENT CONTRACTING & PROCUREMENT COALITION & ASSOCIATION MANAGEMENT committed to the ethical pursuit of our clients’ objectives through informed consultations and strategic planning 617.574.3399 | 12 Post Office Sq., 6th Floor | Boston, Massachusetts 02109 www.lynchassociates.com Craig S. Altemose Leda Ann Anderson Anthony L. Archinski A Better Future Project Planned Parenthood Advocacy New England Police Benevolent 30 Bow Street Fund of Massachusetts Association, Inc. Cambridge, MA 02138 66 Queensberry Street, Apt. 120 7 Technology Drive, Suite 102 Gerald Abban (617) 945-5242 Boston, MA 02215 Chelmsford, MA 01863 Fidelity Brokerage Services, LLC (315) 382-6388 (978) 453-2500 245 Summer Street, Mail Zone V6a Jason A. Aluia Boston, MA 02109 Massachusetts Association Lisa Marie Andoscia Derek L. Armstrong (617) 563-0617 of Health Plans Rosewood Consulting LLC Bank of America, N.A. 40 Court Street, 5th Floor 3 Peach Street 100 Federal Street, MA5-100-09-12 Anthony A. Abdelahad Boston, MA 02108 Wilbraham, MA 01095 Boston, MA 02110 Ventry Associates LLP (617) 338-2244 (413) 575-3400 (617) 464-8613 1 Walnut Street, 4th Floor Boston, MA 02108 Joseph D. Alviani Kevin Andrews George Atanasov (617) 423-0028 Partners HealthCare System, Inc. Massachusetts Charter Public AbbVie Inc. 800 Boylston Street, Suite 1150 School Association 1 North Waukegan Road Allison Alaimo Boston, MA 02199 43 Broad Street, Suite C-401 Department V391, Bldg. ABV1-2 Veterans Inc. (617) 278-1041 Hudson, MA 01749 North Chicago, IL 60064 69 Grove Street (978) 212-5507 (781) 759-9519 Worcester, MA 01605 Megan Amundson (508) 791-1213 NARAL Pro-Choice Massachusetts Esmael Ansari George K.