Boston Market Viewpoint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Savills Studley Report Boston Office Sector Q1 2018

Savills Studley Research Boston Savills Studley Report Boston office sector Q1 2018 SUMMARY Market Highlights LEASING DECLINES RENT RISES "Boston's economy and office market has taken Following a strong fourth quarter of activity, The average asking rent for the entire region a different route in this cycle, deviating from with 4.0 million square feet (msf) leased – increased by 0.7% to $32.38. The Class quarterly activity inched down to 2.6 msf. A asking rent was essentially flat, inching the weak population and job growth displayed Tenants have leased 11.6 msf in the four down by 0.4% to $40.33. in many older Northeast and Midwest metros most recent quarters, 29.5% below the - and locally during prior cycles. This time has long-term market average of 16.4 msf. SALES DOWN SHARPLY truly been different for Boston. The willingness As of March 2018, office sales volume in AVAILABILITY RATES PUSH LOWER Boston totaled $1.9 billion in the last six of many companies to pay top dollar for months, down sharply compared to the $4.9 Boston's expertise in a wide variety of high-tech The market's overall availability rate billion sold in the previous six months. decreased by 50 basis points from 12.7% sectors has been a game-changer." to 12.2%. The Class A availability rate fell by 60 basis points to 13.2%. Steve Woodworth, Managing Director Savills Studley Report | Boston Recovery Covers a Lot of Office-Using Employment Trends Ground, Region a FrontRunner for HQ2 Millions 0.60 5% The duration, magnitude and scope of 0.58 Boston’s expansion in this cycle has been 3% impressive. -

Boston Office Market Report

BOSTON OFFICE MARKET REPORT SECOND QUARTER 2018 NO SIGNS OF SUMMER SLOWDOWN Greater Boston's market showed no signs of weakening during the second quarter by recording strong growth from numerous industry types. The market continued receiving inbound demand as well as converting organic growth into significant expansion. Most notably, Amazon's commitment to nearly 430,000 square feet at Parcel L4 in the Seaport reflects inbound demand while Wayfair's torrid expansion into roughly 395,000 SF in the Back Bay at 222 Berkeley and 500 Boylston Street exemplifies organic growth. The region's demographics and economy have remained solid which has supported and promoted Boston's recent expansion. Firmly rooted in education, technology and life sciences, Boston's diverse economic base has submitted strong job growth through increased recruitment and skilled labor retention from the area’s leading universities and institutions. Looking forward, expect durable market conditions and a diversified economy to guide the region's commercial real estate market to a strong performance over the next several years. 3.5% 3.8% # $2.6B 2ND MAY MAY MA QUARTERLY NATIONALLY IN MASSACHUSETTS NATIONAL VC FUNDING (Q1) QUARTERLY (Q1) UNEMPLOYMENT UNEMPLOYMENT VC FUNDING CLASS A MARKET ASKING RATE VS. DIRECT VACANCY TRENDS $64.00 16.0% $61.00 14.0% $58.00 12.0% GLOBAL DESTINATION $55.00 10.0% World leader in medical innovation and $52.00 8.0% technological advancement $49.00 6.0% TOWER SALES RIPPLE $46.00 4.0% EFFECT Will recent Class A Tower sales push $43.00 2.0% rental rates even higher? $40.00 0.0% 201720162015201420132012201120102009200820072006 YTD2018 TECHNOLOGY & Average Asking Rate Direct Vacancy (%) INNOVATION HUB Fortune 500 leaders and 1,900 homegrown startups CLASS B BUILD TO SUIT AND ASKING RATE VS. -

Suffolk University Institutional Master Plan Notification Form

SUFFOLK UNIVERSITY Institutional Master Plan Notification Form Submitted to Prepared by Boston Redevelopment Authority Vanasse Hangen Brustlin, Inc. Boston, Massachusetts In association with Submitted by Chan Krieger Sieniewicz Suffolk University CBT/Childs Bertman Tseckares, Inc. Boston, Massachusetts Rubin & Rudman LLP Suffolk Construction January, 2008 SUFFOLK UNIVERSITY Table of Contents 1. INTRODUCTION Background.............................................................................................................................1-1 The Urban Campus ................................................................................................................1-2 Institutional Master Planning Summary ..................................................................................1-3 2002 Suffolk University Institutional Master Plan....................................................1-3 2005 Amendment to Suffolk University Institutional Master Plan ...........................1-4 2007 Renewal of the Suffolk University Institutional Master Plan...........................1-5 2007 Amendment to Suffolk University Institutional Master Plan – 10 West Street Student Residence Hall Project .....................................................1-5 Public Process and Coordination............................................................................................1-6 Institutional Master Plan Team .............................................................................................1-10 2. MISSION AND OBJECTIVES Introduction.............................................................................................................................2-1 -

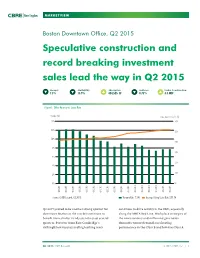

Speculative Construction and Record Breaking Investment Sales Lead the Way in Q2 2015

MARKETVIEW Boston Downtown Office, Q2 2015 Speculative construction and record breaking investment sales lead the way in Q2 2015 Vacancy Availability Absorption Sublease Under Construction 7.5% 13.9% 424,525 SF 0.75% 3.3 MSF Figure 1: Office Vacancy vs. Lease Rate Vacancy (%) Lease Rate Per Sq. Ft. ($) 14% $60 12% $50 10% $40 8% $30 6% $20 4% $10 2% 0% $0 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Source: CBRE Research, Q2 2015. Vacancy Rate 7.5% Average Asking Lease Rate $51.54 Q2 2015 proved to be another strong quarter for continues to drive activity in the CBD, especially downtown Boston as the market$60 continues to along the MBTA Red Line. Workplace strategies of benefit from similar trends seen the past several the new economy and millennial generation quarters. Pressure from East$50 Cambridge’s dominate tenant demand, accelerating strikingly low vacancy and high asking rents performance in the Class B and low-rise Class A $40 $30 Q2 2015 CBRE Research © 2015 CBRE, Inc. | 1 $20 $10 $0 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Sq. Ft. (000’s) 2,000 1,500 1,000 500 0 (5,000) (1,000) Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 MARKETVIEW BOSTON DOWNTOWN OFFICE markets. The investment sales market is red hot, contraction for the overall Boston market, the with record-breaking sales seen in all submarkets. -

B Oston Inner Harbor

93 30 Cambridge St Charlestown Msgr. O’Brien Chelsea St Hy Bridge Hampshire St Co Route 3 mm erc ial To Logan St t International 35 S t B s S Airport e 39 l r Broadway e o r v a t o h S n s Commercial Av C a d t Main St r H o on o f d M 31 i ar n Ch n a Longfellow a w ss t Ne a Cambridge St S ch Bridge u n I C se i C o n t h o d 22 t St a u St n s r State A r 16 w t St 7 A l t 29 e e o 33 S 34 l v a r r s B t n e n t v S o 38 i c H i t Harvard Bridge R m S e a s r n 4 2 e Boston T to r rl g 20 b Memorial Drive a Common in 44 o h Berkeley St sh 3 24 r C a 9 36 14 19 N W l o Public 8 10 41 e rth Beacon St er Garden 26 Beach S 37 n n Clarendon St t n A a v Dartmouth17 St 23Arlington St 42 C 25 43 S 15 21 h o 1 6 tuart S n 5 t r C gr 18 e e Commonwealth Av t t Su ss Commonwealth Av s n m S 46 e i m t 45 h e 40 c o r Boylston St r P 28 o Beacon St 90 t 27 D r 11 o Sobin 12 F Park 32 0 1/4 1/2 mi E Berkeley St 93 Boylston St 13 D St Huntington Av Brookline Av Reserved Channel Columbus Av Tremont St Representative Boston Office Landlord Projects 1 10 St. -

December 20, 2019 IMPORTANT INFORMATION on LEGIONELLA

Charles D. Baker Kathleen A. Theoharides Governor Secretary Karyn E. Polito Martin Suuberg Lieutenant Governor Commissioner December 20, 2019 IMPORTANT INFORMATION ON LEGIONELLA Dear Public Drinking Water Supplier, The Massachusetts Department of Environmental Protection (MassDEP) Drinking Water Program is writing to raise your awareness of Legionella and changes in the U.S. Department of Health and Human Services, Centers for Medicare & Medicaid Services (CMS) and the U.S. Department of Veterans Health Administration (VHA) health care facilities requirements that may impact CMS and VHA facilities on your distribution system and your water system. The CMS and VHA changes are intended to prevent Legionella outbreaks at healthcare and nursing home facilities. This letter also highlights important information about Legionella from the U.S. Environmental Protection Agency (EPA) and U.S. Centers for Disease Control and Prevention (CDC), American Water Works Association, as well as other relevant resources. Legionella is a bacteria found naturally in freshwater environments at generally low levels but can become a health problem when amplified in building water systems, especially large, complex water systems such as hotels, hospitals, and office buildings. When Legionella grows in the biofilm of premise plumbing and is aerosolized through devices such as showers, cooling towers, hot tubs, or fountains, people can breathe in small, contaminated water droplets. Inhalation of Legionella may result in a severe form of pneumonia known as Legionnaires’ disease, or in milder Pontiac fever. Even though Legionella is primarily attributed to premise plumbing issues, public water systems should be aware of the issue. For more information on Legionella, see the attached “Frequently Asked Questions, Information and Resources”. -

85 Devonshire Street Boston, Ma

85 DEVONSHIRE STREET BOSTON, MA RETAIL SPACE FOR LEASE 85 DEVONSHIRE STREET STREET FLOOR MEZZANINE BOSTON, MA 3,665 SF 855 SF – OPEN TO BELOW + 2,900 SF LOWE LEVEL 85 Devonshire Street provides hard corner visibility to a very busy vehicular and pedestrian intersection. Ideally positioned in the center of Downtown Crossing, adjacent to the MBTA - State Street entrance, with access to the Orange and Blue lines. Directly across from Congress Square which is occupied by: • 284,600 SF office including the 200,000 SF joint headquarters for DigitasLBi and Publicis.Sapient • A 165-key, 85,700 SF Hyatt Centric boutique hotel • 51,350 SF of residential space including 35 condominiums • 36,650 SF of retail Densely surrounded by office, hotel, and residential towers new and old, making this is an opportunity for strong seven-day customer counts and maximum brand visibility. 855 SF Dw WATER STREET WATER 3,665 SF OPEN TO BELOW +2,900 SF LOWER LEVEL DEVONSHIRE STREET PROPERTY FEATURES • 4,520 SF street-level retail/restaurant space and 2,900 SF lower-level space available • Corner location adjacent to MBTA entrance, across from Congress Square development, and steps from Freedom Trail and core Financial District • Approximately 55' of dramatic window line frontage along Devonshire Street, and 60’ of floor to ceiling window line along Water Street, allowing for prominent signage and branding visibility • Retail and restaurant neighbors include Dig Inn, HomeGoods, Love Art Sushi, Marshalls, Old Navy, Primark, Roche Bros., Shake Shack, Sweetgreen and T.J.Maxx -

2007 Labeled Buildings List Final Feb6 Bystate

ENERGY STAR® Qualified Buildings and Manufacturing Plants As of December 31, 2007 Building/Plant Name City State Building/Plant Type Alabama Calhoun County Administration Building Anniston AL Courthouse Calhoun County Court House Anniston AL Courthouse 10044 Birmingham AL Office Alabama Operations Center Birmingham AL Office BellSouth City Center Birmingham AL Office Birmingham Homewood TownePlace Suites by Marriott Birmingham AL Hotel/Motel Roberta Plant Calera AL Cement Plant Honda Manufacturing of Alabama, LLC Lincoln AL Auto Assembly Plant Alaska Elmendorf AFB, 3MDG, DoD/VA Joint Venture Hospital Elmendorf Air Force Base AK Hospital Arizona 311QW - Phoenix Chandler Courtyard Chandler AZ Hotel/Motel Bashas' Chandler AZ Supermarket/Grocery Bashas' Food City Chandler AZ Supermarket/Grocery Phoenix Cement Clarkdale AZ Cement Plant Flagstaff Embassy Suites Flagstaff AZ Hotel/Motel Fort Defiance Indian Hospital Fort Defiance AZ Hospital 311K5 - Phoenix Mesa Courtyard Mesa AZ Hotel/Motel 100 North 15th Avenue Building Phoenix AZ Office 1110 West Washington Building Phoenix AZ Office 24th at Camelback Phoenix AZ Office 311JF - Phoenix Camelback Courtyard Phoenix AZ Hotel/Motel 311K3 - Courtyard Phoenix Airport Phoenix AZ Hotel/Motel 311K4 - Phoenix North Courtyard Phoenix AZ Hotel/Motel 3131 East Camelback Phoenix AZ Office 57442 - Phoenix Airport Residence Inn Phoenix AZ Hotel/Motel Arboleda Phoenix AZ Office Bashas' Food City Phoenix AZ Supermarket/Grocery Biltmore Commerce Center Phoenix AZ Office Biltmore Financial Center I Phoenix AZ -

Suffolk University 1 Court Street Residence Hall Project Notification Form

September 2019 Suffolk University 1 Court Street Residence Hall Project Notification Form SUBMITTED TO PREPARED BY Boston Planning and Development Agency IN ASSOCIATION WITH NBBJ C3 Project Notification Form 1 Court Street Residence Hall Boston, Massachusetts SUBMITTED TO Boston Redevelopment Authority, d/b/a Boston Planning and Development Agency One City Hall Square, 9th Floor Boston, MA 02201 PROPONENT Suffolk University 8 Ashburton Place Boston, MA 02108 PREPARED BY VHB 99 High Street, 10th Floor Boston, MA 02110 In association with: NBBJ C3 September 2019 1 Court Street Residence Hall Project Notification Form Table of Contents Chapter 1: Project Description 1.1 Proposed Institutional Project Overview and Purpose ..................................................... 1-1 1.2 Institutional Master Plan Overview ........................................................................................... 1-2 1.2.1 Consistency with the 2020 IMP .................................................................................. 1-2 1.3 Site Context and Existing Conditions ....................................................................................... 1-2 1.3.1 Existing On-site Uses ..................................................................................................... 1-3 1.4 Project Description .......................................................................................................................... 1-3 1.4.1 Proposed Development Program ............................................................................ -

Boston Redevelopment Authority and Brian P

MEMORANDUM DECEMBER 10, 2015 TO: BOSTON REDEVELOPMENT AUTHORITY AND BRIAN P. GOLDEN, DIRECTOR FROM: MICHAEL CHRISTOPHER, DEPUTY DIRECTOR FOR DEVELOPMENT REVIEW/GOVERNMENT AFFAIRS KRISTIN KARA, DEPUTY DIRECTOR FOR SPECIAL PROJECTS COREY ZEHNGEBOT, SENIOR ARCHITECT/URBAN DESIGNER SUBJECT: REQUEST ADOPTION OF THE RESOLUTION ENTITLED “RESOLUTION OF BOSTON REDEVELOPMENT AUTHORITY RE: MODIFICATION TO CERTAIN URBAN RENEWAL PLANS OF THE CITY OF BOSTON” SUMMARY: This Memorandum requests adoption of a Resolution related to modifications to certain urban renewal plans to extend said plans in order to continue Boston’s community development activities. BACKGROUND The City of Boston (“City”) and the Boston Redevelopment Authority (“BRA”) utilize a wide variety of tools to proactively stimulate community development in Boston’s neighborhoods. The urban renewal program, one of these tools, was established by the Federal Housing Act of 1949, as amended, to create housing and promote economic development within the nation’s inner cities. As urban renewal plans approach their anticipated completion or termination dates, the City of Boston, like many cities and towns across Massachusetts, has been examining the role of urban renewal and the extension of urban renewal plans as necessary. The urban renewal program provides the BRA with a set of tools to encourage responsible redevelopment and revitalization of Boston’s neighborhoods. Today, the tools continue to be used to create affordable housing restrictions, promote/protect open space, and assemble parcels and clear title for development, which is a key component to securing project financing and title insurance. During the course of urban renewal in Boston, the City has had twenty-three (23) urban renewal plans. -

LAR Qualified Attorneys Suffolk

LAR Qualified Attorneys Suffolk Victorya Manakin Fee Law Office of Victorya Manakin Phone (617) 787-1222 [email protected] Half Hour $125 556 Cambridge St., Ste 101 Fax (617) 787-1550 One Hour $250 Allston MA 02134 Cash Check Credit Maureen Reilly Fee 654 Beacon Street, 6th Floor Phone (617) 338-2144 [email protected] Half Hour 150 Fax (888) 623-1164 One Hour 250 Bosston MA 02215 Cash Check Credit Jonathan M Bent Fee 75 Arlington Street Phone (617) 532-0797 Jbent!bentwinter.com Half Hour 75 Suite 500 Fax Bentwinter.com One Hour 150 Boston MA 02116 Cash Check Credit Heather M. Ward Fee Law Office of Heather Ward Phone (617) 903-8955 [email protected] Half Hour $100 711 Atlantic Ave., Lower Level Fax www.heatherwardlaw.com One Hour $195 Boston MA 02111 Cash Check Credit Alexis B. Kaplan Fee 92 State Street Phone (617) 903-0225 [email protected] Half Hour 2nd Floor Fax abkaplanlaw.com One Hour Boston MA 02109 Cash Check Credit Alina Zilberberg Fee 92 State Street, Law Office of Alin Phone (617) 391-0063 [email protected] Half Hour $87.50 Fax (617) 391-0064 One Hour $175.00 Boston MA 02109 Cash Check Credit Erin J. Harris Fee 185 Devonshire St., Suite 302 Phone (617) 532-3906 [email protected] Half Hour $112.50 Fax (617) 507-6432 www.harrislawboston.com One Hour $225.00 Boston MA 02210 Cash Check Credit Rachel Engdhal Fee 8 Faneuil Hall Phone (617) 973-6446 [email protected] Half Hour 3rd Floor Fax www.rachelengdahllaw.com One Hour $190-$225 Boston MA 02110 Cash Check Credit Gregory P. -

Get Shopping!Grab a Retail

BEACON STREET Note: the majority of the businesses listed here are subject to COVID-related restrictions. Please call-ahead as you are making plans. BOSTON COMMON STATE HOUSE/BEACON HILL PARK STREET VISITOR INFO CENTER TH CHURCH GRANARY BURYING THE SHAW 54 REGIMENT MEMORIAL GROUND BEACON STREET AFRICAN-AMERICAN HERITAGE TRAIL Freedom Trail NORMAN THEATERS GNC 343 Washington Street, H3 | 58 Winter Street, F1 CRUMP 450 Washington St., E4 BEANTOWN BEANTOWN GALLERY AMC Loews Cinema 19 175 Tremont Street, B2 Lenscrafters (Macy’s) PUB CAFÉ PUB PAPER SOURCE FENWAY PARK HAMILTON PL. Pearle Vision 100 City Hall Plaza, K1 PUBLIC GARDEN NINE TREMONT Boston Opera House 539 Washington Street, C2 MUSEUM OF FINE ARTS WEN’S FALAFEL MOOYAH ZERO TEMPLE BACK BAY/NEWBURY STREET YUNNAN KING BURGERS HOTEL BRONCORE Modern Theatre 525 Washington Street, C2 Tobias & Battite Hearing Healthcare 16 Temple Place, E1 GLOBAL PACK NOODLES INSOMNIA FITNESS SHIP/FEDEX SUFFOLK UNIVERSITY COOKIES Orpheum Theatre 1 Hamilton Place, F2 Vision Care 2000 48 High Street, G7 DR. PHIL’S COMPUTER SISTERS DISCIPLES LAW SCHOOL BOOKSTORE BETTER SORTS RELIGIOUS GIFTS Paramount Center 545 Washington Street, C2 Wig World 27 Temple Place, E2 REPAIR CENTER SOCIAL CLUB SANTACROSS JADE NAILS DISTINCTIVE SHOE CARBON METRO CREDIT UNION ESCAPE CLOTHING SCHOOL STREET COFFEEHOUSE SALON THREADING PLACE FROM ITALY ODESSA INSTANT BOXAROO ATTRACTIONS HOME FURNISHINGS THE ROOM SHOE REPAIR EMPIRE TASTY BURGER T-MOBILE COURT SQUARE Boston Massacre Site Plaza 208 Washington Street, K3 HomeGoods 350 Washington Street, 3G BEAUTY CAFÉ 26 LADDER DISTRICT 26 COURT STREET COMMONWEALTH SALON ONEGIG BOUTIQUE MONEY BANK Boxaroo 55 Court Street, J1 Macy’s 450 Washington Street, F3 MUSEUM CHAPMAN PLACE 2 Avery Street, B3 DEMOCRACY BREWING OF BOSTON Emerson College Urban Arts Gallery 25 Avery Street, B2 Roche Bobois ORPHEUM THEATRE COLONIAL 17 WEST STREET TRADING CO.