Savills Studley Report Boston Office Sector Q1 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Directory of Massachusetts LOBBYISTS 617.646.1000 - BOSTON - WASHINGTON DC GREG M

Directory of Massachusetts LOBBYISTS 617.646.1000 - www.oneillandassoc.com BOSTON - WASHINGTON DC GREG M. PETER J. VICTORIA E. MARK K. MATTHEW P. D’AGOSTINO D’AGOSTINO IRETON MOLLOY MCKENNA Lobbying & Public Aairs Providing comprehensive state and municipal advocacy. PRACTICE AREAS: TRANSPORTATION | HEALTH CARE PUBLIC SAFETY | REGULATIONS | ENERGY ENVIRONMENT | CANNABIS FINANCIAL SERVICES | EMERGING INDUSTRIES 12 POST OFFICE SQUARE, 6TH FLOOR | BOSTON, MA 02109 | 6175743399 WWW.TENAXSTRATEGIES.COM David Albright Oamshri Amarasingham Cynthia Arcate Jewish Alliance for Law and Social Action American Civil Liberties PowerOptions, Inc. A 18 Tremont Street, Suite 320 Union of Massachusetts 129 South Street, 5th Floor Boston, MA 02108 211 Congress Street Boston, MA 02111 Anthony Arthur Abdelahad (617) 227-3000 Boston, MA 02110 (617) 428-4258 Ventry Associates LLP (617) 482-3170 1 Walnut Street Walter Alcorn Luz A. Arevalo Boston, MA 02108 Consumer Technology Association Robert J. Ambrogi Greater Boston, Legal Services (617) 423-0028 1919 South Eads Street Law Office of Robert Ambrogi 197 Friend Street Arlington, VA 22202 128 Main Street Boston, MA 02114 Tate Abdols (571)239-5209 Gloucester, MA 01930 (617) 603-1569 Onex Partners Advisor, Inc. (978) 317-0972 161 Bay Street Theodore J. Alexio Jr. Derek Armstrong Toronto, ON M5J 2S1 Essential Strategies Inc. Shannon Ames Bank of America, N.A. (416) 362-7711 One State Street, Suite 1100 Low Impact Hydropower Institute 100 Federal Street Boston, MA 02109 329 Massachusetts Avenue, Suite 6 Boston, MA 02110 Brendan Scott Abel (617) 227-6666 Lexington, MA 02420 (617) 434-8613 Massachusetts Medical Society (781) 538-4266 860 Winter Street Waltham, MA 02451 Daniel Allegretti Gabriel Amo Kristina Ragosta Arnoux (781) 434-7682 Exelon Generation Company, LLC Magellan Health 1 Essex Drive The Home Depot 8621 Robert Fulton Drive Bow, NH 03304 166 Valley Street, 6M222 Columbia, MD 21046 Lisa C. -

Boston Office Market Report

BOSTON OFFICE MARKET REPORT SECOND QUARTER 2018 NO SIGNS OF SUMMER SLOWDOWN Greater Boston's market showed no signs of weakening during the second quarter by recording strong growth from numerous industry types. The market continued receiving inbound demand as well as converting organic growth into significant expansion. Most notably, Amazon's commitment to nearly 430,000 square feet at Parcel L4 in the Seaport reflects inbound demand while Wayfair's torrid expansion into roughly 395,000 SF in the Back Bay at 222 Berkeley and 500 Boylston Street exemplifies organic growth. The region's demographics and economy have remained solid which has supported and promoted Boston's recent expansion. Firmly rooted in education, technology and life sciences, Boston's diverse economic base has submitted strong job growth through increased recruitment and skilled labor retention from the area’s leading universities and institutions. Looking forward, expect durable market conditions and a diversified economy to guide the region's commercial real estate market to a strong performance over the next several years. 3.5% 3.8% # $2.6B 2ND MAY MAY MA QUARTERLY NATIONALLY IN MASSACHUSETTS NATIONAL VC FUNDING (Q1) QUARTERLY (Q1) UNEMPLOYMENT UNEMPLOYMENT VC FUNDING CLASS A MARKET ASKING RATE VS. DIRECT VACANCY TRENDS $64.00 16.0% $61.00 14.0% $58.00 12.0% GLOBAL DESTINATION $55.00 10.0% World leader in medical innovation and $52.00 8.0% technological advancement $49.00 6.0% TOWER SALES RIPPLE $46.00 4.0% EFFECT Will recent Class A Tower sales push $43.00 2.0% rental rates even higher? $40.00 0.0% 201720162015201420132012201120102009200820072006 YTD2018 TECHNOLOGY & Average Asking Rate Direct Vacancy (%) INNOVATION HUB Fortune 500 leaders and 1,900 homegrown startups CLASS B BUILD TO SUIT AND ASKING RATE VS. -

Retail/Restaurant Opportunity BOSTON, MASSACHUSETTS Introducing Boston’S Market the Opportunity Newest Destination Overview

retail/restaurant opportunity BOSTON, MASSACHUSETTS Introducing Boston’s market the opportunity newest destination overview daily subway boardings: 12,553 state street Congress Square, located centrally in the heart of Boston’s downtown, 100,000 downtown crossing will reinvent four interconnected, congress square (congress and water streets) early 20th century neoclassical and Beaux Arts buildings into a 300,000 SF contemporary, mixed-use office, of committed Congress Square office tenants residential and retail destination. Newly transformed streetscapes $134,855 along Congress Street, Water average household income Street, Devonshire Street and within 0.5 miles Quaker Lane will connect Post congress square (congress street retail storefronts) Office Square to Faneuil Hall with +230,000 daytime population a vibrant mix of retail, restaurants and inviting public spaces. Completion Summer 2018 just steps from: Faneuil Hall 20 MILLION EXCLUSIVE DINING annual visitors AMENITY RETAIL AND Boston’s Historic Freedom Trail FIRST CLASS SERVICES 4 MILLION annual visitors view down devonshire street view from post office square retail market SEAPORT DISTRICT INTERCONTINENTAL BOSTON (424 KEYS) SOUTH STATION (MBTA/AMTRAK) SMITH & BOSTON HARBOR HOTEL WOLLENSKY (230 KEYS) MERITAGE MILLENNIUM TOWER RESTAURANT (442 LUXURY UNITS) THE PALM BOSTON PABU HYATT REGENCY BOSTON (502 KEYS) TRILLIUM THE LANGHAM BEER GARDEN (317 KEYS) T.J .MAXX PAUL BAKERY MARSHALLS MACY’S RUKA LEGAL SEA FOODS BOSTON SPORTS CLUB PRIMARK STERLINGS GRANARY TAVERN GEORGE HOWELL DIG INN THE MERCHANT OLD NAVY KITCHEN & DRINKS HARBORSIDE INN THE GODFREY HOTEL (116 KEYS) B.GOOD MARLIAVE ROCHE BROS. (243 KEYS) AMERICAN EAGLE CHIPOTLE FOREVER 21 OUTFITTERS SWEETGREEN DSW ANN TAYLOR LOFT UNIQLO CLOVER BANANA REPUBLIC ANN TAYLOR JOS. -

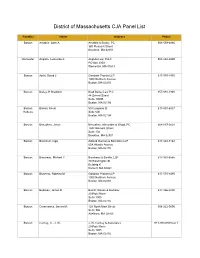

District of Massachusetts CJA Panel List

District of Massachusetts CJA Panel List Panel(s) Name Address Phone Email Boston Amabile, John A Amabile & Burkly, PC 508-559-6966 [email protected] 380 Pleasant Street Brockton, MA 02301 Worcester Angiulo, Leonardo A. Angiulo Law, PLLC 508-868-0899 [email protected] PO Box 2903 Worcester, MA 01613 Boston Apfel, David J Goodwin Procter LLP 617-570-1970 [email protected] 1000 Northern Avenue Boston, MA 02210 Boston Bailey, R Bradford Brad Bailey Law P.C. 857-991-1945 [email protected] 44 School Street Suite 1000B Boston, MA 02108 Boston Barron, Kevin 50 Congress St 617-407-6837 [email protected] Habeas Sutie 600 Boston, MA 02109 Boston Benzaken, Jason Benzaken, Alexander & Wood, PC 508-897-0001 [email protected] 1342 Belmont Street Suite 102 Brockton, MA 02301 Boston Bernstein, Inga Zalkind Duncan & Bernstein LLP 617-820-5168 [email protected] 65A Atlantic Avenue Boston, MA 02110 Boston Bourbeau, Michael C Bourbeau & Bonilla, LLP 617-350-6565 [email protected] 80 Washington St Building K Norwell, MA 02061 District of Massachusetts CJA Panel List Panel(s) Name Address Phone Email Boston Braceras, Roberto M Goodwin Procter LLP 617-570-1895 [email protected] 1000 Northern Avenue Boston, MA 02210 Boston Budreau, James H Bassil & Budreau 617-276-7385 [email protected] 20 Park Place Suite 1005 Boston, MA 02116 Boston Caramanica, James M. 120 North Main Street 508-222-0096 [email protected] Suite 306 Attelboro, MA 02703 Boston Carney, Jr., J. W. J. W. Carney & Associates -

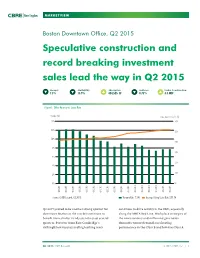

Speculative Construction and Record Breaking Investment Sales Lead the Way in Q2 2015

MARKETVIEW Boston Downtown Office, Q2 2015 Speculative construction and record breaking investment sales lead the way in Q2 2015 Vacancy Availability Absorption Sublease Under Construction 7.5% 13.9% 424,525 SF 0.75% 3.3 MSF Figure 1: Office Vacancy vs. Lease Rate Vacancy (%) Lease Rate Per Sq. Ft. ($) 14% $60 12% $50 10% $40 8% $30 6% $20 4% $10 2% 0% $0 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Source: CBRE Research, Q2 2015. Vacancy Rate 7.5% Average Asking Lease Rate $51.54 Q2 2015 proved to be another strong quarter for continues to drive activity in the CBD, especially downtown Boston as the market$60 continues to along the MBTA Red Line. Workplace strategies of benefit from similar trends seen the past several the new economy and millennial generation quarters. Pressure from East$50 Cambridge’s dominate tenant demand, accelerating strikingly low vacancy and high asking rents performance in the Class B and low-rise Class A $40 $30 Q2 2015 CBRE Research © 2015 CBRE, Inc. | 1 $20 $10 $0 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Sq. Ft. (000’s) 2,000 1,500 1,000 500 0 (5,000) (1,000) Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 MARKETVIEW BOSTON DOWNTOWN OFFICE markets. The investment sales market is red hot, contraction for the overall Boston market, the with record-breaking sales seen in all submarkets. -

CJA Panel List All Alpha.Xlsx

District of Massachusetts CJA Panel List Panel(s) Name Address Phone Boston Amabile, John A Amabile & Burkly, PC 508-559-6966 380 Pleasant Street Brockton, MA 02301 Worcester Angiulo, Leonardo A. Angiulo Law, PLLC 508-868-0899 PO Box 2903 Worcester, MA 01613 Boston Apfel, David J Goodwin Procter LLP 617-570-1970 1000 Northern Avenue Boston, MA 02210 Boston Bailey, R Bradford Brad Bailey Law P.C. 857-991-1945 44 School Street Suite 1000B Boston, MA 02108 Boston Barron, Kevin 50 Congress St 617-407-6837 Habeas Sutie 600 Boston, MA 02109 Boston Benzaken, Jason Benzaken, Alexander & Wood, PC 508-897-0001 1342 Belmont Street Suite 102 Brockton, MA 02301 Boston Bernstein, Inga Zalkind Duncan & Bernstein LLP 617-820-5168 65A Atlantic Avenue Boston, MA 02110 Boston Bourbeau, Michael C Bourbeau & Bonilla, LLP 617-350-6565 80 Washington St Building K Norwell, MA 02061 Boston Braceras, Roberto M Goodwin Procter LLP 617-570-1895 1000 Northern Avenue Boston, MA 02210 Boston Budreau, James H Bassil, Klovee & Budreau 617-366-2200 20 Park Place Suite 1005 Boston, MA 02116 Boston Caramanica, James M. 120 North Main Street 508-222-0096 Suite 306 Attelboro, MA 02703 Boston Carney, Jr., J. W. J. W. Carney & Associates 617-933-0350 ext 1 20 Park Place Suite 1405 Boston, MA 02116 District of Massachusetts CJA Panel List Panel(s) Name Address Phone Boston Christofferson, Eric DLA Piper LLP (US) 617-406-6089 33 Arch Street Boston, MA 02210 Habeas Church, Susan Demissie & Church 617-354-3944 929 Massachusetts Avenue Cambridge, MA 02139 Boston Cipoletta, James J 385 Broadway 781-289-7777 Suite 307 Revere, MA 02151 Boston Cloherty, Daniel J Todd & Weld LLP 617-624-4774 One Federal Street Boston, MA 02110 Boston Connolly, William H 20 Park Plaza 617-542-0200 Suite 1000 Boston, MA 02116 Boston Cunha, John Cunha & Holcomb, P.C. -

Cbrecap Spotlight

cbrecap IT'S AWARDS SEASON! The Colbert Coldwell Circle represents the top CBRE professionals in the United States. The following CBRE/ NE employees were recognized with this great achievement. CBRE/NEW ENGLAND Top 100 2014 Producers EMPLOYEE NEWSLETTER • SPRING 2015 • Simon Butler Vice Chairman/Partner • David Fitzgerald Vice Chairman/Partner spotlight • Biria St. John Vice Chairman/Partner ANNUAL CONFERENCE/SUMMER OUTING SAVEANNUAL CONFERENCE/SUMMER THE DATE OUTING Top 250 2014 Producers SAVE THE DATE • Chris Angelone THURSDAY, JUNE 18, 2015 Executive Vice President/Partner ADD TO CALENDAR • Patrick Cavanagh THURSDAY, JUNE 18, 2015 Executive Vice President/Partner ADD TO CALENDAR • Bob Gibson Executive Vice President/Partner • Bill Moylan Executive Vice President/Partner & & Top 25 Retail Producers • Kevin Higgins Senior Vice President/Principal • Rob Robledo Vice President, Retail Tenant Services cbrecap CBRE/NE WINS THREE 2015 REGIONAL Under 100,000 SF: 410 Totten Pond Road TOBY AWARDS! Tenants at 410 Totten Pond Earth Award: One Beacon Street Road enjoy a private, fully equipped playground and One Beacon Street is LEED-EB basketball court as well Silver certified, and was the first as a cafeteria for all park multi-tenant building in Boston to tenants. achieve the rating. CBRE/NE's Jason Richardson leads the team at CBRE/NE's Philip Boccalatte leads 410 Totten Pond team. the team at One Beacon Street. BOMA BOSTON TOBY WINNERS Renovated Building: 50 Post Office Square Medical Building: 333 Longwood Avenue The 21-story Art Deco office Retail Building: 350 Washington Street building underwent extensive Renovated Building: 50 Post Office Square renovations from January 2011 Historical Building: 501 Boylston Street to 2013. -

Boston Market Viewpoint

Research & Forecast Report GREATER BOSTON MARKET VIEWPOINT Q4 2015 Boston Overview Large Requirements The downtown Boston office market was running on all cylinders in TENANT SF INDUSTRY 2015, posting over two million square feet of positive absorption Putnam Investments 250,000 Financial Services and an unprecedented seven million square feet for the five- Eze Castle 125,000 Technology year period 2011 to 2015. The Financial District was by far the Advent International 100,000 Financial Services largest contributor to the positive results in 2015. Occupancy in this core submarket increased by over 1.3 million square feet WeWork 90,000 Business Services with the majority (920,000 SF) recorded in the low-rise segment Rue LaLa 75,000 Retail of the Class A tower market. Nearly 400,000 square feet of Boston Globe 75,000 Media/Publishing positive absorption was recorded in the Seaport, largely due to the construction completion of 101 Seaport Square, a 420,000-square- Velocity foot office building anchored by PwC. > Velocity (signed lease activity) was healthy over the course of 2015, with approximately 4.6 million square feet of leases signed. Statistics in the core submarkets are as follows: > The largest transaction in 2015 was BNY Mellon’s Boston Market Statistics 250,000-square-foot renewal at One Boston Place. Although this represented a contraction of approximately 100,000 square 2015 MARKET SEGMENT SUPPLY (SF) VACANCY RATE* ABSORPTION feet for the financial services firm, market-wide tenants in Financial District – Class A 27,762,321 9.1% 1,192,196 growth mode far outnumbered those reducing their space requirements. -

TRENDS in the Real Estate Market

TRENDS IN the real estate market 2016 WELCOMING REMARKS Tom Hynes, Co-Chairman KEYNOTE ADDRESS Charlie Baker Governor of Massachusetts PLACEMAKING from concept to reality THE BOSTON MARKET Ron Perry, President 1.75M Rendering by Neoscape 3rd Tallest Building High End Rents Topping $80/RSF H “General Electric to select Boston as new global headquarters”. E “Boston’s biggest office sale this year just closed – for $1.3 billion [500 A Boylston & 222 Berkeley Street]”. D L “It’s official: Putnam Investments making big move to 100 Federal St. ” I “Boston Globe will move HQ to downtown office N [53 State Street]”. E “As Pier 4 develops, Tishman Speyer makes another South Boston S play [One Channel Center - $316.5M]”. K E Y S T vacancy net absorption A T 8.9% 2.1M RSF S K E Y rental rates S T $48-$80 $38-$52 $65-$85 A T S T Back Bay Financial District O W E R Vacancy 5.9% 20th Floor 5.6% S T 6.6% 3.1% U D Y V 5M RSF 30% E L O 250K RSF 250K RSF 250K RSF 200K RSF 175K RSF C One Boston Place 100 Federal Street Landmark Center 125 High Street Schrafft Center I T Y 85K RSF 150K RSF 125K RSF 120K RSF 110K RSF Innovation & Design 125 High Street 1325 Boylston Street 333 Summer Street Landmark Center Building T E N 4M RSF 7 options > 100K RSF A N T S 600K RSF 250K RSF 200K RSF 125K RSF 100K RSF I N M A R K 100K RSF 90K RSF 75K RSF 75K RSF 65K RSF E T =Committed Tenants suburban M 1M RSF I G R destination: boston A T suburban I O N N E W recently completed [office] D E 680K RSF V E L O P M E N 101 Seaport Boulevard 1325 Boylston Street T Skanska Samuels -

Walkboston Annual Report 2015 (PDF)

2015 Annual Report 26th Annual Celebration March 22nd, 2016 Microsoft NERD Center 1 Memorial Drive Cambridge, MA MAKING MASSACHUSETTS MORE WALKABLE WalkBoston Board & Staff Board Officers President | Matt Lawlor Vice President | Linda Sharpe Treasurer | Greg Rogers Secretary | Emma Rothfeld Yashar Counsel | Erik Lund Board: WalkBoston Staff: Joe Beggan Stacey Beuttell | Program Director David Black Julie DeMauro | SRTS Coordinator Hillary Borcherding Dorothea Hass | Sr. Project Manager Betsy Boveroux Brendan Kearney | Communications Manager Amy Branger Wendy Landman | Executive Director Nina Cohen Barbara Maratos | Office Administrator Whitney Dailey Adi Nochur | Project Manager Joyce DiBona Laura O’Rourke | Development Manager Mark Favermann Bob Sloane | Sr. Project Manager Nina Garfinkle Paula Gold Ann Hershfang Kasia Hart | Intern Betsy Johnson Tony Lechuga | Intern Karla Karash Matt Lawlor Erik Lund Tom Ball | Accountant Jerry Pucillo Cathy Tran | Bookkeeper William Reyelt Greg Rogers Linda Sharpe Karen Cord Taylor Emma Rothfeld Yashar 1 program Welcome Matt Lawlor | President 25th Anniversary Reflections Linda Sharpe | Vice President Year in Review Wendy Landman | Executive Director Presentation of Golden Shoe Awards Charlotte Fleetwood Maggie Sachs-Mahmood Boston Project Ministries/Talbot-Norfolk Triangle Neighbors United & Codman Sq. Neighborhood Dev. Corp. Keynote Speaker Leah Shahum | Founder and Director, Vision Zero Network WalkBoston Mission WalkBoston makes walking safer and easier to encourage better health, a cleaner environment -

The Boston Economy - 2003

589 The Boston Economy - 2003 THOMAS M. MENINO, MAYOR CITY OF BOSTON Boston Redevelopment Authority Mark Maloney, Director Clarence J. Jones, Chairman Consuelo Gonzales Thornell, Treasurer Joseph W. Nigro, Jr., Co-Vice Chairman Michael Taylor, Co-Vice Chairman Christopher J. Supple, Member Harry R. Collings, Secretary Report prepared by Dominic Modicamore Jim Vrabel Luis Rosero Policy Development and Research Gregory Perkins, Interim Director Report #589 October 2003 TABLE OF CONTENTS Boston’s Economy – 2003 ...............................................................................................................1 General...........................................................................................................................................1 Overview of Current Economic Conditions……………………………………………………….1 Statistical Data……………………………………………………………………………………..2 New England, Massachusetts, and Metropolitan Boston Economies .............................................................................................2 Employment Structure, Employment Trends, and Occupational Changes.............................................................................................................3 Unemployment...............................................................................................................................6 Largest Employers .........................................................................................................................7 Labor Force and Education............................................................................................................8 -

Legal Matters

'LUHFWRU\RI 0DVVDFKXVHWWV'LUHFWRU\RI /REE\LVWV0DVVDFKXVHWWV /REE\LVWV 7\ISPJ 3H^ Executive Legislative Regulatory Municipal 51 Franklin Street l Boston l 617.778.1200 www.JohnsonHaleyLLP.com The Directory of Massachusetts Lobbyists 2011 1 FROM THE PUBLISHER Dear Reader: Thank you for taking the time to make use of our 2011 Directory of Massachusetts Lobbyists. In 2005, we noticed that there was no comprehensive list of lobbyists in the state. Seeking to fill that void, we began publishing this directory. Now the directory is used by executives, legislators and attorneys as a quick reference to the world of lobbying in our state. Many people use it as a starting point when they begin the process of deciding what lobbyist to use for whatever their need may be. As the publishers of Massachusetts Lawyers Weekly, we sit at a distinct intersection of law and business. And we realize the value of a good lobbyist. That’s why we make sure this directory gets into the hands of thousands of corporate decision makers. For more information about this directory, additional copies or to advertise in future editions of the publication, please contact Melanie Footer at 617.218.8121 or e-mail [email protected]. And once again thanks for your interest in the Directory of Massachusetts Lobbyists. Sincerely, Susan Bocamazo Publisher DONOGHUE BARRETT & SINGAL, P.C . INTEGRATED LEGAL SERVICES Resources. Relationships. Results. • Resources include skilled specialists in legislative and regulatory affairs—and integrated services through our Health Care, Litigation, and Corporate Departments. • Relationships include an expansive network of government, legal, and industry contacts that offer valuable access, insights, and leverage.