Annual Business Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chicago Board Options Exchange Annual Report 2001

01 Chicago Board Options Exchange Annual Report 2001 cv2 CBOE ‘01 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 CBOE is the largest and 01010101010101010most successful options 01010101010101010marketplace in the world. 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010ifc1 CBOE ‘01 ONE HAS OPPORTUNITIES The NUMBER ONE Options Exchange provides customers with a wide selection of products to achieve their unique investment goals. ONE HAS RESPONSIBILITIES The NUMBER ONE Options Exchange is responsible for representing the interests of its members and customers. Whether testifying before Congress, commenting on proposed legislation or working with the Securities and Exchange Commission on finalizing regulations, the CBOE weighs in on behalf of options users everywhere. As an advocate for informed investing, CBOE offers a wide array of educational vehicles, all targeted at educating investors about the use of options as an effective risk management tool. ONE HAS RESOURCES The NUMBER ONE Options Exchange offers a wide variety of resources beginning with a large community of traders who are the most experienced, highly-skilled, well-capitalized liquidity providers in the options arena. In addition, CBOE has a unique, sophisticated hybrid trading floor that facilitates efficient trading. 01 CBOE ‘01 2 CBOE ‘01 “ TO BE THE LEADING MARKETPLACE FOR FINANCIAL DERIVATIVE PRODUCTS, WITH FAIR AND EFFICIENT MARKETS CHARACTERIZED BY DEPTH, LIQUIDITY AND BEST EXECUTION OF PARTICIPANT ORDERS.” CBOE MISSION LETTER FROM THE OFFICE OF THE CHAIRMAN Unprecedented challenges and a need for strategic agility characterized a positive but demanding year in the overall options marketplace. The Chicago Board Options Exchange ® (CBOE®) enjoyed a record-breaking fiscal year, with a 2.2% growth in contracts traded when compared to Fiscal Year 2000, also a record-breaker. -

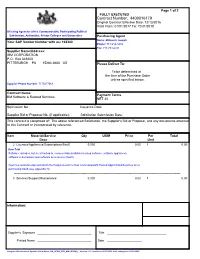

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

Java and Z/OS (And Rdz)

® IBM Software Group Java and z/OS (and RDz) Jon Sayles – [email protected] © 2016 IBM Corporation IBM Software Group | Rational software Merrill Class . They’ll have RDz exposure . Terms & Concepts & Vocabulary Remove fear of Java Analogies – Procedural vocabulary 20 – 30 students - mix of young + old (mostly old) dudes . Call COBOL from Java Java doesn’t create an .exe Objects . z/OS Java Standard z/OS environment JCL – pointing to Unix Aware of JVM – can call COBOL http://www.s390java.com/index.htm IBM Software Group | Rational software Trademarks Trademarks The following are trademarks of the International Business Machines Corporation in the United States and/or other countries. For a complete list of IBM Trademarks, see www.ibm.com/legal/copytrade.shtml: AS/400, DBE, e-business logo, ESCO, eServer, FICON, IBM, IBM Logo, iSeries, MVS, OS/390, pSeries, RS/6000, S/30, VM/ESA, VSE/ESA, Websphere, xSeries, z/OS, zSeries, z/VM The following are trademarks or registered trademarks of other companies Lotus, Notes, and Domino are trademarks or registered trademarks of Lotus Development Corporation Java and all Java-related trademarks and logos are trademarks of Sun Microsystems, Inc., in the United States and other countries LINUX is a registered trademark of Linux Torvalds UNIX is a registered trademark of The Open Group in the United States and other countries. Microsoft, Windows and Windows NT are registered trademarks of Microsoft Corporation. SET and Secure Electronic Transaction are trademarks owned by SET Secure Electronic Transaction LLC. Intel is a registered trademark of Intel Corporation * All other products may be trademarks or registered trademarks of their respective companies. -

Annual Report 2011

ANNUAL REPORT 2011 TO OUR STOCKHOLDERS: I am pleased to report that KLA-Tencor performed at record levels on several fronts in fi scal year 2011. We achieved company records in our most critical fi nancial metrics, including revenues, net income, earnings per share and profi t margins, and our year-over-year revenue growth signifi cantly exceeded that of our peer group and our industry. At the same time, we generated record free cash fl ow and continued to deliver meaningful returns to our stockholders in the form of dividends and stock repurchases. This performance was the result of our unwavering focus on develop- ing market-leading technology, addressing our customers’ most critical needs and driving operational effi ciency. Though our industry has seen a recent slowdown in demand, we remain very excited about KLA-Tencor’s prospects for the future. The long-term demand drivers for KLA-Tencor and our industry remain intact, and we are well positioned to grow as demand for semiconductor capital equipment recovers. Our record results in fi scal year 2011 demonstrate that our strategies are working. Looking back over our 35-year history, we have established a pattern of achievement and leadership, which has enabled us to create the strong foundation from which we now look ahead to the future. Our accomplishments during fi scal year 2011 in each of our four strategic objectives (Customer Focus, Growth, Operational Excellence and Talent Development) are highlighted below: CUSTOMER FOCUS: MARKET LEADERSHIP Our customer focus strategic objective is measured in customer satisfaction and market share. We maintained our market leadership positions among our foundry and logic customers in fi scal year 2011 and improved our market position in memory, as evidenced by achieving record new order levels across all our end markets during the year. -

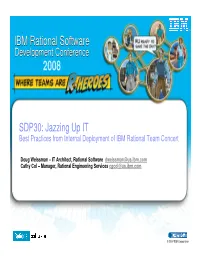

IBM Rational Software IBM Rational Software

® IBM Rational Software Development Conference 2008 SDP30: Jazzing Up IT Best Practices from Internal Deployment of IBM Rational Team Concert Doug Weissman – IT Architect, Rational Software [email protected] Cathy Col – Manager, Rational Engineering Services [email protected] © 2007 IBM Corporation IBM Rational Software Development Conference 2008 Agenda Goal of presentation Why did we centralize deployment of Rational Team Concert? A Simple RTC Configuration Considerations for deploying Rational Team Concert Rational Software’s RTC Deployment Benefits, Best Practices, and Lessons Learned SDP30 – Jazzing Up IT 2 IBM Rational Software Development Conference 2008 Goal of Presentation Help you think about how to deploy Rational Team Concert Give you some suggestions as to possible architectures and configurations Discuss some benefits, best practices, pitfalls, and lessons learned SDP30 – Jazzing Up IT 3 IBM Rational Software Development Conference 2008 Agenda Goal of presentation Why did we centralize deployment of Rational Team Concert? A Simple RTC Configuration Considerations for deploying Rational Team Concert Rational Software’s RTC Deployment Benefits, Best Practices, and Lessons Learned SDP30 – Jazzing Up IT 4 s ent rem qui r re rve l se ima Min IBM Rational Software Development Conference 2008 e Grassroot movement to adopt new technology s u e d bl n si “Jazz” adoptiona was rampant ats Rational! ce d y ac e lo ly s p ee a e fr -b d ad ” o lo ne t n g y ow pa s D rt m a o a E p ch p n dly u w frien e s r o , team -

Sejarah Perkembangan Dan Kemajuan the International Bussines Machines

SEJARAH PERKEMBANGAN DAN KEMAJUAN THE INTERNATIONAL BUSSINES MACHINES Oleh : ANGGARA WISNU PUTRA 1211011018 CIPTA AJENG PRATIWI 1211011034 DERI KURNIAWAN 1211011040 FEBY GIPANTIUS ZAMA 1211011062 NOVITA LIANA SARI 1211011118 RAMA AGUSTINA 1211011128 FAKULTAS EKONOMI DAN BISNIS UNIVERSITAS LAMPUNG BANDAR LAMPUNG 2014 BAB II PEMBAHASAN 2.1 Sejarah berdirinya THE INTERNATIONAL BUSSINES MACHINES (IBM) 1880—1929 Pada tahun 1880-an, beberapa teknologi yang akan menjadi bisnis IBM ditemukan. Julius E. Pitrap menemukan timbangan komputer pada tahun 1885. Alexander Dey menemukan dial recorder tahun 1888. Herman Hollerith menemukan Electric Tabulating Machine 1989 dan pada tahun yang sama Williard Bundy menemukan alat untuk mengukur waktu kerja karyawan. Pada 16 Juni 1911, teknologi-teknologi tersebut dan perusahaan yang memilikinya digabungkan oleh Charles Ranlett Flint dan membentuk Computing Tabulating Recording Company (CTR). Perusahaan yang berbasis di New York ini memiliki 1.300 karyawan dan area perkantoran serta pabrik di Endicott dan Binghamton, New York; Dayton, Ohio; Detroit, Michigan; Washington, D.C.; dan Toronto, Ontario. CTR memproduksi dan menjual berbagai macam jenis mesin mulai dari timbangan komersial hingga pengukur waktu kerja. Pada tahun 1914, Flint merekrut Thomas J. Watson, Sr., dari National Cash Register Company, untuk membantunya memimpin perusahaan. Watson menciptakan slogan, ―THINK‖, yang segera menjadi mantra bagi karyawan CTR. Dalam waktu 11 bulan setelah bergabung, Watson menjadi presiden dari CTR. Perusahaan memfokuskan diri pada penyediaan solusi penghitungan dalam skala besar untuk bisnis. Selama empat tahun pertama kepemimpinannya, Watson sukses meningkatkan pendapatan hingga lebih dari dua kali lipat dan mencapai $9 juta. Ia juga sukses mengembangkan sayap ke Eropa, Amerika Selatan, Asia, dan Australia. Pada 14 Februari 1924, CTR berganti nama menjadi International Business Machines Corporation (IBM). -

USEF) Intermediaire I Dressage National Championship and Yang Showing Garden’S Sam in the USEF Children Dressage

USET Foundation PHILANTHROPIC PARTNER OF US EQUESTRIAN NEWS VOLUME 18, ISSUE 3 • FALL 2019 THE 2020 TOKYO OLYMPIC GAMES WILL BRING AKIKO YAMAZAKI FULL CIRCLE The ardent supporter of U.S. Dressage is looking forward to seeing her passion merge with her heritage. BY MOLLY SORGE Attending the 2020 Tokyo Olympic Games will be an emotional experience for Akiko Yamazaki – and not only because she hopes her horse, Suppenkasper, will be named to the U.S. Dressage Team with rider Steffen Peters. When Yamazaki sits down in the stands at Equestrian Park at Baji Koen, she’ll be sitting next to her mother, Michiko, who is the person who inspired her love of horses, and her two daughters, who share their passion for riding. My mom attended the Tokyo Olympic Games in 1964 as a spectator,” Yamazaki said. “Now we’ll go to watch the 2020 Tokyo Olympic Games at the“ same venue, and hopefully we’ll be watching one of our horses compete. My mother is going to be 79 years old, and she’s really looking forward to going back and watching the Games in Tokyo. We are three generations of riders. It’s coming full circle.” For Yamazaki, who sits on the Board of Trustees and serves as the Secretary of the U.S. Equestrian Team (USET) Foundation, that feeling of legacy is a big part of why she loves equestrian sport so much. Her mother introduced her to riding when she was young, and now Yamazaki’s daughters have not only grown up immersed in the sport but have also developed their own passion for riding. -

Getting Started with Rational DOORS Release 9.2 Before Using This Information, Be Sure to Read the General Information Under the "Notices" Chapter on Page 27

IBM Rational DOORS Getting Started with Rational DOORS Release 9.2 Before using this information, be sure to read the general information under the "Notices" chapter on page 27. This edition applies to IBM Rational DOORS, VERSION 9.2, and to all subsequent releases and modifications until otherwise indicated in new editions. © Copyright IBM Corporation 1993, 2010 US Government Users Restricted Rights—Use, duplication or disclosure restricted by GSA ADP Schedule Contract with IBM Corp. Table of contents Chapter 1: About this manual 1 Typographical Conventions. 1 Related Documentation . 1 Chapter 2: Introducing Rational DOORS 3 About Rational DOORS . 3 About requirements . 4 About modules. 4 About objects and attributes . 5 Object Heading and Object Text attributes. 6 About traceability . 6 About views . 7 About folders and projects . 7 About tracking changes . 8 About baselines . 9 About edit modes. 9 About the Change Proposal System . 10 About partitions . 11 About user types . 11 About discussions . 12 Chapter 3: Quick tour 13 About this tour. 13 Getting ready to start the tour. 13 Install and run the Example Database . 13 Editing a module . 15 Changing your view . 17 Making a link . 18 Creating an attribute. 20 Sorting and filtering the data . 21 Getting Started with Rational DOORS iii Table of contents Finishing the tour . 21 Chapter 4: Contacting support 23 Contacting IBM Rational Software Support . 23 Prerequisites . 23 Submitting problems. 24 Other information. 26 Chapter 5: Notices 27 Trademarks . 29 Index 31 iv Getting Started with Rational DOORS 1 About this manual Welcome to IBM® Rational® DOORS® 9.2, the world’s leading requirements management application. -

Jim Mcnerney

Biography The Boeing Company 100 N. Riverside Plaza, MC 5003-5495 Chicago, IL 60606 www.boeing.com W. JAMES MCNERNEY, JR. Chairman and Chief Executive Officer The Boeing Company W. James (Jim) McNerney, Jr., is chairman of the board and chief executive officer of The Boeing Company. McNerney, 64, oversees the strategic direction of the Chicago-based, $86.6 billion aerospace company. With more than 168,000 employees across the United States and in more than 65 countries, Boeing is the world's largest aerospace company and a top U.S. exporter. It is the leading manufacturer of commercial airplanes, military aircraft, and defense, space and security systems; it supports airlines and U.S. and allied government customers in more than 150 nations. McNerney joined Boeing as chairman, president and CEO on July 1, 2005. Before that, he served as chairman of the board and CEO of 3M, then a $20 billion global technology company with leading positions in electronics, telecommunications, industrial, consumer and office products, health care, safety and other businesses. He joined 3M in 2000 after 19 years at the General Electric Company. McNerney joined General Electric in 1982. There, he held top executive positions including president and CEO of GE Aircraft Engines and GE Lighting; president of GE Asia-Pacific; president and CEO of GE Electrical Distribution and Control; executive vice president of GE Capital, one of the world's largest financial service companies; and president, GE Information Services. Prior to joining GE, McNerney worked at Procter & Gamble and McKinsey & Co., Inc. By appointment of U.S. -

A Foundation for the Future

A FOUNDATION FOR THE FUTURE INVESTORS REPORT 2012–13 NORTHWESTERN UNIVERSITY Dear alumni and friends, As much as this is an Investors Report, it is also living proof that a passion for collaboration continues to define the Kellogg community. Your collective support has powered the forward movement of our ambitious strategic plan, fueled development of our cutting-edge curriculum, enabled our global thought leadership, and helped us attract the highest caliber of students and faculty—all key to solidifying our reputation among the world’s elite business schools. This year, you also helped set a new record for alumni support of Kellogg. Our applications and admissions numbers are up dramatically. We have outpaced our peer schools in career placements for new graduates. And we have broken ground on our new global hub. Your unwavering commitment to everything that Kellogg stands for helps make all that possible. Your continuing support keeps us on our trajectory to transform business education and practice to meet the challenges of the new economy. Thank you for investing in Kellogg today and securing the future for generations of courageous leaders to come. All the best, Sally Blount ’92, Dean 4 KELLOGG.NORTHWESTERN.EDU/INVEST contentS 6 Transforming Together 8 Early Investors 10 Kellogg Leadership Circle 13 Kellogg Investors Leaders Partners Innovators Activators Catalysts who gave $1,000 to $2,499 who gave up to $1,000 99 Corporate Affiliates 101 Kellogg Investors by Class Year 1929 1949 1962 1975 1988 2001 1934 1950 1963 1976 1989 2002 -

Special Issue: the Drucker Centennial

The Journal of The Human Resource Planning Society Volume 32 Issue 4 2009 People &Strategy Special Issue: The Drucker Centennial PersPectives What Drucker Means Around the World Richard Straub/Guido Stein/Thomas Sattelberger/Chuck Ueno/Vaibhav Manek/Shuming Zhao/Danica Purg/ Bob Buford/Rick Wartzman NeW thiNkiNg from drucker’s legacy Design Your Governance Model to Make the Matrix Work Gregory Kesler/Michael H. Schuster Creating a Culture of Agile Leaders: A Developmental Approach Bill Joiner Developing World Class Leaders: The Rohm and Haas Story Rajiv L. Gupta/Karol M. Wasylyshyn Knowledge Management: A Glass Half Full Mary Key/Holly Tompson/Joseph McCann Turning ‘Survive’ into ‘Thrive’: Managing Survivor Engagement in a Downsized Organization Brenda Kowske/Kyle Lundby/Rena Rasch Which is More Important for Successful Change: Commitment to the Organization or the Initiative? Chris Harris/Doyle Lucas Lost in a Time Warp: How Age Stereotypes Impact Older Baby Boomers Who Still Want to Work Ernie Stark Give your Hr team tHe edGe tHey need. Become an HrPS enterPriSe memBer. The Human Resource Planning Society (HRPS) is a strategically focused, “ B e i n g an enterprise member of HrPS groundbreaking network of thousands of HR thought leaders and keeps our Hr professionals up to date on innovators representing the world’s most prominent organizations. In global Hr issues, strategies, trends and practices. the conferences provide insight addition to individual membership, HRPS offers Enterprise Membership, and information about the challenges which allows your entire HR team to take advantage of enhanced benefits, facing Hr today as well as a preview of access to a wealth of additional resources and deep discounts on a variety what we will face in the future. -

A Model Driven Approach for Service Based System Design Using Interaction Templates

Toni Reichelt A Model Driven Approach for Service Based System Design Using Interaction Templates Wissenschaftliche Schriftenreihe EINGEBETTETE, SELBSTORGANISIERENDE SYSTEME Band 10 Prof. Dr. Wolfram Hardt (Hrsg.) Toni Reichelt A Model Driven Approach for Service Based System Design Using Interaction Templates Chemnitz University Press 2012 Impressum Bibliografische Information der Deutschen Nationalbibliothek Die Deutsche Nationalbibliothek verzeichnet diese Publikation in der Deutschen Nationalbibliografie; detaillierte bibliografische Angaben sind im Internet über http://dnb.d-nb.de abrufbar. Zugl.: Chemnitz, Techn. Univ., Diss., 2012 Technische Universität Chemnitz/Universitätsbibliothek Universitätsverlag Chemnitz 09107 Chemnitz http://www.bibliothek.tu-chemnitz.de/UniVerlag/ Herstellung und Auslieferung Verlagshaus Monsenstein und Vannerdat OHG Am Hawerkamp 31 48155 Münster http://www.mv-verlag.de ISBN 978-3-941003-60-6 URL: http://nbn-resolving.de/urn:nbn:de:bsz:ch1-qucosa-85986 Preface to the scientific series “Eingebettete, selbstorganisierende Systeme” The tenth volume of the scientific series Eingebettete, selbstorganisierende Systeme (Em- bedded, self-organised systems) devotes itself to the model driven design of service-oriented systems. Fields of application for such systems, amongst others, range from large scale, distributed enterprise solutions down to modularised embedded systems. The presented work was moti- vated by the complex design process of avionics for unmanned systems, where the increased demand for enhanced system autonomy implies high levels of system collaboration and infor- mation exchange. For such system designs a clear separation between the application logic implemented by system components, the means of interaction between them and finally the realisation of such communication on target platforms is essential. In particular, this sep- aration leads to simplification of the complex design processes and increases the individual components’ re-use potential.