A Theory of Repurchase Agreements, Collateral

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Line of Credit Promissory Note

LINE OF CREDIT PROMISSORY NOTE $500.000.00 April 17. 2018 Loan Amount Date FOR VALUE RECEIVED, the undersigned makers PFMAN LLC, a Florida limited liability company and ORBITAL TECHNOLOGIES, INC., a Delaware corporation (collectively, the "Maker") jointly and severally hereby promise to pay to the order of HARDEE COUNTY INDUSTRIAL DEVELOPMENT AUTHORITY (the "Lender"), at its offices located at 107 East Main Street, Wauchula, Florida 33873, or at such other place as the holder hereof may from time to time designate in writing, in collected funds or U.S. legal tender, the sum specified in this Promissory Note (the "Note"), the principal sum of FIVE HUNDRED THOUSAND DOLLARS ($500,000.00), or such lesser amount outstanding at maturity (the "Principal"), together with interest accrued from the date hereof on the unpaid principal balance at the interest rate or rates per annum set forth herein under Section 3, and any other amounts due in accordance with the terms specified in this Note. The undersigned Maker also promises to pay (i) late charges, fees, and other charges as specified herein, and (ii) the cost of all fees paid or to be paid to public officials for recording, perfecting, maintaining, canceling and/or releasing any security interest in any Collateral securing this Note. This Note is referred to in, and was executed and delivered in connection with, a certain Security Agreement, dated April 17, 2018, by and among the Maker and Lender (the "Security Agreement"). Maker covenants and agrees as follows: 1. PRINCIPAL. This Note evidences a revolving line ofcredit. Prior to an Event ofDefault (as defined in Section 9), Maker may borrow, repay, and reborrow hereunder, provided, however, the total outstanding principal balance shall not exceed FIVE HUNDRED THOUSAND DOLLARS ($500.000.00) at any time. -

Agriculture Real Estate First Mortgage and Participation

AGRICULTURAL REAL ESTATE FIRST MORTGAGE LOANS – Whole Loans and Participations This Eligibility Checklist assists pledgors who have executed the appropriate Advances, Pledge and Security Agreement in determining eligibility of loans for pledging to FHLB Des Moines. A “NO” answer indicates the loan is not eligible under FHLB Des Moines guidelines. GE GENERAL ELIGIBILITY YES NO The requirements of this checklist are specific to the collateral type shown above. Certain Eligible Member Collateral requirements are common to ALL pledged loan collateral as identified in Collateral Procedures. The preparer should have familiarity prior to proceeding with eligibility determination via this checklist. For ease, a summation of these requirements is provided: General Eligibility Checklist. PN PROMISSORY NOTE YES NO 1. Note Execution: Executed with proper signatories and capacities as authorized by any applicable borrowing resolution/other authority. 2. Loan Terms: Matures and requires principal & interest payments to amortize the loan within a 30 year term or less (measured from first payment date following origination or last modification). 3. Disbursement: Loan is fully disbursed and non-revolving. 4. Whole Loans and Participations: Loans must be reported properly based on ownership of the loan. All Participation loans must meet the requirements found in the Participation Loan Guidelines. (Note: 100% participations purchased are not eligible). • Whole Loan: The loan is not participated and is reported in type code 1407. • Retained Participation: The loan is reported in type code 1472. • Purchased Participation: The loan is reported in type code 1572. SI SECURITY INSTRUMENT: Mortgage (or Deed of Trust) and/or Security Agreement YES NO 1. Security Instrument Existence: Note is secured with an unexpired mortgage recorded in the proper jurisdiction. -

1-4 FAMILY RESIDENTIAL FIRST MORTGAGE LOANS – Whole

1-4 FAMILY RESIDENTIAL FIRST MORTGAGE LOANS – Whole Loans and Participations This Eligibility Checklist assists pledgors who have executed the appropriate Advances, Pledge and Security Agreement in determining eligibility of loans for pledging to FHLB Des Moines. A “NO” answer indicates the loan is not eligible under FHLB Des Moines guidelines. GE GENERAL ELIGIBILITY YES NO The requirements of this checklist are specific to the collateral type shown above. Certain Eligible Member Collateral requirements are common to ALL pledged loan collateral as identified in Collateral Procedures. The preparer should have familiarity prior to proceeding with eligibility determination via this checklist. For ease, a summation of these requirements is provided: General Eligibility Checklist. PN PROMISSORY NOTE YES NO 1. Note Execution: Executed with proper signatories and capacities as authorized by any applicable borrowing resolution/other authority. 2. Loan Terms: Matures and requires principal & interest payments to amortize the loan within a 40 year term or less (measured from first payment date following origination or last modification). 3. Disbursement: Loan is fully disbursed and non-revolving. 4. Whole Loans and Participations: Loans must be reported properly based on ownership of the loan. See the Type Code Reporting Instructions section at the end of this checklist for proper type code reporting. • For participation loans, the loan meets the eligibility requirements found in the Participation Loan Guidelines. (Note: 100% participations purchased are not eligible). SI SECURITY INSTRUMENT: Mortgage (or Deed of Trust) and/or Security Agreement YES NO 1. Security Instrument Existence: Note is secured with an unexpired mortgage recorded in the proper jurisdiction. -

A Theory of Repurchase Agreements, Collateral Re-Use, and Repo Intermediation∗

A Theory of Repurchase Agreements, Collateral Re-use, and Repo Intermediation∗ Piero Gottardi Vincent Maurin European University Institute Stockholm School of Economics Cyril Monnet University of Bern, SZ Gerzensee This version: November, 2017 Abstract We show that repurchase agreements (repos) arise as the instrument of choice to borrow in a competitive model with limited commitment. The repo contract traded in equilibrium provides insurance against fluctuations in the asset price in states where collateral value is high and maximizes borrowing capacity when it is low. Haircuts increase both with counterparty risk and asset risk. In equilibrium, lenders choose to re-use collateral. This increases the circulation of the asset and generates a \collateral multiplier" effect. Finally, we show that intermediation by dealers may endogenously arise in equilibrium, with chains of repos among traders. ∗We thank audiences at the Third African Search & Matching Workshop, Bank of Canada, EBI Oslo, SED 2016, EFA Oslo 2016, London FTG 2016 Meeting, the 2015 Money, Banking, and Liquidity Summer Workshop at the St Louis Fed, The Philadelphia Fed, the Sveriges Riksbank, Surrey, Essex, CORE and University of Roma Tor Vergata for very helpful comments. 1 1 Introduction Gorton and Metrick(2012) argue that the financial panic of 2007-08 started with a run on the market for repurchase agreements (repos). Lenders drastically increased the haircut requested for some types of collateral, or stopped lending altogether. This view was very influential in shaping our understanding of the crisis.1 Many attempts to understand repos more deeply as well as calls for regulation quickly followed.2 The very idea that a run on repos could lead to a financial market meltdown speaks to their importance for money markets. -

Broker-Dealer Use of “Idle” Customer Assets: Customer Protection with Sweep Programs and Securities Lending

TEPE – FINAL BROKER-DEALER USE OF “IDLE” CUSTOMER ASSETS: CUSTOMER PROTECTION WITH SWEEP PROGRAMS AND SECURITIES LENDING George Tepe∗ Equity investors, whether hedge funds or retail investors, must trade stocks through broker-dealers, and when these investors are not actively trading, their securities and uninvested cash remain with their broker-dealer. What broker-dealers do with these “idle” customer assets is a vast and largely unexamined business that is a key source of revenue for broker-dealers. This Note provides the first comprehensive examination of the trade-offs in regulating broker-dealer use of idle customer assets through case studies of broker-dealer sweeps of uninvested customer cash, broker- dealer lending of customer margin securities, and the effect of securities lending on customers’ shareholder votes. On one hand, broker-dealer use of idle customer assets potentially increases agency costs and systemic risk by increasing broker-dealer interconnectedness and allowing broker-dealers to profit off customer assets. On the other hand, proper use of idle assets can generate positive outcomes for customers through higher returns and positive social benefits for the general market. This Note proposes and examines potential reforms like increased disclosure and ∗ J.D. Candidate 2017, Columbia Law School; B.A. 2014, Amherst College. The author would like to thank Professor Gabriel Rauterberg for his invaluable guidance and feedback. He would also like to thank the Office of Financial Responsibility in the Division of Trading and Markets at the Securities and Exchange Commission, and especially Mark Attar, for the internship and education that inspired this Note. Finally, the author is grateful to Chloe McKenzie for her unwavering support and the editorial staff of the Columbia Business Law Review for their assistance in preparing this Note for Publication. -

Shadow Banking and New Lending Channels

377 11. S HADOW B ANKING AND N EW L ENDING CHANNELS – P AST AND F UTURE Patricia Jackson 1 11.1. I NTRODUCTION The history of shadow banking is one of shifts in the type of institution involved, and rate growth, but there are two common elements across the decades. Shadow banking has caused or been at the heart of various financial crises in different periods and one important factor behind its growth has been the style and extent of bank regulation. In the 1970s and 1980s the growth in shadow banking (then called secondary banking or non-bank banking) tended to be related to property lending and, even though it was not complex, the crises were sufficiently severe to require central bank/ government intervention. The 1990s steadily saw more and more complex structures being used in shadow banking peaking in 2007/8 and being central to the financial crisis. The Financial Stability Board (FSB) estimates that the size of the global shadow banking system grew from USD 26 trillion in 2002 to USD 62 trillion in 2007 (FSB (2012a)). One question is what lies ahead. The Basel III capital and liquidity buffers and wider uncertainty regarding future regulatory change have led to deleveraging and this in turn is leading shadow banking again to grow. The FSB (2012a) indicates that after falling slightly in 2008 shadow banking assets have now grown above 2007 levels 2 but the market is focused more on traditional banking products than was the case pre-crisis. There has also been a proliferation of different types of lending channel. -

Rehypothecation and Securities Commingling in the United States and the United Kingdom

2009 STANDARDIZATION OF SECURITIES REGULATION 253 STANDARDIZATION OF SECURITIES REGULATION: REHYPOTHECATION AND SECURITIES COMMINGLING IN THE UNITED STATES AND THE UNITED KINGDOM MARIYA DERYUGINA∗ I. Introduction While securities laws and regulations in the United States strictly prohibit United States brokers and dealers from rehypothecating and commingling their clients’ securities in most circumstances, United Kingdom regulations to a much larger extent permit both rehypothe- cation and the commingling of broker assets with customer assets. The asymmetry in the legal rules governing transactions in these two large and interrelated financial markets has led to customer confusion regarding the ownership or title status of their securities, misunder- standing regarding the customers’ legal rights in any given trans- action or investment, and an increase in the transaction costs associ- ated with obtaining prime brokerage services. Industry participants largely ignored, failed to notice or failed to consider the full implications of this large regulatory discrepancy until the collapse of Lehman Brothers Holdings, Inc. (“Lehman”) in the United States and the subsequent collapse of its affiliate, Lehman Brothers International (Europe) in the United Kingdom. While the United States bankruptcy of Lehman proceeded relatively smoothly, United Kingdom rehypothecation and asset commingling rules stifled the resolution process. Hedge funds and other clients of the United Kingdom affiliate of Lehman were unable to withdraw or reclaim the assets they had placed with the broker, leading to massive market losses and, in some cases, to the failure of hedge fund businesses. The Lehman failure highlighted the riskiness of allowing rehypothecation and the commingling of client assets in the United Kingdom and the benefits of prohibiting such practices. -

Comment Letter on File No. S7-22-06

1120 Connecticut Avenue, NW Washington, DC 20036 202-663-5326 Fax: 202-828-5047 www.aba.com Sarah A. Miller General Counsel September 8, 2008 Florence E. Harmon Jennifer J. Johnson Acting Secretary Secretary Securities and Exchange Commission Board of Governors of the 100 F Street, N.E. Federal Reserve System Washington, D.C. 20549-1090 20th Street and Constitution Avenue, N.W. Washington, D.C. 20551 Re: Status of Bank Repurchase and Reverse Repurchase Agreement Activities Involving Non-Exempt Securities under the Securities Exchange Act of 1934, SEC Release Nos. 34-56501 and 34-56502; Regulation R; Docket No. R-1274 Ladies and Gentlemen: The ABA Securities Association (“ABASA”)1 appreciates the opportunity to submit this letter in response to the request by the Securities and Exchange Commission (“SEC”) and the Board of Governors of the Federal Reserve System (the “Board”) (hereinafter referred collectively to as the “Agencies”) for information on the nature and extent of bank repurchase and reverse repurchase (“repo”) agreement activities involving non-exempt securities. The Agencies’ request for information was made in the context of their joint adoption of Regulation R, which implements the so-called “push- out” provisions under Section 3(a)(4) of the Securities Exchange Act of 1934 (the “Exchange Act”), as amended by the Gramm-Leach-Bliley Act (“GLBA”).2 We have provided responses to the Agencies’ specific requests for information in the attached annex. ABASA urges the Agencies to clarify 1 ABASA is a separately chartered affiliate of the American Bankers Association (“ABA”) representing those holding company members of the ABA actively engaged in capital markets, investment banking, and broker-dealer activities. -

A Theory of Repurchase Agreements, Collateral Re-Use, and Repo Intermediation”

FINANCE RESEARCH SEMINAR SUPPORTED BY UNIGESTION “A Theory of Repurchase Agreements, Collateral Re-use, and Repo Intermediation” Prof. Piero GOTTARDI European University Institute Abstract This paper characterizes repurchase agreements (repos) as equilibrium contracts starting from first principles. We show that a repo allows the borrower to augment its consumption today while hedging both agents against future market price risk. As a result, safer assets will command a lower haircut and a higher liquidity premium relative to riskier assets. Haircuts may also be negative. When lenders can re-use the asset they receive in a repo, we show that there exists a collateral multiplier effect and borrowing increases. In addition, with collateral re-use, lenders might also re-pledge the asset to third parties. In the model, intermediation arises as an equilibrium choice of traders and trustworthy agents play a role as intermediary. These findings are helpful to rationalize chains of trades observed on the repo market. Friday, September 23, 2016, 10:30-12:00 Room 126, Extranef building at the University of Lausanne A Theory of Repurchase Agreements, Collateral Re-use, and Repo Intermediation∗ Piero Gottardi Vincent Maurin European University Institute European University Institute Cyril Monnet University of Bern, SZ Gerzensee & Swiss National Bank This version: September, 2016 [Preliminary and Incomplete] Abstract This paper characterizes repurchase agreements (repos) as equilibrium contracts starting from first principles. We show that a repo allows the bor- rower to augment its consumption today while hedging both agents againt future market price risk. As a result, safer assets will command a lower hair- cut and a higher liquidity premium relative to riskier assets. -

Section 3.2 — Loans

LOANS Section 3.2 INTRODUCTION.............................................................. 3 Credit Card-related Merchant Activities ...................... 33 LOAN ADMINISTRATION ............................................. 3 OTHER CREDIT ISSUES .............................................. 34 Lending Policies ............................................................. 3 Appraisals .................................................................... 34 Loan Review Systems .................................................... 4 Valuation of Troubled Income-Producing Properties Credit Risk Rating or Grading Systems ..................... 4 ................................................................................. 35 Loan Review System Elements .................................. 5 Appraisal Regulation ............................................... 35 Current Expected Credit Losses (CECL) ....................... 6 Interagency Appraisal and Evaluation Guidelines ... 37 Allowance for Loan and Lease Losses (ALLL) ............. 6 Examination Treatment ........................................... 41 Responsibility of the Board and Management ........... 7 Loan Participations ...................................................... 41 Factors to Consider in Estimating Credit Losses........ 7 Accounting .............................................................. 41 Examiner Responsibilities .......................................... 8 Right to Repurchase ................................................. 42 Regulatory Reporting of the -

Global Securities Financing Data Collection and Aggregation

Global Securities Financing Data Collection and Aggregation Frequently Asked Questions 12 April 2021 The Financial Stability Board (FSB) coordinates at the international level the work of national financial authorities and international standard-setting bodies in order to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies. Its mandate is set out in the FSB Charter, which governs the policymaking and related activities of the FSB. These activities, including any decisions reached in their context, shall not be binding or give rise to any legal rights or obligations. Contact the Financial Stability Board Sign up for e-mail alerts: www.fsb.org/emailalert Follow the FSB on Twitter: @FinStbBoard E-mail the FSB at: [email protected] Copyright © 2021 Financial Stability Board. Please refer to the terms and conditions Table of Contents Background ........................................................................................................................... 1 Abbreviations ......................................................................................................................... 2 Frequently Asked Questions .................................................................................................. 3 Q1. How should collateral residual maturity (i.e. Data Elements 4.12, 6.12 and 9.9 in the SFT Data Standards be reported in the case of securities with embedded options? ............. 3 Q2. Should securities lending provided as an agent by a Central Securities Depository -

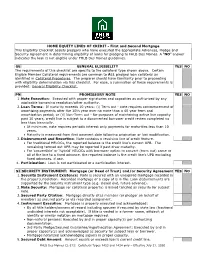

HELOC First and Second Mortgage Checklist

HOME EQUITY LINES OF CREDIT - First and Second Mortgage This Eligibility Checklist assists pledgors who have executed the appropriate Advances, Pledge and Security Agreement in determining eligibility of loans for pledging to FHLB Des Moines. A “NO” answer indicates the loan is not eligible under FHLB Des Moines guidelines. GE GENERAL ELIGIBILITY YES NO The requirements of this checklist are specific to the collateral type shown above. Certain Eligible Member Collateral requirements are common to ALL pledged loan collateral as identified in Collateral Procedures. The preparer should have familiarity prior to proceeding with eligibility determination via this checklist. For ease, a summation of these requirements is provided: General Eligibility Checklist. PN PROMISSORY NOTE YES NO 1. Note Execution: Executed with proper signatories and capacities as authorized by any applicable borrowing resolution/other authority. 2. Loan Terms: If maturity exceeds 10 years: (i) Term out - note requires commencement of amortizing payments after the 10th year over no more than a 40 year term and amortization period; or (ii) Non-Term out - for purposes of maintaining active line capacity past 10 years, credit line is subject to a documented borrower credit review completed no less than biennially. • At minimum, note requires periodic interest only payments for maturities less than 10 years. • Maturity is measured from first payment date following origination or last modification. 3. Disbursement and Reporting: Note contains a revolving line of credit feature. • For traditional HELOCs, the reported balance is the credit line's current UPB. The remaining termed out UPB may be reported if past draw maturity. • For ‘convertible’ or ‘hybrid’ HELOCs with borrower option to convert (term out) some or all of the line to a fixed advance, the reported balance is the credit line's UPB excluding fixed advances, if any.