Woolworths: Calling Drinks on Endeavour

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Procurar Conviction Australian Equity Portfolio

Procurar Conviction Australian Equity Portfolio Portfolio performance – March 2021 Cumulative performance 1 mth 3 mth 6 mth 1 yr 2 yr S.I. (%) (%) (%) (%) (% pa) (% pa) Portfolio Total 3.2 5.8 22.5 43.1 12.0 8.9 Return Benchmark* 2.3 4.2 18.5 38.3 8.7 8.2 Excess Return 0.9 1.6 4.0 4.8 3.3 0.7 Past performance is not a reliable indicator of future performance. Performance is calculated before taxes and other fees such as model management and platform fees and are net of underlying investment management fees. For full details of fees, please refer to the relevant platform provider. Performance is notional in nature and the actual performance of individual portfolios may differ to the performance of the Managed Portfolios. Inception date 1st March 2018. *Benchmark is the S&P/ASX 200 TR Index AUD. Market review The Australian equity market experienced another positive quarter Performance contributors of performance to the end of March, delivering a 4.1% return as Top 5 Contributors to Performance (12m) % measured by the S&P/ASX 300 Accumulation Index. Low levels of community transmission and the rollout of the COVID-19 vaccine Nine Entertainment Co 2.43 program have delivered a boost of optimism for investors, Santos 1.52 particularly sectors directly linked to the re-opening of the James Hardie 1.43 economy, in particular consumer discretionary, industrial and Xero Limited 1.36 resources. Seven Group 1.32 Top 5 Detractors from Performance (12m) % Global equities gained over the quarter, with the MSCI World ex Australia Index AUD up 6.0%. -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Woolworths Group Limited ASX Code: WOW Price: $39.29 12 Mth Target Price: $40.60 Rating: Neutral

GICS - Food/Staples Woolworths Group Limited ASX Code: WOW Price: $39.29 12 Mth Target Price: $40.60 Rating: Neutral Business Summary Snapshot Woolworths (WOW) is a retail operator in Australia and New Zealand, with Date 26 September 2021 3,357 stores and approximately 215,000 employees. Its business division Market Cap. $49,806m Shares on issue 1,267.7m comprises of Australian Food, New Zealand Food and Big W. 12 Month High $42.66 12 Month Low Australian Food: This division is involved in procurement of food and related $31.80 products for resale and provision of services to customers in Australia. This Rating division is divided in three sections woolsworth supermarkets, Everyday Rating Neutral reward, and Financial services and insurance. This section includes 12 Mth Target Price $40.60 Supermarket chain operating 995 stores across Australia, Woolworths Capital Gain 3.9% Rewards loyalty program and financial products tailored to Woolworths Gross Yield 4.1% Implied Total Return customers. 8.1% New Zealand Food: This division is involved in procurement of food and Investment Fundamentals drinks for resale to customers in New Zealand. This division own 181 FYE 30 Jun 2021A 2022F 2023F 2024F Countdown stores and has over 18,000 team members and more than Profit $m 1,972.0 1,735.0 1,893.0 1,995.0 20,000 product lines. Profit (norm)* $m 1,972.0 1,735.0 1,893.0 1,995.0 Big W: Big W brand is involved in procurement of discount general EPS* ¢ 156.0 141.0 155.0 163.0 merchandise products for resale to customers in Australia. -

Full Year Profit Announcement

F20 Final Profit and Dividend Announcement For the 52 weeks ended 28 June 2020 Bringing our Purpose to life and creating a COVIDSafe environment F20 Group highlights1,2,3 Group Online Group Group Dividend sales sales EBIT NPAT per share $63,675 M $3,523 M $3,219M $1,602M 94 ¢ % % % 5 8.1 41.8% (0.4) (1.2) (7.8)% Woolworths Group CEO, Brad Banducci, said: “At our half-year results in February, we spoke about the many challenges the communities we operate in had faced including drought, bushfires, the White Island tragedy in New Zealand and unrest in Hong Kong. At the time, no one could have imagined how the rest of the year would unfold with the devastating impact of COVID-19. Our main priority for F21 is making COVIDSafe a part of everything we do. I again want to recognise the way our team has continued to respond to the ongoing challenges, and I continue to be inspired by our team's collective commitment to do the right thing. “COVID-19 had a material impact on the Group’s financial performance for the year. After strong first half Group EBIT1 growth of 11.4%, EBIT growth in H2 was distorted by COVID. The closure of Hotels for much of the last four months of the financial year led to a material decline in its H2 EBIT compared to the prior year. However, the impact of the closures was partially offset by strong sales-driven EBIT growth across our retail businesses, despite materially higher customer and team safety costs. -

Half-Year Profit Announcement

26 February 2020 ASX Market Announcements Office Australian Securities Exchange 20 Bridge Street Sydney NSW 2000 HALF-YEAR RESULTS ANNOUNCEMENT Attached for release to the market is the Half-Year Results Announcement for the period ended 5 January 2020. Marcin Firek Company Secretary Woolworths Group Limited For further information contact: Media: Woolworths Group Press Office: +61 2 8885 1033 [email protected] Investors and Analysts: Paul van Meurs, Head of Investor Relations: +61 407 521 651 Woolworths Group Limited ABN 88 000 014 675 1 Woolworths Way, Bella Vista NSW 2153 F20 Half-Year Profit and Dividend Announcement For the 27 weeks ended 5 January 2020 Sales from Group online sales Group continuing operations $1,650M $32,410M highlights 31.6% 6.0% EBIT from NPAT from H20 dividend per share continuing operations1 continuing operations1 $1,893M $979M 46¢ 2 2 11.4% 15.7% 2.2% Progress on key priorities: More to do: • Strong sales and EBIT growth in the half across all • Finalise review of salary shortfalls and fully businesses recompense impacted salaried store team members • Progress on digital and data; X businesses • Renewed customer and team focus in Australian continuing to scale Food given busy change agenda in H1 • Endeavour Group restructure approved; Chairman, • Complete separation of Endeavour Group CEO and COO/CFO elects appointed • Fully ramp up MSRDC and realise projected • Improved financial performance from BIG W with benefits; embed Customer Operating Model; first H1 profit since F16 deliver first -

South Australian Petroleum Prospectivity Summary

South Australian petroleum prospectivity summary NAPE 2021 1. South Australian Petroleum Review (PESA News, second quarter 2021 https://pesa.com.au/pesa- news-magazine/ ) 2. State of Play in SA, Elinor Alexander. Presented at PESA Deal Day on 14 June 2021 TECH TALK TECH TALK ") Marla Moomba South Australian ") ") Petroleum Review Coober Pedy (May–2021) INTRODUCTION Acreage Releases: Competitive acreage process (Figure 2). PEL 680 has been releases have been used successfully granted to Beach Energy and Cooper The Energy Resources Division in by the Department to manage highly Energy in the Otway Basin (formerly the South Australian Department for prospective Cooper Basin acreage OT2019-B block). Energy and Mining is the lead agency since 1998. The expiry of long term ") Ceduna for petroleum, geothermal and carbon exploration licenses (PELs 5 and 6) Petroleum Retention Licences: An ") Port capture and storage activities in the enabled the most significant structured initiative in 2013 to increase the extent Augusta state. It has responsibility for the release of onshore Australian acreage in of retention and production licences generation of royalty income, economic the industry’s history, and has generated has been very successful resulting in ") Port Bonython development, wealth and jobs, public (in today’s terms): a massive increase from 7,645 km2 in ") Port safety and the minimisation of impacts 2013, up to the current 17,107 km2 Pirie on the environment through efficient 44 PELs and 5 PELAs and resultant in April 2021. There are currently 210 management of the state's petroleum PPLs and PRLs from 89,100 km2 of petroleum retention licences, with and geothermal rights on behalf of the acreage; almost all of these located over proven people of South Australia. -

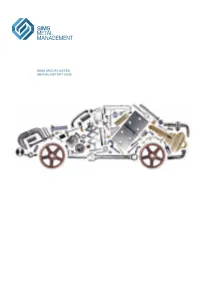

SIMS GROUP LIMITED Annual REPORT 2008 SIM S G R O U P L IM IT E D a N N U a L RE P O R T 2 0

SIMS GROUP LIMITED GROUP SIMS ANN U a L REPORT2008 L ThE average motor vEhIcle SIMS GROUP LIMITED Lasts 13.5 yEars anD comprises annUaL report 2008 approximately 15,000 IndividuaL Parts, Of whIch 80% are potentially recOverable. Approximately 68% Of a vEhIcle’S Parts by weighT aRE steel, followed by plastic (9%) anD nOn ferrous metals (8%), with ThE remaInder rubber, glass anD other materials. www.simsMM.cOM finanCiaL Summary Corporate DireCtory For the year ended 30 June 2008 SeCuritieS exChange LiSting Shareholder enquirieS The Company’s ordinary shares are quoted Enquiries from investors regarding their $7.67 b 38% $433m 81% 306¢ 60% 130¢ 8% on the Australian Securities Exchange under share holdings should be directed to: the ASX Code ‘SGM’. Computershare Investor Services Pty Limited TotaL REvEnue Profit after Tax EaRnIngs per ShaRE DIvidends per Share The Company’s American Depositary Shares Level 3 (ADSs) are quoted on the New York Stock 60 Carrington Street Exchange under the symbol ‘SMS’. The Company Sydney NSW 2000 has a Level II ADS program, and the Depositary Postal Address: is the Bank of New York Mellon Corporation. GPO Box 7045 ADSs trade under cusip number 829160100 Sydney NSW 2001 with each ADS representing one (1) ordinary Telephone: 1300 855 080 share. Further information and investor Facsimile: (02) 8235 8150 enquiries on ADSs may be directed to: Company SeCretarieS $181m 42% 14.6% 22% 10.9% 43% $8.02 72% The Bank of New York Mellon Corporation Frank Moratti Depositary Receipts Division Scott Miller Net caSh flowS Return -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

Full-Year 2020 Results and Briefing

Woodside Petroleum Ltd. ASX Announcement ACN 004 898 962 Mia Yellagonga Thursday, 18 February 2021 11 Mount Street Perth WA 6000 ASX: WPL Australia OTC: WOPEY T +61 8 9348 4000 www.woodside.com.au WOODSIDE FULL-YEAR 2020 RESULTS Woodside delivered record full-year production of 100.3 million barrels of oil equivalent and its best-ever safety performance despite the difficult external conditions in 2020. The reported net loss after tax of US$4,028 million was impacted by the non-cash impairments and onerous contract provision announced in July 2020. Sustained operational excellence helped deliver underlying net profit after tax (NPAT) of US$447 million. The directors have declared a final dividend of US 12 cents per share (cps), bringing the full-year dividend to US 38 cps. The dividend was based on the underlying NPAT of US$447 million. Woodside CEO Peter Coleman said production topped 100 million barrels of oil equivalent for the first time in Woodside’s history. “Strong production outcomes were delivered even though we weathered a direct hit from Tropical Cyclone Damien in February, followed by operational challenges posed by the pandemic. “The outstanding performance of our base business in 2020 was reflected in our low unit production cost of $4.8 per barrel of oil equivalent and the high reliability of our operated LNG facilities. “The decisions to defer the targeted final investment decision (FID) on our Scarborough and Pluto Train 2 developments and the review of the value of our assets were appropriate responses to extraordinary market uncertainty caused by the pandemic and lower oil and gas prices. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

2021 Sustainability Report 3

1 2021 Sustainability Report 3 Contents CEO statement We acknowledge the Traditional Owners It is with great pleasure that I present the 2021 of the land on which our operations exist 3 CEO statement Santos Sustainability Report, demonstrating how and on which we work. We recognise their the principles of sustainability are critical to 4 About us the way that we operate our business and deliver continuing connection to land, waters on our Transform-Build-Grow strategy. and culture. We pay our respects to their 7 Our approach to sustainability Elders past, present and emerging. As Australia’s biggest domestic gas supplier and a leading 7 Our sustainability pillars Asia-Pacific LNG supplier, Santos has improved the lives of people throughout Australia and Asia for more santos.com/sustainability/ Governance and than 50 years. Our values drive everything we do, as we 9 build a better future for our customers, employees and management approaches the communities in which we operate. With significant expansion in recent years, this responsibility grows even As a major fuels producer for the Asia-Pacific region, 12 Structure of this report greater. Santos assets span across Australia, Papua Santos has an important global role to play in a sustainable New Guinea and Timor-Leste, with our focus continuing world. We are committed to realising a global future where 13 Economic sustainability to be on safely providing cleaner, reliable, low-cost temperature increase is limited to below 2 degrees Celsius, fuel products. while reliable and affordable energy continues to power 17 Health and safety domestic and global markets. -

Disclosures on Stakeholder Engagement

CIM1224_ACCAStakeholderReport.qxd:Layout 1 4/4/07 1:18 PM Page 1 Disclosures on stakeholder engagement Reporting Trilogy – Research on sustainability reporting in Australia Part 1 CIM1224_ACCAStakeholderReport.qxd:Layout 1 4/4/07 1:18 PM Page 2 Contents Who is a stakeholder? 4 Methodology 5 Results 7 Conclusions 19 Acknowledgments 20 Appendix 1 – About ACCA and Net Balance Foundation 21 Appendix 2 – Comparisons with other studies on stakeholder engagement 22 Appendix 3 – G3 criteria on stakeholder engagement 23 CIM1224_ACCAStakeholderReport.qxd:Layout 1 4/4/07 1:18 PM Page 3 Foreword This report is the first of three in a series of research projects carried out by ACCA Australia/NZ, in collaboration with Net Balance Foundation Limited, investigating trends in certain selected areas of sustainability reporting and disclosures in Australia. The three topics are: stakeholder engagement, climate change and human capital management. The aim of this trilogy of research projects is to delve deeper into 3 key areas of sustainability reporting by analysing the level and quality of disclosures by large Australian corporates. Stakeholder engagement (the theme of this particular report) has for a long time been recognised as extremely important for corporations, helping to manage (social and environmental) risks, improve reputation, identify new business opportunities by gauging customer/consumer needs and concerns, boost employee morale and input into business strategy and policy. This report summarises the findings of the research, identifying any trends, outlining strengths and weaknesses and making recommendations for the future. The two research papers on climate change disclosures and human capital management disclosures will be published later in 2007.