R Weekly Round up 8 - 12 Feb 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CREST Connect a Newsletter from CRISIL Real Estate Star Ratings (CREST) Volume 23: January - February 2017

CREST Connect A Newsletter from CRISIL Real Estate Star Ratings (CREST) Volume 23: January - February 2017 About CREST Rated project details CREST in media CREST in Surat Page No 1 Page No 2 Page No 5 Page No 18 About CRISIL Real Estate Star Ratings (CREST) • Associated since 1996 with over 700 real estate developers through rating and research assignments • Pioneered the concept of city-specific project ratings in 2010 to increase transparency and help property buyers make informed decisions • Rated over 477 projects of 262 developer groups in 66 cities. Projects cover over 318 million square feet (sq ft) of construction space spanning real estate segments such as residential, plotted development, villas, commercial, retail, townships, hospitality, special economic zone, and mixed-use. CREST Parameters Developers’ track record, with focus on construction, financial strength, Sponsor quality and ability to complete project Financial quality Project viability, developers’ financial strength, and accounting quality Legal quality Land title, sales agreement, and other statutory approvals and clearances Structural quality, project consultants’ track record, execution capability, Construction quality and after-sales service Project concept, process innovation, building design, and construction Innovation technology CREST Success Metrics • High acceptance ratio, and independent evaluation − 83% acceptance in our portfolio • Over 200 clients have provided repeat mandates, which is 83% of our rating portfolio • High sales impetus for rated projects − Sales velocity per month doubled for projects that got rating at early stage of sales • Necessitates high involvement of the rated organisation due to independent third-party evaluation on a regular basis − Reasonable upgrades (about 28%) noticed in ratings portfolio, as projects are under continuous surveillance by a third-party agency − Received investor/customer grievances in less than 3% of the rated project Details of Rated Projects (The following list includes ratings announced in January and February 2017. -

General Awareness–Current Affairs Month of March-2019

GENERAL AWARENESS–CURRENT AFFAIRS MONTH OF MARCH-2019 List of Important Days March 1 - Zero Discrimination Day (Theme – “Act to change laws that Discriminate”) March 4 - National Safety Day (Themes – “Cultivate and Sustain A Safety Culture for Building Nation”) Mar 4-10 - National Safety Week March 7 - Janaushadhi Diwas March 8 - International Women’s Day (Theme – “Think Equal, Build Smart, Innovate for Change”). March 12 - World Day against Cyber Censorship March 12 - 30th anniversary of the World Wide Web (WWW) March 14 - (2nd Thursday of March) World Kidney Day (Theme - “Kidney Health for Everyone Everywhere”) March 14 - Pi Day (Pi's value (3.14)) March 15 - World Consumer Rights Day (In India this day is celebrated as Viswa Upabhokta Adhikar Diwas). (Theme – “Trusted Smart Products”) March 20 - International Day of Happiness. (Theme – “Happier Together”) March 20 - World Day of Theatre for Children and Young People March 20 - World Sparrow Day. (Theme – “I LOVE Sparrows”) March 21 - International Day of Forests. (Theme “Forests and Education”) March 21 - World Poetry Day March 21 - World Down Syndrome Day March 21 - International Day for the Elimination of Racial Discrimination (Theme – “Mitigating and countering rising nationalist populism and extreme supremacist ideologies”) March 21 - World Puppetry Day March 22 - World Water Day (Theme – “Leaving no one behind”) March 23 - World Meteorological Day (Theme – “The Sun, the Earth and the Weather”) March 23 - 88th Shaheed Diwas (Martyr’s Day) March 24 - World Tuberculosis (TB) Day (Theme – “It’s time”) March 25 - International Day of Remembrance of the Victims of Slavery and Transatlantic Slave Trade. (Theme – “Remember Slavery: The Power of the Arts for Justice”) March 26 - Independence Day of Bangladesh March 27 - World Theatre Day (WTD) March 30 - Rajasthan Diwas Reserve Bank of India • The Reserve Bank of India (RBI) has fined Yes Bank ₹1 crore for not complying with its directions about SWIFT, a financial messaging software. -

Bharat Electronics Limited

Bharat Electronics Limited General Knowledge Q : Recently which country has abolished death penalty? (A) Kazakhstan (B) Iran (C) Iraq (D) Bangladesh Correct Answer : A Q : What is the name of the great classical singer who conferred the Padma Vibhushan at the age of 89? (A) Mala Adiga (B) Ghulam Mustafa Khan (C) Sunita Yadav (D) Savita agarwal Correct Answer : B Q : Which Indian messaging app has been officially closed? (A) Liky (B) Hike (C) Tiktok (D) Pub https://www.freshersnow.com/previous-year-question-papers/ Bharat Electronics Limited Correct Answer : B Q : Recently, who has got India's first Covid-19 vaccine? (A) Ramesh Desai (B) Varun Kumar (C) Rajesh Nirala (D) Manish Kumar Correct Answer : D Q : Recently, the famous personality 'Ghulam Mustafa Khan' has passed away, was he? (A) musician (B) Scientist (C) Former Prime Minister (D) Former President Correct Answer : A Q : The Union Cabinet has recently approved the signing of a Memorandum of Understanding between India and which country regarding the participation of 'specified skilled workers'? (A) Russia (B) Japan (C) Germany https://www.freshersnow.com/previous-year-question-papers/ Bharat Electronics Limited (D) Iraq Correct Answer : B Q : Prime Minister Narendra Modi will do groundbreaking of which two projects in Gujarat today through video conferencing? (A) Ahmedabad Metro Rail Project (Phase II), Surat Metro Rail Project (B) Bangalore Metro Rail Project (Phase II), Surat Metro Rail Project (C) Surat Metro Rail Project (Phase II), Surat Metro Rail Project (D) Jaipur Metro -

Metro Transit System: a Case Study of Surat

International Journal of Research in Engineering and Science (IJRES) ISSN (Online): 2320-9364, ISSN (Print): 2320-9356 www.ijres.org Volume 9 Issue 2 ǁ 2021 ǁ PP. 72-76 Metro Transit System: A case study of Surat Tandel Gangeshvari1, Himanshu Padhya2 1Post Graduate Student in Town and Country Planning, Civil Engineering Department, Sarvajanik College of Engineering & Technology, Surat-395001 2P.G. incharge Town and Country Planning, Civil Engineering Department, Sarvajanik College of Engineering & Technology, Surat-395001 Abstract: Surat is Gujarat’s 2nd most popular city, India’s 8th most popular city. It is the 73rd largest urban area in the world. Diamond city Surat’s population grew from 2.8 million to 4.5 million as per 2011 census. Surat is a unique case where population has already exceeded 5 million and shall have approximately 07 million populations by the year 2021. Surat is the most dynamic cities of India having a faster growth rate due to migration from various parts of Gujarat. Due to high population growth rate there is a demand for transport creating pressure on existing transport system. There is more demand of transportation cause congestion on roads due to increasing in private transport. The inter-city traffic volume in Surat necessitated with integrated multi model mass transit rapid system. The paper deals with the “Metro transit system in Surat”. This paper provides information of differentiation of Surat metro transit system and other mass transit system at the area under the metro project. The project scope includes detailed studies related to traffic demand forecasting, location and land planning, transport mode integration and financial analysis. -

Smart Metropolitan Regional Development No Place for In-Migrants

Newsletter presenting ongoing research of groups participating into project to be published as a book year 2018 by Springer-Nature. For private circulation only. Editorial Team ASFA SIDDIQUI ~ GORA MBOUP ~ SUDESHNA GHOSH ~ ELINA ALATALO SmartBulletin Metropolitan Regional Development - Economic and Spatial Design Strategies 3 / 3 Year 2017, 1st of September Presented in this Bulletin AHMEDABAD-GANDHINAGAR ~ BANGALORE ~ CHANDIGARH HONG KONG ~ JAIPUR ~ KOZHIKODE ~ NEW DELHI ~ SURAT By Authors: Jignesh G. Bhatt, Omkar K. Jani, Krupesh A. Chauhan, Leena Garg, Bhasker Vijaykumar Bhatt, T M Vinod Kumar, Mohd. Firoz C., Namratha Radha- krishnan, H. B. Singh, Prabh Bedi, Neha Goel Tripathi, Asfa Siddiqui, Pramod Ku- mar, Ashok Kumar, Amit Chatterjee- Binayak Choudhary, Premjeet Dasgupta, Gaurav Vaidya, Sujata Govada, Timothy Rodgers STUDY AREAS Our research project consist now of 16 Metropolitan Regions INSTITUTIONS There are 25 different institutions involved MILESTONES BULLETIN BOOK Bulletin 1 Pittsburgh, Naples, 15th March, Chapters Draft 1 15th November, 2017 (USA and Eu- Stuttgart 2017 rope) Bulletin 2 Dakar, Conakry, Abuja, 1st June, Chapters Final draft 31st December, 2017 (Africa) Johannesburg, Nairobi 2017 Bulletin 3 Ahmedabad- 1st September, Manuscript Submis- 1st January, 2018 (Asia) Gandhinagar, Banga- 2017 sion to Publisher lore, Chandigarh, Hong Publication of book April, 2018 Kong, Jaipur, Kozhi- kode, New Delhi, Surat Maps on the cover: Jaipur (1993 to 2013). Source: In-house research at IIRS (Thunyaporn Thoopthimthean, Asfa Siddiqui, Sadhana Jain, “Spatio-temporal pattern of Land Surface temperature in Jaipur City”) 2 PROJECT DETAILS Authors and Institutions S No. Study Metropolitan Countries Authors Institutions Regions 1. Dakar Senegal Dr.Gora Mboup, Global Observatory linking Research to Ac- tion (GORA), New York, USA Dr. -

National Infrastructure Pipeline

National Infrastructure Pipeline Report of the Task Force Department of Economic Affairs Ministry of Finance Government of India Volume II 1 2 Contents Infrastructure Progress 20 Sector Progress, Deficits and Challenges, Vision and Reforms 23 General Reforms 174 Financial Sector Reforms 188 Infrastructure Financing 206 Business Models 230 Financing the NIP 244 Way Forward 248 Annexure 254 3 List of Figures Figure 1 Year-wise investment trend in infrastructure (Rs lakh crore, FY13-17, FY 18E and FY 19E) 21 Figure 2 Share of infrastructure investment by the Centre, states and private sector 21 Figure 3 Power sector investment (Rs lakh crore) and share in total infrastructure investment (%) 24 Figure 4 Trends in power generation capacity (GW) and per capita electricity consumption in India (kWh) 25 Figure 5 Trend in power transmission lines in India (ckm) 25 Figure 6 Length of natural gas pipeline in India (in km) 27 Figure 7 CGD bidding rounds snapshot 27 Figure 8 Per capita consumption (kWh/ person) 29 Figure 9 Share of fossil fuel in electricity generation (%) 29 Figure 10 Electricity distribution losses (%) 29 Figure 11 Gas consumption by different sectors (in MMSCMD) 30 Figure 12 Roads sector infrastructure investment (Rs lakh crore) and share in total infrastructure investment (%) 46 Figure 13 Trend in road network in India (lakh km) 46 Figure 14 Achievement targets set by MoRTH 47 Figure 15 Road connectivity (Score: 1 - 100) 49 Figure 16 Quality of road infrastructure (Score: 1 – 7) 49 Figure 17 Railways infrastructure investment (Rs -

Rajhans Elita - Palgam, Surat All Set to Make Sure the Best Living Experience Ever

https://www.propertywala.com/rajhans-elita-surat Rajhans Elita - Palgam, Surat All set to make sure the best living experience ever. Rajhans Elita by Rajhans Groupat the very prime location of Palgam in Surat offers residential project that host 3 and 4 bhk apartments in various sizes. Project ID: J290151411 Builder: Rajhans Group Location: Rajhans Elita, Palgam, Surat - 395009 (Gujarat) Completion Date: Jan, 2021 Status: Started Description Rajhans Elita by Rajhans Group at the very prime location of Palgam in Surat offers residential project that host 3 and 4 bhk apartments in the size ranges in between 2395 to 3575 sqft. The property basks in the luxury of modern living that is finely crafted with world class equipment for daily living, recreation and fitness. It is the outcome of conscious designing of a perfect living space where residents will never feel want of any necessity. Amenities: Basement Car Parking with Multiple Entry and Exit Grand Entrance Lobby Temple within the Premises Gazebo Aroma Garden Waiting Reception Sand Pit Vaastu Compliant Homes Central Garden Entrance Entrance Foyer Cycling and Jogging Track Deck Seating Kid's Game Zone Water Bodies Victoria's Cricket Pitch Air Hockey Stunning Crafted Sculpture School Bus Pick-up Stand Fountain Wall Cascade Paved Walkway Lily Pond and Lotus Pond Strategic Location Advantage. Rajhans Infracon is a name to bank upon in the Indian realty market. In a span of merely 10 years, the builder has transformed Gujrat's infrastructural facet. The builder has received the coveted CREDAI Award in 2012 for the 'Best Residential Apartment Lifestyle Non Metro' category' and the CNBC AWAAZ Real Estate Award in 2013 for the 'Best Fully Completed Luxury Residential Project from Surat City'. -

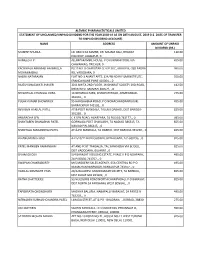

Name Address Amount of Unpaid Dividend (Rs.) Mukesh Shukla Lic Cbo‐3 Ka Samne, Dr

ALEMBIC PHARMACEUTICALS LIMITED STATEMENT OF UNCLAIMED/UNPAID DIVIDEND FOR THE YEAR 2018‐19 AS ON 28TH AUGUST, 2019 (I.E. DATE OF TRANSFER TO UNPAID DIVIDEND ACCOUNT) NAME ADDRESS AMOUNT OF UNPAID DIVIDEND (RS.) MUKESH SHUKLA LIC CBO‐3 KA SAMNE, DR. MAJAM GALI, BHAGAT 110.00 COLONEY, JABALPUR, 0 HAMEED A P . ALUMPARAMBIL HOUSE, P O KURANHIYOOR, VIA 495.00 CHAVAKKAD, TRICHUR, 0 KACHWALA ABBASALI HAJIMULLA PLOT NO. 8 CHAROTAR CO OP SOC, GROUP B, OLD PADRA 990.00 MOHMMADALI RD, VADODARA, 0 NALINI NATARAJAN FLAT NO‐1 ANANT APTS, 124/4B NEAR FILM INSTITUTE, 550.00 ERANDAWANE PUNE 410004, , 0 RAJESH BHAGWATI JHAVERI 30 B AMITA 2ND FLOOR, JAYBHARAT SOCIETY 3RD ROAD, 412.50 KHAR WEST MUMBAI 400521, , 0 SEVANTILAL CHUNILAL VORA 14 NIHARIKA PARK, KHANPUR ROAD, AHMEDABAD‐ 275.00 381001, , 0 PULAK KUMAR BHOWMICK 95 HARISHABHA ROAD, P O NONACHANDANPUKUR, 495.00 BARRACKPUR 743102, , 0 REVABEN HARILAL PATEL AT & POST MANDALA, TALUKA DABHOI, DIST BARODA‐ 825.00 391230, , 0 ANURADHA SEN C K SEN ROAD, AGARPARA, 24 PGS (N) 743177, , 0 495.00 SHANTABEN SHANABHAI PATEL GORWAGA POST CHAKLASHI, TA NADIAD 386315, TA 825.00 NADIAD PIN‐386315, , 0 SHANTILAL MAGANBHAI PATEL AT & PO MANDALA, TA DABHOI, DIST BARODA‐391230, , 0 825.00 B HANUMANTH RAO 4‐2‐510/11 BADI CHOWDI, HYDERABAD, A P‐500195, , 0 825.00 PATEL MANIBEN RAMANBHAI AT AND POST TANDALJA, TAL.SANKHEDA VIA BODELI, 825.00 DIST VADODARA, GUJARAT., 0 SIVAM GHOSH 5/4 BARASAT HOUSING ESTATE, PHASE‐II P O NOAPARA, 495.00 24‐PAGS(N) 743707, , 0 SWAPAN CHAKRABORTY M/S MODERN SALES AGENCY, 65A CENTRAL RD P O 495.00 -

Monetising the Metro

1 2 Indian Metro Systems – 2020 Analysis Contents Metro Rail In India: Introduction ............................................................................................................ 5 Brief Global History of Metro systems .................................................................................................... 5 Why is Metro the right MRT option? ...................................................................................................... 8 Key Benefits ........................................................................................................................................ 9 Impact on Urbanisation ...................................................................................................................... 9 When to Build a Metro ..................................................................................................................... 10 When Not to Build a Metro .............................................................................................................. 10 Implementation of Metro In Indian Context ........................................................................................ 11 Indian Issues with Implementation................................................................................................... 13 Metro in India: Spotlight Kolkata .......................................................................................................... 14 Metro in India: Spotlight Delhi ............................................................................................................. -

Diamond Research and Mercantile City Limited

Diamond Research and Mercantile City Limited A Government of Gujarat owned Company CIN : U75143GJ2015SGC083828 SUDA Bhawan, Nanpura, Surat-395001 Email : [email protected], Phone: (0261) 2462710 Fax: (0261) 2470318 MINUTES OF THE SECOND ANNUAL GENERAL MEETING OF DIAMOND RESEARCH AND MERCANTILE CITY LIMITED, HELD ON 1ST FEBRUARY, 2018 AT OFFICE OF THE CHIEF SECRETARY, GUJARAT, 5TH FLOOR, BLOCK NO. 1, SACHIVALAYA, GANDHINAGAR. PRESENT: Dr. J. N. Singh, IAS Chief Secretary Mr. Pankaj Kumar, IAS Principal Secretary, Revenue Department Mr. Mukesh Puri, IAS Principal Secretary, UD & UHD Mr. Sanjeev Kumar, IAS Secretary (EA), Finance Department Mr. Ashwini Kumar, CEO, GIDB Mr. M. Thennarasan, IAS Surat Municipal Commissioner Mr. Lochana Sehra, IAS Managing Director, GUDC Mr. M. Nagarajan , IAS Chief Executive Authority, SUDA Mr. Mahendra Patel, IAS Collector, Surat Mr. Prakash Dutta, IAS Senior Town Planner, Surat Urban Development Authority (SUDA) INVITEES: Mr. Kayomarz Panthaki & Partners of M/s. Natvarlal Vepari & Co. Mr. Urvesh Zaveri, Chartered Accountants Mrs. Savitaben Patel I/c. Chief Financial Officer, DREAMCL and Chief Accountant of Surat Urban Development Authority (SUDA) IN ATTENDANCE: All the members in person by virtue of the post they hold. QUORUM: The requisite quorum for the meeting being present, the meeting was initiated. Diamond Research and Mercantile City Limited A Government of Gujarat owned Company CIN : U75143GJ2015SGC083828 SUDA Bhawan, Nanpura, Surat-395001 Email : [email protected], Phone: (0261) 2462710 Fax: (0261) 2470318 1. TO ELECT CHAIRMAN OF THE MEETING Dr. J. N. Singh, IAS was unanimously elected as Chairman of the meeting and took the chair and presided over the meeting. NOTICE: Notice of the meeting along with Directors and Auditors report already circulated to the members was taken as read and following business was transacted. -

Development Programme 2020-21

BUDGET PUBLICATION NO. 35 GOVERNMENT OF GUJARAT DEVELOPMENT PROGRAMME 2020-21 GENERAL ADMINISTRATION DEPARTMENT PLANNING DIVISION SACHIVALAYA, GANDHINAGAR. FEBRUARY, 2020 DEVELOPMENT PROGRAMME 2020-21 CONTENTS PART - I CHAPTERS Page No. I Gujarat Current Scenario ( 1-12 ) II Development Approach ( 13-32 ) III Employment and Skill Development ( 33-37 ) IV Tribal Development Programme ( 38-44 ) V Social Development ( 45-47 ) VI Gender Focus ( 48-52 ) VII Human Development Approach to Decentralised Development ( 53-56 ) VIII E- Governance (57-61 ) IX Twenty Point Programme ( 62-72 ) X Externally Aided Projects in the State (73-74 ) PART – II DEPARTMENTWISE OBJECTIVE, STRATEGY AND IMPORTANT SCHEMES 1 Agriculture and Co-operation Department (1-59) 2 Climate Change Department (60-62) 3 Education Department. (63-97) 4 Energy and Petrochemicals Department (98-105) 5 Food, Civil Supplies and Consumer Affairs Department (106-111) 6 Forest and Environment Department (112-123) 7 General Administration Department (124-131) 8 Health and Family Welfare Department (132-150) 9 Home Department (151-154) 10 Information and Broadcasting Department. (155-156) 11 Industries and Mines Department (157-228) 12 Labour and Employment Department (229-234) 13 Legal Department (235-236) 14 Narmada, W.R., W.S. & Kalpsar Department (237-251) 15 Ports and Transport Department (252-253) 16 Panchayat, Rural Housing & Rural Development Department (254-268) 17 Roads and Buildings Department (269-279) 18 Revenue Department (280-285) 19 Social Justice and Empowerment Department -

Comprehensive Mobility Plan Surat 2046 SURAT MUNICIPAL CORPORATION 22Nd January, 2018 Presentation Structure

Comprehensive Mobility Plan Surat 2046 SURAT MUNICIPAL CORPORATION 22nd January, 2018 Presentation Structure . Part 1- Trends and Developments affecting Mobility in Surat . Part 2- Travel behavior of Surtis . Part 3 : System Performance . Part 4: Mobility challenges for future . Part 5: People’s expectations from the Plan . Part 6: Forecasts . Part 7: Proposals . Part 8: Institutional Setup . Part 9: Project Costing Page . 2 What is Comprehensive Mobility Plan (CMP) ? . The Ministry of Urban Development, Government of India formulated the National Urban Transport Policy in April, 2006 . NUTP envisaged the preparation of Comprehensive Mobility plans. CMP is a strategic document which provides the direction for the development of urban transportation in the city. It cover all elements of urban transport under an integrated planning process. It is a long-term vision for desirable accessibility and mobility pattern for people and goods in the city to provide, safe, secure, efficient, reliable and seamless connectivity that supports and enhances economic, social and environmental sustainability. (Preparing a Comprehensive Mobility Plan(CMP)—A Toolkit, MoUD, 2014) CMP Surat - 30 years Horizon- 2046 Page . 3 Surat CMP- Study Area Delineation Administrative Boundaries: SMC comprises of : 326.52 Sq. km area 7 Zones 89 Wards SUDA comprises of : 985.16 sq km area 121 Villages 18 Urban area with SUDA and 2 outside SUDA 2 INA within SUDA (Sachin and Hazira) Total Study area 1351 sq km Comprises of 15 Urban Area 182 Villages 2 INA (Sachin and Hazira)