Canada's Top 50 Women in Fintech 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2020 Public Accountability Statement

2020 PUBLIC ACCOUNTABILITY STATEMENT ABOUT CORPORATE SMALL ACCESS TO NUMBER OF DEBT TAXES BRANCH THIS REPORT DONATIONS & BUSINESS FINANCIAL EMPLOYEES FINANCING OPENINGS, PHILANTHROPIC BANKING SERVICES IN CANADA CLOSINGS & ACTIVITY RELOCATIONS What’s Inside 2 About this Report 17 Number of Employees in Canada 3 Corporate Donations & Philanthropic Activity 18 Debt Financing 9 Small Business Banking 20 Taxes 11 Access to Financial Services 21 Branch Openings, Closings & Relocations About this Report Scope of Reporting About Scotiabank This Public Accountability Statement includes Scotiabank is a leading bank in the Americas. information from November 1, 2019 to Guided by our purpose: “for every future”, we help October 31, 2020, for the following affiliates our customers, their families and their communities of Scotiabank in Canada: Scotia Capital Inc., achieve success through a broad range of advice, National Trust Company, Scotia Mortgage products and services, including personal and Corporation, Scotia General Insurance Company, commercial banking, wealth management and ADS Canadian Bank, Montreal Trust Company private banking, corporate and investment banking, of Canada, Scotia Life Insurance Company, and capital markets. With a team of over 90,000 The Bank of Nova Scotia Trust Company, employees and assets of approximately $1.1 trillion Scotia Dealer Advantage Inc., Roynat Inc., (as at October 31, 2020), Scotiabank trades on the MD Private Trust Company, and MD Life Insurance Toronto Stock Exchange (TSX: BNS) and New York Company. These affiliates are finance entities or Stock Exchange (NYSE: BNS). For more information, financial institution subsidiaries of Scotiabank please visit scotiabank.com and follow us on Twitter operating in Canada that have less than $1 billion @ScotiabankViews. -

Navigating the Emv Implementation Process

PARTNERING FOR SUCCESS: NAVIGATING THE EMV IMPLEMENTATION PROCESS A Mercator Advisory Group Research Brief Sponsored by Moneris Solutions November 2014 Partnering for Success: Navigating the EMV ImplementationProcess A Mercator Advisory Group Research Brief Sponsored by Moneris Solutions Contents The EMV Standard .............................................................................................................................3 Reducing Counterfeit Card Fraud .......................................................................................................... 3 Reducing Card Theft Fraud .................................................................................................................... 3 Chip and PIN vs. Chip and Signature ...................................................................................................... 3 Card Network EMV Road Maps ............................................................................................................. 4 Outlook: EMV Adoption in the United States ......................................................................................5 Credit Card Issuance .............................................................................................................................. 5 Debit Card Issuance ............................................................................................................................... 6 Acceptance ........................................................................................................................................... -

To Consult DPQ/Moneris Preferred Pricing

Preferred Rates For Your Business Les Dentistes propriétaires du Québec (DPQ) and Moneris® are pleased to introduce preferred card payment processing rates for your business.† Moneris Transaction 1 Interac Per Transaction Rate Card Type * Assessment Fee Interchange Fee Fee Debit Card $0.040 VISA 0.10% 0.09% Foreign Assessment Fee (VISA) of 0.40% will apply to all gross foreign sales dollar volume processed. Card Brand Fee (Interac) of $0.0085 will apply to each Interac transaction. An Interac fee of $0.035 Mastercard 0.10% 0.08% per transaction will apply to each Interac Flash® (contactless) transaction. Foreign Assessment Fee (Mastercard) of 0.60% will apply to all gross foreign sales dollar volume processed. For more information about the applicable Discover 0.10% 0.063% Interchange rates, Foreign Assessment Fee (Discover) of 0.40% will apply to all gross foreign sales dollar volume processed. please visit moneris.com/interchange POS Solution(s) Rates Union Pay 0.10% 0.1% Standalone $22.00/month Foreign Assessment Fee (UnionPay) of 0.10% will apply to all gross foreign sales dollar volume processed. PIN Pad $16.00/month Visa Debit 0.10% Short Range Wireless $45.00/month Debit MasterCard 0.10% $50.00/month * You agree that you are responsible for the fulfillment of any increase imposed by the Long Range Wireless (plus $75.00 one time activation fee) Card Brand and any fees, fines, penalties, or assessments levied by the Card Brands on us or our parent banks, RBC and BMO, in connection with the processing of your transactions. -

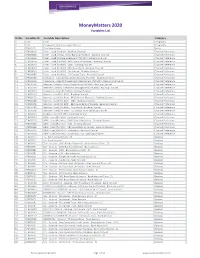

Moneymatters 2020 Variables List

MoneyMatters 2020 Variables List Order Variable ID Variable Description Category 0 CODE Code Geography 0 GEO Geographic Summarization Indicator Geography 1 CBASHHD Total Households Basics 2 CFM0001B Teller - Used [Pst Mth] - Banking Channel Channel Preference 3 CFM0002B Teller - Used for Day to Day Banking [Pst Mth] - Banking Channel Channel Preference 4 CFM0003B Teller - Used to Make Investment [Pst Mth] - Banking Channel Channel Preference 5 CFM0004B Teller - Used [Pst Mth] - BMO Bank of Montreal - Banking Channel Channel Preference 6 CFM0005B Teller - Used [Pst Mth] - CIBC - Banking Channel Channel Preference 7 CFM0006B Teller - Used [Pst Mth] - RBC Royal Bank - Banking Channel Channel Preference 8 CFM0007B Teller - Used [Pst Mth] - Scotiabank - Banking Channel Channel Preference 9 CFM0008B Teller - Used [Pst Mth] - TD Canada Trust - Banking Channel Channel Preference 10 CFM0010B Telephone - Used for Day to Day Banking [Pst Mth] - Banking Channel Channel Preference 11 CFM0011B Telephone - Used for Investment Management [Pst Mth] - Banking Channel (!) Channel Preference 12 CFM0013B Internet - Used for Day to Day Banking [Pst Mth] - Banking Channel Channel Preference 13 CFM0014B Internet - Used for Investment Management [Pst Mth] - Banking Channel Channel Preference 14 CFM0009B Telephone - Used [Pst Mth] - Banking Channel Channel Preference 15 CFM0012B Internet - Used [Pst Mth] - Banking Channel Channel Preference 16 CFM0015B Internet - Used [Pst Mth] - BMO Bank of Montreal - Banking Channel Channel Preference 17 CFM0016B Internet - -

Audited Annual Financial Statements for the Year Ended December 31, 2018

Audited Annual Financial Statements For the year ended December 31, 2018 Tangerine Balanced Portfolio Tangerine Balanced Portfolio Audited Annual Financial Statements for the year ended December 31, 2018 (In Canadian dollars, unless otherwise indicated) Independent Auditors’ Report To the Unitholders of Tangerine Balanced Portfolio (the “Fund”) Opinion We have audited the financial statements of the Fund, which comprise the statements of financial position as at December 31, 2018 and 2017, and the statements of comprehensive income, statements of changes in net assets attributable to holders of redeemable units and statements of cash flows for the years then ended, and notes to the financial statements, including a summary of significant accounting policies. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Fund as at December 31, 2018 and 2017, and its financial performance and its cash flows for the years then ended in accordance with International Financial Reporting Standards (IFRSs). Basis for Opinion We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Fund in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Other Information Management is responsible for the other information. -

2008 Annual Report to Shareholders

191ST ANNUAL REPORT 2008 Defining great customer experience I value a clear plan for the retirement I want. I appreciate a bank that can help my company in good times and bad. Who will explain all my mortgage options so that I actually understand? Thanks for giving me the advice that makes sense for me. Defining great customer experience begins with making sense of it all. BMO’s vision – to be the bank that defines great customer experience – galvanizes our organization and encourages every one of our 37,000 employees to help us succeed. In everything we do, we define great customer experience. We do so by helping our customers make sense of their financial lives, and by bringing clarity to the complexities of money. BMO gratefully acknowledges our customers who so generously gave their time and portraits to this annual report. Adolphe A. Tinling Linda Knight Scott Saxberg Maria Monreal-Cameron President and Principal Designer CEO, President and CEO, President and CEO, Adolphe Anthony T. Design CarePartners Crescent Point Energy Trust Hispanic Chamber of Commerce International and Associates Waterloo, Ontario Calgary, Alberta of Wisconsin Montreal, Quebec Milwaukee, Wisconsin Who We Are A Canadian-based North American bank, established in 1817, BMO® Financial Group is highly diversified. We work with millions of personal, commercial, corporate and institutional customers through our operating groups: Personal and Commercial Banking Canada, Personal and Commercial Banking U.S., Private Client Group and BMO Capital Markets. Our 37,000 employees are dedicated to making BMO the bank that defines great customer experience. Our approach is relationship-driven. -

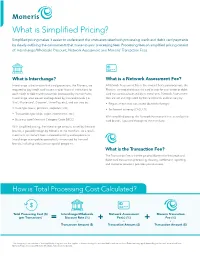

What Is Simplified Pricing?

What is Simplified Pricing? Simplified pricing makes it easier to understand the costs associated with processing credit and debit card payments by clearly outlining the components that make up your processing fees. Processing fees on simplified pricing consist of: Interchange/Wholesale Discount, Network Assessment and Moneris® Transaction Fees. What is Interchange? What is a Network Assessment Fee? Interchange is the amount that card processors, like Moneris, are A Network Assessment Fee is the amount that card processors, like required to pay credit card issuers and/or financial institutions for Moneris, are required to pay the card brands for each credit or debit each credit or debit card transaction processed by its merchants. card transaction processed by its merchants. Network Assessment Interchange rates are set and regulated by the card brands (i.e. fees are set and regulated by the card brands and can vary by: ® ® ® Visa , Mastercard , Discover , UnionPay, etc.), and can vary by: • Region where card was issued (domestic/foreign) • Card type (basic, premium, corporate, etc.) • Settlement currency (CAD, US) • Transaction type (chip, swipe, ecommerce, etc.) With simplified pricing, the Network Assessment Fee, as set by the • Business type/Merchant Category Code (MCC) card brands, is passed through to the merchant. With simplified pricing, the interchange amount, as set by the card brands, is passed through by Moneris to the merchant. As a result, merchants will benefit from increased visibility and exposure to interchange rate updates periodically announced by the card brands, including reductions or special programs. What is the Transaction Fee? The Transaction Fee is the fee paid to Moneris for the credit and debit card transaction processing, clearing, settlement, reporting and customer service it provides your business. -

For Apple® Ipad®, Iphone® and Ipod Touch®

For Apple® iPad®, iPhone® and iPod touch® (11/17) For more information and assistance: Web: getpayd.com/paydpro/support Email: [email protected] Toll-free: 1-855-423-PAYD (7293) Record your Moneris® merchant ID here: __________________________________________ Contents Introduction ................................................................................................ 6 Before you get started .............................................................................. 7 Activating your PAYD Pro store .............................................................. 8 Setting up the PAYD App on your mobile device .............................. 9 Downloading and installing the PAYD App from the App Store SM 10 Setting up the PAYD PIN Pad ................................................................. 11 Pairing a new PAYD PIN Pad with your mobile device 12 Pairing an initialized PAYD PIN Pad with a different mobile device 19 Pairing a replacement PAYD PIN Pad with your mobile device 22 Other PAYD PIN Pad settings 24 Changing an initialized PAYD PIN Pad's default language 24 Bluetooth pairing in Legacy mode 26 Ready to use the PAYD App? 30 Optional features ..................................................................................... 31 Setting the transaction details level 31 Setting a default payment device 32 1 Enabling Pre-Authorizations 32 Enabling tip prompting 33 Setting a tax rate 34 Location-mapping transactions 35 Viewing a location map 35 Setting a quick PIN for sign-in 36 Pre-filling the employee ID/store ID at -

BMO Financial Group Reports Third Quarter 2018 Results

BMO Financial Group Reports Third Quarter 2018 Results REPORT TO SHAREHOLDERS Financial Results Highlights Third Quarter 2018 Compared With Third Quarter 2017: • Net income of $1,536 million, up 11%; adjusted net income1 of $1,565 million, up 14% • EPS2 of $2.31, up 13%; adjusted EPS1,2 of $2.36, up 16% • ROE of 14.7%, up from 13.4%; adjusted ROE1 of 15.0%, up from 13.3% • Provision for credit losses3 (PCL) of $186 million compared with $202 million on an adjusted basis in the prior year and $126 million on a reported basis; prior year reported provision for credit losses includes a decrease in the collective allowance of $76 million pre-tax • Common Equity Tier 1 Ratio of 11.4% Year-to-Date 2018 Compared With Year-to-Date 2017: • Net income of $3,755 million, down 9%, reflecting the revaluation of our U.S. net deferred tax asset4 and a restructuring charge in the current year5 and a net gain6 in the prior year; adjusted net income1 of $4,450 million, up 6% • EPS2,4,5 of $5.59, down 8%; adjusted EPS1,2 of $6.67, up 7% • ROE of 12.3%, compared with 13.7%; adjusted ROE1 of 14.6%, up from 13.9% • Provision for credit losses of $487 million3 compared with $620 million on an adjusted basis and $544 million on a reported basis Toronto, August 28, 2018 – For the third quarter ended July 31, 2018, BMO Financial Group recorded net income of $1,536 million or $2.31 per share on a reported basis, and net income of $1,565 million or $2.36 per share on an adjusted basis. -

2016 APEGS Annual Report

2016 Annual Report ON THE COVER: March 7, 1997 - Honourable John E.N. Wiebe Lieutenant Governor of Saskatchewan signs the proclamation of The Engineering and Geoscience Professions Act, attended by Heinrich Feldkamp, P.Eng., FEC (APES President 1996 – 1997) and Frances Haidl, P.Geo., FEC (Hon.), FGC (Act Amendment Committee) 2 Table of Contents President's Report . 4 Geoscientists Canada Director’s Report . 30 Executive Director and Registrar's Report . 6 College of Engineering, University of Saskatchewan . 34 Investigation Committee. 8 Department of Geological Sciences, University of Saskatchewan. 35 Discipline Committee . 9 Faculty of Engineering & Applied Science, University of Regina . 36 30 by 30 Task Group . 10 Department of Geology, University of Regina. 38 Governance Board . 11 Saskatoon Engineering Students' Society . 39 Academic Review Committee . 12 Regina Engineering Students' Society. 39 Licensee Admissions Committee . 13 D.M. Kent Geology Club (U of R Geology Students) . 40 Experience Review Committee . 14 Regina Engineering Society. 41 Professional Practice Examination Committee. 14 Saskatoon Engineering Society . 43 Registrar's Advisory Committee . 15 Moose Jaw Engineering Society. 44 Legislative Liaison Committee . 15 Saskatchewan Geological Society (Regina). 44 Saskatchewan Construction Panel . 16 Association of Consulting Engineering Companies - SK . 46 Image and Identity Board . 16 Awards Committee. 17 Financial Report . 47 Connection and Involvement Committee . 18 Balance Sheet . 48 Professional Edge Committee . 19 Consolidated Statement of Revenue and Expenditures. 49 Communications and Public Relations Committee. 20 Investments & Cash Funds . 52 Equity and Diversity Committee . 21 Education Board . 22 2015-2016 APEGS Council . 55 2016 APEGS Volunteers. 56 Professional Development Committee . 23 Student Development Committee . 24 K-12 Committee . -

CUSTODIAL AGREEMENTS As of April 30, 2019

Contact: Samantha Duffield Manager, Financial Compliance Phone: (416) 943-4662 Email: [email protected] CUSTODIAL AGREEMENTS The following is an alphabetical listing of prescribed Custodial Agreements executed as of April 30, 2019 between the Mutual Fund Dealers Association of Canada (MFDA), as bare trustee on behalf of Members, and mutual fund companies and other financial institutions, in accordance to the Member Regulation Notice MSN-0058, Acceptable Securities Locations. Please ensure that your assets held are included in the types of products listed by the entity. Fund Manager/ Financial Institution Type of Products 1 1832 Asset Management L.P. Mutual Fund / Hedge Fund / Labour Dynamic Mutual Fund Sponsored Fund / Deposit Accounts 2 Acker Finley Asset Management Inc. Mutual Fund 3 ACM Advisors Ltd. Mortgage Investment Fund 4 Acorn Global Investments Inc. Hedge Fund 5 ADS Canadian Bank GIC’s / High Interest Savings Account 6 AGF Investments Inc. Mutual Fund / Pooled Fund - Acuity Pooled Funds - AGF Pooled Funds - AGF family of mutual funds - AGF Elements family of mutual funds - Harmony family of mutual funds 7 AIP Asset Management Inc. Mutual Fund / Hedge Fund / Limited Partnership 8 AlphaNorth Asset Management Mutual Fund 9 Arrow Capital Management Inc. Investment Products 10 ATB Investment Management Inc. Mutual Fund 11 Aurion Capital Management Inc. Pooled Fund 12 Aventine Management Group Inc. Mutual Fund 13 B2B Bank GIC’s / High Interest Investment Accounts 14 Bank of Montreal GIC’s / High Interest Savings Accounts 15 Bank of Montreal Mortgage Corporation GIC’s 16 Bank of Nova Scotia (The) GIC’s 17 Barometer Capital Management Inc. Mutual Fund / Pooled Fund Doc 110950 Page 1 of 30 Fund Manager/ Financial Institution Type of Products 18 BC Advantage Fund Management Limited Venture Capital Corporation (VCC) Funds 19 B.E.S.T. -

2020 Canada Banking and Credit Card Mobile App

Investments in Easy-to-Use Digital Tools Paying Off for Banks, Credit Card Companies in Canada, J.D. Power Finds Ease of Navigation, Accessibility of Important Information and Seamless Cross-Channel Experience Seen As Key Drivers of Customer Satisfaction TORONTO: 10 June 2020 — During the height of the COVID-19 pandemic, 41% of retail bank customers said they were using their bank’s mobile app more frequently than ever before, and 40% said they were using credit cards in a contactless manner. Years of digital investments are paying off as banks support homebound customers to continue their banking activities, based on a series of recent J.D. Power studies, released today, of bank and credit card online and mobile app users. Data shows that ease of use, speed and accessibility of common features are the most-often-cited variables shared by the best-performing digital platforms. The studies—J.D. Power 2020 Canada Banking Mobile App Satisfaction Study,SM 2020 Canada Online Banking Satisfaction Study,SM 2020 Canada Credit Card Mobile App Satisfaction StudySM and 2020 Canada Online Credit Card Satisfaction Study SM—track overall customer satisfaction with banking and credit card providers’ digital offerings. “Banks have been investing heavily in digital for several years and those investments paid off during the past three months as the COVID-19 pandemic dramatically accelerated the shift to digital, forcing many remaining holdouts to finally take the plunge,” said Jennifer White, senior consultant for banking and payment intelligence at J.D. Power. “It’s never been more important for banks and credit card companies to make their digital offerings easy to access and use.