2008 Annual Report to Shareholders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Navigating the Emv Implementation Process

PARTNERING FOR SUCCESS: NAVIGATING THE EMV IMPLEMENTATION PROCESS A Mercator Advisory Group Research Brief Sponsored by Moneris Solutions November 2014 Partnering for Success: Navigating the EMV ImplementationProcess A Mercator Advisory Group Research Brief Sponsored by Moneris Solutions Contents The EMV Standard .............................................................................................................................3 Reducing Counterfeit Card Fraud .......................................................................................................... 3 Reducing Card Theft Fraud .................................................................................................................... 3 Chip and PIN vs. Chip and Signature ...................................................................................................... 3 Card Network EMV Road Maps ............................................................................................................. 4 Outlook: EMV Adoption in the United States ......................................................................................5 Credit Card Issuance .............................................................................................................................. 5 Debit Card Issuance ............................................................................................................................... 6 Acceptance ........................................................................................................................................... -

To Consult DPQ/Moneris Preferred Pricing

Preferred Rates For Your Business Les Dentistes propriétaires du Québec (DPQ) and Moneris® are pleased to introduce preferred card payment processing rates for your business.† Moneris Transaction 1 Interac Per Transaction Rate Card Type * Assessment Fee Interchange Fee Fee Debit Card $0.040 VISA 0.10% 0.09% Foreign Assessment Fee (VISA) of 0.40% will apply to all gross foreign sales dollar volume processed. Card Brand Fee (Interac) of $0.0085 will apply to each Interac transaction. An Interac fee of $0.035 Mastercard 0.10% 0.08% per transaction will apply to each Interac Flash® (contactless) transaction. Foreign Assessment Fee (Mastercard) of 0.60% will apply to all gross foreign sales dollar volume processed. For more information about the applicable Discover 0.10% 0.063% Interchange rates, Foreign Assessment Fee (Discover) of 0.40% will apply to all gross foreign sales dollar volume processed. please visit moneris.com/interchange POS Solution(s) Rates Union Pay 0.10% 0.1% Standalone $22.00/month Foreign Assessment Fee (UnionPay) of 0.10% will apply to all gross foreign sales dollar volume processed. PIN Pad $16.00/month Visa Debit 0.10% Short Range Wireless $45.00/month Debit MasterCard 0.10% $50.00/month * You agree that you are responsible for the fulfillment of any increase imposed by the Long Range Wireless (plus $75.00 one time activation fee) Card Brand and any fees, fines, penalties, or assessments levied by the Card Brands on us or our parent banks, RBC and BMO, in connection with the processing of your transactions. -

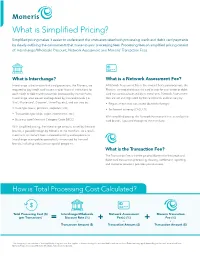

What Is Simplified Pricing?

What is Simplified Pricing? Simplified pricing makes it easier to understand the costs associated with processing credit and debit card payments by clearly outlining the components that make up your processing fees. Processing fees on simplified pricing consist of: Interchange/Wholesale Discount, Network Assessment and Moneris® Transaction Fees. What is Interchange? What is a Network Assessment Fee? Interchange is the amount that card processors, like Moneris, are A Network Assessment Fee is the amount that card processors, like required to pay credit card issuers and/or financial institutions for Moneris, are required to pay the card brands for each credit or debit each credit or debit card transaction processed by its merchants. card transaction processed by its merchants. Network Assessment Interchange rates are set and regulated by the card brands (i.e. fees are set and regulated by the card brands and can vary by: ® ® ® Visa , Mastercard , Discover , UnionPay, etc.), and can vary by: • Region where card was issued (domestic/foreign) • Card type (basic, premium, corporate, etc.) • Settlement currency (CAD, US) • Transaction type (chip, swipe, ecommerce, etc.) With simplified pricing, the Network Assessment Fee, as set by the • Business type/Merchant Category Code (MCC) card brands, is passed through to the merchant. With simplified pricing, the interchange amount, as set by the card brands, is passed through by Moneris to the merchant. As a result, merchants will benefit from increased visibility and exposure to interchange rate updates periodically announced by the card brands, including reductions or special programs. What is the Transaction Fee? The Transaction Fee is the fee paid to Moneris for the credit and debit card transaction processing, clearing, settlement, reporting and customer service it provides your business. -

For Apple® Ipad®, Iphone® and Ipod Touch®

For Apple® iPad®, iPhone® and iPod touch® (11/17) For more information and assistance: Web: getpayd.com/paydpro/support Email: [email protected] Toll-free: 1-855-423-PAYD (7293) Record your Moneris® merchant ID here: __________________________________________ Contents Introduction ................................................................................................ 6 Before you get started .............................................................................. 7 Activating your PAYD Pro store .............................................................. 8 Setting up the PAYD App on your mobile device .............................. 9 Downloading and installing the PAYD App from the App Store SM 10 Setting up the PAYD PIN Pad ................................................................. 11 Pairing a new PAYD PIN Pad with your mobile device 12 Pairing an initialized PAYD PIN Pad with a different mobile device 19 Pairing a replacement PAYD PIN Pad with your mobile device 22 Other PAYD PIN Pad settings 24 Changing an initialized PAYD PIN Pad's default language 24 Bluetooth pairing in Legacy mode 26 Ready to use the PAYD App? 30 Optional features ..................................................................................... 31 Setting the transaction details level 31 Setting a default payment device 32 1 Enabling Pre-Authorizations 32 Enabling tip prompting 33 Setting a tax rate 34 Location-mapping transactions 35 Viewing a location map 35 Setting a quick PIN for sign-in 36 Pre-filling the employee ID/store ID at -

National Ballet of Canada 2018/19 Annual Report

2018/19 Annual Report Table of Contents Messages from the Artistic Director, Executive Director & Board Chair 3 Company Snapshot 4 Soaring: The Campaign for The National Ballet of Canada 5 2018/19 Performances 6 Community Engagement 19 Equity, Diversity and Inclusion 25 New Initiatives 26 2018/19 Dancer Roster 29 Awards 30 Dancer Anniversaries 32 In Memoriam 34 The National Ballet of Canada Orchestra 35 The National Ballet of Canada Board of Directors 36 Our Donors 37 Staff 53 Attendance 55 Summary Financial Statements 56 Grant Thornton Auditors’ Report 57 Selected Statistics 58 Guillaume Côté is sponsored through Dancers First by Emmanuelle Gattuso, C.M. and Allan Slaight, C.M. Tanya Howard is sponsored through Dancers First by Nancy Pencer. Tanya Howard and Guillaume Côté in Being and Nothingness. Photo by Aleksandar Antonijevic. national.ballet.ca 2 Messages The National Ballet of Canada “ continued to make significant gains in 2018/19 within a climate of steady leadership and fiscal balance. With the support of an engaged donor community, we were able to tour overseas, collaborate on new work, host an international competition and offer a variety of engagement programmes to our diverse audiences nationwide.” Barry Hughson, Executive Director Among the many artistic achievements of “ our 2018/19 season, I am proud to include The 2018/19 season has been a our first ever company tour to Moscow and “ continuation of everything The National St. Petersburg with three exciting ballets Ballet of Canada has come to stand for from our recent repertoire. In Toronto, we in recent years – innovation, ambition, presented the North American premiere excellence and community. -

Judges Scores

ISU World Figure Skating Championships 2008 MEN FREE SKATING JUDGES DETAILS PER SKATER Total Total Total Total NOC Segment Element Program Component Deductions Rank Name Code Score Score Score (factored) = + + - 1 Jeffrey BUTTLE CAN 163.07 84.29 78.78 0.00 # Executed Base GOE The Judges Panel Scores Elements Info Value (in random order) of Panel 1 3A+2T+2Lo 10.30 0.29 0 0 0 0 2 0 0 0 0 2 1 1 10.59 2 3F+3T 9.50 1.29 1 1 1 1 2 0 2 2 1 2 2 1 10.79 3 CUSp4 3.00 0.50 1 0 1 1 2 0 1 1 2 1 2 1 3.50 4 3A 7.50 0.29 1 0 0 0 2 0 1 0 1 2 0 0 7.79 5 FSSp4 3.00 0.29 1 0 1 1 1 0 1 1 0 2 0 1 3.29 6 CiSt3 3.10 0.71 1 1 2 2 2 1 2 1 1 2 2 2 3.81 7 3Lz+2T 8.03 x 1.00 1 1 1 1 1 1 1 1 1 2 1 1 9.03 8 3Lo 5.50 x 1.14 2 1 1 1 1 0 1 2 0 2 1 1 6.64 9 3S 4.95 x 1.00 0 1 2 0 2 1 2 2 1 2 2 0 5.95 10 SlSt3 3.10 0.71 1 2 2 1 2 1 2 1 1 2 2 2 3.81 11 2A 3.85 x 1.00 0 1 1 1 2 0 2 2 0 2 2 1 4.85 12 3Lz 6.60 x 0.00 0 0 0 -1 0 0 0 0 0 0 0 0 6.60 13 CoSp4 3.00 0.43 1 0 1 1 1 0 1 2 1 2 0 1 3.43 14 CCoSp4 3.50 0.71 1 1 1 1 2 1 2 2 1 2 2 2 4.21 74.93 84.29 Program Components Factor Skating Skills 2.00 7.75 7.50 8.00 7.75 8.25 8.25 8.50 8.25 8.00 8.00 8.00 7.50 7.89 Transition / Linking Footwork 2.00 7.50 7.25 7.75 8.00 7.50 8.00 8.00 8.25 7.75 8.00 7.75 7.25 7.75 Performance / Execution 2.00 7.75 7.75 8.00 7.75 8.00 8.25 8.00 8.00 7.75 8.00 8.00 7.25 7.86 Choreography / Composition 2.00 7.50 7.50 8.00 8.25 8.25 8.00 7.75 8.00 8.00 8.25 8.00 7.50 7.89 Interpretation 2.00 7.75 7.75 8.00 8.00 8.50 8.25 8.50 8.25 8.00 8.00 8.25 7.50 8.00 Judges Total Program Component Score (factored) -

BMO Financial Group Reports Third Quarter 2018 Results

BMO Financial Group Reports Third Quarter 2018 Results REPORT TO SHAREHOLDERS Financial Results Highlights Third Quarter 2018 Compared With Third Quarter 2017: • Net income of $1,536 million, up 11%; adjusted net income1 of $1,565 million, up 14% • EPS2 of $2.31, up 13%; adjusted EPS1,2 of $2.36, up 16% • ROE of 14.7%, up from 13.4%; adjusted ROE1 of 15.0%, up from 13.3% • Provision for credit losses3 (PCL) of $186 million compared with $202 million on an adjusted basis in the prior year and $126 million on a reported basis; prior year reported provision for credit losses includes a decrease in the collective allowance of $76 million pre-tax • Common Equity Tier 1 Ratio of 11.4% Year-to-Date 2018 Compared With Year-to-Date 2017: • Net income of $3,755 million, down 9%, reflecting the revaluation of our U.S. net deferred tax asset4 and a restructuring charge in the current year5 and a net gain6 in the prior year; adjusted net income1 of $4,450 million, up 6% • EPS2,4,5 of $5.59, down 8%; adjusted EPS1,2 of $6.67, up 7% • ROE of 12.3%, compared with 13.7%; adjusted ROE1 of 14.6%, up from 13.9% • Provision for credit losses of $487 million3 compared with $620 million on an adjusted basis and $544 million on a reported basis Toronto, August 28, 2018 – For the third quarter ended July 31, 2018, BMO Financial Group recorded net income of $1,536 million or $2.31 per share on a reported basis, and net income of $1,565 million or $2.36 per share on an adjusted basis. -

Train with the Best Coached by the Best

TRAIN WITH THE BEST COACHED BY THE BEST THE BY COACHED BEST THE WITH TRAIN Ice Castle International Training Center was founded by Ponomarenko. Ice Castle has become a host to many other Olympic, former Ice Follies star Carol Probst and her husband Walter. Together World, and International skaters who come to draw on the remarkable they created the only true complete training center in the world. The talent concentrated at this facility. Michelle Kwan trained here for over Ice Castle facility is nestled in the forest at an altitude of 5,400 feet in ten years with her coach, Rafael Arutyunyan. Three-time World Pair Southern California’s San Bernardino Mountains, less than two hours Champions Shen and Zhao, as well as 2008 World Champions Jeffrey east of Los Angeles. Buttle and Mao Asada have made Ice Castle their home. Almost from conception, Ice Castle International Training Center has The reasons Ice Castle is so popular are not hard to identify: An attracted the world’s finest skaters and coaches since the dedicated international size rink (185’ x 85’), superbly maintained, completely figure skating rink was opened in 1988. Olympic Champion Robin mirrored at one end for choreography, equipped with cross-rink jump Cousins from England began a long line of notables in the skating harness and ballet bar, high-altitude indoor training, and world-class world to teach and/or train here. coaches, Ice Castle provides deep experience from its staff at all levels Coaches such as Frank Carroll, Irina Rodrina, Peter Oppegard, and so that every skater, from the novice first stepping onto the ice to other luminaries made Ice Castle home to skaters such as Lu Chen, the world-class competitor, can train and grow under one roof at a Nicole Bobeck, Surya Bonaly, Bourne and Kraatz, and Klimova and consistent pace. -

Quick Reference Booklet 11 August 2020

Quick Reference Booklet 11 August 2020 QR Summary of Changes, 11 August 2020 Summary of Changes, 11 August 2020 This document reflects updates effective since the 15 October 2019 version. Table 1: Descriptions of Changes Description of Change Where to Look Chapter 3—Card Acceptor Business Codes Card Acceptor Business (CAB) Programs and (MCCs) Descriptions Updated country-specific CAB program to include Throughout AUS4, Australia transit 4. Added Macedonia to MCC 9406. MCC 9406—Government-owned Lottery (Specific Countries) Added MCC 9406 Government-owned Lottery Card Acceptor Business Codes (MCCs)— (Specific Countries) to All Transaction Category Transaction Category Codes Codes. Removed vending machines from MCC 5499. MCC 5499—Miscellaneous Food Stores— Convenience Stores, Markets, Specialty Stores Added P for MCC 9399 and MCC 7800. Removed Card Acceptor Business Codes (MCCs)— note in MCC Description. Abbreviated Removed sentence: “This MCC may also be used MCC 9399—Government Services—not to identify U.S. state lottery ticket sales by elsewhere classified merchants properly registered with Mastercard as set forth in section 9.4.5 of the Security Rules and Proceduresmanual.” Added MCC—Electric Vehicle Charging. MCC 5552—Electric Vehicle Charging Added Card Acceptor Business Segment codes for Card Acceptor Business (CAB) Programs and Uruguay. Descriptions Added Card Acceptor Business program, MON2, Throughout to MCC 4829 and MCC 6540. Added 2021 holiday schedule Holiday Processing Schedule ©1990–©2020 Mastercard. Proprietary. All rights reserved. Quick Reference Booklet • 11 August 2020 2 Contents Contents Summary of Changes, 11 August 2020.............................................................2 Chapter 1: Holiday Processing Schedule........................................................ 12 Overview Settlement U.S. Dollar Holiday Schedule............................................................13 Settlement Holidays........................................................................................................ -

What Is Simplified Pricing?

What is Simplified Pricing? Simplified pricing makes it easier to understand the costs associated with processing credit and debit card payments by clearly outlining the components that make up your processing fees. Processing fees on simplified pricing consist of: Interchange/Wholesale Discount, Network Assessment and Moneris® Transaction Fees. What is Interchange? What is a Network Assessment Fee? Interchange is the amount that card processors, like Moneris, are A Network Assessment Fee is the amount that card processors, required to pay credit card issuers and/or financial institutions for like Moneris, are required to pay the card brands for each credit or each credit or debit card transaction processed by its merchants. debit card transaction processed by its merchants. Network Interchange rates are set and regulated by the card brands (i.e. Assessment fees are set and regulated by the card brands and can Visa®, Mastercard®, Discover®, UnionPay, etc.), and can vary by: vary by: • Card type (basic, premium, corporate, etc.) • Region where card was issued (domestic/foreign) • Transaction type (chip, swipe, ecommerce, etc.) • Settlement currency (CAD, US) • Business type/Merchant Category Code (MCC) With simplified pricing, the Network Assessment Fee, as set by With simplified pricing, the interchange amount, as set by the the card brands, is passed through to the merchant. card brands, is passed through by Moneris to the merchant. As a result, merchants will benefit from increased visibility and exposure to interchange rate updates periodically announced by the card brands, including reductions or special programs. What is the Transaction Fee? The Transaction Fee is the fee paid to Moneris for the credit and debit card transaction processing, clearing, settlement, reporting and customer service it provides your business. -

200Th Annual Report 2017 TOMORROW TODAY STARTS We Aren’T Waiting Marla Philpot Associate Project Manager Chicago, IL for the Future to Arrive

BMO Financial Group 200th Annual Report 2017 TOMORROW TODAY STARTS We aren’t waiting Marla Philpot Associate Project Manager Chicago, IL for the future to arrive. We’re creating it. Connecting. Learning. Ervey Ayvar Coordinator, Administrative Services, U.S. Finance Adapting. Innovating. Chicago, IL Business Review 2 Who We Are / Finding new ways Financial Snapshot 3 Reasons to Invest in BMO 4 Chairman’s Message to be relevant. 5 Chief Executive Officer’s Message 9 Priorities and Principles 10 Tomorrow Starts Today 16 Performance Highlights Ready for what Gerrick Ratliff 18 Our Strategic Footprint Human Resources 20 Executive Committee Consultant Chicago, IL 21 Board of Directors comes next. Financial Review 24 Financial Performance and Condition at a Glance 26 Management’s Discussion and Analysis 122 Supplemental Information 136 Statement of Management’s Responsibility for Financial Information 137 Independent Auditors’ Report of Registered Public Accounting Firm 138 Report of Independent Registered Public Accounting Firm 139 Consolidated Financial Statements 144 Notes to Consolidated Financial Statements Resources and Directories 202 Glossary of Financial Terms 2 017 204 Where to Find More Information IBC Shareholder Information Financial Snapshot Who We Are Reported Adjusted 1 Established in 1817, BMO Financial Group is As at or for the year ended October 31 a highly diversified financial services provider (Canadian $ in millions, except as noted) 2017 2016 2017 2016 based in North America. We are the eighth- Revenue, net of CCPB2 (p 38) 20,722 19,544 20,722 19,628 largest bank in North America by assets, with Provision for credit losses (p 42) 774 815 850 815 total assets of $710 billion and an engaged Non-interest expense (p 43) 13,302 12,997 13,007 12,544 and diverse base of employees. -

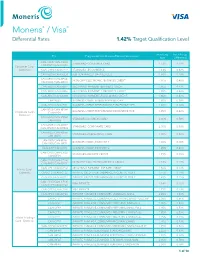

Moneris® / Visa® Differential Rates 1.42% Target Qualification Level

Moneris® / Visa® Differential Rates 1.42% Target Qualification Level Interchange Interchange Fee Program As Identified on Moneris Statements: Rate Differential CAN-CS01/CAN-CS02/ STANDARD–CONSUMER CARD 1.52% 0.10% CAN-DS01/CAN-DS02 Consumer Card - Domestic CAN-C918/CAN-C919 STANDARD -ECOMMERCE 1.44% 0.02% CAN-XED3/CAN-XED4 B2B - ENHANCED DATA LEVEL 2 1.60% 0.18% CAN-XE03/CAN-XE04/ NON-CHIP ELECTRONIC–BUSINESS CREDIT 1.90% 0.48% CAN-VE03/CAN-WE03 CAN-XB03/CAN-XB04 RECURRING PAYMENT–BUSINESS CREDIT 1.85% 0.43% CAN-XB05/CAN-XB06 RECURRING PAYMENT–CORPORATE CREDIT 1.85% 0.43% CAN-XB07/CAN-XB08 RECURRING PAYMENT–PURCHASING CREDIT 1.85% 0.43% CAN-XE33 BUSINESS CREDIT EMERGING NNSS-CHIP 1.80% 0.38% CAN-XP01/CAN-XP02 BUSINESS CREDIT PERFORMANCE INCENTIVE TIER 1.80% 0.38% CAN-XP03/CAN-XP04/ BUSINESS CREDIT,PERFORMANC EINCENTIVE TIER 1.85% 0.43% Corporate Card - CAN-VP04 Domestic CAN-XS03/CAN-XS04/ STANDARD–BUSINESS CARD 2.00% 0.58% CAN-WS03 CAN-XS05/CAN-XS06/ STANDARD–CORPORATE CARD 2.00% 0.58% CAN-WS05/CAN-WS06 CAN-XS07/CAN-XS08/ STANDARD–PURCHASING CARD 2.00% 0.58% CAN-WS07 CAN-XI05/CAN-XI06/ BUSINESS CREDIT,INDUSTRY 1 1.80% 0.38% CAN-VI05/CAN-WI05 CAN-XI07/CAN-XI08 BUSINESS CREDIT,INDUSTRY 2 1.85% 0.43% CAN-CF01/CAN-CF02/ STANDARD–INFINITE CREDIT 1.71% 0.29% CAN-DF01 CAN-CF07/CAN-CF08/ NON-CHIP ELECTRONIC–INFINITE CREDIT 1.61% 0.19% CAN-EF07/CAN-DF07 CAN-CF11/CAN-CF12 RECURRING PAYMENT–INFINITE CREDIT 1.56% 0.14% Infinite Card - Domestic CAN-CF21/CAN-CF22 INFINITE CREDIT PERFORMANCE INCENTIVE TIER 1 1.56% 0.14% CAN-CF23/CAN-CF24 INFINITE CREDIT