Annual Report 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Impact of Coal Fired Power Plant Emissions on Ambient Air Quality Using a Diffusion Model

IMPACT OF COAL FIRED POWER PLANT EMISSIONS ON AMBIENT AIR QUALITY USING A DIFFUSION MODEL by MASHIAT HOSSAIN (Std. ID: 0417042144 P) A thesis submitted to Department of Civil Engineering, Bangladesh University of Engineering and Technology, Dhaka in partial fulfillment of the requirements for the degree of MASTER OF SCIENCE IN CIVIL ENGINEERING (ENVIRONMENTAL) DEPARTMENT OF CIVIL ENGINEERING BANGLADESH UNIVERSITY OF ENGINEERING & TECHNOLOGY, DHAKA JUNE, 2019 The thesis titled “Impact of Coal Fired Power Plant Emissions on Ambient Air Quality using a Diffusion Model” submitted by Mashiat Hossain, Roll No.: 0417042144 P, Session: April, 2017 has been accepted as satisfactory in partial fulfillment of the requirement for the degree of Master of Science in Civil Engineering (Environmental) on June 12, 2019. BOARD OF EXAMINERS jkkkkkkkkkkkkkkkkkkkkkjjjjjjjjk Dr. Muhammad Ashraf Ali Chairman Professor (Supervisor) Dept. of Civil Engineering, BUET. jjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjjj Dr. Ahsanul Kabir Member Professor & Head of the Dept. (Ex-Officio) Dept. of Civil Engineering, BUET. hhhhhhhhhhhhhhhhhhhhhhhnnnn Dr. Tanvir Ahmed Member Associate Professor Dept. of Civil Engineering, BUET. hhhhhhhhhhhhhhhhhhhhhhhnnnn Dr. Provat Kumar Saha Member Assistant Professor Dept. of Civil Engineering, BUET. hhhhhhhhhhhhhhhhhhhhhhhhhhhhh Dr. Ganesh Chandra Saha Member Professor (External) Dept. of Civil Engineering, DUET Gazipur. ii Declaration It is hereby declared that the studies embodied in this thesis are the results of experiments carried -

Problems and Progress Towards Sustainable Power

2nd Foundation Training Course th th 08 July to 18 September 2020 Problems and Progress towards Sustainable Power Supervised by: Sheikh Faezul Amin Joint Secretary, Power Division, Ministry of Power, Energy and Mineral Resources Submitted by: Group – 06 Md. Dolu Mia (2160) Md. Toufique Aziz (2201) Muhammad Tanvirul Hasan (2234) Mohammad Shamsur Rahman (2235) Md. Zillur Rahman Bhuiyan (2236) Fariha Sadeque (2237) Md. Arafat Ul Huq (2240) 1 September, 2020 Acknowledgement Firstly all praises and thanks to the Almighty Allah for His showers of blessings for giving us strength, ability and knowledge to finish the research work. We would like to express our deep and sincere gratitude to our research supervisor, Mr. Sheikh Faezul Amin, Joint Secretary, Power Division, for giving us the opportunity to do research on “Problems and Progress towards Sustainable Power” and providing invaluable guidance throughout this research. His dynamism, vision, sincerity and motivation have deeply inspired us. He has taught us the methodology to carry out the research and to present the research works as clearly as possible. It was a great privilege and honor to work and study under his guidance. We are extremely grateful for what he has offered us. We would also like to thank him for his friendship, empathy, and great sense of humor. We are extremely grateful to each member of our group for everyone’s genuine collaboration throughout this research work. We are extending our thanks to the Principal Adviser: Md. Mahbub-ul-Alam, NDC, Rector, BPMI, Course Adviser: Md. Golam Rabbani, MDS (Admin & Finance), BPMI, Course Director: Mohammad Rafiqul Islam, Director (Training), BPMI. -

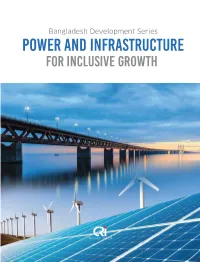

Power and Infrastructure for Inclusive Growth

Bangladesh Development Series Power and Infrastructure for Inclusive Growth Bangladesh Development Series Power and Infrastructure for Inclusive Growth Introduction The present Awami League government led by Prime Minister Sheikh Hasina earmarked on a host of mega infrastructural projects to transform the future of the country and to change the course of national progress. To this end, a good number of projects have been put under the Fast-Track scheme, which have been envisaged, introduced and supervised by Honorable Prime Minister Sheikh Hasina herself, resulting in full swing progress being accomplished. Some major aspects in the transport and power development policy action were considered by the present government for sustainable development in Bangladesh. The goals of transforming to an efcient transport system was linked with fostering economic development, enhancing the quality of the environment, reducing energy consumption, promoting transportation-friendly development patterns and encouraging fair and equitable access and safe mobility to residents of different socioeconomic groups. From Padma Multipurpose Bridge, to the country’s rst ever nuclear power plant, and the deep sea port are some of such dream projects, rolled out to boost up the wheel of national progress, seeing substantial progress. On impact, lives in long deprived regions have started to change, horizons for businesses are opening up fast, employment opportunities are being created, and the inux of international investment is rising, adding further impetus to the national growth. Table of Contents Introduction 01. Power and Energy Initiatives 05 02. Flagship Power Plant Projects 12 03. Infrastructure for Inclusive Growth 19 04. Rapid Transit for Dhaka Commuters 24 05. -

Country Report Bangladesh August 2019

_________________________________________________________________________________________________________________________________________________________ Country Report Bangladesh Generated on August 13th 2019 Economist Intelligence Unit 20 Cabot Square London E14 4QW United Kingdom _________________________________________________________________________________________________________________________________________________________ The Economist Intelligence Unit The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For 60 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide. The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group. London New York The Economist Intelligence Unit The Economist Intelligence Unit 20 Cabot Square The Economist Group London 750 Third Avenue E14 4QW 5th Floor United Kingdom New York, NY 10017, US Tel: +44 (0) 20 7576 8181 Tel: +1 212 541 0500 Fax: +44 (0) 20 7576 8476 Fax: +1 212 586 0248 E-mail: [email protected] E-mail: [email protected] Hong Kong Geneva The Economist Intelligence Unit The Economist Intelligence Unit 1301 Cityplaza Four Rue de l’Athénée 32 12 Taikoo Wan Road 1206 Geneva Taikoo Shing Switzerland Hong Kong Tel: +852 2585 3888 Tel: +41 22 566 24 70 Fax: +852 2802 7638 Fax: +41 22 346 93 47 E-mail: [email protected] E-mail: [email protected] This report can be accessed electronically as soon as it is published by visiting store.eiu.com or by contacting a local sales representative. -

MGI Newsletter English 10.5''X15''

Issue 01 || Volume 01 QUARTERLY NEWSLETTER New Product Launch Employees First TOP NEWS INSIDE Awards & Achievements Quiz Questions Successful Campaigns Get to Know EDITORIAL EDITORS’ NOTE EDITORIAL TEAM Dear readers and reviewers of 'Breaking Advisory Board Boundaries' Tanveer Mostafa It gives me immense pleasure to welcome Kazi Md. Mohiuddin you to the first edition of Breaking Boundaries. Firstly, a huge amount of heartfelt appreciation is due to everyone Project Manager who has successfully breathed life into Faisal Rahman this collective dream- especially Tanveer Elora Majumder Mostafa (Director), Kazi Md. Mohiuddin (Sr. GM, Brand), the Corporate Brand Team and the In-house Design Team. Creative and Graphic Without your immense support, none of Md. Habibullah Al Habib this would have been possible. The entire Monsorul Alam newsletter is the outcome of months of efforts by all. Coordinator Let’s get a quick idea of the whole journey. Md. Omar Faruque Our cover page will give you an idea of the Chowdhury Md Tanim major events that we have conducted, and Istiack Rashid going further to this- you will explore how it has impacted our organization. Furthermore, we have talked about our Contributors new product developments, launches, Sadia Islam Ema innovations, along with some positive Mukim Hasan initiatives that MGI has taken and participated in. This will be a good Masab Nur Rahman opportunity for you to learn about our Najirun Khan Pathan Raihan massive organization just by glancing Rumana Afrose properly on a few pages. Sunjeeda Parvin The last part is dedicated especially to all Fahim Bin Najib our colleagues. It includes segments of all Tanvir Wahid Lashker the hidden talents that we have and also Apurbo Islam Mashuk contains an interesting section where our employees get to participate directly by answering a few questions. -

Securing Space and Access for Marginalized Fishing Communities in an Industrialized Ocean: How Bangladesh Is Going to Experience It?

Securing Space and Access for Marginalized Fishing Communities in an Industrialized Ocean: How Bangladesh is going to experience it? A Research Paper presented by: Peerzadi Farzana Hossain (Bangladesh) in partial fulfilment of the requirements for obtaining the degree of MASTER OF ARTS IN DEVELOPMENT STUDIES Major: Agrarian, Food and Environmental Studies (AFES) Specialization: Environment and Sustainable Development Members of the Examining Committee: Murat Arsel, PhD Christina Sathyamala, PhD The Hague, The Netherlands December 2020 ii Contents List of Tables v List of Figures v List of Maps v List of Appendices v List of Acronyms vi Abstract viii Chapter 1 Introduction 1 1.1 Background of Bangladesh’s blue economy 1 1.2 Competing interpretations of blue economy 2 1.3 Small-scale commercial fishing units of Bangladesh 4 1.3.1 Characteristics of fishing fleets and units 4 1.3.2 Organization of small-scale commercial units 5 1.3.3 Why small-scale commercial fishing units? 7 1.3.4 Regulatory framework for marine fisheries 7 1.4 Research Problem Statement 8 1.5 Research questions 9 1.6 Analytical framework 9 Chapter 2 Methodology 11 2.1 Literature review 11 2.2 Individual interviews 12 2.3 Group interviews 12 2.5 Description of field site 13 2.6 Positionality, reflexivity and limitations 14 2.7 Scope and challenges 15 Chapter 3 Findings on blue economy narratives 17 3.1 ‘Blue economy’ in the context of Bangladesh 17 3.2 Quantitative validation from literature 19 3.3 Experts’ reflection on blue economy trajectories and concerns 22 3.3.1 -

A Path to Renewable Energy from the Energy Crisis in Bangladesh

Journal of Engineering Research and Reports 11(2): 6-19, 2020; Article no.JERR.55315 ISSN: 2582-2926 A Path to Renewable Energy from the Energy Crisis in Bangladesh Zafrin Ahmed Liza1, Hajera Akhter2, Md. Shahibuzzaman1 and Mohammad Rakibul Islam3* 1Department of Anthropology, Shahjalal University of Science and Technology (SUST), Sylhet-3114, Bangladesh. 2Department of Political Science, Shahjalal University of Science and Technology (SUST), Sylhet-3114, Bangladesh. 3Department of Electrical and Electronic Engineering, Islamic University of Technology (IUT), Gazipur-1704, Bangladesh. Authors’ contributions This work was carried out in collaboration among all authors. Author ZAL designed the study, managed the literature searches, organized different sections and wrote the social impact part, authors HA and MS wrote the first draft of the manuscript and author MRI performed the technical analysis part. All authors read and approved the final manuscript. Article Information DOI: 10.9734/JERR/2020/v11i217055 Editor(s): (1) Dr. Felipe Silva Semaan, Federal University, Brazil. Reviewers: (1) Bankole Adebanji, Ekiti State University, Nigeria. (2) Wen-Yeau Chang, St. John’s University, Taiwan. (3) Guy Clarence Semassou, University of Abomey-Calavi, Benin. (4) Alfred Ba’amani Ba’ams, Modibbo Adama University of Technology, Nigeria. Complete Peer review History: http://www.sdiarticle4.com/review-history/55315 Received 06 January 2020 Original Research Article Accepted 11 March 2020 Published 20 March 2020 ABSTRACT Bangladesh is facing a tremendous energy crisis and the economic development of this country was jeopardized due to the lack of energy resources. Due to the progression of technology, the consumption of power is rising gradually. Adequate and consistent source of electricity is a key requirement for a constant and successful economic development. -

Daily News Flash

DSEX 5,748.31 0.29% Gold (Ounce) $1,311.30 CSCX 10,646.57 0.25% Oil (Barrel) $63.84 Daily News Flash 14th February 2019 Sell Sell Dollar 83.20 84.40 GBP 105.75 109.75 Sell Sell Euro 93.80 97.80 Rupee 1.16 1.24 Table of Contents Macro Economy ............................................................................................................ 1 HC ORDERS LIST OF MONEY LAUNDERERS, LOAN DEFAULTERS ........................................................................ 1 BUSINESSES TO HELP IN NEW VAT LAW IMPLEMENTATION ................................................................................. 2 BB WARNS OF FRAUD IN FINTECH SERVICES ............................................................................................................... 3 EXPORT PERFORMANCE OF MANY SECTORS FALLS SHORT OF EXPECTATIONS ......................................... 4 THREE INVESTMENT DEALS EXPECTED TO BE SIGNED ........................................................................................... 6 COAL IMPORT FOR PAYRA POWER PLANT BY AUGUST LIKELY .......................................................................... 7 FSRU GAS SUPPLY TO NAT'L GRID RISES TO 450 MMCFD ........................................................................................ 7 SERVICE SECTOR'S H1 EXPORT EARNINGS SOAR OVER 50PC ............................................................................... 8 GOVT RELAXES CONTRACT FARMING TERM FOR NON-EUROPEAN MARKETS ............................................. 9 DEAL ON PAYRA PORT MASTER PLAN TODAY .......................................................................................................... -

Budget Speech 2021-2022

Bangladesh Towards a Resilient Future Protecting Lives And Livelihoods National Budget Speech 2021-2022 A H M Mustafa Kamal FCA, MP Minister Ministry of Finance Government of the People’s Republic of Bangladesh 20 Jaisthya 1428 03 June 2021 ii Table of Content Topic Page Chapter I Tribute Profound Respect and Gratitude to the Father of the Nation 1-2 Bangabandhu Sheikh Mujibur Rahman and all the martyrs in the independence war Chapter II Birth Centenary of Sheikh Mujib and the Golden Jubilee of Independence Celebration of the Birth Centenary of Bangabandhu Sheikh 3-14 Mujib and the Golden Jubilee of Independence; the position of Bangladesh in the field of economy Chapter III Graduating to the status of a developing country and the journey onward Bangladesh becomes eligibile for graduation into a 15-20 developing country; Post-graduation challenges as a developing country; Strategies to deal with the post- graduation situation Chapter IV COVID-19 Pandemic and Economic Recovery The impact of COVID-19 pandemic in Bangladesh; 21-25 implementation of fiscal packages for economic recovery from COVID-19 impact; Assistance from Development Partners to combat COVID-19 impact. Chapter V Perspective and Background: Global Economy and Bangladesh Global economic forecasts amid the COVID-19 pandemic; 26-28 Current economic position and the image of Bangladesh i Topic Page Chapter VI The Supplementary Budget The Supplementary Budget for the current FY 2020-2021; 29-30 Revised Revenue Income and Revised Expenditure; Revised Budget Deficit and its Financing -

Election Manifesto 2018

Allah is Great Joy Bangla Joy Bangabandhu Bangladesh on the march towards Prosperity Election Manifesto 2018 Bangladesh Awami League Election Manifesto 2018 Bangladesh on the march towards Prosperity 11th National Parliament Election-2018 Election Manifesto of Bangladesh Awami League Bangladesh Awami League Election Manifesto 2018 CONTENTS 1.0 Our Special Undertakings 5 2.0 Background 6 2.1 Glorious Five Years (June 1996-July 2001): 8 The Golden Period of fulfilling the aspirations of Freedom 2.2 BNP-Jamaat Alliance government (October 2001 to 10 November 2006): People’s resistance against plunder, misrule and violence 2.3 The regime of Caretaker government: Conspiracy against 12 Democracy and Way to overcome 2.4 The Awami League Tenure (January 2009-December 2013): 13 Transcending Crises and March towards a New Dawn 2.5 Awami League Tenure (January 2014 - December 2018): 15 Bangladesh – a Miracle on the path of Development and Prosperity 3.0 Running the Government on two Terms: Success and 17 Achievements in (2009-2018): Objectives and Plan for the next Five Years (2019-2023) 3.1 Democracy, Election and Functional Parliament 17 3.2 The Rule of Law and Human Rights Protection 18 3.3 Efficient, Service-oriented and Accountable Administration 20 3.4 Developing a Citizen-friendly Law and Order Enforcing Agency 21 3.5 Policy of Zero-Tolerance against Corruption 22 3.6 Violence, Terrorism, Communalism and 23 Eradication of Drugs 3.7 Local Government: Empowerment of the People 24 3.8 Macroeconomy: High Income, Sustainable and 26 Inclusive -

Vol 17 Issue 14 All.Pdf

Editor Fortnightly Magazine, Vol 17, Issue 14, January 1-15 Mollah M Amzad Hossain Advisory Editor Anwarul Islam Tarek Mortuza Ahmad Faruque Saiful Amin International Editor Dr. Nafis Ahmed Contributing Editors Saleque Sufi Online Editor GSM Shamsuzzoha (Nasim) Managing Editor Afroza Hossain Bangabandhu’s policy was to ensure hassle-free power supply at affordable price Magazine Administrator for achieving economic development of the country. His strategy was to utilize AKM Shamsul Hoque own resources instead of dependence on imported fuel. Bangladesh in its long Reporters Arunima Hossain journey of about 50 years since independence made significant progress — be it in Mohiuddin Miah terms of the economy or other areas. The energy sector is not also lagging behind. Assistant Online Editor The power subsector has made remarkable progress particularly in generation Aditya Hossain thanks to tremendous efforts especially over the last 11 years. The overcapacity of Design & Graphics Md. Monirul Islam late drew some criticisms though. However, one of the major issues of concern is Photography that the country is gradually getting dependent on imported fuel, putting price Bulbul Ahmed pressure on the consumers. There is a projection that the country is approaching Production towards 90 percent dependence on the imported fuel. Ultimately, the consumers Mufazzal Hossain Joy Computer Graphics will have to bear the brunt. Md. Uzzal Hossain The main challenge is to increase the contribution of own fuel to the fuel mix to Circulation Assistant limit the power generation cost. It is not an easy task, however. But, hectic efforts Khokan Chandra Das Editorial, News & Commercial should be there for exploring own primary fuel alongside taking a realistic plan to Room 509, Eastern Trade Center limit the use of imported fuel to its lowest possible level. -

Bangladesh) (798) Les Sundarbans (Bangladesh) (798)

World Heritage 44 COM Patrimoine mondial Paris, 30 March 2021 Original: English UNITED NATIONS EDUCATIONAL, SCIENTIFIC AND CULTURAL ORGANIZATION ORGANISATION DES NATIONS UNIES POUR L'EDUCATION, LA SCIENCE ET LA CULTURE CONVENTION CONCERNING THE PROTECTION OF THE WORLD CULTURAL AND NATURAL HERITAGE CONVENTION CONCERNANT LA PROTECTION DU PATRIMOINE MONDIAL, CULTUREL ET NATUREL WORLD HERITAGE COMMITTEE / COMITE DU PATRIMOINE MONDIAL Extended forty-fourth session / Quarante-quatrième session élargie Fuzhou (China) / Online meeting / Fuzhou (Chine) / Réunion en ligne 16 - 31 July 2021 / 16 – 31 juillet 2021 Item 7 of the Provisional Agenda: State of conservation of properties inscribed on the World Heritage List and/or on the List of World Heritage in Danger Point 7 de l’Ordre du jour provisoire : Etat de conservation de biens inscrits sur la Liste du patrimoine mondial et/ou sur la Liste du patrimoine mondial en péril MISSION REPORT / RAPPORT DE MISSION The Sundarbans (Bangladesh) (798) Les Sundarbans (Bangladesh) (798) 9-17 December/décembre 2019 REPORT ON THE JOINT UNESCO/IUCN REACTIVE MONITORING MISSION TO THE SUNDARBANS, BANGLADESH FROM 9 TO 17 DECEMBER 2019 Photo: © G. Broucke/UNESCO Guy Broucke (UNESCO) Akane Nakamura (UNESCO World Heritage Centre) Elena Osipova (IUCN) Andrew Wyatt (IUCN) October 2020 1/73 TABLE OF CONTENTS TABLE OF CONTENTS ............................................................................................................. 2 LIST OF ACRONYMS ...............................................................................................................