RETAIL REAL ESTATE Southeast US Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Track Record of Prior Experience of the Senior Cobalt Team

Track Record of Prior Experience of the Senior Cobalt Team Dedicated Executives PROPERTY City Square Property Type Responsibility Company/Client Term Feet COLORADO Richard Taylor Aurora Mall Aurora, CO 1,250,000 Suburban Mall Property Management - New Development DeBartolo Corp 7 Years CEO Westland Center Denver, CO 850,000 Suburban Mall Property Management and $30 million Disposition May Centers/ Centermark 9 Years North Valley Mall Denver, CO 700,000 Suburban Mall Property Management and Redevelopment First Union 3 Years FLORIDA Tyrone Square Mall St Petersburg, FL 1,180,000 Suburban Mall Property Management DeBartolo Corp 3 Years University Mall Tampa, FL 1,300,000 Suburban Mall Property Management and New Development DeBartolo Corp 2 Years Property Management, Asset Management, New Development Altamonte Mall Orlando, FL 1,200,000 Suburban Mall DeBartolo Corp and O'Connor Group 1 Year and $125 million Disposition Edison Mall Ft Meyers, FL 1,000,000 Suburban Mall Property Management and Redevelopment The O'Connor Group 9 Years Volusia Mall Daytona Beach ,FL 950,000 Suburban Mall Property and Asset Management DeBartolo Corp 1 Year DeSoto Square Mall Bradenton, FL 850,000 Suburban Mall Property Management DeBartolo Corp 1 Year Pinellas Square Mall St Petersburg, FL 800,000 Suburban Mall Property Management and New Development DeBartolo Corp 1 Year EastLake Mall Tampa, FL 850,000 Suburban Mall Property Management and New Development DeBartolo Corp 1 Year INDIANA Lafayette Square Mall Indianapolis, IN 1,100,000 Suburban Mall Property Management -

Michael Kors® Make Your Move at Sunglass Hut®

Michael Kors® Make Your Move at Sunglass Hut® Official Rules NO PURCHASE OR PAYMENT OF ANY KIND IS NECESSARY TO ENTER OR WIN. A PURCHASE OR PAYMENT WILL NOT INCREASE YOUR CHANCES OF WINNING. VOID WHERE PROHIBITED BY LAW OR REGULATION and outside the fifty United States (and the District of ColuMbia). Subject to all federal, state, and local laws, regulations, and ordinances. This Gift ProMotion (“Gift Promotion”) is open only to residents of the fifty (50) United States and the District of ColuMbia ("U.S.") who are at least eighteen (18) years old at the tiMe of entry (each who enters, an “Entrant”). 1. GIFT PROMOTION TIMING: Michael Kors® Make Your Move at Sunglass Hut® Gift Promotion (the “Gift ProMotion”) begins on Friday, March 22, 2019 at 12:01 a.m. Eastern Time (“ET”) and ends at 11:59:59 p.m. ET on Wednesday, April 3, 2019 (the “Gift Period”). Participation in the Gift Promotion does not constitute entry into any other promotion, contest or game. By participating in the Gift Promotion, each Entrant unconditionally accepts and agrees to comply with and abide by these Official Rules and the decisions of Luxottica of America Inc., 4000 Luxottica Place, Mason, OH 45040 d/b/a Sunglass Hut (the “Sponsor”) and WYNG, 360 Park Avenue S., 20th Floor, NY, NY 10010 (the “AdMinistrator”), whose decisions shall be final and legally binding in all respects. 2. ELIGIBILITY: Employees, officers, and directors of Sponsor, Administrator, and each of their respective directors, officers, shareholders, and employees, affiliates, subsidiaries, distributors, -

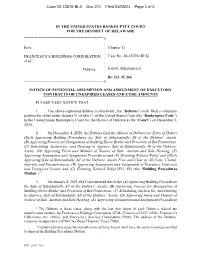

271 Filed 01/06/21 Page 1 of 5

Case 20-13076-BLS Doc 271 Filed 01/06/21 Page 1 of 5 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x : In re: : Chapter 11 : FRANCESCA’S HOLDINGS CORPORATION, Case No. 20-13076 (BLS) 1 : et al., : : Debtors. Jointly Administered : : Re: D.I. 45, 266 ------------------------------------------------------------ x NOTICE OF POTENTIAL ASSUMPTION AND ASSIGNMENT OF EXECUTORY CONTRACTS OR UNEXPIRED LEASES AND CURE AMOUNTS PLEASE TAKE NOTICE THAT: 1. The above-captioned debtors (collectively, the “Debtors”) each filed a voluntary petition for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Delaware (the “Court”) on December 3, 2020. 2. On December 4, 2020, the Debtors filed the Motion of Debtors for Entry of Orders (I)(A) Approving Bidding Procedures for Sale of Substantially All of the Debtors’ Assets, (B) Approving Process for Designation of Stalking Horse Bidder and Provision of Bid Protections, (C) Scheduling Auction for, and Hearing to Approve, Sale of Substantially All of the Debtors’ Assets, (D) Approving Form and Manner of Notices of Sale, Auction and Sale Hearing, (E) Approving Assumption and Assignment Procedures and (F) Granting Related Relief and (II)(A) Approving Sale of Substantially All of the Debtors’ Assets Free and Clear of All Liens, Claims, Interests and Encumbrances, (B) Approving Assumption and Assignment of Executory Contracts and Unexpired Leases -

National Hot Dog Month

NATIONAL HOT DOG DAY PROMOTION ‐ PRETZELMAKER Participating Store List ADDRESS I ADDRESS II CITY STATE ZIP PHONE NUMBER Brookwood Village 724 Brookwood Village Birmingham AL 35209 (205) 871‐1333 Parkway Place Mall 2801 Memorial Parkway SW Huntsville AL 35801 (205) 539‐3255 The Shoppes at EastChase 7048 EastChase Parkway Montgomery AL 36117 (334) 356‐8111 Regency Mall 301 Cox Creek Parkway,Space #1302 Florence AL 35630 (256) 760‐1980 Central Mall 5111 Rogers Avenue Fort Smith AR 72903 (479) 452‐2525 Desert Sky Mall 7611 West Thomas Rd. Phoenix AZ 85033 (623) 873‐1540 Foothills Mall ‐ Bakery Cafe 7401 N La Cholla Blvd #155 Tucson AZ 85741 (520) 531‐8404 Tucson Mall 4500 N Oracle Rd Suite 212 Tucson AZ 85705 Flagstaff Mall 4650 Northe Highway 89 Flagstaff AZ 86004 Park Place Mall 5870 East Broadway, #K‐9 Tuscon AZ 85711 Del Monte Mall 520 Del Monte Center, U‐526 Monterey CA 93940 (831) 646‐0243 Bayshore Mall 3300 Broadway Spc #304A Eureka CA 95501 (707) 444‐9595 Weberstown Mall 4950 Pacific Ave Stockton CA 95207 (209) 474‐3466 Folsom Premium Outlet 13000 Folsom Blvd.,Suite 210 Folsom CA 95630‐0002 (916) 351‐1448 Galleria at Roseville 1151 Galleria Blvd.,#276 Roseville CA 95678 (916) 878‐5418 Sunrise Mall 6138 Sunrise Mall Citrus Heights CA 95610 (916) 723‐7197 Solano Town Center 1350 Travis Blvd, Space FC98 Fairfield CA 94533 Fashion Square at Sherman 14006 Riverside Drive,Space #86 Sherman Oaks CA 91423‐6300 (818) 990‐7161 Antelope Valley Mall 1233 kW. Rancho Vista Blvd., #1111 Palmdale CA 93551 (661) 947‐8444 Moreno Valley Mall 22500 Town Cir Ste 1205 Moreno Valley CA 92553 (951) 653‐2557 The Oaks Mall 378 W. -

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 Gamestop Dimond Center 80

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 GameStop Dimond Center 800 East Dimond Boulevard #3-118 Anchorage AK 99515 665 1703 (907) 272-7341 GameStop Anchorage 5th Ave. Mall 320 W. 5th Ave, Suite 172 Anchorage AK 99501 665 6139 (907) 332-0000 GameStop Tikahtnu Commons 11118 N. Muldoon Rd. ste. 165 Anchorage AK 99504 665 6803 (907) 868-1688 GameStop Elmendorf AFB 5800 Westover Dr. Elmendorf AK 99506 75 1833 (907) 474-4550 GameStop Bentley Mall 32 College Rd. Fairbanks AK 99701 665 3219 (907) 456-5700 GameStop & Movies, Too Fairbanks Center 419 Merhar Avenue Suite A Fairbanks AK 99701 665 6140 (907) 357-5775 GameStop Cottonwood Creek Place 1867 E. George Parks Hwy Wasilla AK 99654 665 5601 (205) 621-3131 GameStop Colonial Promenade Alabaster 300 Colonial Prom Pkwy, #3100 Alabaster AL 35007 701 3915 (256) 233-3167 GameStop French Farm Pavillions 229 French Farm Blvd. Unit M Athens AL 35611 705 2989 (256) 538-2397 GameStop Attalia Plaza 977 Gilbert Ferry Rd. SE Attalla AL 35954 705 4115 (334) 887-0333 GameStop Colonial University Village 1627-28a Opelika Rd Auburn AL 36830 707 3917 (205) 425-4985 GameStop Colonial Promenade Tannehill 4933 Promenade Parkway, Suite 147 Bessemer AL 35022 701 1595 (205) 661-6010 GameStop Trussville S/C 5964 Chalkville Mountain Rd Birmingham AL 35235 700 3431 (205) 836-4717 GameStop Roebuck Center 9256 Parkway East, Suite C Birmingham AL 35206 700 3534 (205) 788-4035 GameStop & Movies, Too Five Pointes West S/C 2239 Bessemer Rd., Suite 14 Birmingham AL 35208 700 3693 (205) 957-2600 GameStop The Shops at Eastwood 1632 Montclair Blvd. -

Montgomery, AL 36116 392 Units

| EXCLUSIVE MULTIFAMILY OFFERING DAVID OAKLEY Senior Vice President 205.918.0785 [email protected] DAVID ETCHISON Senior Associate 205.918.0785 [email protected] 5800 Eagle Circle | Montgomery, AL 36116 ROYCE EMERSON 392 Units | Built: 1986 | $15,000,000 Senior Associate 205.918.0785 [email protected] Attractive Double-Digit Cash-on-Cash Returns Superior Unit Mix and Amenities Value-Add Opportunity through Interior Upgrad Employment Growth Outpacing National Average For Real-Time Property Information go to: eaglelanding.hpapts.com DAVID OAKLEY Attractive Double-Digit Cash-on-Cash Returns Senior Vice President 205.918.0785 Superior Unit Mix and Amenities [email protected] DAVID ETCHISON Value-Add Opportunity through Interior Upgrad Senior Associate 205.918.0785 Employment Growth Outpacing National Average [email protected] ROYCE EMERSON Senior Associate 205.918.0785 [email protected] For Real-Time Property Information Scan QR code or go to: eaglelanding.hpapts.com Alabama Office 2120 16th Avenue South Suite 101 HENDRICKS & PARTNERS IS NOW HENDRICKS-BERKADIA Birmingham, Alabama 35205 To find out more visit HendricksBerkadia.com/merger Phone: 205.918.0785 Fax: 205.918.0786 hendricksberkadia.com apartmentupdate.com THE ASSET The Opportunity 1 Property Summary 3 Upgraded Units 5 Location Description 6 Location Map 8 Aerials 9 Floor Plans 12 Property Photos 13 VALUATION Financial Analysis 16 Notes to Pro Forma 23 MARKET POSITIONING Comparable Rental Properties 25 Comparable Sale Properties 30 APPENDIX Economic & Demographic Profile 32 Demographics 37 EAGLE LANDING eaglelanding.hpapts.com THE OPPORTUNITY Hendricks-Berkadia is pleased to announce the exclusive opportunity to acquire Eagle Landing, a 392-unit garden style apartment community in the rejuvenated Eastern submarket of Montgomery, Alabama. -

NPD Participating Store List 2017

PRETZELMAKER National Pretzel Day Participating Store List ADDRESS I ADDRESS II CITY STATE ZIP PHONE NUMBER Village Mall Auburn 1627 Opelika Road,#10 Auburn AL 36830 (334) 821-8368 Brookwood Village 718 Brookwood Village Birmingham AL 35209 (205) 871-1333 Regency Mall 301 Cox Creek Parkway,Space #1302 Florence AL 35630 (256) 760-1980 Parkway Place Mall 2801 Memorial Parkway SW Huntsville AL 35801 (205) 539-3255 The Shoppes at EastChase 7048 EastChase Parkway Montgomery AL 36117 (334) 356-8111 Eastern Shore Centre 30500 State Hwy 181 Spc 810 Spanish Fort AL 36527 (251) 621-7977 Central Mall 5111 Rogers Avenue Fort Smith AR 72903 (479) 452-2525 Flagstaff Mall 4650 Northe Highway 89 Flagstaff AZ 86004 Desert Sky Mall 7611 West Thomas Rd. Phoenix AZ 85033 (623) 873-1540 Foothills Mall - Bakery Cafe 7401 N La Cholla Blvd #155 Tucson AZ 85741 (520) 531-8404 Tucson Mall 4500 N Oracle Rd Suite 212 Tucson AZ 85705 Park Place Mall 5870 East Broadway, #K-9 Tuscon AZ 85711 Sunrise Mall 6138 Sunrise Mall Citrus Heights CA 95610 (916) 723-7197 Solano Town Center 1350 Travis Blvd., Space B-13 Fairfield CA 94533 707-423-1942 Solano Town Center 1350 Travis Blvd, Space FC98 Fairfield CA 94533 Folsom Premium Outlet 13000 Folsom Blvd.,Suite 210 Folsom CA 95630-0002 (916) 351-1448 Del Monte Mall 520 Del Monte Center, U-526 Monterey CA 93940 (831) 646-0243 Moreno Valley Mall 22500 Town Cir Ste 1205 Moreno Valley CA 92553 (951) 653-2557 Galleria at Roseville 1151 Galleria Blvd.,#276 Roseville CA 95678 (916) 878-5418 Fashion Square at Sherman Oaks 14006 Riverside Drive,Space #86 Sherman Oaks CA 91423-6300 (818) 990-7161 Weberstown Mall 4950 Pacific Ave Stockton CA 95207 (209) 474-3466 The Oaks Mall 378 W. -

Pari Passu Loans in Cmbs 2.0 Last Updated: January 5, 2018

PARI PASSU LOANS IN CMBS 2.0 LAST UPDATED: JANUARY 5, 2018 % of % of Has Issuance Issuance Cut-Off Pari Master Special Master Special B DBRS Property State or Origination Trust Whole-Loan Balance at Passu Pari Passu Servicer Servicer Servicer Servicer Number note Rated Property Name Deal Name Type Country City Province Year Balance Balance Issuance in Deal Piece (Loan) (Loan) (Transaction) (Transaction) 1 no 111 Livingston Street CD 2017-CD3 Office US Brooklyn NY 2017 67,000,000 120,000,000 5.05% 55.83% A-1, A-3 Midland Midland Midland Midland 1 no 111 Livingston Street CGCMT 2017-P7 Office US Brooklyn NY 2017 29,000,000 120,000,000 2.83% 24.17% A-2 Midland Midland Wells Fargo Rialto 1 yes 111 Livingston Street CD 2017-CD4 Office US Brooklyn NY 2017 24,000,000 120,000,000 2.67% 20.00% A-4 Midland Midland Midland Rialto 2 yes 1155 Northern Boulevard PFP 2017-4 Office US Manhasset NY 2017 9,523,109 11,630,063 1.46% 81.88% N/A Wells Fargo Wells Fargo Wells Fargo Wells Fargo 1166 Avenue of the 3 yes yes BBCMS 2017-C1 Office US New York NY 2017 56,250,000 110,000,000 6.57% 66.18% A-1 Wells Fargo Rialto Wells Fargo Rialto Americas 1166 Avenue of the 3 yes yes WFCM 2017-RB1 Office US New York NY 2017 28,750,000 110,000,000 4.51% 33.82% A-2 Wells Fargo Rialto Wells Fargo C-III Americas 4 yes 123 William Street WFCM 2017-RB1 Office US New York NY 2017 62,500,000 140,000,000 9.80% 44.64% A-1 Wells Fargo C-III Wells Fargo C-III 4 yes 123 William Street MSC 2017-H1 Office US New York NY 2017 50,000,000 140,000,000 4.59% 35.71% A-2 Wells Fargo C-III -

Socio-Economic and Demographic Context

Market Feasibility Analysis Grayling Place Apartments Columbus, Muscogee County, Georgia Prepared for: TBG Residential Effective Date: April 30, 2018 Site Inspection: March 30, 2018 Grayling Place | Table of Contents TABLE OF CONTENTS EXECUTIVE SUMMARY ........................................................................................................... V 1. INTRODUCTION .............................................................................................................. 1 A. Overview of Subject .............................................................................................................................................. 1 B. Purpose of Report ................................................................................................................................................. 1 C. Format of Report .................................................................................................................................................. 1 D. Client, Intended User, and Intended Use ............................................................................................................. 1 E. Applicable Requirements ...................................................................................................................................... 1 F. Scope of Work ...................................................................................................................................................... 1 G. Report Limitations ............................................................................................................................................... -

Store # Store Name Dates Clinique Gift Is Running 140 3.3.17

Store # Store Name Dates Clinique Gift Is Running 140 0140 - TRIANGLE TOWN CENTER 3.3.17 - 3.22.17 141 0141 - CARY TOWN CENTER 3.3.17 - 3.22.17 143 0143 - ALAMANCE CROSSING 3.3.17 - 3.22.17 144 0144 - FOUR SEASONS 3.3.17 - 3.22.17 145 0145 - HANES 3.3.17 - 3.22.17 146 0146 - VALLEY HILLS MALL 3.3.17 - 3.22.17 148 0148 - ASHEVILLE MALL 3.3.17 - 3.22.17 150 0150 - SOUTH PARK 3.3.17 - 3.22.17 151 0151 - CAROLINA PLACE 3.3.17 - 3.22.17 152 0152 - EASTRIDGE MALL 3.3.17 - 3.22.17 153 0153 - NORTHLAKE MALL 3.3.17 - 3.22.17 156 0156 - WESTFIELD INDEPENDENCE MALL 3.3.17 - 3.22.17 161 0161 - CITADEL MALL 3.3.17 - 3.22.17 162 0162 - NORTHWOOD MALL 3.3.17 - 3.22.17 163 0163 - COASTAL GRAND 3.3.17 - 3.22.17 164 0164 - COLUMBIANA CENTRE 3.3.17 - 3.22.17 166 0166 - HAYWOOD MALL 3.3.17 - 3.22.17 167 0167 - WESTGATE MALL 3.3.17 - 3.22.17 168 0168 - ANDERSON MALL 3.3.17 - 3.22.17 170 0170 - MACARTHUR CENTER 3.3.17 - 3.13.17 171 0171 - LYNNHAVEN MALL 3.3.17 - 3.13.17 172 0172 - GREENBRIER MALL 3.3.17 - 3.13.17 174 0174 - PATRICK HENRY MALL 3.3.17 - 3.13.17 176 0176 - SHORT PUMP TOWN CENTER 3.3.17 - 3.13.17 179 0179 - STONY POINT 3.3.17 - 3.13.17 201 0201 - INTERNATIONAL PLAZA 3.3.17 - 3.22.17 203 0203 - CITRUS PARK TOWN CENTER 3.3.17 - 3.22.17 204 0204 - BRANDON TOWN CENTER 3.3.17 - 3.22.17 205 0205 - TYRONE SQUARE 3.3.17 - 3.22.17 206 0206 - COUNTRYSIDE MALL 3.3.17 - 3.22.17 207 0207 - GULFVIEW SQUARE 3.3.17 - 3.22.17 208 0208 - WIREGRASS 3.3.17 - 3.22.17 209 0209 - LAKELAND SQUARE 3.3.17 - 3.22.17 210 0210 - EAGLE RIDGE CENTER 3.3.17 - 3.22.17 213 0213 -

Dillard's Store Name: Wacoal Fi(Gh)T for the Cure ™

Wacoal Fi(gh)t for the Cure ™ Help Knockout Breast Cancer at a Fit for the Cure ® Event. Event Dillard's Store Name: City: State: Event Date: Hours: Parkway Place Huntsville AL 10/11/12 10-8 Eastern Shore Center Spanish Fort AL 10/5/12 10-8 Bel Air Mall Mobile AL 10/6/12 10-8 Wiregrass Commons Dothan AL 10/5/12 10-8 Quintard Mall Oxford AL 10/2/12 10-8 Village Mall Auburn AL 10/5/12 10-8 The Shoppes at Eastchase Montgomery AL 10/4/12 10-8 Regency Square Mall Florence AL 10/5/12 10-8 Park Plaza Little Rock AR 10/5/12 10-8 Hot Springs Mall Hot Springs AR 10/5/12 10-8 Northwest Arkansas Fayetteville AR 9/20/12 10-8 Pines Mall Pine Bluff AR 10/5/12 10-8 The Mall @ Turtle Creek Jonesboro AR 10/5/12 10-8 McCain Mall N. Little Rock AR 10/5/12 10-8 Pinnacle Hills Promenade Rogers AR 9/19/12 10-8 Central Mall Ft. Smith AR 9/21/12 10-8 Scottsdale Scottsdale AZ 10/26/12 10-8 Paradise Valley Phoenix AZ 10/25/12 10-8 Park Place Tucson AZ 10/18/12 10-8 Westridge/Desert Sky Mall Phoenix AZ 10/5/12 10-8 Arrowhead Towne Center Glendale AZ 10/19/12 10-8 Chandler Fashion Mall Chandler AZ 10/20/12 10-8 Superstition Mall Mesa AZ 10/5/12 10-8 San Tan Village Gilbert AZ 10/5/12 10-8 Prescott Gateway Prescott AZ 10/5/12 10-8 The Shops at Lake Havas Lake Havasu AZ 10/5/12 10-8 Tucson Mall Tucson AZ 10/17/12 10-8 Flagstaff Flagstaff AZ 10/5/12 10-8 Promenade At Casa Grande Casa Grande AZ 10/5/12 10-8 Yuma Palms Yuma AZ 10/4/12 10-8 Sierra Vista Towne Ctr. -

Columbus, GA 31904 RET AIL ADVISORS Offering Memorandum CONFIDENTIALITY & DISCLAIMER STATEMENT

IHOP ™ 2111 AIRPORT THRUWAY, COLUMBUS, GA 31904 RET AIL ADVISORS OFFERING MEMORANDUM CONFIDENTIALITY & DISCLAIMER STATEMENT This Offering Memorandum contains select information pertaining to the business and affairs of IHOP located at 2111 Airport Thruway, Columbus, GA 31904 (“Property”). It has been prepared by Matthews Retail Advisors . This Offering Memorandum may not be all-inclusive or contain all of the information a prospective purchaser may desire. The information contained in this Offering Memorandum is confidential and furnished solely for the purpose of a review by a prospective purchaser of the Property. It is not to be used for any other purpose or made available to any other person without the written consent of Seller or Matthews Retail Advisors . The material is based in part upon information supplied by the Seller and in part upon financial information obtained from sources it deems reliable. Owner, nor their officers, employees, or agents makes any representation or warranty, express or implied, as to the accuracy or completeness of this Offering Memorandum or any of its contents and no legal liability is assumed or shall be implied with respect thereto. Prospective purchasers should make their own projections and form their own conclusions without reliance upon the material contained herein and conduct their own due diligence. By acknowledging your receipt of this Offering Memorandum for the Property, you agree: 1. The Offering Memorandum and its contents are confidential; 2. You will hold it and treat it in the strictest of confidence; and 3. You will not, directly or indirectly, disclose or permit anyone else to disclose this Offering Memorandum or its contents in any fashion or manner detrimental to the interest of the Seller.