Link to an Accessible Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fact Sheet:Middle East and Africa ESG Screened Index Equity Sub

EMEA_INST Managed Pension Funds Limited Middle East and Africa ESG Screened Index Equity Sub-Fund Equities 30 June 2021 Fund Objective Performance ® The Sub-Fund aims to track the FTSE Developed Annualised Fund Benchmark Difference Middle East and Africa ex Controversies ex CW 1 Year (%) 23.30 23.28 0.01 Index, or its recognised replacement or equivalent. 3 Year (%) 4.75 4.84 -0.09 Investment Strategy 5 Year (%) 0.78 0.89 -0.11 The Sub-Fund primarily invests at all times in a Since Inception (%) 4.04 4.18 -0.14 sample of equities constituting the Index with such other securities as MPF shall deem it necessary Cumulative to capture the performance of the Index. Stock 3 Month (%) 11.54 11.51 0.04 index futures can be used for efficient portfolio 1 Year (%) 23.30 23.28 0.01 management. 3 Year (%) 14.95 15.24 -0.29 The following are excluded by the index provider from the index: Controversies (as defined by the ten 5 Year (%) 3.96 4.52 -0.56 principles of the UN Global Compact); Controversial Since Inception (%) 65.75 68.57 -2.81 weapons (including chemical & biological weapons, cluster munitions and anti-personnel landmines). Calendar 2021 (year to date) 9.74 9.71 0.03 Benchmark 2020 -1.28 -1.47 0.19 FTSE Developed Middle East and Africa ex 2019 10.82 11.07 -0.24 Controversies ex CW Index 2018 -0.47 -0.12 -0.35 Structure 2017 -10.77 -10.66 -0.12 Limited Company Past performance is not a guarantee of future results. -

HOUSTON REAL ESTATE MISSION to ISRAEL March 3-9, 2018

Program dated: May 24, 2017 HOUSTON REAL ESTATE MISSION TO ISRAEL March 3-9, 2018 D a y O n e : Saturday, March 3, 2018 DEPARTURE . Depart the U.S.A. Overnight: Flight D a y T w o : Sunday, March 4, 2018 TLV 24/7 . 12:00 p.m. Meet your tour educator in the hotel lobby. Enjoy lunch at Blue Sky, with it’s a wide selection of fish, vegetables, olive oil and artisan cheese, accompanied with local wines and overlooking the stunning views of the Mediterranean Sea. A Look into Our Journey: Tour orientation with the Mission Chair and the tour educator. The Booming Tel Aviv Real Estate Market: Take a tour of various locations around Tel Aviv with Ilan Pivko, a leading Israeli Architect and entrepreneur. Return to the hotel. Cocktails overlooking the Mediterranean Sea. Combining Business Abroad and Real Estate in Israel: Dinner at 2C with Danna Azrieli, the Acting Chairman of The Azrieli Group, at the Azrieli Towers. Overnight: Tel Aviv D a y T h r e e : Monday, March 5, 2018 FROM RED ROOFTOPS TO HIGH-RISERS . The Laws of Urban Development in Israel: Private breakfast at the hotel with Dr. Efrat Tolkowsky, CEO of the Gazit-Globe Real Estate Institute at IDC. Stroll down Rothschild Boulevard to view examples of the intriguing Bauhaus-style architecture from the 1930s; the local proliferation of the style won Tel Aviv recognition as a UNESCO World Heritage site and the nickname of ‘the White City'. Explore the commercial and residential developments with Dr. Micha Gross, the head of the Tel Aviv Bauhaus Center. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

W. TELFED August 1993 Vol

W. TELFED August 1993 Vol. 19 No. 3 46 SOKOLOV (2nd Floor) RAMAT-HASHARON Tel. 03*5400070 Home 052-446967 Fax 03-5400077 Dear Friends, Hectic times these. I'm sure we're all anxiously watching events in S. Africa in the hope that the transition will be as peaceful as possible. Of course events in the north over the past week also add to one's daily worries. A bit difficult to talk about holidays and having a good time under such circumstances, but 1 suppose life must carry on and maybe "dafka" because of the daily strain you owe it to yourself to take a break every now and then!!! After the few blasts in Turkey, there has been a definite drop off in interest. The best deals are still to be had to Antalya, Marmaris etc. where a week's package H/Board can be had for approx. $585.- II! The Greek Islands of Rhodes, Crete, Samos, Santorini and Corfu are all being serviced by direct charter flights this summer with packages from $650 - $990 depending on type of hotel etc. With El-Al starting direct flights to Paphos in Cyprus its also become very popular this year with very inexpensive 3 nite 4 nite or 7 nite packages at beautiful hotels. All the above should carry on until the middle of October. SAA announced this week that as of beginning of September they are starting to fly twice a week to Jhb — on Monday and Wednesday, both flights in a 767. With 3 weekly flights planning your forthcoming trip to S.A. -

Domestically Owned Versus Foreign-Owned Banks in Israel

Domestic bank intermediation: domestically owned versus foreign-owned banks in Israel David Marzuk1 1. The Israeli banking system – an overview A. The structure of the banking system and its scope of activity Israel has a highly developed banking system. At the end of June 2009, there were 23 banking corporations registered in Israel, including 14 commercial banks, two mortgage banks, two joint-service companies and five foreign banks. Despite the spate of financial deregulation in recent years, the Israeli banking sector still plays a key role in the country’s financial system and overall economy. It is also highly concentrated – the five main banking groups (Bank Hapoalim, Bank Leumi, First International Bank, Israel Discount Bank and Mizrahi-Tefahot Bank) together accounted for 94.3% of total assets as of June 2009. The two largest groups (Bank Leumi and Bank Hapoalim) accounted for almost 56.8% of total assets. The sector as a whole and the large banking groups in particular are organised around the concept of “universal” banking, in which commercial banks offer a full range of retail and corporate banking services. Those services include: mortgages, leasing and other forms of finance; brokerage in the local and foreign capital markets; underwriting and investment banking; and numerous specialised services. Furthermore, until the mid-1990s, the banking groups were deeply involved in non-financial activities. However, a law passed in 1996 forced the banks to divest their controlling stakes in non-financial companies and conglomerates (including insurance companies). This development was part of a privatisation process which was almost completed in 2005 (with the important exception of Bank Leumi). -

Delek Cover English 04.2006

ANNUAL REPORT 2005 Delek Group Ltd 7, Giborei Israel St., P.O.B 8464, Industrial Zone South, Netanya 42504, Israel Tel: 972 9 8638444, 972 9 8638555 Fax: 972 9 885495 www.delek-group.com Table of Contents: Chapter A Corporate Description Chapter B Director's Report on the Corporation Chapter C Financial Statements for December 31, 2004 Chapter D Additional Information on the Corporation Chapter E MATAV - CABLE SYSTEMS MEDIA LTD IMPORTANT This document is an unofficial translation from the Hebrew original of the 2005 annual report of Delek Group Ltd. that was submitted to the Tel-Aviv Stock Exchange and the Israeli Securities Authority on March 29, 2006. The Hebrew version submitted to the TASE and the Israeli Securities Authority shall be the sole binding version. Investors are urged to review the full Hebrew report. Part One – A Description of the General Development of the Company's Businesses 1. The Company's Activities and the Development of its Business ......................... 3 2. Sectors of Operation .................................................................................................. 6 3. Equity Investments in the Company and Transactions in its Shares................... 7 4. Dividend Distribution ................................................................................................. 8 5. Financial Information Regarding the Group's Sectors........................................... 9 6. The General Environment and Outside Influences................................................. 9 7. Oil Refining Sector -

Discount Bank

corporate responsibility 2018report 04 SOCIAL REPORT 2018 SOCIAL REPORT 2018 05 The Employees 94 Nurturing human capital policy 96 table of contents 05 Employee hiring 99 Discount Bank’s employees 98 Diversity and equal opportunity 104 The Discount values and their integration into the operation of the Bank 06 Maintaining employee rights 111 Discount Bank Summarized Sustainability Performance Table 08 Investing more in employees 120 About the report 10 Goals 136 Greetings from the Chairman and the President & CEO 12 01 Suppliers 138 Discount's eight Corporate Social Responsibility Report 14 Promotion of Responsible Procurement 140 Managing social responsibility at Discount 16 06 Goals 145 Dialogue with stakeholders 16 Discount for the community 146 The process of identifying the material topics 17 "Discount Sprint for the Future" 148 Reporting to the Global Compact 19 07 Discount volunteering in the community 152 Assurance examination 20 Investment in the community 154 Group profile and financial data 22 Goals 158 02 Discount Bank - General Overview 24 Green Discount 162 Mercantile Discount Bank General Overview 29 08 Policy 164 Israel Credit Cards Ltd. ("ICC") – General Overview 31 "Green Credit" 165 IDB Bank - General Overview 33 Promoting green building 166 Membership of organizations and external Initiatives 35 Responsible consumption of resources 168 Social Responsibility Ratings 36 Carbon footprint 172 Commendations and prizes 37 Goals 179 Discount Bank and the United Nations' sustainable development goals 38 Corporate Governance -

Glass-Steagall: the American Nightmare That Became the Israeli Dream

Fordham Journal of Corporate & Financial Law Volume 9, Number 2 2004 Article 7 Glass-Steagall: The American Nightmare that Became the Israeli Dream Ehud Ofer∗ ∗ Copyright c 2004 by the authors. Fordham Journal of Corporate & Financial Law is produced by The Berkeley Electronic Press (bepress). http://ir.lawnet.fordham.edu/jcfl GLASS-STEAGALL: THE AMERICAN NIGHTMARE THAT BECAME THE ISRAELI DREAM Ehud Ofer* INTRODUCTION This Note will examine the securities activities of banks in Israel. The relatively new legislation dealing with this aspect-Regulation of Investment Advice and Investment Portfolio Management Law (the "Law")-was enacted in 1995 as a lesson learned from the Share Regulation Affair of October 1983 (the "Share Regulation Affair" or the "Crisis of 1983"). In many ways in economic history, 1983 was for Israel what 1929 was for the United States. This Note will compare Israel's episode with the U.S. episode and will use the comparison to review the adequacy of the Israeli legislative response to the Crisis of 1983. The Law was enacted, primarily, based on American experience and legislation. This Note will compare the legislation enacted in both countries. To better understand the differences, this Note will introduce the unique financial market in Israel. Furthermore, this Note will present the recent legislative development in the United States (i.e., Gramm-Leach-Bliley Act) which repealed parts of the Depression-era Glass-Steagall Act. The Note will examine the necessity of Israeli "adjustments" to the Law due to this new development. * Ehud Ofer is a graduate of the LL.M. program in Banking, Corporate and Finance Law at Fordham University School of Law. -

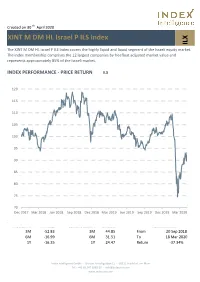

ILX XINT M DM HL Israel P ILS Index

Created on 30 th April 2020 XINT M DM HL Israel P ILS Index ILX The XINT M DM HL Israel P ILS Index covers the highly liquid and liquid segment of the Israeli equity market. The index membership comprises the 12 largest companies by freefloat adjusted market value and represents approximately 85% of the Israeli market. INDEX PERFORMANCE - PRICE RETURN ILX 120 115 110 105 100 95 90 85 80 75 70 Dec 2017 Mar 2018 Jun 2018 Sep 2018 Dec 2018 Mar 2019 Jun 2019 Sep 2019 Dec 2019 Mar 2020 Index Return % annualised Standard Deviation % annualised Maximum Drawdown 3M -52.83 3M 44.85 From 20 Sep 2018 6M -16.99 6M 31.51 To 18 Mar 2020 1Y -16.35 1Y 24.47 Return -37.34% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com TOP 10 Largest Constituents FFMV million Weight Industry Sector Check Point Software Technologies Ltd 17.07% 4,471,198 17.07% Technology Teva Pharmaceutical Industries Ltd 15.55% 4,072,206 15.55% Health Care Nice Ltd 13.77% 3,605,623 13.77% Technology Bank Leumi Le Israel BM 10.57% 2,769,635 10.57% Banks Bank Hapoalim BM 9.74% 2,551,239 9.74% Banks Wix.com Ltd 8.43% 2,206,957 8.43% Technology Israel Discount Bank Ltd 5.05% 1,323,487 5.05% Banks CyberArk Software Ltd 4.94% 1,294,068 4.94% Technology Elbit Systems Ltd 4.40% 1,152,520 4.40% Industrial Goods & Services Mizrahi Tefahot Bank Ltd 3.86% 1,010,693 3.86% Banks Total 24,457,627 93.37% This information has been prepared by Index Intelligence GmbH (“IIG”). -

Immediate Report 4/08/08

MIZRAHI TEFAHOT BANK LTD No. with the Registrar of Companies: 520000522 To Israel Securities To Tel Aviv Stock Exchange Ltd T121 Date of transmission: Authority (Public) December 17, 2017 www.isa.gov.il www.tase.co.il Ref: 2017-01-117204 Immediate Report Explanation: This form may not be used if an appropriate form exists for the reported event. Issue results must be reported under T20 and not under this form. Bond rating or corporation rating reports must be submitted through Form T125. Nature of the Event: Application for the Approval of a Class Action Lawsuit The reference numbers of previous documents on the subject: Mizrahi Tefahot Bank Ltd (the “Bank) respectfully reports as follows: On December 17, 2017, an application to approve a class action lawsuit was produced for the Bank, which was submitted to the Jerusalem District Court against the Bank, Otsar Hahayal Bank, Bank Leumi le-Israel and Mercantile Discount Bank (“the Respondent Banks”). The applicants claim that the Respondent Banks, which provide credit under the Small Businesses Fund, require borrowers to make a deposit out of the loan monies, which constitutes the prohibited making of a service conditional upon the purchase of another service, while allegedly raising the loan’s effective interest rate. It is further claimed that this conduct is tantamount to a restrictive arrangement. The applicant noted in her application that the action amount attributed to the Bank is over ILS 147 million. Attached file The company is not a shell company, as defined in the TASE Rules and Regulations. Date on which the corporation first learned of the event: December 17, 2017 at 14:45. -

Class Actions Against Banks Under the New Israeli Law on Class Actions

CLASS ACTIONS AGAINST BANKS UNDER THE NEW ISRAELI LAW ON CLASS ACTIONS * DR. RUTH PLATO SHINAR I. Introduction....................................................................256 II. Causes of Action for Class Actions Against Banks ....... 259 III. The Representative Filing The Action ........................... 264 IV. The Conditions for Certification of a Class Action....... 265 V. Conclusion .................................................................... 281 * Dr. Ruth Plato Shinar is the Senior Lecturer and Director of the Center for Banking Law, Netanya Academic College, Israel. The author wishes to thank the Van Calker Foundation and the Swiss Institute of Comparative law for their generous support of the research for this article, which was principally conducted at the Swiss Institute of Comparative Law in Lausanne, Switzerland during the summer of 2006. 2007 CLASS ACTIONS AGAINST BANKS IN ISRAEL 256 I. INTRODUCTION In March 2006, Israel enacted a modern and far-reaching Class Action Law1 (the “Class Action Law”) to regulate class action suits in a centralized and exhaustive manner. Prior to the law’s enactment, class actions in Israel were common in various fields,2 including banking. The basis for class actions against banks was the Banking (Service to Customer) Law (“the Banking Law”), which contained a chapter on class actions. However, the new Class Action Law abolished this chapter, as well as all other laws concerning Class Actions in different fields, and today the arrangement of class actions is concentrated in -

Figure 1.3 A

Bank Leumi Group Figure 1.3 A. Banking and finance in Israel Bank Leumi Le-Israel Ltd. (1) The structure of Israel's banking system and a Arab Israel Bank Ltd. (1) C. Capital market and financial companies investments in main investee companies , Leumi Mortgage Bank Ltd. (merged with Leumi Card Ltd.(5) Bank Hapoalim Group Bank Leumi Le-Israel Ltd. as of December Leumi Securities and Investments Ltd. (9) December 2012 Leumi Capital Market Services Ltd. (9) 31, 2012) (2) A. Banking and finance in Israel (1) Leumi Leasing and Investments Ltd. (3) The Bank Leumi Le-Israel Trust Co Ltd. (9) Bank Hapoalim Ltd. Leumi Finance Company Ltd. (4) Leumi Partners Ltd. (7)(9) Total assets: NIS 1,301 billion B. Banking and finance abroad (6) Leumi Industrial Development Bank Ltd. (7) D. Non-banking corporations Herfindahl index: H = 0.217 Bank Hapoalim (Switzerland) Ltd. Leumi Real Holdings Ltd. (7) The Israel Corporation Ltd. Bank Hapoalim (Luxembourg) Ltd. Leumi Financial Holdings Ltd. (7) CR 2 = 58% Bank Hapoalim (Cayman Islands) Ltd. B. Banking and finance abroad (6) Bank Hapoalim (Latin America) S.A. Bank Leumi (USA) Bank Pozitif Kredi Ve Kalkinma Bankasi A.S. (with Bank Leumi (UK) plc a holding in JSC Bank Pozitif) Leumi Private Bank S.A. C. Capital market and financial companies (9) Bank Leumi Luxembourg Isracard (5) Bank Leumi Romania Poalim Express Ltd. (5) Leumi International Investments NV Bank Leumi Group, Bank Hapoalim Group, Poalim Capital Markets Ltd. (8) Leumi Re Limited (9) 29% 29% Poalim Sahar Ltd. (9) The Bank Hapoalim Trust Co Ltd.