Bluestar Israel Equity Update First Quarter 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PAZ OIL COMPANY LTD. 2015 Annual Report

PMdesigners LTD. OIL COMPANY PAZ 2015 Annual Report .... PAZ OIL COMPANY PAZ OIL COMPANY LTD. Euro Park, Holland Building 2015 Annual Report Yakum 6097200, Israel www.paz.co.il WorldReginfo - b1d0d604-1d01-4a24-939b-ab2b538ff8c0 PAZ OIL COMPANY LTD. 2015 Annual Report WorldReginfo - b1d0d604-1d01-4a24-939b-ab2b538ff8c0 Disclaimer This document is a convenience translation from the Hebrew original of the separate financial data dated December 31, 2015 (the "Statements") issued by Paz Oil Company Ltd. (the "Company"). Only the Hebrew original of the Statements is legally binding. No reliance may by placed for any purpose whatsoever on the completeness, accuracy or fairness of information contained in this document. No warranty or representation, express or implied, is made or given by or on behalf of the Company or any of its directors, officers or employees or any other person as to the accuracy, completeness or fairness of the information contained in this document and no responsibility or liability is accepted by any person for such information. WorldReginfo - b1d0d604-1d01-4a24-939b-ab2b538ff8c0 PAZ OIL COMPANY LTD. Table of Contents A. Description of the Company’s Business B. Report of the Board of Directors on the State of Affairs of the Corporation C. Consolidated Financial Statements D. Additional Details about the Company E. Separate Financial Data as of December 31, 2015 WorldReginfo - b1d0d604-1d01-4a24-939b-ab2b538ff8c0 A. Description of the Company’s Business WorldReginfo - b1d0d604-1d01-4a24-939b-ab2b538ff8c0 Chapter A - Description of the Company's Business Description of the Company's Business – Contents Part 1: Description of the General Development of the Company's Business ............................................................ -

HOUSTON REAL ESTATE MISSION to ISRAEL March 3-9, 2018

Program dated: May 24, 2017 HOUSTON REAL ESTATE MISSION TO ISRAEL March 3-9, 2018 D a y O n e : Saturday, March 3, 2018 DEPARTURE . Depart the U.S.A. Overnight: Flight D a y T w o : Sunday, March 4, 2018 TLV 24/7 . 12:00 p.m. Meet your tour educator in the hotel lobby. Enjoy lunch at Blue Sky, with it’s a wide selection of fish, vegetables, olive oil and artisan cheese, accompanied with local wines and overlooking the stunning views of the Mediterranean Sea. A Look into Our Journey: Tour orientation with the Mission Chair and the tour educator. The Booming Tel Aviv Real Estate Market: Take a tour of various locations around Tel Aviv with Ilan Pivko, a leading Israeli Architect and entrepreneur. Return to the hotel. Cocktails overlooking the Mediterranean Sea. Combining Business Abroad and Real Estate in Israel: Dinner at 2C with Danna Azrieli, the Acting Chairman of The Azrieli Group, at the Azrieli Towers. Overnight: Tel Aviv D a y T h r e e : Monday, March 5, 2018 FROM RED ROOFTOPS TO HIGH-RISERS . The Laws of Urban Development in Israel: Private breakfast at the hotel with Dr. Efrat Tolkowsky, CEO of the Gazit-Globe Real Estate Institute at IDC. Stroll down Rothschild Boulevard to view examples of the intriguing Bauhaus-style architecture from the 1930s; the local proliferation of the style won Tel Aviv recognition as a UNESCO World Heritage site and the nickname of ‘the White City'. Explore the commercial and residential developments with Dr. Micha Gross, the head of the Tel Aviv Bauhaus Center. -

Bigitech Fact Sheet 2017.12

BlueStar Israel Global Technology IndexTM TM Q417 BIGITech Fact Sheet INDEX OVERVIEW The BlueStar Israel Global Technology IndexTM provides a benchmark for investors to track Israeli and Israel-linked technology companies trading worldwide. The index is constructed using BlueStar Indexes’ unique methodology and proprietary database of Israeli and Israel- linked companies. BIGITechTM is a modified market capitalization weighted index, capping the top-weighted constituents at 10%. It includes the largest and most liquid technology companies, as well as mid and small cap companies that display sufficient liquidity for global investors. The methodology allows for the inclusion of Israeli companies listed on the Tel Aviv Stock Exchange and other major exchanges such as the London Stock Exchange, New York Stock Exchange, and NASDAQ. Furthermore the methodology provides for the inclusion of companies that develop, manufacture, and/or deliver innovative technologies in a wide range of tech sectors, including Bio- Tech, Agriculture-Tech, Defense-Tech, Clean-Tech as well as Info-tech. Top Ten Index Constituents GICS Industry Exposure Company Index Weight (%) Industry Weight (%) Nice Ltd 7.63 Software 27.78 Amdocs Ltd 7.44 Semiconductors & Semiconductor 14.49 Check Point Software Tech 7.11 IT Services 10.15 Tower Semiconductor Ltd 4.66 Biotechnology 7.52 Elbit Systems Ltd 4.41 Internet Software & Services 5.47 Mellanox Technologies Ltd 4.26 Aerospace & Defense 5.45 Verint Systems Inc 3.89 Communications Equipment 5.24 Ormat Technologies Inc 3.52 Health Care Equipment & Suppli 4.86 Wix.Com Ltd 3.37 Independent Power and Renewabl 4.36 Orbotech Ltd 3.26 Electronic Equipment, Instrume 3.96 Total 49.52 Technology Hardware, Storage & 1.70 Diversified Financial Services 1.68 Pharmaceuticals 1.49 Hotels, Restaurants & Leisure 1.43 Machinery 1.38 BIGITech™ Internal Index Data Commercial Services & Supplies 0.69 Other 12.35 Index Statistics No. -

Frutarom Industries Ltd. Directors' Report of the Company's State of Affairs for the Period Ended June 30, 2018 A. Review Of

FRUTAROM INDUSTRIES LTD. DIRECTORS' REPORT OF THE COMPANY'S STATE OF AFFAIRS FOR THE PERIOD ENDED JUNE 30, 2018 BOARD OF DIRECTORS' DISCUSSIONS ON THE COMPANY'S STATE OF BUSINESS A. REVIEW OF ACTIVITY Frutarom Industries Ltd. (the "Company”) is a global company established in Israel in 1933. Frutarom became a public company in 1996 upon registration of its shares for trade on the Tel Aviv Stock Exchange. In February 2005, the Company’s Global Depository Receipts were also listed on the London Stock Exchange Official List. The Company, itself and through its subsidiaries ("Frutarom" or the "Group") develops, produces and markets flavors and fine ingredients used in the manufacturing of food, beverages, flavors and fragrances, pharma/nutraceuticals, cosmetics and personal care products. As of the date of the publication of the report Frutarom operated 73 production sites, 92 research and development laboratories, and 110 sales offices in Europe, North America, Latin America, Israel, Asia, Africa and New Zealand, and it marketed and sold over 70,000 products to more than 30,000 customers in more than 150 countries and employs approx. 5,600 people throughout the world. On May 7, 2018, Frutarom signed a merger agreement (the "Merger Agreement") with International Flavors & Fragrances Inc. (the "Purchasing Company") an international public company, whose securities are listed for trading on the New York Stok Exchange (under the symbol IFF) and on the Euronext Paris Stock Exchange (under the symbol IFF) and Icon Newco Ltd, a private company -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

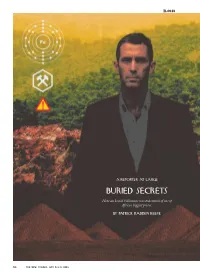

4C Buried Secrets

R-0048 a reporter at laRgE bURiEd sEcrets How an Israeli billionaire wrested control of one of Africa’s biggest prizes. bY paTRick radden keefE 50 THE NEW YORKER, JULY 8 & 15, 2013 TNY—2013_07_08&15—PAGE 50—133SC.—Live art r23707—CritiCAL PHOTOGRAPH TO BE WATCHED THROUGHOUT THE ENTIRE PRESS run—pLEASE PULL KODAK APPROVAL PROOF F0R PRESS COLOR GUID- ANCE 4C ne of the world’s largest known de- As wealthy countries confront the posits of untapped iron ore is buried prospect of rapidly depleting natural re- insideO a great, forested mountain range in sources, they are turning, increasingly, the tiny West African republic of Guinea. to Africa, where oil and minerals worth In the country’s southeast highlands, far trillions of dollars remain trapped in the from any city or major roads, the Siman- ground. By one estimate, the continent dou Mountains stretch for seventy miles, holds thirty per cent of the world’s min- looming over the jungle floor like a giant eral reserves. Paul Collier, who runs the dinosaur spine. Some of the peaks have Center for the Study of African Econo- nicknames that were bestowed by geolo- mies, at Oxford, has suggested that “a gists and miners who have worked in the new scramble for Africa” is under way. area; one is Iron Maiden, another Metal- Bilateral trade between China and Af- lica. Iron ore is the raw material that, once rica, which in 2000 stood at ten billion smelted, becomes steel, and the ore at Si- dollars, is projected to top two hundred mandou is unusually rich, meaning that billion dollars this year. -

Public Companies Profiting from Illegal Israeli Settlements on Palestinian Land

Public Companies Profiting from Illegal Israeli Settlements on Palestinian Land Yellow highlighting denotes companies held by the United Methodist General Board of Pension and Health Benefits (GBPHB) as of 12/31/14 I. Public Companies Located in Illegal Settlements ACE AUTO DEPOT LTD. (TLV:ACDP) - owns hardware store in the illegal settlement of Ma'ale Adumim http://www.ace.co.il/default.asp?catid=%7BE79CAE46-40FB-4818-A7BF-FF1C01A96109%7D, http://www.machat.co.il/businesses.php, http://www.nytimes.com/2007/03/14/world/middleeast/14israel.html?_r=3&oref=slogin&oref=slogin&, http://investing.businessweek.com/research/stocks/snapshot/snapshot.asp?ticker=ACDP:IT ALON BLUE SQUARE ISRAEL LTD. (NYSE:BSI) - has facilities in the Barkan and Atarot Industrial Zones and operates supermarkets in many West Bank settlements www.whoprofits.org/company/blue- square-israel, http://www.haaretz.com/business/shefa-shuk-no-more-boycotted-chain-renamed-zol-b-shefa-1.378092, www.bsi.co.il/Common/FilesBinaryWrite.aspx?id=3140 AVGOL INDUSTRIES 1953 LTD. (TLV:AVGL) - has a major manufacturing plant in the Barkan Industrial Zone http://www.unitedmethodistdivestment.com/ReportCorporateResearchTripWestBank2010FinalVersion3.pdf (United Methodist eyewitness report), http://panjiva.com/Avgol-Ltd/1370180, http://www.haaretz.com/print-edition/business/avgol- sees-bright-future-for-nonwoven-textiles-in-china-1.282397 AVIS BUDGET GROUP INC. (NASDAQ:CAR) - leases cars in the illegal settlements of Beitar Illit and Modi’in Illit http://rent.avis.co.il/en/pages/car_rental_israel_stations, http://www.carrentalisrael.com/car-rental- israel.asp?refr= BANK HAPOALIM LTD. (TLV:POLI) - has branches in settlements; provides financing for housing projects in illegal settlements, mortgages for settlers, and financing for the Jerusalem light rail project, which connects illegal settlements with Jerusalem http://www.haaretz.com/print-edition/business/bank-hapoalim-to-lead-financing-for-jerusalem-light-rail-line-1.97706, http://www.whoprofits.org/company/bank-hapoalim BANK LEUMI LE-ISRAEL LTD. -

Ormat Technologies Inc

ORMAT TECHNOLOGIES INC MEETING DATE Wed, 06 Nov 2019 13:00 TYPE EGM ISSUE DATE Fri, 25 Oct 2019 MEETING LOCATION 6140 Plumas Street, Reno, NV 89519 CURRENT INDICES PIRC Global SECTOR Electric services COMPANY OVERVIEW Ormat Technologies is a provider of renewable power and energy technology. The Company is based in Reno, Nevada, and has over 150 power plants. MEETING SPECIFIC INFORMATION Ordinary resolutions are approved by simple majority of the votes cast. PROPOSALS ADVICE 1 Board Proposal to Declassify the Board For It is considered that staggered elections do not pursue shareholders’ best interest, as they entrench the board against hostile takeovers. In this sense, the Board’s proposal is welcomed as it will introduce annual election for all directors of the board, which is considered to be best practice. 2 Adjourn Meeting Oppose The Board requests authority to adjourn the special meeting until a later date or dates, if necessary, in order to permit further solicitation of proxies if there are not sufficient votes at the time of the special meeting to approve the merger. An oppose vote is recommended to any adjournment or postponement of meetings if a sufficient number of votes are present to constitute a quorum. It is considered that where a quorum is present, the vote outcome should be considered representative of shareholder opinion. ORMAT TECHNOLOGIES INC 06 Nov 2019 EGM 1 of 5 BOARD AND COMMITTEE COMPOSITION (post-Meeting) INDEPENDENT BY DIRECTOR GENDER PIRC COMPANY BOARD AC RC NC SC TENURE Dan Falk M No Yes NED C M M - 14 Todd C. -

2013 Annual Report on Form 10-K

Annual Report 13 Create Meaningful Connections About LivePerson LivePerson, Inc. (NASDAQ: LPSN, TASE: LPSN) offers a cloud-based platform that enables businesses to proactively connect in real-time with their customers via chat, voice, and content delivery at the right time, through the right channel, including websites, social media, and mobile devices. This "intelligent engagement" is driven by real-time behavioral analytics, producing connections based on a true understanding of business objectives and customer needs. More than 8,500 companies rely on LivePerson's platform to increase conversions and improve customer experience, including Cisco, Hewlett-Packard, IBM, Microsoft, Verizon, Sky, Walt Disney, PNC and Orbitz. LivePerson is headquartered in New York City with offices in Atlanta, Amsterdam, London, Melbourne, San Francisco, Santa Monica, Tokyo and Tel Aviv. Annual Revenue (in millions) Quarterly Revenue (in millions) 2011 2012 2013 $180 $50 46.9 178 45.2 $160 $45 43.2 42.5 42.5 157 $40 39.7 $140 38.5 36.8 36.5 $35 34.3 133 31.9 $120 30.4 $30 $100 110 $25 $80 87 $20 $60 $15 $40 $10 $20 2009 2010 2011 2012 2013 Q1 Q2 Q3 Q4 Safe Harbor Statement Statements in this report regarding LivePerson that are not historical facts are forward-looking statements and are subject to risks and uncertainties that could cause actual future events or results to differ materially from such statements. Any such forward-looking statements, including but not limited to financial guidance, are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. -

NASDAQ Stock Market

Nasdaq Stock Market Friday, December 28, 2018 Name Symbol Close 1st Constitution Bancorp FCCY 19.75 1st Source SRCE 40.25 2U TWOU 48.31 21st Century Fox Cl A FOXA 47.97 21st Century Fox Cl B FOX 47.62 21Vianet Group ADR VNET 8.63 51job ADR JOBS 61.7 111 ADR YI 6.05 360 Finance ADR QFIN 15.74 1347 Property Insurance Holdings PIH 4.05 1-800-FLOWERS.COM Cl A FLWS 11.92 AAON AAON 34.85 Abiomed ABMD 318.17 Acacia Communications ACIA 37.69 Acacia Research - Acacia ACTG 3 Technologies Acadia Healthcare ACHC 25.56 ACADIA Pharmaceuticals ACAD 15.65 Acceleron Pharma XLRN 44.13 Access National ANCX 21.31 Accuray ARAY 3.45 AcelRx Pharmaceuticals ACRX 2.34 Aceto ACET 0.82 Achaogen AKAO 1.31 Achillion Pharmaceuticals ACHN 1.48 AC Immune ACIU 9.78 ACI Worldwide ACIW 27.25 Aclaris Therapeutics ACRS 7.31 ACM Research Cl A ACMR 10.47 Acorda Therapeutics ACOR 14.98 Activision Blizzard ATVI 46.8 Adamas Pharmaceuticals ADMS 8.45 Adaptimmune Therapeutics ADR ADAP 5.15 Addus HomeCare ADUS 67.27 ADDvantage Technologies Group AEY 1.43 Adobe ADBE 223.13 Adtran ADTN 10.82 Aduro Biotech ADRO 2.65 Advanced Emissions Solutions ADES 10.07 Advanced Energy Industries AEIS 42.71 Advanced Micro Devices AMD 17.82 Advaxis ADXS 0.19 Adverum Biotechnologies ADVM 3.2 Aegion AEGN 16.24 Aeglea BioTherapeutics AGLE 7.67 Aemetis AMTX 0.57 Aerie Pharmaceuticals AERI 35.52 AeroVironment AVAV 67.57 Aevi Genomic Medicine GNMX 0.67 Affimed AFMD 3.11 Agile Therapeutics AGRX 0.61 Agilysys AGYS 14.59 Agios Pharmaceuticals AGIO 45.3 AGNC Investment AGNC 17.73 AgroFresh Solutions AGFS 3.85 -

Israel and the Alien Tort Statute

Summer 2014 No.54 JTheUSTICE magazine of the International Association of Jewish Lawyers and Jurists In this issue The International Court of Justice Adjudicating the Arab-Israel Disputes? Boycotts, Divestment, Sanctions and the Law Israel and the Alien Tort Statute Corporations and Human Rights Zivotofsky v. Kerry - A Historical Constitutional Battle Preachers of Hate and Freedom of Expression UNRWA Panel at UN IAJLJ Activities The International Association of Jewish Lawyers and Jurists Honorary President: Hadassa Ben-Itto, Judge (Ret.) (Israel) Life time Member: Irwin Cotler, Prof. (Canada) Honorary Vice Presidents: Joseph Roubache (France) Oreste Bisazza Terracini, Dr. (Italy) Executive Committee: Board of Governors: President: Irit Kohn (Israel) Irit Kohn (Israel) Haim Klugman (Israel) Avraham (Avi) D. Doron (Israel) Deputy President: Meir Rosenne, Dr. (Israel) Haim Klugman (Israel) Mirella M. Bamberger (Israel) Alyza D. Lewin (USA) Vice President and Treasurer: Marcos Arnoldo Grabivker, Judge (Argentina) Avraham (Avi) D. Doron (Israel) Maurizio Ruben (Italy) Alex Hertman (Israel) Vice President and Coordinator with Amos Shapira, Prof. (Israel) International Organizations: Avishai Sapir (Israel) Meir Rosenne, Dr. (Israel) David Pardes (Belgium) Dov Shefi, Brig. (Ret.) (Israel) Vice President and Secretary General: Edna Bekenstein, Judge (Ret.) (Israel) Mirella M. Bamberger (Israel) Edna Kaplan-Hagler, Judge (Ret.) Dr. (Israel) Efraim (Efi) Chalamish, Dr. (USA) Vice Presidents: Ethia Simha (Israel) Alyza D. Lewin (USA) Jeremy D. Margolis (USA) Marcos Arnoldo Grabivker, Judge (Argentina) Jimena Bronfman (Chile) Maurizio Ruben (Italy) Jonathan Lux (UK) Lipa Meir, Dr. (Israel) Academic Adviser: Mala Tabory, Dr. (Israel) Yaffa Zilbershats, Prof. (Israel) Maria Canals De-Cediel, Dr. (Switzerland) Meir Linzen (Israel) Representatives to the U.N. -

Annual Report 2010 Annual Report 2010

Delek Group Ltd 7, Giborei Israel St., P.O.B 8464, Industrial Zone South, Netanya 42504, Israel Tel: 972 9 8638444, 972 9 8638555 Fax: 972 9 8854955 www.delek-group.com ANNUAL REPORT 2010 ANNUAL ANNUAL REPORT 2010 DelekDelek Group Group Ltd Ltd 7,7, Giborei Giborei Israel Israel St., St., P.O.B P.O.B 8464, 8464, Industrial Industrial Zone Zone South, South, Netanya Netanya 42504, 42504, Israel Israel Tel:Tel: 972 972 9 98638444, 8638444, 972 972 9 98638555 8638555 Fax: Fax: 972 972 9 98854955 8854955 www.delek-group.comwww.delek-group.com WorldReginfo - dd8f0e77-e950-4954-a47f-a98641dde1c8 IMPORTANT This document is an unofficial translation for convenience only of the Hebrew original of December 31, 2010 financial report of Delek Group Ltd. that was submitted to the Tel-Aviv Stock Exchange and the Israeli Securities Authority on March 31, 2010. The Hebrew version submitted to the TASE and the Israeli Securities Authority shall be the sole binding legal version. WorldReginfo - dd8f0e77-e950-4954-a47f-a98641dde1c8 Table of Contents Chapter A | Corporate Description Chapter B | Board of Directors Report on the State of the Company’s Affairs Chapter C | Financial Statements for December 31, 2010 Chapter D | Additional Information on the Corporation Chapter E | Annual report for 2010 on the Effectiveness of Internal Controls for Financial Reporting and Disclosure WorldReginfo - dd8f0e77-e950-4954-a47f-a98641dde1c8 Chapter A Corporate Description WorldReginfo - dd8f0e77-e950-4954-a47f-a98641dde1c8 Chapter A – Description of the Corporation's Business Table of Contents Chapter A – Description of the Corporation's Business ......................................................... 1 Part One – Description of the Corporation's Business ..........................................................