Final-Admission-Document.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Development Securities PLC Annual Report 2006

Development Securities PLC Annual Report 2006 1 Financial highlights Development Securities PLC Annual Report 2006 Financial highlights £23.6m 6.75p 63.4p Profit after tax Annual dividends per share Earnings per share £231.4m £14.4m 568p Net assets Net borrowings Net assets per share Net assets per share Earnings per share Dividends per share 06 568* 06 63.4* 06 6.75* 05 510* 05 54.8* 05 6.37* 04 472* 04 54.3* 04 6.0* 03 444 03 4.2 03 5.4 02 423 02 26.9 02 5.0 01 423 01 24.0 01 4.5 Contents 02 Chairman’s statement 04 Our strategy 12 Review of operations 18 Property investment portfolio 22 Sustainability report 24 Board of Directors 26 Report of the Directors 28 Corporate governance 32 Contents of the financial statements 68 Remuneration report 76 Financial calendar and advisors *stated in accordance with IFRS 2 Chairman’s statement Development Securities PLC Annual Report 2006 Chairman’s statement I am pleased to report another very for other potential property acquisitions. The growing size and strength of our satisfactory year for your Company, We were pleased with the strength of support balance sheet, recently augmented by the resulting in a significant uplift in demonstrated by both existing and new £23.1 million share placing, supports our shareholder funds. shareholders for this successful placing. adjusted business model, whereby we now consider it appropriate to secure direct An increased contribution from our development Strategy ownership of land for development. Our recent activities, coupled with a strong performance Shareholders will be aware that the strategic £33.5 million acquisition of Curzon Park, in from our property investment portfolio enables focus of our development activities over the equal partnership with Grainger PLC, is a me to report a profit after tax of £23.6 million last two years has been suburban London case in point. -

Tuesday July 30, 1996

7±30±96 Tuesday Vol. 61 No. 147 July 30, 1996 Pages 39555±39838 federal register 1 II Federal Register / Vol. 61, No. 147 / Tuesday, July 30, 1996 SUBSCRIPTIONS AND COPIES PUBLIC Subscriptions: Paper or fiche 202±512±1800 FEDERAL REGISTER Published daily, Monday through Friday, Assistance with public subscriptions 512±1806 (not published on Saturdays, Sundays, or on official holidays), by General online information 202±512±1530 the Office of the Federal Register, National Archives and Records Administration, Washington, DC 20408, under the Federal Register Single copies/back copies: Act (49 Stat. 500, as amended; 44 U.S.C. Ch. 15) and the Paper or fiche 512±1800 regulations of the Administrative Committee of the Federal Register Assistance with public single copies 512±1803 (1 CFR Ch. I). Distribution is made only by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC FEDERAL AGENCIES 20402. Subscriptions: The Federal Register provides a uniform system for making Paper or fiche 523±5243 available to the public regulations and legal notices issued by Assistance with Federal agency subscriptions 523±5243 Federal agencies. These include Presidential proclamations and For other telephone numbers, see the Reader Aids section Executive Orders and Federal agency documents having general applicability and legal effect, documents required to be published at the end of this issue. by act of Congress and other Federal agency documents of public interest. Documents are on file for public inspection in the Office of the Federal Register the day before they are published, unless earlier filing is requested by the issuing agency. -

D08-38 Appendices a to E

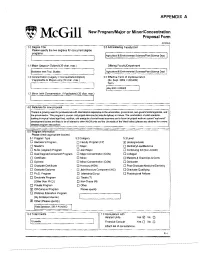

APPENDIX A NewProgram/Major or Minor/Concentration , McGill Proposal Form (0712004) 1,0 DegreeTitle 2,0 Administering Faculty/Unit Please specifythe two degrees for concurrentdegree programs Agricultural &Environmental SdencesIPlant Science Dept. 1.1 Major (Legacy:: Subject)(30-char. max.) . Offering Faculty/Department IBarbadOS Inter.Trop. Studies Aglicultural & Environmental SciencesIPlant Science Dept. 1.2 Concentration(Legacy =ConcentrationJOption) 30 EffectiveTerm of Implementation If applicableto Majors only (30 char, max) (Ex. Sept 2004 == 200409) Term IMay 2009 1200905 1,3 Minor (withConcentration, if Applicable)(30 char. max.) I ~ I 4.0 Rationalefor new proposal I There tsa growing need forprofessionals with international experience intheunlversilles, government, non-govemmental agencies. and theprivate sector. This program is course- and project-intensive butinterdisciplinary in nature. Thecombination ofsolk! academic training intropical Island a91i-fooo. nutrition, and energy Ina tourist-based economy anda focus onproject work oncurrent 'realwortd' development issues arelikely tobe ofinterest toother McGill units and the University of thewest Indies (please see attached fora more detailed program description). - 5.0 ProgramInformation Please check appropriate boxtes) 5.1 Program Type 5.2 Category 5.3 Level o Bachelor'sProgram o FacultyProgram(FP) . ~ Undergraduate o Master's o Major o DentistryfLawlMedicine o M.Sc. (Applied) Program o Joint Major o Continuing Ed (Non-Credit) o Dual Degree/ConcurrentProgram o MajorConcentration -

Register of Lords' Interests

REGISTER OF LORDS’ INTERESTS _________________ The following Members of the House of Lords have registered relevant interests under the code of conduct: ABERDARE, LORD Category 10: Non-financial interests (a) Director, F.C.M. Limited (recording rights) Category 10: Non-financial interests (c) Trustee, National Library of Wales (interest ceased 31 March 2021) Category 10: Non-financial interests (e) Trustee, Stephen Dodgson Trust (promotes continued awareness/performance of works of composer Stephen Dodgson) Chairman and Trustee, Berlioz Sesquicentenary Committee (music) Director, UK Focused Ultrasound Foundation (charitable company limited by guarantee) Chairman and Trustee, Berlioz Society Trustee, West Wycombe Charitable Trust ADAMS OF CRAIGIELEA, BARONESS Nil No registrable interests ADDINGTON, LORD Category 1: Directorships Chairman, Microlink PC (UK) Ltd (computing and software) Category 10: Non-financial interests (a) Director and Trustee, The Atlas Foundation (registered charity; seeks to improve lives of disadvantaged people across the world) Category 10: Non-financial interests (d) President (formerly Vice President), British Dyslexia Association Category 10: Non-financial interests (e) Vice President, UK Sports Association Vice President, Lakenham Hewitt Rugby Club (interest ceased 30 November 2020) ADEBOWALE, LORD Category 1: Directorships Director, Leadership in Mind Ltd (business activities; certain income from services provided personally by the member is or will be paid to this company; see category 4(a)) Director, Visionable -

Kirk King Appointed New GM of Berger Paints

Established October 1895 See inside Monday February 17, 2020 $1 VAT Inclusive High cost concern MINISTER of Maritime Affairs and the Blue Economy,Kirk Humphrey says he is concerned about the high cost of some of the eco-friendly food-grade products available on the local market. He made the comments after touring COT Holdings at Newton Industrial Estate, Christ Church, stating that it is imperative that a way is found to reduce the cost of the inputs so that the products can be sold more competitively. “Some of the costs that you see on some of these items are not in sync with what they have had to pay, so that what you see reflected as the final price has no bearing to the ban that we have put on single use plastics. I have said before and I am saying it now, we have persons in Barbados, the corporate companies [who] have a responsibility to engage in practices that are in sync with Barbadian values,” he said. He continued, “There is an ethical kind of behaviour that should bind all of us.” Haynesville Youth Group Dancers and Dancin’ Africa performing at the Holetown Monument. Minister Humphrey said in the process of some of his ministry’s investigations, when the cost of the containers and the selling price were compared,“it was insane”, hinting that the latter was extremely high. With that in mind, he said they have BIGGER, BETTER also heard that there are some persons who are Holetown Festival attempting to sell the banned single use plastics quietly, despite the fact off to grand start that it is illegal to do so. -

The Analysis of Ceramic Symbolism from the First Street Site in Barbados

Western Michigan University ScholarWorks at WMU Master's Theses Graduate College 12-2006 The Analysis of Ceramic Symbolism from the First Street Site in Barbados Aya Hashimoto Follow this and additional works at: https://scholarworks.wmich.edu/masters_theses Part of the Social and Cultural Anthropology Commons Recommended Citation Hashimoto, Aya, "The Analysis of Ceramic Symbolism from the First Street Site in Barbados" (2006). Master's Theses. 3863. https://scholarworks.wmich.edu/masters_theses/3863 This Masters Thesis-Open Access is brought to you for free and open access by the Graduate College at ScholarWorks at WMU. It has been accepted for inclusion in Master's Theses by an authorized administrator of ScholarWorks at WMU. For more information, please contact [email protected]. THE ANALYSIS OF CERAMIC SYMBOLISM FROM THE FIRST STREET SITE IN BARBADOS by Aya Hashimoto A Thesis Submitted to the Faculty of The Graduate College in partial fulfillmentof the requirements for the Degree of Master of Arts Department of Anthropology Western Michigan University Kalamazoo, Michigan December 2006 @2006 Aya Hashimoto ACKNOWLEDGMENTS I would like to thank Dr. Michael S. Nassaney for taking the time to discuss with me his perception of the topics contained herein. His guidance. and advice on organizing my thoughts were invaluable and necessary to complete this work. I also thank the members of my graduate committee, Dr. Laura Spielvogel and Dr. Frederick H. Smith for taking the time to review my work, and lending important advice. In addition, I would also like to thank my friends Adriana, Cleothia, and Maxwell who supported me in finishing my work. -

Conygar Zdp Plc the Conygar Investment Company Plc Liberum Capital Limited

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take you are recommended to seek your own financial advice immediately from an independent financial adviser, who is authorised under the Financial Services and Markets Act 2000 (as amended) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. A copy of this document, which constitutes a prospectus relating to Conygar ZDP PLC (the ‘‘Issuer’’) in connection with the issue of ZDP shares of £0.01 each in the capital of the Issuer (‘‘ZDP Shares’’), prepared in accordance with the Prospectus Rules of the Financial Conduct Authority (‘‘FCA’’) made under Section 84 of FSMA, has been filed with the FCA in accordance with Rule 3.2 of the Prospectus Rules. Application has been made to the UK Listing Authority and to the London Stock Exchange respectively for admission of the ZDP Shares: (i) to the Official List (by way of a standard listing under Chapter 14 of the Listing Rules); and (ii) to the London Stock Exchange’s main market for listed securities. It is expected that Admission will become effective and that unconditional dealings in the ZDP Shares will commence on the London Stock Exchange at 8.00 a.m. (London time) on 10 January 2014. The attention of prospective investors is drawn, in particular, to the Risk Factors set out on pages 11 to 17 of this prospectus. CONYGAR ZDP PLC (a company incorporated in England and Wales with -

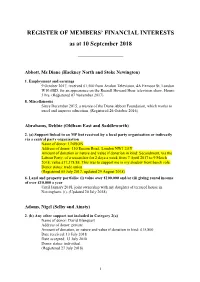

REGISTER of MEMBERS' FINANCIAL INTERESTS As at 10

REGISTER OF MEMBERS’ FINANCIAL INTERESTS as at 10 September 2018 _________________ Abbott, Ms Diane (Hackney North and Stoke Newington) 1. Employment and earnings 9 October 2017, received £1,500 from Avalon Television, 4A Exmoor St, London W10 6BD, for an appearance on the Russell Howard Hour television show. Hours: 3 hrs. (Registered 07 November 2017) 8. Miscellaneous Since December 2015, a trustee of the Diane Abbott Foundation, which works to excel and improve education. (Registered 26 October 2016) Abrahams, Debbie (Oldham East and Saddleworth) 2. (a) Support linked to an MP but received by a local party organisation or indirectly via a central party organisation Name of donor: UNISON Address of donor: 130 Euston Road, London NW1 2AY Amount of donation or nature and value if donation in kind: Secondment, via the Labour Party, of a researcher for 2 days a week from 7 April 2017 to 9 March 2018; value £17,378.88. This was to support me in my shadow front bench role. Donor status: trade union (Registered 05 July 2017; updated 29 August 2018) 6. Land and property portfolio: (i) value over £100,000 and/or (ii) giving rental income of over £10,000 a year Until January 2018, joint ownership with my daughter of terraced house in Nottingham: (i). (Updated 20 July 2018) Adams, Nigel (Selby and Ainsty) 2. (b) Any other support not included in Category 2(a) Name of donor: David Blanquart Address of donor: private Amount of donation, or nature and value if donation in kind: £15,800 Date received: 13 July 2018 Date accepted: 13 July 2018 Donor -

Climate Change and Coastal Human Settlements: Barbados and Guyana

Economic Commission for Latin America and the Caribbean Subregional Headquarters for the Caribbean LIMITED LC/CAR/L.326 22 October 2011 ORIGINAL: ENGLISH AN ASSESSMENT OF THE ECONOMIC IMPACT OF CLIMATE CHANGE ON THE COASTAL AND HUMAN SETTLEMENTS SECTOR IN BARBADOS __________ This document has been reproduced without formal editing. i Acknowledgement The Economic Commission for Latin America and the Caribbean (ECLAC) Subregional Headquarters for the Caribbean wishes to acknowledge the assistance of Maurice Mason, consultant, in the preparation of this report. ii Table of contents I. THE INTRODUCTION .............................................................................................................. 1 A. OVERVIEW ......................................................................................................................... 1 B. OBJECTIVE .......................................................................................................................... 1 C. GENERAL METHODOLOGICAL APPROACH ......................................................................... 2 II. MANIFESTATION OF CLIMATE CHANGE ......................................................................... 3 A. SEA LEVEL RISE ................................................................................................................. 3 B. CHANGE IN WEATHER CONDITION ..................................................................................... 5 1 .Projection for the Atlantic Storm ........................................................................... -

Popular Culture and the Remapping of Barbadian Identity

“In Plenty and In Time of Need”: Popular Culture and the Remapping of Barbadian Identity by Lia Tamar Bascomb A dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in African American Studies in the Graduate Division of University of California, Berkeley Committee in charge: Professor Leigh Raiford, Chair Professor Brandi Catanese Professor Nadia Ellis Professor Laura Pérez Spring 2013 “In Plenty and In Time of Need”: Popular Culture and the Remapping of Barbadian Identity © 2013 by Lia Tamar Bascomb 1 Abstract “In Plenty and In Time of Need”: Popular Culture and the Remapping of Barbadian Identity by Lia Tamar Bascomb Doctor of Philosophy in African American Studies University of California at Berkeley Professor Leigh Raiford, Chair This dissertation is a cultural history of Barbados since its 1966 independence. As a pivotal point in the Transatlantic Slave Trade of the seventeenth and eighteenth centuries, one of Britain’s most prized colonies well into the mid twentieth century, and, since 1966, one of the most stable postcolonial nation-states in the Western hemisphere, Barbados offers an extremely important and, yet, understudied site of world history. Barbadian identity stands at a crossroads where ideals of British respectability, African cultural retentions, U.S. commodity markets, and global economic flows meet. Focusing on the rise of Barbadian popular music, performance, and visual culture this dissertation demonstrates how the unique history of Barbados has contributed to complex relations of national, gendered, and sexual identities, and how these identities are represented and interpreted on a global stage. This project examines the relation between the global pop culture market, the Barbadian artists within it, and the goals and desires of Barbadian people over the past fifty years, ultimately positing that the popular culture market is a site for postcolonial identity formation. -

JIB Group Holdings Limited Annual Report and Financial Statements 31

Company number: 02956529 JIB Group Holdings Limited Annual Report and Financial Statements for the Year Ended 31 December 2019 JIB Group Holdings Limited Company number: 02956529 Contents Company Information 1 Strategic Report 2 to 3 Directors' Report 4 to 5 Statement of Directors' Responsibilities 6 Independent Auditor’s Report 7 to 9 Profit and Loss Account 10 Statement of Comprehensive Income 11 Balance Sheet 12 Statement of Changes in Equity 13 Notes to the Financial Statements 14 to 41 JIB Group Holdings Limited Company number: 02956529 Company Information Directors J Flahive M D Jones Company secretary Marsh Secretarial Services Limited Registered office The St Botolph Building 138 Houndsditch London EC3A 7AW Page 1 JIB Group Holdings Limited Company number: 02956529 Strategic Report for the Year Ended 31 December 2019 The directors present their strategic report for JIB Group Holdings Limited ('the Company') for the year ended 31 December 2019. Principal activities Until 1 April 2019, the Company formed part of the Managed Services Division of Jardine Lloyd Thompson Group plc (‘the JLT Group’). On 1 April 2019 the JLT Group was acquired by Marsh & McLennan Companies, Inc (‘MMC’ or ‘the Group’). The Company acts as an intermediary holding company and expects to trade for the foreseeable future. Business review Profit before taxation amounts to £2,936,364,664 (2018: Loss of £(7,960,953)). During the year, and as part of a wider Group restructure to integrate the JLT Group companies with the MMC companies, the Company adopted new Articles of Association to facilitate the following: • On the 24 June 2019 the Company was transferred the entire legal and beneficial interest in a loan from JLT US. -

Royal Travel Appendix 2017-18

SCHEDULE OF JOURNEYS COSTING £15,000 OR MORE Year Ended 31 March 2018 Household Method of Date Itinerary Description of Engagement Cost (£) travel The Princess Royal Charter / 3-7 Apr London - Accra - Kumasi - FCO visit to Ghana and Sierra Leone. 68,815 Scheduled Flight Freetown - Accra - London The Queen and The Royal Train / 12-13 Apr Windsor - Leicester - Windsor Attend Maundy Service, Leicester Cathedral. 18,768 Duke of Edinburgh S76 The Countess of Wessex Charter 2-3 May Farnborough - Tallinn - The Countess of Wessex Royal Colonel, 5th Battalion The Rifles, 16,316 Farnborough visit 5th Battalion The Rifles in Estonia. The Prince of Wales and Charter / 9-12 May Brize Norton - Aldergrove - Visit Seamus Heaney Homeplace, Bellaghy; open North West 33,812 The Duchess of Helicopter Londonderry - Lisburn - Dublin - Cancer Centre, Altnagelvin Hospital, Londonderry; host reception Cornwall Kilkenny, Thomastown - Curragh at Hillsborough Castle; open PSNI Memorial Garden, Belfast; visit Camp - Kilcullen - Dublin – Brize Dromore; open Dromore Central Primary School. Norton The Queen Charter / 25-May London - Manchester - Tatenhill, Visit Needlewood Estate: Eland Lodge Farmhouse, Hareholes 21,639 Helicopter Tutbury - Birmingham - Farm Cottage, Lower Castle Hayes Farm. Birmingham – Aberdeen The Queen and The Charter 30-May Aberdeen - Northolt Residence to residence. 16,871 Duke of Edinburgh The Duke of York Scheduled Flight 11-16 Jun London - Singapore - London FCO visit to attend the Commonwealth Science Conference in 35,742 Singapore. 29-31 May London - Singapore - London Staff planning visit. The Prince of Wales Royal Train 15-16 Jun Ayr - London Attend investiture at Buckingham Palace. 19,760 The Duke of York Charter 3-5 Jul Farnborough - Aberdeen - Hold Pitch @ Palace on Tour at Elevator; visit Entrepreneur Hub 15,119 Edinburgh - Biggin Hill ABVenture.; attend Palace of Holyroodhouse Garden Party.