Focus On: W2 Focus On: W2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Planning and Transportation Department

TOWN PLANNING APPLICATIONS WEEKLY DECISIONS LIST Week Ending : 03 January 2021 CENTRAL AREA TEAM (Covering the W1 area) This list of decisions made by the Council is divided into the Central, North and South Area Teams and the Trees Team. For further information you can view details of the application and the formal decision online www.westminster.gov.uk/planning. Deirdra Armsby Director of Place Shaping and Town Planning City Hall 64 Victoria Street London SW1E 6QP dcwkdecs091231 1 Bryanston & Dorset Square Hyde Park Knightsbridge & Belgravia Marylebone High Street Address : Sherlock Holmes Hotel Ward : Marylebone High Street 108-114 Baker Street London W1U 8ED Ref. No. : 20/06923/TCH Type: Applic. for tables and chairs Proposal : Use of an area of the public highway measuring 14.0m x 2.5m for the placing of 12 tables, 24 chairs and 14 planters in connection with the existing building use. Date Received : 30.10.20 Date Valid : 04.11.20 Date Amended : 04.11.2020 Date Decision : 30.12.20 Decision Application Permitted Level Delegated Decision Address : Barley Mow Ward : Marylebone High Street 8 Dorset Street London W1U 6QW Ref. No. : 20/07124/LBC Type: Listed Building Consent Application Proposal : Installation of three traditional awnings to front elevation. Date Received : 09.11.20 Date Valid : 09.11.20 Date Amended : 09.11.2020 Date Decision : 30.12.20 Decision Application Permitted Level Delegated Decision St James’s West End Address : 15 Carlos Place Ward : West End London W1K 2EY Ref. No. : 20/05965/FULL Type: Application for full Planning Permission Proposal : Installation of a flagpole on the front of the building. -

Johnson 1 C. Johnson: Social Contract And

C. Johnson: Social Contract and Energy in Pimlico ORIGINAL ARTICLE District heating as heterotopia: Tracing the social contract through domestic energy infrastructure in Pimlico, London Charlotte Johnson UCL Institute for Sustainable Resources, University College London, London, WC1H 0NN, UK Corresponding author: Charlotte Johnson; e-mail: [email protected] The Pimlico District Heating Undertaking (PDHU) was London’s first attempt at neighborhood heating. Built in the 1950s to supply landmark social housing project Churchill Gardens, the district heating system sent heat from nearby Battersea power station into the radiators of the housing estate. The network is a rare example in the United Kingdom, where, unlike other European states, district heating did not become widespread. Today the heating system supplies more than 3,000 homes in the London Borough of Westminster, having survived the closure of the power station and the privatization of the housing estate it supplies. Therefore, this article argues, the neighborhood can be understood as a heterotopia, a site of an alternative sociotechnical order. This concept is used to understand the layers of economic, political, and technological rationalities that have supported PDHU and to question how it has survived radical changes in housing and energy policy in the United Kingdom. This lens allows us to see the tension between the urban planning and engineering perspective, which celebrates this Johnson 1 system as a future-oriented “experiment,” and the reality of managing and using the system on the estate. The article analyzes this technology-enabled standard of living as a social contract between state and citizen, suggesting a way to analyze contemporary questions of district energy. -

Character Overview Westminster Has 56 Designated Conservation Areas

Westminster’s Conservation Areas - Character Overview Westminster has 56 designated conservation areas which cover over 76% of the City. These cover a diverse range of townscapes from all periods of the City’s development and their distinctive character reflects Westminster’s differing roles at the heart of national life and government, as a business and commercial centre, and as home to diverse residential communities. A significant number are more residential areas often dominated by Georgian and Victorian terraced housing but there are also conservation areas which are focused on enclaves of later housing development, including innovative post-war housing estates. Some of the conservation areas in south Westminster are dominated by government and institutional uses and in mixed central areas such as Soho and Marylebone, it is the historic layout and the dense urban character combined with the mix of uses which creates distinctive local character. Despite its dense urban character, however, more than a third of the City is open space and our Royal Parks are also designated conservation areas. Many of Westminster’s conservation areas have a high proportion of listed buildings and some contain townscape of more than local significance. Below provides a brief summary overview of the character of each of these areas and their designation dates. The conservation area audits and other documentation listed should be referred to for more detail on individual areas. 1. Adelphi The Adelphi takes its name from the 18th Century development of residential terraces by the Adam brothers and is located immediately to the south of the Strand. The southern boundary of the conservation area is the former shoreline of the Thames. -

St James Conservation Area Audit

ST JAMES’S 17 CONSERVATION AREA AUDIT AREA CONSERVATION Document Title: St James Conservation Area Audit Status: Adopted Supplementary Planning Guidance Document ID No.: 2471 This report is based on a draft prepared by B D P. Following a consultation programme undertaken by the council it was adopted as Supplementary Planning Guidance by the Cabinet Member for City Development on 27 November 2002. Published December 2002 © Westminster City Council Department of Planning & Transportation, Development Planning Services, City Hall, 64 Victoria Street, London SW1E 6QP www.westminster.gov.uk PREFACE Since the designation of the first conservation areas in 1967 the City Council has undertaken a comprehensive programme of conservation area designation, extensions and policy development. There are now 53 conservation areas in Westminster, covering 76% of the City. These conservation areas are the subject of detailed policies in the Unitary Development Plan and in Supplementary Planning Guidance. In addition to the basic activity of designation and the formulation of general policy, the City Council is required to undertake conservation area appraisals and to devise local policies in order to protect the unique character of each area. Although this process was first undertaken with the various designation reports, more recent national guidance (as found in Planning Policy Guidance Note 15 and the English Heritage Conservation Area Practice and Conservation Area Appraisal documents) requires detailed appraisals of each conservation area in the form of formally approved and published documents. This enhanced process involves the review of original designation procedures and boundaries; analysis of historical development; identification of all listed buildings and those unlisted buildings making a positive contribution to an area; and the identification and description of key townscape features, including street patterns, trees, open spaces and building types. -

The Burlington Arcade Would Like to Welcome You to a VIP Invitation with One of London’S Luxury Must-See Shopping Destinations

The Burlington Arcade would like to welcome you to a VIP Invitation with one of London’s luxury must-see shopping destinations BEST OF BRITISH SUPERIOR LUXURY SHOPPING SERVICE & England’s oldest and longest shopping BEADLES arcade, open since 1819, The Burlington TOURS Arcade is a true luxury landmark in London. The Burlington Beadles Housing over 40 specialist shops and are the knowledgeable designer brands including Lulu Guinness uniformed guards and Jimmy Choo’s only UK menswear of the Arcade ȂƤǡ since 1819. They vintage watches, bespoke footwear and the conduct pre-booked Ƥ Ǥ historical tours of the Located discreetly between Bond Street Arcade for visitors and and Piccadilly, the Arcade has long been uphold the rules of the favoured by Royalty, celebrities and the arcade which include prohibiting the opening of cream of British society. umbrellas, bicycles and whistling. The only person who has been given permission to whistle in the Arcade is Sir Paul McCartney. HOTEL GUEST BENEFITS ǤǡƤ the details below and hand to the Burlington Beadles when you visit. They will provide you with the Burlington VIP Card. COMPLIMENTARY VIP EXPERIENCES ơ Ǥ Pre-booked at least 24 hours in advance. Ƥǣ ǡ the expert consultants match your personality to a fragrance. This takes 45 minutes and available to 1-6 persons per session. LADURÉE MACAROONS ǣ Group tea tasting sessions at LupondeTea shop can Internationally famed for its macaroons, Ǧ ơ Parisian tearoom Ladurée, lets you rest and Organic Tea Estate. revive whilst enjoying the surroundings of the To Pre-book simply contact Ellen Lewis directly on: beautiful Arcade. -

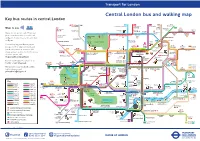

Central London Bus and Walking Map Key Bus Routes in Central London

General A3 Leaflet v2 23/07/2015 10:49 Page 1 Transport for London Central London bus and walking map Key bus routes in central London Stoke West 139 24 C2 390 43 Hampstead to Hampstead Heath to Parliament to Archway to Newington Ways to pay 23 Hill Fields Friern 73 Westbourne Barnet Newington Kentish Green Dalston Clapton Park Abbey Road Camden Lock Pond Market Town York Way Junction The Zoo Agar Grove Caledonian Buses do not accept cash. Please use Road Mildmay Hackney 38 Camden Park Central your contactless debit or credit card Ladbroke Grove ZSL Camden Town Road SainsburyÕs LordÕs Cricket London Ground Zoo Essex Road or Oyster. Contactless is the same fare Lisson Grove Albany Street for The Zoo Mornington 274 Islington Angel as Oyster. Ladbroke Grove Sherlock London Holmes RegentÕs Park Crescent Canal Museum Museum You can top up your Oyster pay as Westbourne Grove Madame St John KingÕs TussaudÕs Street Bethnal 8 to Bow you go credit or buy Travelcards and Euston Cross SadlerÕs Wells Old Street Church 205 Telecom Theatre Green bus & tram passes at around 4,000 Marylebone Tower 14 Charles Dickens Old Ford Paddington Museum shops across London. For the locations Great Warren Street 10 Barbican Shoreditch 453 74 Baker Street and and Euston Square St Pancras Portland International 59 Centre High Street of these, please visit Gloucester Place Street Edgware Road Moorgate 11 PollockÕs 188 TheobaldÕs 23 tfl.gov.uk/ticketstopfinder Toy Museum 159 Russell Road Marble Museum Goodge Street Square For live travel updates, follow us on Arch British -

1 Draft Paper Elisabete Mendes Silva Polytechnic Institute of Bragança

Draft paper Elisabete Mendes Silva Polytechnic Institute of Bragança-Portugal University of Lisbon Centre for English Studies, Faculty of Arts and Humanities, Portugal [email protected] Power, cosmopolitanism and socio-spatial division in the commercial arena in Victorian and Edwardian London The developments of the English Revolution and of the British Empire expedited commerce and transformed the social and cultural status quo of Britain and the world. More specifically in London, the metropolis of the country, in the eighteenth century, there was already a sheer number of retail shops that would set forth an urban world of commerce and consumerism. Magnificent and wide-ranging shops served householders with commodities that mesmerized consumers, giving way to new traditions within the commercial and social fabric of London. Therefore, going shopping during the Victorian Age became mandatory in the middle and upper classes‟ social agendas. Harrods Department store opens in 1864, adding new elements to retailing by providing a sole space with a myriad of different commodities. In 1909, Gordon Selfridge opens Selfridges, transforming the concept of urban commerce by imposing a more cosmopolitan outlook in the commercial arena. Within this context, I intend to focus primarily on two of the largest department stores, Harrods and Selfridges, drawing attention to the way these two spaces were perceived when they first opened to the public and the effect they had in the city of London and in its people. I shall discuss how these department stores rendered space for social inclusion and exclusion, gender and race under the spell of the Victorian ethos, national conservatism and imperialism. -

Commissioning Case Study Co-Production of Early Years Services in Queen’S Park

Commissioning case study Co-production of early years services in Queen’s Park co-design whole-systems model cost–benefit analysis community champions early years services of the community with the intention of reversing generations of state dependency and of reforming The headlines hyper-local public and community services. A community meeting was held to discuss priorities and residents raised particular concerns about gang l Westminster City Council’s children’s services violence and more broadly about the quality and department and Central London Community Health availability of services and support for children and are committed to a neighbourhood-based co-design young people. Early years was chosen by residents of children’s centre services. to be the focus of the neighbourhood community budget pilot. It was estimated that in the four years l The neighbourhood community budget pilot that would follow the launch of the pilot around one has provided an opportunity to develop and test thousand new children would be born in the Queen’s an integrated, whole-systems model for the delivery Park ward. The ambition for the community was for of early years services, with residents and partner these children to benefit from a progressive reduction agencies working together in new ways. of risk in their later years. l The pace of change within different organisations When deciding on the early years focus, residents represented on a partnership is not consistent made the point that they were concerned not solely and this has to be taken into account when with money but also with the way in which the establishing a timeline for co-designing and design of services took place largely unseen by the co-commissioning services. -

LONDON Cushman & Wakefield Global Cities Retail Guide

LONDON Cushman & Wakefield Global Cities Retail Guide Cushman & Wakefield | London | 2019 0 For decades London has led the way in terms of innovation, fashion and retail trends. It is the focal location for new retailers seeking representation in the United Kingdom. London plays a key role on the regional, national and international stage. It is a top target destination for international retailers, and has attracted a greater number of international brands than any other city globally. Demand among international retailers remains strong with high profile deals by the likes of Microsoft, Samsung, Peloton, Gentle Monster and Free People. For those adopting a flagship store only strategy, London gives access to the UK market and is also seen as the springboard for store expansion to the rest of Europe. One of the trends to have emerged is the number of retailers upsizing flagship stores in London; these have included Adidas, Asics, Alexander McQueen, Hermès and Next. Another developing trend is the growing number of food markets. Openings planned include Eataly in City of London, Kerb in Seven Dials and Market Halls on Oxford Street. London is the home to 8.85 million people and hosting over 26 million visitors annually, contributing more than £11.2 billion to the local economy. In central London there is limited retail supply LONDON and retailers are showing strong trading performances. OVERVIEW Cushman & Wakefield | London | 2019 1 LONDON KEY RETAIL STREETS & AREAS CENTRAL LONDON MAYFAIR Central London is undoubtedly one of the forefront Mount Street is located in Mayfair about a ten minute walk destinations for international brands, particularly those from Bond Street, and has become a luxury destination for with larger format store requirements. -

PEMBROKE BUILDING KENSINGTON VILLAGE Avonmore Road London W14 8DG

PEMBROKE BUILDING KENSINGTON VILLAGE Avonmore Road London W14 8DG 4th floor office TON V ING ILL S Avonmore Rd A N G E E K A315 Kensington A Gardens Stoner Rd B Stanwick Rd C A315 Hyde Park Gate PEMBROKE A3220 BUILDING D E HIGH STREET KENSINGTON LOCATION: A315 The Pembroke Building is located in Kensington Village, Warwiick Road Warwick Gardens Queens Gate between Hammersmith and Kensington, adjacent to Cromwell Road (A4) and just South of Hammersmith KENSINGTON Road. The building is a short walk from West Kensington OLYMPIA Keinsington High Street (4 mins) and Earls Court (12 mins). The Village also benefits from pedestrian entrances from the A4 with Warwiick Road A3220 Earls Court Road vehicular access from Avonmore Road. Olympia Brook Green A219 Shepherds Bush Road Cromwell Road Hammersmith Road A4 4 A315 1 EARLS A3220 HAMMERSMITH 3 A4 COURT Old Brompton Road A3218 5 Talgarth Road Earls Court A4 2 WEST 7 KENSINGTON A3220 BARONS COURT Redclie Gardens 6 Finborough Road WEST North End Rd Queens Club BROMPTON lham Road Fu Charing Lillie Road Chelsea & Cross Westminster Hospital Normand Hospital Park A219 Directory: Lillie Road Local Occupiers: Lillie Road Homestead Rd 1. Tesco Superstore 5. Fortune (Chinese Restaurant) A. Universal Music, C. ArchantA308 A3220 2. Famous Three Kings (pub) 6. Eat-Aroi (Thai Restaurant) ADM Promotions & D. Holler Digital, A308 3. Sainsbury’s Local 7. Curtains Up (pub) Eaglemoss Publications Leo Burnett & Kaplan ad 4. Premier Inn (hotel) & Barons Court Theatre B. CACI Ltd E. Zodiak Media Digital Store CONNECTIVITY: Transport links to Kensington Village are excellent, with Earls Court, West Kensington (District line), Kensington Olympia (District and Mainline) and Barons Court (Piccadilly line) a short walk away providing good links into central London and the West. -

The Challenges of French Impressionism in Great Britain

Crossing the Channel: The Challenges of French Impressionism in Great Britain By Catherine Cheney Senior Honors Thesis Department of Art History University of North Carolina at Chapel Hill April 8, 2016 Approved: 1 Introduction: French Impressionism in England As Impressionism spread throughout Europe in the late nineteenth century, the movement took hold in the British art community and helped to change the fundamental ways in which people viewed and collected art. Impressionism made its debut in London in 1870 when Claude Monet, Camille Pissarro, and Paul Durand-Ruel sought safe haven in London during the Franco- Prussian war. The two artists created works of London landscapes done in the new Impressionist style. Paul Durand-Ruel, a commercial dealer, marketed the Impressionist works of these two artists and of the other Impressionist artists that he brought over from Paris. The movement was officially organized for the First Impressionist Exhibition in 1874 in Paris, but the initial introduction in London laid the groundwork for promoting this new style throughout the international art world. This thesis will explore, first, the cultural transformations of London that allowed for the introduction of Impressionism as a new style in England; second, the now- famous Thames series that Monet created in the 1890s and notable exhibitions held in London during the time; and finally, the impact Impressionism had on private collectors and adding Impressionist works to the national collections. With the exception of Edouard Manet, who met with success at the Salon in Paris over the years and did not exhibit with the Impressionists, the modern artists were not received well. -

London “By Seeing London, I Have Seen As Much of Life As the World Can Show.” - Samuel Johnson, 1773

London “By seeing London, I have seen as much of life as the world can show.” - Samuel Johnson, 1773 Beautifully situated in the enviable borough of Westminster, the Residences offers luxury and bespoke design with overwhelming views of the City’s skyline without compromise. THE WESTMINSTER RESIDENCES Unrivalled location in the heart of Westminster Village Horse Guards Parade London Eye Westminster Abbey St James's Park Houses of Parliament EDGWARE ROAD London School of Economics and Political Science London Film School King's College Imperial College THE WESTMINSTER RESIDENCES London College of Communication Chelsea Physics Gardens N WORLD HERITAGE HISTORY FINEST BESPOKE APARTMENTS ExQuisIte Private SettingS “London is a modern Babylon.” - Benjamin Disraeli An historic building of IMPRESSIVE STATURE nestles in the heart of WESTMINSTER VILLAGE. Offering a collection of 14 EXQUISITE high-end residential LUXURY APARTMENTS THE WESTMINSTER RESIDENCES GREAT PETER STREET The distinguished history of Great Peter Street has witnessed the grandeur of London society over the last 300 years. 29 Great Peter Street has a long and illustrious history spanning several centuries. It was one of the streets that Charles Dickens has written about and named it as ‘the Devil’s acre’. However it has since become the epicentre of the British political establishment, situated as it is, literally a stone’s throw from the Houses of Parliament. Architecturally, the area in which Great Peter Street sits has quintessen- tially been described as ‘the essence of Old Westminster’. This exceptional location is surrounded by Grade II listed houses from the 1700s. The building itself is a homage to Georgian architecture and also it is prevalent in the area.