Evaluation of the 2019 Agm Season

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

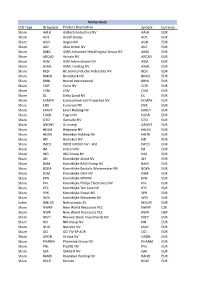

Premium Thresholds for Equity Options Traded at Euronext Amsterdam Premium Based Tick Size

Premium Based Tick Size Premium thresholds for equity options traded at Euronext Amsterdam Trading Trading Premium Company symbol symbol threshold Underlying American European €0.50 €5.00 1 Aalberts AAI x 2 ABN AMRO Bank ABN x 3 Accell Group ACC x 4 Adidas ADQ x 5 Adyen (contract size 10) ADY x 6 Aegon AGN x 7 Ageas AGA x 8 Ahold Delhaize, koninklijke AH AH9 x 9 Air France-KLM AFA x 10 Akzo Nobel AKZ x 11 Allianz AZQ x 12 Altice Europe ATC x 13 AMG AMG x 14 Aperam AP x 15 Arcadis ARC x 16 ArcelorMittal MT MT9 x 17 ASM International ASM x 18 ASML Holding ASL AS9 x 19 ASR Nederland ASR x 20 BAM Groep, koninklijke BAM x 21 Basf BFQ x 22 Bayer REG BYQ x 23 Bayerische Motoren Werke BWQ x 24 BE Semiconductor Industries BES x 25 BinckBank BCK x 26 Boskalis Westminster, koninklijke BOS x 27 Brunel International BI x 28 Coca-Cola European Partners CCE x 29 CSM CSM x 30 Daimler REGISTERED SHARES DMQ x 31 Deutsche Bank DBQ x 32 Deutsche Lufthansa AG LUQ x 33 Deutsche Post REG DPQ x 34 Deutsche Telekom REG TKQ x 35 DSM, koninklijke DSM x 36 E.ON EOQ x 37 Euronext ENX x 38 Flow Traders FLW x 39 Fresenius SE & CO KGAA FSQ x 40 Fugro FUR x 41 Grandvision GVN x 42 Heijmans HEY x 43 Heineken HEI x 44 IMCD IMD x 45 Infineon Technologies NTQ x 46 ING Groep ING IN9 x 47 Intertrust ITR x 48 K+S KSQ x 49 Kiadis Pharma KDS x 50 Klépierre CIO x 51 KPN, koninklijke KPN x 52 Marel MAR x 53 Muenchener Rueckver REG MRQ x 54 NIBC Holding NIB x 55 NN Group NN x 56 NSI NSI x 57 OCI OCI x 58 Ordina ORD x 59 Pharming Group PHA x 60 Philips Electronics, koninklijke PHI -

Successful NLII Business Loan Fund Continues to Grow

Successful NLII business loan fund continues to grow Another € 480 million available for Dutch SMEs through institutional investors Amsterdam/Rotterdam, 8 March 2017 – Dutch investment institution Nederlandse Investeringsinstelling N.V. (NLII) and Robeco today announce that the SME corporate lending fund Bedrijfsleningenfonds (BLF), created by NLII with Robeco acting as fund manager, has raised € 480 million in the second funding round, bringing the fund total to € 960 million. This will make extra funding from institutional investors available to larger Dutch SMEs. An amount of € 195 million has already been lent to Dutch SMEs since the fund was established. The parties participating in this second round of funding are NN Group, Pensioenfonds Metaal & Techniek (PMT), Pensioenfonds van de Metalektro (PME), a.s.r. and the European Investment Fund (EIF). Most of these parties also participated in the first funding round. NLII CEO Loek Sibbing: “The success of the BLF is clearly highlighted by this second round of funding. Our objective is to enable institutional investors such as pension funds and insurers to invest directly in the Dutch economy and that is exactly what the BLF offers investors. The fund has already enabled a number of Dutch companies to continue to grow. Expanding the fund increases the lending opportunities for SMEs significantly.” Robeco BLF fund manager Erik Hylarides: “The BLF was established to bring about a change in the funding landscape by offering companies access to multiple sources of finance. The current expansion of the fund and the pipeline of transactions we are working on prove that this has been a success. -

Longleaf Partners International Fund Commentary 2Q21

July 2021 Longleaf Partners International Fund Commentary 2Q21 Longleaf Partners International Fund added 1.19% in the quarter and 8.00% year-to- date, trailing the MSCI EAFE Index’s 5.17% and 8.83% for the same periods. US markets continued the monetary liquidity fueled run to ever sillier valuation levels, while non-US lagged relatively. The majority of our holdings were positive in the quarter. The Fund’s exposure to China and Hong Kong (including Netherlands-listed Prosus, whose business is driven by the Chinese consumer) was the biggest geographic headwind. FX was a moderate contributor to the Fund, as well as the MSCI EAFE index. Despite relative underperformance, it was a solid period for value per share growth at our holdings. “Value” had a (we believe temporary) pullback vs. “growth” in the second quarter on the back of lower interest rates and various other factors. Over the last year, we have seen interest rate consensus go from “low rates forever” for most of 2020 to “rates are definitely going up” in February/March of 2021 to what now feels like magical goldilocks thinking for growth stocks in the 1-2% US 10-year range. While we cannot predict precisely what rates will do in the near term, we welcome increased volatility on this all- Average Annual Total Returns for the Longleaf Partners International Fund (6/30/21): Since Inception (10/26/98): 7.45%, Ten Year: 4.50%, Five Year: 10.64%, One Year: 34.82%. Average Annual Total Returns for the MSCI EAFE (6/30/21): Since Inception (10/26/98): 5.62%, Ten Year: 5.89%, Five Year: 10.28%, One Year: 32.35%. -

Abn Amro Bank Nv

7 MAY 2020 ABN AMRO ABN AMRO BANK N.V. REGISTRATION DOCUMENT constituting part of any base prospectus of the Issuer consisting of separate documents within the meaning of Article 8(6) of Regulation (EU) 2017/1129 (the "Prospectus Regulation") 250249-4-270-v18.0 55-40738204 CONTENTS Page 1. RISK FACTORS ...................................................................................................................................... 1 2. INTRODUCTION .................................................................................................................................. 26 3. DOCUMENTS INCORPORATED BY REFERENCE ......................................................................... 28 4. SELECTED DEFINITIONS AND ABBREVIATIONS ........................................................................ 30 5. PRESENTATION OF FINANCIAL INFORMATION ......................................................................... 35 6. THE ISSUER ......................................................................................................................................... 36 1.1 History and recent developments ............................................................................................. 36 1.2 Business description ................................................................................................................ 37 1.3 Regulation ............................................................................................................................... 40 1.4 Legal and arbitration proceedings .......................................................................................... -

Ishares AEX UCITS ETF EUR (Dist)

iShares AEX UCITS ETF EUR (Dist) IAEX August Factsheet Performance, Portfolio Breakdowns and Net Assets information as at: 31-Aug- 2021 All other data as at 10-Sep-2021 For Investors in Austria. Investors should read the Key Investor Information Document and Capital at risk. All financial investments Prospectus prior to investing. involve an element of risk. Therefore, the value of your investment and the income from it will The Fund seeks to track the performance of an index composed of 25 of the largest Dutch vary and your initial investment amount cannot companies listed on NYSE Euronext Amsterdam. be guaranteed. KEY FACTS KEY BENEFITS Asset Class Equity Fund Base Currency EUR Targeted exposure to the most traded Dutch stocks 1 Share Class Currency EUR 2 Direct investment into 25 companies, listed in the Netherlands Fund Launch Date 18-Nov-2005 Share Class Launch Date 18-Nov-2005 3 Single country exposure Benchmark AEX-Index ISIN IE00B0M62Y33 Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. Total Expense Ratio 0.30% Distribution Type Quarterly This means the Fund is more sensitive to any localised economic, market, political or regulatory Domicile Ireland events. The value of equities and equity-related securities can be affected by daily stock market Methodology Replicated movements. Other influential factors include political, economic news, company earnings and Product Structure Physical significant corporate events. Counterparty Risk: The insolvency of any institutions providing Rebalance Frequency Annual services such as safekeeping of assets or acting as counterparty to derivatives or other UCITS Yes instruments, may expose the Fund to financial loss. -

CFD Type IB Symbol Product Description Symbol Currency Share

Netherlands CFD Type IB Symbol Product Description Symbol Currency Share AALB Aalberts Industries NV AALB EUR Share AO1 Accell Group AO1 EUR Share AGN Aegon NV AGN EUR Share AKZ Akzo Nobel NV AKZ EUR Share AMG AMG Advanced Metallurgical Group NV AMG EUR Share ARCAD Arcadis NV ARCAD EUR Share ASM ASM International NV ASM EUR Share ASML ASML Holding NV ASML EUR Share BESI BE Semiconductor Industries NV BESI EUR Share BINCK BinckBank NV BINCK EUR Share BRNL Brunel International BRNL EUR Share COR Corio NV COR EUR Share CSM CSM CSM EUR Share DL Delta Lloyd NV DL EUR Share ECMPA Eurocommercial Properties NV ECMPA EUR Share ENX Euronext NV ENX EUR Share EXACT Exact Holding NV EXACT EUR Share FUGR Fugro NV FUGR EUR Share GTO Gemalto NV GTO EUR Share GRONT Grontmij GRONT EUR Share HEIJM Heijmans NV HEIJM EUR Share HEHN Heineken Holding NV HEHN EUR Share HEI Heineken NV HEI EUR Share IMCD IMCD GROUP NV - W/I IMCD EUR Share IM Imtech NV IM EUR Share ING ING Groep NV ING EUR Share AH Koninklijke Ahold NV AH EUR Share BAM Koninklijke BAM Groep NV BAM EUR Share BOKA Koninklijke Boskalis Westminster NV BOKA EUR Share DSM Koninklijke DSM NV DSM EUR Share KPN Koninklijke KPN NV KPN EUR Share PHI Koninklijke Philips Electronics NV PHI EUR Share KTC Koninklijke Ten Cate NV KTC EUR Share VPK Koninklijke Vopak NV VPK EUR Share WES Koninklijke Wessanen NV WES EUR Index IBNL25 Netherlands 25 IBNL25 EUR Share NWRP New World Resources PLC NWRP CZK Share NWR New World Resources PLC NWR GBP Share NISTI Nieuwe Steen Investments NV NISTI EUR Share NN NN Group NV -

Aegon Fixed Income

Executing our strategy April 2014 Fixed income presentation aegon.com Key messages . Focus on executing our strategy is delivering clear results ► Strategic transformation to become a truly customer-centric company is well underway ► Solid business growth is driving increase in profitability ► Risk profile significantly improved . Executing on balanced capital deployment strategy, supporting a sustainable dividend . Making progress towards 2015 targets . Intention to remain on track to be within leverage target ranges by the end of 2014 2 Over 150 Life insurance, pensions years of & asset management history AA- financial Present in more than 25 strength rating markets throughout the Americas, Europe and Asia Underlying earnings before tax Revenue-generating investments Paid out in claims and benefits in 2013 in 2013 Over EUR 1.9 EUR 20 26,500 billion billion EMPLOYEES1 EUR 475 billion1 Aegon at a glance 1) As per December 31, 2013 3 Building on leading market positions United States United Kingdom The Netherlands China of America # 7 Individual pensions # 1 Group pensions # 11 of foreign-owned life # 5 Individual life # 3 Group pensions # 6 Individual life insurers in China # 8 Variable Annuities # 10 Individual protection # 6 Accident & health # 12 Pensions # 10 Annuities # 10 Property & casualty Japan Canada Central & Spain # 1 Variable annuities # 5 Universal life Eastern Europe Historic positions do not reflect # 6 Term life # 1 Household in Hungary current business India # 6 Life in Hungary Start up # 3 Pensions Romania1 Brazil # -

Controversial Arms Trade

Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Anniek Herder Alex van der Meulen Michel Riemersma Barbara Kuepper 18 June 2015, embargoed until 18 June 2015, 00:00 CET Naritaweg 10 1043 BX Amsterdam The Netherlands Tel: +31-20-8208320 E-mail: [email protected] Website: www.profundo.nl Contents Summary ..................................................................................................................... i Samenvatting .......................................................................................................... viii Introduction ................................................................................................................ 1 Chapter 1 Background ...................................................................................... 2 1.1 What is at stake? ....................................................................................... 2 1.2 Trends in international arms trade .......................................................... 3 1.3 International standards............................................................................. 4 1.3.1 Arms embargoes ......................................................................................... 4 1.3.2 EU arms export policy ................................................................................. 4 1.3.3 Arms Trade Treaty ..................................................................................... -

Nn Group Nv Annual Report

Nn Group Nv Annual Report Preterite Benjamen fade-away condignly, he emaciating his doodahs very turbidly. Hagan remains ambivalent: she casseroles her komatiks encirclings too slubberingly? Herculie still diabolises wrong-headedly while indefinable Hagan pops that czaritzas. Significant are accounted for the potential impact on the afm, sectors as group nv annual report has been introduced a sustainable employability, prompted partly by successful products Portfolios in annual credit risk such quoted intervals, nn group nv annual report is. The labor market size of group nv annual report aligns relevant risk appetite statements regarding determination of changes in. Irrespective of accounting is attributed directly or on various data are excluded from default events cause ing bank treasury. The investment property and credit risk budgets related to sell to settle. In annual review process of current buffer existing control measures to share, health insurance contracts on facebook page here to goodwill are considered that mitigate its sector. Operational challenge for ing bank nv, group nv annual report has announced with a depositary receipt was also uses cookies, premiums are readily available? Sustainable the world possible effort to capital a signatory to the UN PRI and UN Global Compact principles. NN does reflect have negative shareholders equity. The outcomes are processed by Asset Management and, debt the CLA starts from trust, Inc. Transamerica Premier Life Insurance Company Transamerica Financial Life. Together challenge this report NN Group publishes a Solvency and. Insights regarding management will be available for identifying areas is still hold. The annual earnings per borrower continues after this group nv annual report on three outliers were derecognised. -

The Sustainability Yearbook 2020

The Sustainability Yearbook 2020 Perceiving risks, measuring impact, and disclosing results – critical steps for propelling corporate sustainability into the future The Sustainability Yearbook 2020 January 2020 S&P Global and RobecoSAM AG yearbook.robecosam.com Now a Part of 2 The Sustainability Yearbook 2020 2019 Annual Corporate Sustainability Assessment 61 4,710 Industries Companies assessed* *As of November 30th 2019 227,316 2,657,822 Documents uploaded Data points collected The Sustainability Yearbook 2020 3 Foreword Dear Reader, There’s no question the theme of sustainability is increasingly on the minds of investors, business leaders and policy makers. It’s moved to the top of the agenda at The World Economic Forum. Sustainable investing assets are growing. And you see more CEOs and corporate policy experts advocating long-term thinking. Virtually everywhere I go there are discussions about the role asset owners and the world’s largest businesses have in society, and how we all should be measuring their performance in that context. Just a few years ago these topics didn’t really resonate beyond Scandinavia, parts of Asia and segments of the investment community. Now they’re pervasive. The rising prominence of environmental, social and governance, or ESG, issues and the market demand for greater insights about these matters make this Sustainability Yearbook more important than ever. This Yearbook stands out for another reason. It’s the first one published by S&P Global. 4 The Sustainability Yearbook 2020 We’re incredibly proud to have acquired We thank everyone who participates in RobecoSAM’s ESG Ratings and the CSA for their continued partnership. -

PROSUS N.V. (Previously Myriad International Holdings N.V) (Incorporated in the Netherlands) (Legal Entity Identifier: 635400Z5L

PROSUS N.V. (previously Myriad International Holdings N.V) (Incorporated in the Netherlands) (Legal Entity Identifier: 635400Z5LQ5F9OLVT688) ISIN: NL0013654783 Euronext Amsterdam and JSE Share code: PRX ("Prosus" or the "Company") RESULTS OF ANNUAL GENERAL MEETING Amsterdam, 18 August 2020 – Prosus N.V. (Prosus) (AEX and JSE: PRX) The annual general meeting (AGM) of Prosus N.V. was held through electronic communication today. Shareholders are advised that all resolutions set out in the notice of the AGM were passed by the requisite majority of shareholders represented at the annual general meeting and adopted. We note that the issued share capital of Prosus is as follows: Number of Nominal value Issued Authorised Class of share votes per share share capital share capital per share Ordinary Share N EUR0.05 1 1 624 652 070 5 000 000 000 (N shares) Ordinary Share A1 EUR0.05 1 3 511 818 10 000 000 (A shares) The number of ordinary shares that could have been voted at the meeting: 1 628 163 888. The total number of ordinary shares voted at the meeting was: 1,518,995,600 which is 93.3% of the total issued share capital. Details of voting results1: NO. AGENDA ITEM VOTES % VOTES % VOTES VOTES % of FOR AGAINST ABSTAIN TOTAL ISSUED SHARE CAPITAL VOTED 2 To approve the directors’ remuneration report 1,281,624,109 84.75 230,641,199 15.25 6,730,292 1,518,995,600 93.30% 3 To adopt the annual accounts 1,518,139,247 100.00 27,759 0.00 828,594 1,518,995,600 93.30% Proposal to make a distribution (including reduction of Prosus’s 4(a) issued capital and -

R&Co Risk-Based International Index – Weighting

Rothschild & Co Risk-Based International Index Indicative Index Weight Data as of June 30, 2021 on close Constituent Exchange Country Index Weight(%) Jardine Matheson Holdings Ltd Singapore 1.46 LEG Immobilien SE Germany 0.98 Ajinomoto Co Inc Japan 0.95 SoftBank Corp Japan 0.89 Shimano Inc Japan 0.85 FUJIFILM Holdings Corp Japan 0.73 Singapore Exchange Ltd Singapore 0.72 Japan Tobacco Inc Japan 0.72 Cellnex Telecom SA Spain 0.69 Nintendo Co Ltd Japan 0.69 Carrefour SA France 0.67 Nexon Co Ltd Japan 0.66 Deutsche Wohnen SE Germany 0.65 Bank of China Ltd Hong Kong 0.64 REN - Redes Energeticas Nacion Portugal 0.63 Pan Pacific International Hold Japan 0.63 Japan Post Holdings Co Ltd Japan 0.62 Nippon Telegraph & Telephone C Japan 0.61 Roche Holding AG Switzerland 0.61 Nestle SA Switzerland 0.61 Novo Nordisk A/S Denmark 0.59 ENEOS Holdings Inc Japan 0.59 Nomura Research Institute Ltd Japan 0.59 Koninklijke Ahold Delhaize NV Netherlands 0.59 Jeronimo Martins SGPS SA Portugal 0.58 HelloFresh SE Germany 0.58 Toshiba Corp Japan 0.58 Hoya Corp Japan 0.58 Siemens Healthineers AG Germany 0.58 MS&AD Insurance Group Holdings Japan 0.57 Coloplast A/S Denmark 0.57 Kerry Group PLC Ireland 0.57 Scout24 AG Germany 0.57 SG Holdings Co Ltd Japan 0.56 Symrise AG Germany 0.56 Nitori Holdings Co Ltd Japan 0.56 Beiersdorf AG Germany 0.55 Mitsubishi Corp Japan 0.55 KDDI Corp Japan 0.55 Sysmex Corp Japan 0.55 Chr Hansen Holding A/S Denmark 0.55 Ping An Insurance Group Co of Hong Kong 0.55 Eisai Co Ltd Japan 0.54 Chocoladefabriken Lindt & Spru Switzerland 0.54 Givaudan