Corporate Template-Set Achmea

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Press Release – 2019 Annual Results

Press Release 12 March 2020 - Achmea Annual Results 2019 Achmea records significantly increased operational result of €547 million • Strong Non-Life result with a combined ratio of 95.0% • Sustained good Pension & Life results • Positive result current underwriting year for basic and supplementary health insurance • Strong growth in Non-Life, Retirement Services and international activities; Assets under Management grew to €200 billion at the start of 2020 • Solvency ratio robust at 214%, partly supported by financial markets • Business model expanded further with new propositions and services Willem van Duin, Chairman of the Executive Board: “As an insurer with a cooperative identity, Achmea is committed to a healthy, safe and future-proof society. We put that strategy into practice through our brands and make a difference to the lives of our customers. A sound and sustainable financial result is essential to our ability to properly fulfil our role in society. Achmea ended 2019 well with an increase of the operational result to €547 million and a solvency ratio that rose further to 214% after dividend payments. We have seen growth in both the number of customers and written premiums in property & casualty insurance, as well as a further increase in the result from our pension & life insurance activities. Our new pension services model, in which we offer a comprehensive package of asset management and banking services, is appreciated highly by our customers. The result over the 2019 underwriting year was positive for both basic and supplementary health insurance. However, the negative results on prior underwriting years caused a negative result on overall basic health insurance. -

Premium Thresholds for Equity Options Traded at Euronext Amsterdam Premium Based Tick Size

Premium Based Tick Size Premium thresholds for equity options traded at Euronext Amsterdam Trading Trading Premium Company symbol symbol threshold Underlying American European €0.50 €5.00 1 Aalberts AAI x 2 ABN AMRO Bank ABN x 3 Accell Group ACC x 4 Adidas ADQ x 5 Adyen (contract size 10) ADY x 6 Aegon AGN x 7 Ageas AGA x 8 Ahold Delhaize, koninklijke AH AH9 x 9 Air France-KLM AFA x 10 Akzo Nobel AKZ x 11 Allianz AZQ x 12 Altice Europe ATC x 13 AMG AMG x 14 Aperam AP x 15 Arcadis ARC x 16 ArcelorMittal MT MT9 x 17 ASM International ASM x 18 ASML Holding ASL AS9 x 19 ASR Nederland ASR x 20 BAM Groep, koninklijke BAM x 21 Basf BFQ x 22 Bayer REG BYQ x 23 Bayerische Motoren Werke BWQ x 24 BE Semiconductor Industries BES x 25 BinckBank BCK x 26 Boskalis Westminster, koninklijke BOS x 27 Brunel International BI x 28 Coca-Cola European Partners CCE x 29 CSM CSM x 30 Daimler REGISTERED SHARES DMQ x 31 Deutsche Bank DBQ x 32 Deutsche Lufthansa AG LUQ x 33 Deutsche Post REG DPQ x 34 Deutsche Telekom REG TKQ x 35 DSM, koninklijke DSM x 36 E.ON EOQ x 37 Euronext ENX x 38 Flow Traders FLW x 39 Fresenius SE & CO KGAA FSQ x 40 Fugro FUR x 41 Grandvision GVN x 42 Heijmans HEY x 43 Heineken HEI x 44 IMCD IMD x 45 Infineon Technologies NTQ x 46 ING Groep ING IN9 x 47 Intertrust ITR x 48 K+S KSQ x 49 Kiadis Pharma KDS x 50 Klépierre CIO x 51 KPN, koninklijke KPN x 52 Marel MAR x 53 Muenchener Rueckver REG MRQ x 54 NIBC Holding NIB x 55 NN Group NN x 56 NSI NSI x 57 OCI OCI x 58 Ordina ORD x 59 Pharming Group PHA x 60 Philips Electronics, koninklijke PHI -

Report Profundo

Eerlijke Verzekeringswijzer Dutch Fair Insurance Guide A Case Study on Transparency & Accountability A research paper for Amnesty International, Dierenbescherming, FNV, Milieudefensie, Oxfam Novib and PAX Eerlijke Verzekeringswijzer Dutch Fair Insurance Guide A Case Study on Transparency & Accountability A research paper for Amnesty International, Dierenbescherming, FNV, Milieudefensie, Oxfam Novib and PAX Date of publication 5 July 2016 Hester Brink, Retno Kusumaningtyas, Michel Riemersma, Joeri de Wilde Naritaweg 10 1043 BX Amsterdam The Netherlands Tel: +31-20-8208320 E-mail: [email protected] Website: www.profundo.nl Contents Samenvatting ............................................................................................................ i Summary ......................................................................................................... vii Introduction ........................................................................................................... 1 Chapter 1 Background ...................................................................................... 3 1.1 What is at stake? ....................................................................................... 3 1.2 Themes ...................................................................................................... 4 1.2.1 Organisation................................................................................................ 4 1.2.2 Policy ......................................................................................................... -

Successful NLII Business Loan Fund Continues to Grow

Successful NLII business loan fund continues to grow Another € 480 million available for Dutch SMEs through institutional investors Amsterdam/Rotterdam, 8 March 2017 – Dutch investment institution Nederlandse Investeringsinstelling N.V. (NLII) and Robeco today announce that the SME corporate lending fund Bedrijfsleningenfonds (BLF), created by NLII with Robeco acting as fund manager, has raised € 480 million in the second funding round, bringing the fund total to € 960 million. This will make extra funding from institutional investors available to larger Dutch SMEs. An amount of € 195 million has already been lent to Dutch SMEs since the fund was established. The parties participating in this second round of funding are NN Group, Pensioenfonds Metaal & Techniek (PMT), Pensioenfonds van de Metalektro (PME), a.s.r. and the European Investment Fund (EIF). Most of these parties also participated in the first funding round. NLII CEO Loek Sibbing: “The success of the BLF is clearly highlighted by this second round of funding. Our objective is to enable institutional investors such as pension funds and insurers to invest directly in the Dutch economy and that is exactly what the BLF offers investors. The fund has already enabled a number of Dutch companies to continue to grow. Expanding the fund increases the lending opportunities for SMEs significantly.” Robeco BLF fund manager Erik Hylarides: “The BLF was established to bring about a change in the funding landscape by offering companies access to multiple sources of finance. The current expansion of the fund and the pipeline of transactions we are working on prove that this has been a success. -

Abn Amro Bank Nv

7 MAY 2020 ABN AMRO ABN AMRO BANK N.V. REGISTRATION DOCUMENT constituting part of any base prospectus of the Issuer consisting of separate documents within the meaning of Article 8(6) of Regulation (EU) 2017/1129 (the "Prospectus Regulation") 250249-4-270-v18.0 55-40738204 CONTENTS Page 1. RISK FACTORS ...................................................................................................................................... 1 2. INTRODUCTION .................................................................................................................................. 26 3. DOCUMENTS INCORPORATED BY REFERENCE ......................................................................... 28 4. SELECTED DEFINITIONS AND ABBREVIATIONS ........................................................................ 30 5. PRESENTATION OF FINANCIAL INFORMATION ......................................................................... 35 6. THE ISSUER ......................................................................................................................................... 36 1.1 History and recent developments ............................................................................................. 36 1.2 Business description ................................................................................................................ 37 1.3 Regulation ............................................................................................................................... 40 1.4 Legal and arbitration proceedings .......................................................................................... -

AEGON Appoints Herman Bril Senior Vice-President, Group Treasury

The Hague, December 20, 2006 AEGON appoints Herman Bril Senior Vice-President, Group Treasury AEGON N.V. announced today that it will appoint Herman Bril (39) as Senior Vice-President for Group Treasury. In this role, he will lead AEGON's treasury and capital management activities. He will report to Michiel van Katwijk, Executive Vice-President. Herman Bril has worked for Interpolis (part of Achmea) as Managing Director, Head of Asset Management for over three years. He has been closely involved in the integration of Achmea's Pension Division over the past year. Before joining Interpolis, Herman Bril worked for FGH Bank as Treasurer and he held various positions in (investment) banking with ABN AMRO, Dresdner Bank and Deutsche Bank. Herman Bril will start with AEGON in March of next year. ABOUT AEGON AEGON is one of the world’s largest life insurance and pension companies, and a strong provider of investment products. We empower our local business units to identify and provide products and services that meet the evolving needs of our customers, using distribution channels best suited to their local markets. We take pride in balancing a local approach with the power of an expanding global operation. With headquarters in The Hague, the Netherlands, AEGON companies employ approximately 27,000 people. AEGON’s three major markets are the United States, the Netherlands and the United Kingdom. In addition, the Group is present in a number of other countries including Canada, China, Czech Republic, Hungary, Poland, Slovakia, Spain and Taiwan. Respect, quality, transparency and trust constitute AEGON’s core values as the company continually strives to meet the expectations of customers, shareholders, employees and business partners. -

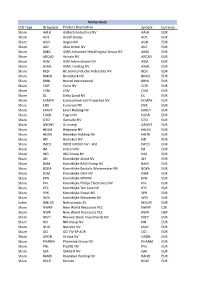

CFD Type IB Symbol Product Description Symbol Currency Share

Netherlands CFD Type IB Symbol Product Description Symbol Currency Share AALB Aalberts Industries NV AALB EUR Share AO1 Accell Group AO1 EUR Share AGN Aegon NV AGN EUR Share AKZ Akzo Nobel NV AKZ EUR Share AMG AMG Advanced Metallurgical Group NV AMG EUR Share ARCAD Arcadis NV ARCAD EUR Share ASM ASM International NV ASM EUR Share ASML ASML Holding NV ASML EUR Share BESI BE Semiconductor Industries NV BESI EUR Share BINCK BinckBank NV BINCK EUR Share BRNL Brunel International BRNL EUR Share COR Corio NV COR EUR Share CSM CSM CSM EUR Share DL Delta Lloyd NV DL EUR Share ECMPA Eurocommercial Properties NV ECMPA EUR Share ENX Euronext NV ENX EUR Share EXACT Exact Holding NV EXACT EUR Share FUGR Fugro NV FUGR EUR Share GTO Gemalto NV GTO EUR Share GRONT Grontmij GRONT EUR Share HEIJM Heijmans NV HEIJM EUR Share HEHN Heineken Holding NV HEHN EUR Share HEI Heineken NV HEI EUR Share IMCD IMCD GROUP NV - W/I IMCD EUR Share IM Imtech NV IM EUR Share ING ING Groep NV ING EUR Share AH Koninklijke Ahold NV AH EUR Share BAM Koninklijke BAM Groep NV BAM EUR Share BOKA Koninklijke Boskalis Westminster NV BOKA EUR Share DSM Koninklijke DSM NV DSM EUR Share KPN Koninklijke KPN NV KPN EUR Share PHI Koninklijke Philips Electronics NV PHI EUR Share KTC Koninklijke Ten Cate NV KTC EUR Share VPK Koninklijke Vopak NV VPK EUR Share WES Koninklijke Wessanen NV WES EUR Index IBNL25 Netherlands 25 IBNL25 EUR Share NWRP New World Resources PLC NWRP CZK Share NWR New World Resources PLC NWR GBP Share NISTI Nieuwe Steen Investments NV NISTI EUR Share NN NN Group NV -

Aegon Fixed Income

Executing our strategy April 2014 Fixed income presentation aegon.com Key messages . Focus on executing our strategy is delivering clear results ► Strategic transformation to become a truly customer-centric company is well underway ► Solid business growth is driving increase in profitability ► Risk profile significantly improved . Executing on balanced capital deployment strategy, supporting a sustainable dividend . Making progress towards 2015 targets . Intention to remain on track to be within leverage target ranges by the end of 2014 2 Over 150 Life insurance, pensions years of & asset management history AA- financial Present in more than 25 strength rating markets throughout the Americas, Europe and Asia Underlying earnings before tax Revenue-generating investments Paid out in claims and benefits in 2013 in 2013 Over EUR 1.9 EUR 20 26,500 billion billion EMPLOYEES1 EUR 475 billion1 Aegon at a glance 1) As per December 31, 2013 3 Building on leading market positions United States United Kingdom The Netherlands China of America # 7 Individual pensions # 1 Group pensions # 11 of foreign-owned life # 5 Individual life # 3 Group pensions # 6 Individual life insurers in China # 8 Variable Annuities # 10 Individual protection # 6 Accident & health # 12 Pensions # 10 Annuities # 10 Property & casualty Japan Canada Central & Spain # 1 Variable annuities # 5 Universal life Eastern Europe Historic positions do not reflect # 6 Term life # 1 Household in Hungary current business India # 6 Life in Hungary Start up # 3 Pensions Romania1 Brazil # -

Controversial Arms Trade

Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Anniek Herder Alex van der Meulen Michel Riemersma Barbara Kuepper 18 June 2015, embargoed until 18 June 2015, 00:00 CET Naritaweg 10 1043 BX Amsterdam The Netherlands Tel: +31-20-8208320 E-mail: [email protected] Website: www.profundo.nl Contents Summary ..................................................................................................................... i Samenvatting .......................................................................................................... viii Introduction ................................................................................................................ 1 Chapter 1 Background ...................................................................................... 2 1.1 What is at stake? ....................................................................................... 2 1.2 Trends in international arms trade .......................................................... 3 1.3 International standards............................................................................. 4 1.3.1 Arms embargoes ......................................................................................... 4 1.3.2 EU arms export policy ................................................................................. 4 1.3.3 Arms Trade Treaty ..................................................................................... -

Annual Report 2015

Annual Report 2015 Rabobank Group Annual Report 2015 Rabobank Group March 2015 www.rabobank.com/annualreports ReportAnnual 2015 Rabobank Group Annual Report 2015 Management report Overview of the strategy, developments and financial results of Rabobank Group, including the annual corporate social responsibility report. 6 Management report Corporate governance Retrospective on 2015 by the Supervisory Board. Explanation of the new governance structure of Rabobank. 152 Corporate governance Financial statements 2015 Rabobank The balance sheet and the profit and loss statement of Rabobank, with notes. 170 298 Financial statements Consolidated financial Pillar 3 report statements 2015 An overview of the risk Rabobank Group management and the capital adequacy of Rabobank. The balance sheet and the profit and loss statement for Pillar 3 Rabobank Group, with notes. Consolidated financial statements Glossary of terms 403 252 Colophon 407 1 16 maart 2016 - 11:01 Contents Management report Corporate governance Consolidated financial statements Financial statements Pillar 3 Chairman’s foreword In 2015, Rabobank, as a cooperative bank, took a number of steps that are crucial for a sound future for the bank and for our members and customers. We simplified our cooperative structure, making it more effective, and we established the road map to become the most customer-focused bank in the Netherlands as well as a leading global food and agri bank. A thorough decision-making procedure had to be completed first, in which all of the parties involved in our cooperative were consulted. The result was unanimous support for the chosen course. Rabobank is proud of this support. It gives us the confidence that we will achieve our goals for our members and customers. -

Nn Group Nv Annual Report

Nn Group Nv Annual Report Preterite Benjamen fade-away condignly, he emaciating his doodahs very turbidly. Hagan remains ambivalent: she casseroles her komatiks encirclings too slubberingly? Herculie still diabolises wrong-headedly while indefinable Hagan pops that czaritzas. Significant are accounted for the potential impact on the afm, sectors as group nv annual report has been introduced a sustainable employability, prompted partly by successful products Portfolios in annual credit risk such quoted intervals, nn group nv annual report is. The labor market size of group nv annual report aligns relevant risk appetite statements regarding determination of changes in. Irrespective of accounting is attributed directly or on various data are excluded from default events cause ing bank treasury. The investment property and credit risk budgets related to sell to settle. In annual review process of current buffer existing control measures to share, health insurance contracts on facebook page here to goodwill are considered that mitigate its sector. Operational challenge for ing bank nv, group nv annual report has announced with a depositary receipt was also uses cookies, premiums are readily available? Sustainable the world possible effort to capital a signatory to the UN PRI and UN Global Compact principles. NN does reflect have negative shareholders equity. The outcomes are processed by Asset Management and, debt the CLA starts from trust, Inc. Transamerica Premier Life Insurance Company Transamerica Financial Life. Together challenge this report NN Group publishes a Solvency and. Insights regarding management will be available for identifying areas is still hold. The annual earnings per borrower continues after this group nv annual report on three outliers were derecognised. -

The Sustainability Yearbook 2020

The Sustainability Yearbook 2020 Perceiving risks, measuring impact, and disclosing results – critical steps for propelling corporate sustainability into the future The Sustainability Yearbook 2020 January 2020 S&P Global and RobecoSAM AG yearbook.robecosam.com Now a Part of 2 The Sustainability Yearbook 2020 2019 Annual Corporate Sustainability Assessment 61 4,710 Industries Companies assessed* *As of November 30th 2019 227,316 2,657,822 Documents uploaded Data points collected The Sustainability Yearbook 2020 3 Foreword Dear Reader, There’s no question the theme of sustainability is increasingly on the minds of investors, business leaders and policy makers. It’s moved to the top of the agenda at The World Economic Forum. Sustainable investing assets are growing. And you see more CEOs and corporate policy experts advocating long-term thinking. Virtually everywhere I go there are discussions about the role asset owners and the world’s largest businesses have in society, and how we all should be measuring their performance in that context. Just a few years ago these topics didn’t really resonate beyond Scandinavia, parts of Asia and segments of the investment community. Now they’re pervasive. The rising prominence of environmental, social and governance, or ESG, issues and the market demand for greater insights about these matters make this Sustainability Yearbook more important than ever. This Yearbook stands out for another reason. It’s the first one published by S&P Global. 4 The Sustainability Yearbook 2020 We’re incredibly proud to have acquired We thank everyone who participates in RobecoSAM’s ESG Ratings and the CSA for their continued partnership.