Case M.8096 - INTERNATIONAL PAPER COMPANY / WEYERHAEUSER TARGET BUSINESS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Supply Chain

COMPANY OVERVIEW 2015 MAKING PRODUCTS PEOPLE DEPEND ON EVERY DAY PERFORMANCE PEOPLE PLANET International Paper is a global leader in packaging, paper, and pulp. We use renewable resources responsibly to make recyclable products that people depend on every day. We are unified around shared commitments to strengthen our people and communities, provide solutions for our customers, and ensure the sustainability of our company and our planet. Our fiber sourcing policies promote healthy and productive forests for generations to come In 2015, 93% of our facilities operated without a serious injury $15.5 million donated to address critical community needs and improve MAKING our planet PRODUCTS PEOPLE DEPEND ON CONTENTS EVERY DAY 2 2015 Highlights 3 CEO Comments 4 Businesses 6 Performance 12 People $22.4 billion 20 Planet net sales in 2015 28 Awards & Recognitions 29 Vision 2020 Goals International Paper Company Overview 2015 2 65% 13% 22% REVENUE Industrial Consumer Paper 2015 GLOBAL HIGHLIGHTS Packaging Packaging and Pulp We use renewable resources responsibly to make recyclable products people depend on every day. BY BUSINESS $2.6 billion net sales Manufacturing operations in 24 countries EMEA*/ Russia North Asia ** America $1.3 billion net sales Global 55,000 India $17.2 billion Headquarters: employees globally net sales Memphis, Tenn. $0.2 billion Latin net sales America 44,000 $1.1 billion volunteer hours net sales *Europe, Middle East, Africa worked by employees **Includes the net sales of the International Paper Sun joint venture through -

INTERNATIONAL PAPER COMPANY (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 _____________________________________________________ FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the fiscal year ended December 31, 2012 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File No. 1-3157 INTERNATIONAL PAPER COMPANY (Exact name of registrant as specified in its charter) New York 13-0872805 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 6400 Poplar Avenue Memphis, Tennessee (Address of principal executive offices) 38197 (Zip Code) Registrant’s telephone number, including area code: (901) 419-7000 _____________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Stock, $1 per share par value New York Stock Exchange _____________________________________________________ Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

4Th Quarter 2013

February - 2014 4th Quarter 2013 Inside the Issue A Letter From Our Chairman Peter Masias ● A Letter from the Corporate Director of Safety & Risk Management Conference Green Bay Packaging Chairman - 2 ● 2014 Safety What a Great Year PPSA Members! and Health Conference - 3 With the New Year in full swing, we wanted to provide you with the most ● 2014 Conference up-to-date safety information. Inside this quarterly report, you will find the End of Year Speakers - 4 Injury and Illness Statistics reports. If you have questions regarding the reports, please let ● OSHA Newsletter - 7 us know. ● For the Life of a Friend - 8 PPSA is currently in the middle of planning our 71st Annual Conference in St. Petersburg, ● Red Wing Shoe Florida at the Viony Resort June 22-25 (www.ppsa.org/14conference.) This year the Recall - 10 conference theme is The Flaming Cs of Safety. Attendees can expect some HOT topics ● Safety Flash Near Miss to include individual commitment and the importance of developing a caring culture, new - 11 control methods celebrating safety innovations, and life changing injuries and how to focus ● GHS Update - 14 on the high risk areas. ● Executive Eagle Award Information - 16 In addition to our upcoming conference, PPSA is pleased to welcome three new board members - Hazel A. Ladner, Regional Safety and Health Manager for North America at ● Executive Eagle Award MeadWestVaco, Steve Gearheart, Safety Director at Hartford City Paper, and Eric Barnes, Nomination Form - 17 Regional EHS Manager for International Paper. Be sure to welcome Hazel, Steve and Eric ● Safety Innovator Award at the June Safety and Health Conference. -

Ref. 676.03 SMO 2Nd

INDEX Refer to Chapter Refer to Chapter Refer to Chapter A test 14 acid pretreatment 10 acetate 4 acidproof brick 8 abaca 3 acetate laminating 18 acid pulping 8 abatement 20 acetate pulp 4 acid rain 21 odor 21 acetic acid 4 acid-refined tall oil 6 pollution 20 acetic anhydride 4 acid-resistant 14 abatement device 21 acetone 4 acid size 5 abietic acid 6 acetylated starch 5 acid-stable size 5 abrasion 24 acetyl radical 4 acid sulfite process 8 abrasion debarker I acetylating agent 4 acid tower 8 abrasion resistance 14 acid(s) 4, 8 acid treatment 10 abrasion test 14 abietic 6 acidulating 4 abrasive 7 acetic 4 acidulating agent 4 abrasive backing papers 16 accumulator 8 acidulation 6 abrasiveness 14 carbonic 20 acoustical board 16 abrasive segment 7 Caro's 10 acoustical testing 14 abrasivity (of mineral fillers) 13 cooking 8 acoustic leak detector 9 absorbency 11,14 digester 8 acre-foot 20 relative II fatty 6 acrylamide resins 5 water II formamidine sulfinic 10 acrylic binders 17 absorbent 14,24 formic 4 acrylic fiber 3 absorbent capacity II glucuronic 4 activatable chemical 9 absorbent grades 16 humic 20 activated carbon 20 absorption 5 hydroxy 4 activated sludge 20 capillary 13 hypochlorous 10 activated sludge loading 20 ink 14 lignosulfonic 8 activated sludge process 20 light 14 linoleic 6 activation 4 mechanical 13 mineral 4 surface II tensile energy 14 oleic 6 activation energy 8 vapor 13 pectic 4 Arrhenius 4 absorption coefficient 14 peracetic 10 activator 5 accelerated aging 14 raw 8 active alkali 8 accelerated aging test 14 resin -

Terminology on Paper & Pulp: Types of Paper and Containerboard, Containerboard Grades and Tests

Terminology On Paper & Pulp: Types of Paper and Containerboard, Containerboard Grades and Tests Prepared for the Meeting of the Paper & Pulp Industry Project By Aselia Urmanbetova Date: September 10, 2001 1 Paper Products Chart: Containerboard Tree/Waste Paper Pulp Paper Paperboard Brown Coated Uncoated (container- board) Brown (65% White (95%- Copying Paper Newsprint hardwood and 100% 35% softwood) softwood) White Tissue (paperboard package) SBS (Solid Boxboard Bleach Sulfate) Coated Uncoated 2 Examples of Containerboard Grades/Mead Corporation: (Refer to the Glossary for the Explanation of the Terms) Standard Grades Grade Basis Weight Moisture Ring Crush Concora 26 SC 26.0 9.0 N/A 63 30 SC 30.0 9.0 50 68 33 SC 33.0 9.0 60 72 36 SC 36.0 9.0 71 79 40 SC 40.0 9.0 82 79 45 SC 45.0 9.0 102 95 Light Weights Grade Basis Weight Moisture Porosity Concora STFI 18 SC 18.0 7.5 30 33 9.5 20 SC 20.0 7.5 30 35 10.5 23 SC 23.0 9.0 30 59 12.0 Polar Chem Grade Basis Weight Moisture Ring Crush Concora Wet Mullen 30 PC 30.0 9.0 50 68 4.0 33 PC 33.0 9.0 60 72 4.0 36 PC 36.0 9.0 71 79 4.0 40 PC 40.0 9.0 82 79 4.0 45 PC 45.0 9.0 102 95 4.0 3 Paper Products and Containerboard Glossary B Flute A flute that is approximately 0.097 inches high. -

MERCER COUNTY IMPROVEMENT AUTHORITY SOLID WASTE and RECYCLING QUANTIFICATION and CHARACTERIZATION STUDY

REPORT FOR MERCER COUNTY IMPROVEMENT AUTHORITY SOLID WASTE and RECYCLING QUANTIFICATION and CHARACTERIZATION STUDY PREPARED BY T&M ASSOCIATES 1256 NORTH CHURCH STREET, MOORESTOWN, NJ 08057 856.722.6700 | TANDMASSOCIATES.COM September 2015 TABLE OF CONTENTS EXECUTIVE SUMMARY ............................................................................................................................ 1 INTRODUCTION ........................................................................................................................................ 2 BACKGROUND ............................................................................................................................................. 2 MERCER COUNTY RECYCLING PROGRAM | SOLID WASTE MANAGEMENT PLAN ........................................ 2 METHODOLOGY ....................................................................................................................................... 4 GENERAL ..................................................................................................................................................... 4 BASIS OF STUDY | ASTM D5231 ................................................................................................................. 4 T&M PERSONNEL AND TRAINING ................................................................................................................ 5 SAMPLING PROCEDURES ............................................................................................................................ 6 SORTING -

Sanitary Products

About Nordic Swan Ecolabelled Sanitary Products Version 6.8 Background to ecolabelling 04 May 2021 Content 1 Summary 3 2 Basic facts about the criteria 5 2.1 Sanitary products that may carry the Nordic Swan Ecolabel 5 2.2 Justification for Nordic Ecolabelling 6 3 About the criteria revision 7 3.1 Earlier versions of the criteria 8 3.2 Nordic Swan Ecolabel licences in the Nordic Market 8 4 The Nordic market 9 5 Other labels 10 6 Environmental assessment of sanitary products 12 6.1 Disposable products 12 6.2 Material composition 15 6.3 Environmental conditions for the materials 20 6.4 Renewable versus fossil-based materials 24 6.5 Relevance, Potential and Steerability 25 7 Justification of the requirements 27 7.1 Product group definition 27 7.2 Environmental requirements in general 30 7.3 Description of the product 35 7.4 Requirements for chemical products and chemical substances 36 7.5 Requirements concerning materials in the product and packaging 49 7.6 Product performance 92 7.7 Quality and regulatory requirements 94 8 Changes compared to previous version 95 9 Terms and definitions 97 Appendix 1 Requirement for regenerated cellulose Appendix 2 Guidelines for standard, renewable comoditives 023 Sanitary Products, version 6.8, 04 May 2021 This document is a translation of an original in Norwegian. In case of dispute, the original document should be taken as authoritative. Addresses In 1989, the Nordic Council of Ministers decided to introduce a voluntary official ecolabel, the Nordic Swan Ecolabel. These organisations/companies operate the Nordic ecolabelling system on behalf of their own country’s government. -

International Paper Equity Earnings and Dividends Received by International Paper, Have Been Prepared by the Management of Ilim

Investor Roadshow | February 23, 2017 Forward-Looking Statements Certain statements in these slides and made during this presentation may be considered forward-looking statements. These statements reflect management's current views and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied in these statements. Factors which could cause actual results to differ include but are not limited to: (i) the level of our indebtedness and changes in interest rates; (ii) industry conditions, including but not limited to changes in the cost or availability of raw materials, energy and transportation costs, competition we face, cyclicality and changes in consumer preferences, demand and pricing for our products; (iii) global economic conditions and political changes, including but not limited to the impairment of financial institutions, changes in currency exchange rates, credit ratings issued by recognized credit rating organizations, the amount of our future pension funding obligation, changes in tax laws and pension and health care costs; (iv) unanticipated expenditures related to the cost of compliance with existing and new environmental and other governmental regulations and to actual or potential litigation; (v) changes in our estimates for the costs and insurance coverage associated with the recent incident at our Pensacola, Florida mill and for the time required to resume full operations at the mill; (vi) whether we experience a material disruption at one of our other manufacturing facilities; (vii) risks inherent in conducting business through joint ventures; (viii) the failure to realize the expected synergies and cost-savings from our purchase of the cellulose fibers business of Weyerhaeuser Company; and (ix) our ability to achieve the benefits we expect from all other strategic acquisitions, divestitures and restructurings. -

22) General Principles of Food Packaging: Packaging Materials 1

22) GENERAL PRINCIPLES OF FOOD PACKAGING: PACKAGING MATERIALS 1. Glass Pliny the Elder recorded that Phoenician sailors came ashore and, not finding any local materials suitable for supporting their cooking pots above the sandy shore, used lumps of trona (natural soda or sodium carbonate) that formed part of their ship’s cargo. As the trona was heated in the fire it combined with the sand to give a material that flowed. This story may not be entirely accurate but points to the fact that glass as a man-made material has a long history and some of the oldest dated Middle Eastern pieces are over 4000 years old; a deep blue charm is estimated to date from 7000 BC. Egyptians and Romans fashioned a wide range of intricate and colored glass objects. A highly developed industry existed in Syria in 1500 BC. In medieval times the centre of the glass blowing expertise was Venice (1200-1600 AD). The serendipitous preparation of glass by the Phoenician sailors is basically the same as that used today. A mixture of purified sand is heated with sodium and calcium carbonate together with some sodium sulphate. The gases evolved help to stir the mixture. The addition of calcium is necessary to make the glass insoluble in water - simple sodium glass is water soluble to give a very viscous liquid known as water-glass (used as an egg preservative in WW2). For those who like the chemistry: Na2CO3 + SiO2 -> Na2SiO3 + CO2 CaCO3 + SiO2 -> CaSiO3 + CO2 Na2SO4 + SiO2 -> Na2SiO3 + SO3 Glass made as above is known as soda-glass. -

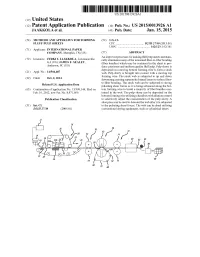

(12) Patent Application Publication (10) Pub. No.: US 2015/0013926 A1 JAAKKOLA Et Al

US 2015 0013926A1 (19) United States (12) Patent Application Publication (10) Pub. No.: US 2015/0013926 A1 JAAKKOLA et al. (43) Pub. Date: Jan. 15, 2015 (54) METHODS AND APPARATUS FOR FORMING (52) U.S. Cl. FLUFF PULP SHEETS CPC ..................................... D2IH 27/30 (2013.01) USPC ........................................... 162/123; 162/141 (71) Applicant: INTERNATIONAL PAPER COMPANY, Memphis, TN (US) (57) ABSTRACT An improved processes for making fluff pulp sheets mechani (72) Inventors: JYRKI T. JAAKKOLA, Lawrenceville, cally eliminates many of the unwanted fiber-to-fiber bonding GA (US); JAMES E. SEALEY, (fiber bundles) which may be contained in the sheet to pro Anderson, SC (US) duce consistent and uniform quality fluff pulp. Pulp slurry is deposited on a moving bottom forming wire to form a stock (21) Appl. No.: 14/504,487 web. Pulp slurry is brought into contact with a moving top 1-1. forming wire. The stock web is subjected to up and down (22) Filed: Oct. 2, 2014 dewatering creating separately formed layers to reduce fiber O O to-fiber bonding. The stock web can be subjected to strong Related U.S. Application Data pulsating shear forces as it is being advanced along the bot (63) Continuation of application No. 13/398,144, filed on tom forming wire to break a majority of fiber bundles con Feb. 16, 2012, now Pat. No. 8,871,059. tained in the web. The pulp slurry can be deposited on the bottom forming wire utilizing aheadbox with dilution control Publication Classification to selectively adjust the concentration of the pulp slurry. A shoe press can be used to dewater the web after it is subjected (51) Int. -

Sunday, October 27, 2019

PROGRAM TRACKS Engineering, Reliability, Energy, Recovery, Lime Career Development Environmental Corrosion & Materials Kiln and Recaust Nonwood Pulping & Bleaching Recycling Forum Sustainability IBBC Conference PROGRAM AS OF 05/11/19 ( SUBJECT TO CHANGE) Sunday, October 27, 2019 7:30AM – 4:00PM Bleach Plant Operations Workshop** 8:00AM – 4:00PM Brown Stock Washing Workshop** 8:00AM – 4:00PM Project Management Workshop** 12:00PM – 1:00PM Joint Team Review of Conference Logistics* 1:00PM - 4:30PM Engineering Division & Pulp Manufacture Division Councils* 4:00PM - 5:00PM Nonwood Fiber Committee Meeting 4:00PM - 5:00PM Alkaline Pulping & Bleaching Committee Meeting 5:00PM – 7:00PM Welcome Reception & Exhibit 7:00PM -9:30PM Awards Dinner* * Invitation Only ** Additional registration fee required *** Pre-registration required Monday, October 28, 2019 7:00AM – 8:15AM Speaker Breakfast 7:30AM-8:30AM Women in Industry Breakfast 8:30AM – 10:00AM Session 1: Opening Session & Keynote Session Chair: Carl Houtman, USDA Forest Products Laboratory Keynote: Angie Slaughter, Vice President Sustainability, Anheuser - Busch 10:00AM – 10:30AM Break & Exhibit Open 10:30AM – 12:00PM Session 2: State of the Industry Session Chair: AF&PA Sustainability Update - Jerry Schwartz, American Forest & Paper Association 10:30AM – 12:00PM Session 3: Pulping Optimization Session Chair: Pulp Suspension Density Evaluation for Improved Production Calculation at the Discharge of a Continuous Digester - Bruno Goncalves, Lwarcel Celulose Technical and Economic Modelling of -

Conocophillips 2021 Proxy Statement

A Message from Our Chairman and Chief Executive Officer and Lead Director MARCH 29, 2021 Dear Fellow Stockholders, S SAFETY On behalf of the Board of Directors (the “Board”) and the Executive Leadership Team, we are pleased to No task is so important that invite you to participate in the 2021 Annual Meeting of Stockholders (the “Annual Meeting”). We planned we can’t take the time to do to return to an in-person meeting this year; however, the health and well-being of our employees, it safely. A safe company is a stockholders and partners remain of the utmost importance to us, and due to the ongoing coronavirus successful company. (COVID-19) pandemic and to be consistent with our SPIRIT Values and public health guidelines, this year’s Annual Meeting will be virtual only. This does not represent a change in our stockholder engagement philosophy and we remain committed to an in-person meeting in 2022. P PEOPLE We respect one another. We The Annual Meeting will be held on Tuesday, May 11, 2021, at 9:00 a.m. Central Daylight Time. It will be recognize that our success conducted via live webcast. You will be able to participate online at www.virtualshareholdermeeting.com/ depends upon the capabilities COP2021. You may submit questions electronically both before and during the meeting or by using a live and inclusion of our employees. phone line during the meeting, and you will also be able to vote your shares electronically (other than We value different voices and shares held through our employee benefit plans, which must be voted prior to the meeting).