Dairy Value Chain in West Amhara (Bahir Dar Zuria and Fogera Woreda Case)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Districts of Ethiopia

Region District or Woredas Zone Remarks Afar Region Argobba Special Woreda -- Independent district/woredas Afar Region Afambo Zone 1 (Awsi Rasu) Afar Region Asayita Zone 1 (Awsi Rasu) Afar Region Chifra Zone 1 (Awsi Rasu) Afar Region Dubti Zone 1 (Awsi Rasu) Afar Region Elidar Zone 1 (Awsi Rasu) Afar Region Kori Zone 1 (Awsi Rasu) Afar Region Mille Zone 1 (Awsi Rasu) Afar Region Abala Zone 2 (Kilbet Rasu) Afar Region Afdera Zone 2 (Kilbet Rasu) Afar Region Berhale Zone 2 (Kilbet Rasu) Afar Region Dallol Zone 2 (Kilbet Rasu) Afar Region Erebti Zone 2 (Kilbet Rasu) Afar Region Koneba Zone 2 (Kilbet Rasu) Afar Region Megale Zone 2 (Kilbet Rasu) Afar Region Amibara Zone 3 (Gabi Rasu) Afar Region Awash Fentale Zone 3 (Gabi Rasu) Afar Region Bure Mudaytu Zone 3 (Gabi Rasu) Afar Region Dulecha Zone 3 (Gabi Rasu) Afar Region Gewane Zone 3 (Gabi Rasu) Afar Region Aura Zone 4 (Fantena Rasu) Afar Region Ewa Zone 4 (Fantena Rasu) Afar Region Gulina Zone 4 (Fantena Rasu) Afar Region Teru Zone 4 (Fantena Rasu) Afar Region Yalo Zone 4 (Fantena Rasu) Afar Region Dalifage (formerly known as Artuma) Zone 5 (Hari Rasu) Afar Region Dewe Zone 5 (Hari Rasu) Afar Region Hadele Ele (formerly known as Fursi) Zone 5 (Hari Rasu) Afar Region Simurobi Gele'alo Zone 5 (Hari Rasu) Afar Region Telalak Zone 5 (Hari Rasu) Amhara Region Achefer -- Defunct district/woredas Amhara Region Angolalla Terana Asagirt -- Defunct district/woredas Amhara Region Artuma Fursina Jile -- Defunct district/woredas Amhara Region Banja -- Defunct district/woredas Amhara Region Belessa -- -

Feasibility Study for a Lake Tana Biosphere Reserve, Ethiopia

Friedrich zur Heide Feasibility Study for a Lake Tana Biosphere Reserve, Ethiopia BfN-Skripten 317 2012 Feasibility Study for a Lake Tana Biosphere Reserve, Ethiopia Friedrich zur Heide Cover pictures: Tributary of the Blue Nile River near the Nile falls (top left); fisher in his traditional Papyrus boat (Tanqua) at the southwestern papyrus belt of Lake Tana (top centre); flooded shores of Deq Island (top right); wild coffee on Zege Peninsula (bottom left); field with Guizotia scabra in the Chimba wetland (bottom centre) and Nymphaea nouchali var. caerulea (bottom right) (F. zur Heide). Author’s address: Friedrich zur Heide Michael Succow Foundation Ellernholzstrasse 1/3 D-17489 Greifswald, Germany Phone: +49 3834 83 542-15 Fax: +49 3834 83 542-22 Email: [email protected] Co-authors/support: Dr. Lutz Fähser Michael Succow Foundation Renée Moreaux Institute of Botany and Landscape Ecology, University of Greifswald Christian Sefrin Department of Geography, University of Bonn Maxi Springsguth Institute of Botany and Landscape Ecology, University of Greifswald Fanny Mundt Institute of Botany and Landscape Ecology, University of Greifswald Scientific Supervisor: Prof. Dr. Michael Succow Michael Succow Foundation Email: [email protected] Technical Supervisor at BfN: Florian Carius Division I 2.3 “International Nature Conservation” Email: [email protected] The study was conducted by the Michael Succow Foundation (MSF) in cooperation with the Amhara National Regional State Bureau of Culture, Tourism and Parks Development (BoCTPD) and supported by the German Federal Agency for Nature Conservation (BfN) with funds from the Environmental Research Plan (FKZ: 3510 82 3900) of the German Federal Ministry for the Environment, Nature Conservation and Nuclear Safety (BMU). -

(IJVHSR) ISSN 2332-2748 a Survey on the Prevalence of Bovine T

OPEN ACCESS https://scidoc.org/IJVHSR.php International Journal of Veterinary Health Science & Research (IJVHSR) ISSN 2332-2748 A Survey on the Prevalence of Bovine Trypanosomosis in Bahir Dar Zuria and Bure Woreda, Amhara Regional State, Ethiopia Research Article Shemsia M* Bahir Dar Animal Health Diagnostic and Investigation Laboratory, Bahir Dar, Ethiopia. Abstract A study was conducted from November 2007 to April 2008 in Bahir Dar zuria woreda of tsetse free and Bure woreda of tsetse infested area of Amhara region of Northwest Ethiopia to investigate the prevalence of trypanosomosis in cattle. In each study area randomly selected cattle were sampled and their blood investigated using parasitological methods. The diagnostic techniques used include PCV (packed cell volume) to measure the degree of anaemia, heamatocrit centrifugation techniques (buffy coat examination) and thin smear. A total of 600 cattle (300 from Bahir Dar zuria woreda and 300 from Bure woreda) were sampled. Among them 80 cattle 45 (15%) in Bure woreda and 35 (11.66%) in Bahir Dar zuria were positive for trypano- some infection. The species of trypanosome infected during the study were Trypanosoma vivax (64%) and Trypanosoma congolense (36%) in Bure woreda but only Trypanosoma vivax (100%) were found in Bahir Dar zuria woreda. No significance difference in susceptibility was seen between male and female but significant differences in infection rate were observed between ages. Trypanosome infections were mainly due to Trypanosoma vivax and the significantly reduced the average packed cell volume and the body condition of the animals. The study revealed that trypanosomosis in cattle is an important disease in Amhara region of Northwest Ethiopia. -

Impact of Khat Production on Household Welfare in Amhara Region of Ethiopia

Impact of khat production on household welfare in Amhara region of Ethiopia by Hanna Lynn Ruder B.S., Kansas State University, 2016 A THESIS submitted in partial fulfillment of the requirements for the degree MASTER OF SCIENCE Department of Agricultural Economics College of Agriculture KANSAS STATE UNIVERSITY Manhattan, Kansas 2018 Approved by: Major Professor Dr. Benjamin Schwab Copyright © Hanna Ruder 2018. Abstract Khat, a lucrative cash crop cultivated in and near the Horn of Africa, is gaining the interest of researchers around the globe. Despite its potential to provide excess income, economic opportunity, and access to technology to those who produce it, the conflicting legal status around the globe causes policy and trade disputes between countries. Research on the impact of khat production on household welfare is sparse. To address this, the purpose of this research is to determine what factors affect the decision to grow khat and subsequently determine the impact of khat production on labor, income, education expenditure, and food security. Data was extracted from a survey conducted in early 2017. A total of 365 households in the Amhara Region of Ethiopia were surveyed. We estimate the factors affecting the decision to grow khat by employing use of two logit models and one linear probability model to calculate marginal effects. We estimate the impact of khat production on labor, income, education expenditure, and food security through propensity score matching. Khat production appears to be adopted by households who are educated and apt to adopt improved technologies. These households are likely to own a donkey, own irrigation, and own more plots than a non-producing household. -

The Political Economy of Agricultural Investment in Amhara National Regional State (Anrs): a Focus on Flower Farms in Bahir Dar Zuria Woreda

DSpace Institution DSpace Repository http://dspace.org Political Science Thesis and Dissertations 2018-07-17 THE POLITICAL ECONOMY OF AGRICULTURAL INVESTMENT IN AMHARA NATIONAL REGIONAL STATE (ANRS): A FOCUS ON FLOWER FARMS IN BAHIR DAR ZURIA WOREDA ASABU, SEWNET http://hdl.handle.net/123456789/8869 Downloaded from DSpace Repository, DSpace Institution's institutional repository BAHIR DAR UNIVERSITY FACULTY OF SOCIAL SCIENCE DEPARTMENT OF POLITICAL SCIENCE AND INTERNATIONAL STUDIES THE POLITICAL ECONOMY OF AGRICULTURAL INVESTMENT IN AMHARA NATIONAL REGIONAL STATE (ANRS): A FOCUS ON FLOWER FARMS IN BAHIR DAR ZURIA WOREDA BY ASABU SEWNET JUNE, 2018 BAHIR DAR, ETHIOPIA BAHIR DAR UNIVERSITY FACULTY OF SOCIAL SCIENCES DEPARTMENT OF POLITICAL SCIENCE AND INTERNATIONAL STUDIES THE POLITICAL ECONOMY OF AGRICULTURAL INVESTMENT IN ANRS: A FOCUS ON FLOWER FARMS IN BAHIR DAR ZURIA WOREDA A THESIS SUBMITTED TO THE DEPARTMENT OF POLITICAL SCIENCE AND INTERNATIONAL STUDIES IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ARTS IN POLITICAL SCIENCE BY ASABU SEWNET ADVISOR BELACHEW G.(PhD) JUNE 2018 BAHIR DAR, ETHIOPIA © 2018 Asabu Sewnet BAHIR DAR UNIVERSITY FACULTY OF SOCIAL SCIENCES DEPARTMENT OF POLITICAL SCIENCE AND INTERNATIONAL STUDIES THE POLITICAL ECONOMY OF AGRICULTURAL INVESTMENT IN ANRS: A FOCUS ON FLOWER FARMS IN BAHIR DAR ZURIA WOREDA BY ASABU SEWNET Approved by board of examiners: _____________________________________ _____________________________ Advisor’s Signature _____________________________________ ____________________________ -

Modeling Malaria Cases Associated with Environmental Risk Factors in Ethiopia Using Geographically Weighted Regression

MODELING MALARIA CASES ASSOCIATED WITH ENVIRONMENTAL RISK FACTORS IN ETHIOPIA USING GEOGRAPHICALLY WEIGHTED REGRESSION Berhanu Berga Dadi i MODELING MALARIA CASES ASSOCIATED WITH ENVIRONMENTAL RISK FACTORS IN ETHIOPIA USING THE GEOGRAPHICALLY WEIGHTED REGRESSION MODEL, 2015-2016 Dissertation supervised by Dr.Jorge Mateu Mahiques,PhD Professor, Department of Mathematics University of Jaume I Castellon, Spain Ana Cristina Costa, PhD Professor, Nova Information Management School University of Nova Lisbon, Portugal Pablo Juan Verdoy, PhD Professor, Department of Mathematics University of Jaume I Castellon, Spain March 2020 ii DECLARATION OF ORIGINALITY I declare that the work described in this document is my own and not from someone else. All the assistance I have received from other people is duly acknowledged, and all the sources (published or not published) referenced. This work has not been previously evaluated or submitted to the University of Jaume I Castellon, Spain, or elsewhere. Castellon, 30th Feburaury 2020 Berhanu Berga Dadi iii Acknowledgments Before and above anything, I want to thank our Lord Jesus Christ, Son of GOD, for his blessing and protection to all of us to live. I want to thank also all consortium of Erasmus Mundus Master's program in Geospatial Technologies for their financial and material support during all period of my study. Grateful acknowledgment expressed to Supervisors: Prof.Dr.Jorge Mateu Mahiques, Universitat Jaume I(UJI), Prof.Dr.Ana Cristina Costa, Universidade NOVA de Lisboa, and Prof.Dr.Pablo Juan Verdoy, Universitat Jaume I(UJI) for their immense support, outstanding guidance, encouragement and helpful comments throughout my thesis work. Finally, but not least, I would like to thank my lovely wife, Workababa Bekele, and beloved daughter Loise Berhanu and son Nethan Berhanu for their patience, inspiration, and understanding during the entire period of my study. -

Yes I Do. Ethiopia – Amhara Region

Yes I Do. Ethiopia – Amhara Region The situation of child marriage in Qewet and Bahir Dar Zurida: a focus on gender roles, parenting and young people’s future perspectives Abeje Berhanu Dereje Tesama Beleyne Worku Almaz Mekonnen Lisa Juanola Anke van der Kwaak University of Addis Ababa & Royal Tropical Institute January 2019 1 Contents Abbreviations ................................................................................................................................................ 3 1. Introduction .......................................................................................................................................... 4 1.1 Background of the Yes I Do programme .............................................................................................. 4 1.2 Process of identifying themes for this study ....................................................................................... 4 1.3 Social and gender norms related to child marrige .............................................................................. 5 1.4 Objective of the study ......................................................................................................................... 7 2. Methodology ......................................................................................................................................... 9 2.1 Description of the study areas ............................................................................................................. 9 2.1.1 Qewet woreda, North Shewa zone.............................................................................................. -

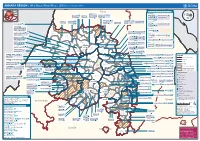

AMHARA REGION : Who Does What Where (3W) (As of 13 February 2013)

AMHARA REGION : Who Does What Where (3W) (as of 13 February 2013) Tigray Tigray Interventions/Projects at Woreda Level Afar Amhara ERCS: Lay Gayint: Beneshangul Gumu / Dire Dawa Plan Int.: Addis Ababa Hareri Save the fk Save the Save the df d/k/ CARE:f k Save the Children:f Gambela Save the Oromia Children: Children:f Children: Somali FHI: Welthungerhilfe: SNNPR j j Children:l lf/k / Oxfam GB:af ACF: ACF: Save the Save the af/k af/k Save the df Save the Save the Tach Gayint: Children:f Children: Children:fj Children:l Children: l FHI:l/k MSF Holand:f/ ! kj CARE: k Save the Children:f ! FHI:lf/k Oxfam GB: a Tselemt Save the Childrenf: j Addi Dessie Zuria: WVE: Arekay dlfk Tsegede ! Beyeda Concern:î l/ Mirab ! Concern:/ Welthungerhilfe:k Save the Children: Armacho f/k Debark Save the Children:fj Kelela: Welthungerhilfe: ! / Tach Abergele CRS: ak Save the Children:fj ! Armacho ! FHI: Save the l/k Save thef Dabat Janamora Legambo: Children:dfkj Children: ! Plan Int.:d/ j WVE: Concern: GOAL: Save the Children: dlfk Sahla k/ a / f ! ! Save the ! Lay Metema North Ziquala Children:fkj Armacho Wegera ACF: Save the Children: Tenta: ! k f Gonder ! Wag WVE: Plan Int.: / Concern: Save the dlfk Himra d k/ a WVE: ! Children: f Sekota GOAL: dlf Save the Children: Concern: Save the / ! Save: f/k Chilga ! a/ j East Children:f West ! Belesa FHI:l Save the Children:/ /k ! Gonder Belesa Dehana ! CRS: Welthungerhilfe:/ Dembia Zuria ! î Save thedf Gaz GOAL: Children: Quara ! / j CARE: WVE: Gibla ! l ! Save the Children: Welthungerhilfe: k d k/ Takusa dlfj k -

Addis Ababa University College of Development Studies Tourism Development and Managment Programme

ADDIS ABABA UNIVERSITY COLLEGE OF DEVELOPMENT STUDIES TOURISM DEVELOPMENT AND MANAGMENT PROGRAMME Assess Tourism Resources and Its Development Challenges in Sekela Wereda, West Gojjam, Amhara National Regional State, Ethiopia Submitted by: Mekuanent Ayalew Kassa A Thesis Submitted to the College of Development Studies of Addis Ababa University in Partial Fulfillment of the Requirements for the Degree of Master of Arts in Tourism Development and Management Addis Ababa University Addis Ababa, Ethiopia June, 2019 1 ADDIS ABABA UNIVERSITY COLLEGE OF DEVELOPMENT STUDIES TOURISM DEVELOPMENT AND MANAGMENT PROGRAMME Assess Tourism Resources and Its Development Challenges in Sekela Wereda, West Gojjam, Amhara National Regional State, Ethiopia Submitted by: Mekuanent Ayalew Kassa A Thesis Submitted to the College of Development Studies of Addis Ababa University in Partial Fulfillment of the Requirements for the Degree of Master of Arts in Tourism Development and Management Addis Ababa University Addis Ababa, Ethiopia June, 2019 2 ADDIS ABABA UNIVERSITY COLLEGE OF DEVELOPMENT STUDIES TOURISM DEVELOPMENT AND MANAGMENT PROGRAMME This is to certify that the thesis prepared by Mekuanent Ayalew Kassa, entitled: "Assess Tourism Resources and Its Development Opportunities and Challenges in Sekela Wereda". In partial fulfillment of the requirements for the Degree of Master of Art in Tourism Development and Management complies with the regulations of the University and meets the accepted standards with respect to originality and quality. Signed by Examining -

The Role of Users at the Different Levels of Wash Projects

Briefing note – No. 6 The Role of Users at the Different Levels of WaSH Projects Learning and Communications in WASH in Amhara Introductio n recommendations for increasing community management of WaSH in the Amhara Region. The In Africa and other developing countries, sustainability of rural water supply is quite low with 30 to 60% of the main research document will soon be available at schemes becoming non-functional at some point after www.wateraidethiopia.org and www.bdu.edu.et. implementation (Brikké and Bredero, 2003). The lack of community participation especially in management has been recognized as one of the reasons for the low Background sustainability (Carter.1999). For example, limited Harvey and Reed (2006) explain that “community involvement of the community at all stages of water participation does not automatically lead to effective development, the lack of a modest water service fee community management, nor should it have to. and a shortage of adequate skill and capacity to Community participation is a prerequisite for maintain water resources are specific aspects of sustainability, i.e. to achieve efficiency, effectiveness, community participation that have decreased equity, and replicablity, but community management is sustainability of rural water supply in the Amhara not. The community management in rural Ethiopia is Region of Ethiopia (Mengesha et al, 2003). based on the formation of water user committees All water supply providers in Ethiopia are currently usually at each water point in order to follow up the following the principle of community participation and implementation process, to manage the WaSH scheme community management in the rural area. -

English-Full (0.5

Enhancing the Role of Forestry in Building Climate Resilient Green Economy in Ethiopia Strategy for scaling up effective forest management practices in Amhara National Regional State with particular emphasis on smallholder plantations Wubalem Tadesse Alemu Gezahegne Teshome Tesema Bitew Shibabaw Berihun Tefera Habtemariam Kassa Center for International Forestry Research Ethiopia Office Addis Ababa October 2015 Copyright © Center for International Forestry Research, 2015 Cover photo by authors FOREWORD This regional strategy document for scaling up effective forest management practices in Amhara National Regional State, with particular emphasis on smallholder plantations, was produced as one of the outputs of a project entitled “Enhancing the Role of Forestry in Ethiopia’s Climate Resilient Green Economy”, and implemented between September 2013 and August 2015. CIFOR and our ministry actively collaborated in the planning and implementation of the project, which involved over 25 senior experts drawn from Federal ministries, regional bureaus, Federal and regional research institutes, and from Wondo Genet College of Forestry and Natural Resources and other universities. The senior experts were organised into five teams, which set out to identify effective forest management practices, and enabling conditions for scaling them up, with the aim of significantly enhancing the role of forests in building a climate resilient green economy in Ethiopia. The five forest management practices studied were: the establishment and management of area exclosures; the management of plantation forests; Participatory Forest Management (PFM); agroforestry (AF); and the management of dry forests and woodlands. Each team focused on only one of the five forest management practices, and concentrated its study in one regional state. -

ASSESSMENT of CHALLENGES of SUSTAINABLE RURAL WATER SUPPLY: QUARIT WOREDA, AMHARA REGION a Project Paper Presented to the Facult

ASSESSMENT OF CHALLENGES OF SUSTAINABLE RURAL WATER SUPPLY: QUARIT WOREDA, AMHARA REGION A Project Paper Presented to the Faculty of the Graduate School Of Cornell University In Partial Fulfillment of the Requirements for the Degree of Master of Professional Studies by Zemenu Awoke January 2012 © 2012 Zemenu Awoke Alemeyehu ABSTRACT Sustainability of water supplies is a key challenge, both in terms of water resources and service delivery. The United Nations International Children’s Fund (UNICEF) estimates that one third of rural water supplies in sub-Saharan Africa are non- operational at any given time. Consequently, the objective of this study is to identify the main challenges to sustainable rural water supply systems by evaluating and comparing functional and non-functional systems. The study was carried out in Quarit Woreda located in West Gojjam, Amhara Region, Ethiopia. A total of 217 water supply points (169 hand-dug wells and 50 natural protected springs) were constructed in the years 2005 to 2009. Of these water points, 184 were functional and 33 were non-functional. Twelve water supply systems (six functional and six non-functional) among these systems were selected. A household survey concerning the demand responsiveness of projects, water use practices, construction quality, financial management and their level of satisfaction was conducted at 180 households. All surveyed water projects were initiated by the community and the almost all of the potential users contributed money and labor towards the construction of the water supply point. One of the main differences between the functional and non-functional system was the involvement of the local leaders.