Présentation Powerpoint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Innovation in Loyalty and Customer Experience at Orange Belgium

CASE STUDY INNOVATION IN LOYALTY AND CUSTOMER EXPERIENCE AT ORANGE BELGIUM © 2019 Evolving Systems, Inc. Evolving Systems is a registered trademark of Evolving Systems, Inc. E: [email protected] I T: +1 303 802 1000 I F: +1 303 802 1420 Evolving Systems and Orange Belgium - for the continued management, enhancement and expansion of the customer loyalty program, Orange Thank You – has been recognized by the prestigious Total Telecoms World Communications Awards as a step forward in digital engagement. Evolving was initially selected by Orange to create a brand-new loyalty concept, provide the technical foundation, and deliver a shared new vision to enhance customer loyalty. SITUATION In 2013, Orange Belgium acknowledged a need to revitalise its approach to customer loyalty. Its existing programs weren’t delivering the desired outcomes and additionally were providing little, if any, brand differentiation. Plus, the appearance of aggressive new competitors in the market as well as regulatory changes relating to the mobile industry meant that a new approach was urgently needed to protect and improve the company’s market position. Orange’s initial objectives for its new approach included creating a single program for all markets - pre and postpaid. While addressing churn remained a primary goal, the company realised that traditional loyalty approaches had been ineffective at doing this in the past. “We knew we could make industry-standard offers like increasing megabytes” says Benoit Berthelot, Customer Engagement Manager at Orange Belgium, “but we also knew such offers were easily imitated and did little to really build strong relationships with our subscribers”. Instead, Orange wanted to “rewire” the entire customer relationship and in the process create something more emotionally engaging. -

Je Zenders in Wallonië

Je zenders in Wallonië 34 ● Cartoon Network 73 ● HD Museum TV F Franstalige zenders Muziek 35 ● HD Studio 100 76 HD National Geographic Wild EC ND M F 141 HD Bel RTL TV Klassiek 36 ● Baby TV 77 Science et Vie TV EC ND M F 142 ● HD Tipik Vision ● HD 41 ● Boomerang KC K M F 78 Histoire TV EC ND NS M F 1 La Une 143 Radio Contact Vision 2 ● HD Tipik 42 ● Nick Jr KC K M F 79 HD Ushuaïa TV EC ND M F 144 ● RFM TV 3 ● HD RTL-TVI 43 ● Tiji KC K M F 80 Animaux EC ND M F 145 Trace Urban 4 ● HD Club RTL 44 ● Canal J KC K M F 82 ● HD Crime District EC F 150 HD Stingray Classica EC MC M F ● 5 HD Plug RTL 45 ● Mangas KC K M F 85 ● HD VICEtv 151 HD Mezzo Live EC MC NS M F 6 ● HD TF1 46 ● HD Gulli KC K F 86 HD E! 152 MTV 80s EC MC M F 7 ● HD France 2 49 Studio 100 GO Pass (toegang) 87 HD Dobbit TV 153 HD MTV Live EC MC M F 8 ● HD France 3 88 HD Game One F M 9 ● HD La Trois 154 MTV Hits EC NS F Entertainment, cultuur en natuur 89 ● MTV FR 10 Regionale zender ● HD F EC M F ● HD AS 90 My Zen TV 155 ● Melody MC NS 11 ● Pickx Live 50 Pickx+ FR FR FR 99 ● HD Pickx+ AS 13 ● HD Pickx+ AS 51 ● HD Be1 14 ● HD Pickx+ Sports 1 AS BS 52 ● HD Be Séries Regionaal 17 ● HD Canal Z 53 ● HD Be Ciné Sport 160 ●x bx1 18 HD LN24 54 ● HD Ciné+ Premier 100 ● HD Pickx Live 161 ●x Antenne Centre 20 ● HD AB3 55 ● HD Ciné+ Frisson 101- ● HD Pickx+ Sports 1-10 AS IS BS 110 162 ●x Canal C 21 ● HD ABXPLORE 56 ● HD Ciné+ Classic 111 ● HD Eleven Pro League 1 AS IS BS 163 ●x Canal Zoom 57 Netflix N 112 ● HD Eleven Pro League 2 AS IS BS 164 ●x MaTélé Klassiek Internationaal 60 ● HD Action -

Annual Financial Statements 2020

ANNUAL FINANCIAL STATEMENTS 2020 CI FIRST ASSET EXCHANGE-TRADED FUNDS DECEMBER 31, 2020 Table of Contents Independent Auditor’s Report .............................................................................................. 1 CI First Asset 1-5 Year Laddered Government Strip Bond Index ETF .......................................... 4 CI First Asset Active Canadian Dividend ETF............................................................................... 12 CI First Asset Active Credit ETF ................................................................................................... 22 CI First Asset Active Utility & Infrastructure ETF ....................................................................... 36 CI First Asset Canadian Buyback Index ETF ................................................................................. 46 CI First Asset Canadian Convertible Bond ETF ............................................................................ 55 CI First Asset Canadian REIT ETF ................................................................................................. 66 CI First Asset CanBanc Income Class ETF.................................................................................... 76 CI First Asset Core Canadian Equity Income Class ETF ............................................................... 84 CI First Asset Energy Giants Covered Call ETF ............................................................................ 93 CI First Asset Enhanced Government Bond ETF.......................................................................... -

Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Industry analysis #3 2019 Mobile data – first half 2019 Mobile data consumption continues to grow – a majority of operators now rewarded with ARPU Taiwan: Unlimited is so last year – Korea: 5G boosts usage Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2019. tefficient AB www.tefficient.com 5 September 2019 1 The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth – for the first time a majority is in green. Read on to see who delivered on “more for more” – and who didn’t. Speaking of which, we take a closer look at the development of one of the unlimited powerhouses – Taiwan. Are people getting tired of mobile data? We also provide insight into South Korea – the world’s leading 5G market. Just how much effect did 5G have on the data usage? tefficient AB www.tefficient.com 5 September 2019 2 Fifteen operators now above 10 GB per SIM per month Figure 1 shows the average mobile data usage for 115 reporting or reported1 mobile operators globally with values for the first half of 2019 or for the full year of 2018. DNA, FI 3, AT Zain, KW Elisa, FI LMT, LV Taiwan Mobile, TW 1) FarEasTone, TW 1) Zain, BH Zain, SA Chunghwa, TW 1) *Telia, FI Jio, IN Nova, IS **Maxis, MY Tele2, LV 3, DK Celcom, MY **Digi, MY **LG Uplus, KR 1) Telenor, SE Zain, JO 3, SE Telia, DK China Unicom, CN (handset) Bite, -

ZONE COUNTRIES OPERATOR TADIG CODE Calls

Calls made abroad SMS sent abroad Calls To Belgium SMS TADIG To zones SMS to SMS to SMS to ZONE COUNTRIES OPERATOR received Local and Europe received CODE 2,3 and 4 Belgium EUR ROW abroad (= zone1) abroad 3 AFGHANISTAN AFGHAN WIRELESS COMMUNICATION COMPANY 'AWCC' AFGAW 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN AREEBA MTN AFGAR 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN TDCA AFGTD 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 3 AFGHANISTAN ETISALAT AFGHANISTAN AFGEA 0,91 0,99 2,27 2,89 0,00 0,41 0,62 0,62 1 ALANDS ISLANDS (FINLAND) ALANDS MOBILTELEFON AB FINAM 0,08 0,29 0,29 2,07 0,00 0,09 0,09 0,54 2 ALBANIA AMC (ALBANIAN MOBILE COMMUNICATIONS) ALBAM 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALBANIA VODAFONE ALBVF 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALBANIA EAGLE MOBILE SH.A ALBEM 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA DJEZZY (ORASCOM) DZAOT 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA ATM (MOBILIS) (EX-PTT Algeria) DZAA1 0,74 0,91 1,65 2,27 0,00 0,41 0,62 0,62 2 ALGERIA WATANIYA TELECOM ALGERIE S.P.A. -

Belgian Cable Observatory

Belgian Cable Observatory PRODUCED B Y IDATE O N BEHALF O F O R A N G E BELGIUM UNDER T H E ACADEMIC CONTROL OF PROF A. DE STREEL,DIRECTOR O F C R I D S , NAMUR UNIVERSITY Agenda – What are the impacts of cable opening on Belgian broadband markets so far? Cable opening scores better than copper opening in the past Price trends and competitive environment have not changed much at this stage Investments were upheld Regulatory changes have been decided recently Conclusion: Cable opening is off to an encouraging start, but it is still too early to draw definitive conclusions NGA adoption keeps increasing at a steady pace in Belgium Market shares on the Belgian Residential NGA fixed broadband Net Residential NGA lines additions per player market In number of lines In % of subscriptions Source: BIPT Source: BIPT Cable opening shows better results than copper unbundling COPPER LOCAL LOOP UNBUNDLING HAS FAILED IN BELGIUM, AS ON THE CONTRARY, AFTER ONLY TWO YEARS OF AVAILABILITY, DEMONSTRATED BY STEADILY DECREASING WHOLESALE PRODUCTS SALES BITSTREAM CABLE ADOPTION IS RAPIDLY INCREASING Sales of fully and partially unbundled lines by Proximus, 2010-2017 • Since the opening of the cable market, Orange Belgium as its main Number of lines beneficiary has gained more than 155,000 Cable subscribers in Belgium • This represents an average quarterly increase of +39% in subscribers since Q1 2016 • As a comparison, two years after the beginning of copper local loop unbundling in Belgium, the total of fully and partially unbundled copper lines activated was -

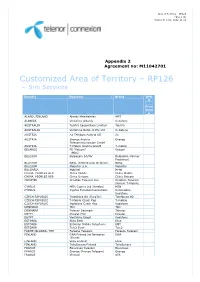

Customized Area of Territory – RP126 – Sim Services

Area of Territory – RP126 Page 1 (3) Version D rel01, 2012-11-21 Appendix 2 Agreement no: M11042701 Customized Area of Territory – RP126 – Sim Services Country Operator Brand GPR S Price Grou p ALAND, FINLAND Alands Mobiltelefon AMT ALBANIA Vodafone Albania Vodafone AUSTRALIA Telstra Corporation Limited Telstra AUSTRALIA Vodafone Network Pty Ltd Vodafone AUSTRIA A1 Telekom Austria AG A1 AUSTRIA Orange Austria Orange Telecommunication GmbH AUSTRIA T-Mobile Austria GmbH T-mobile BELARUS FE “Velcom” Velcom (MDC) BELGIUM Belgacom SA/NV Belgacom (former Proximus) BELGIUM BASE (KPN Orange Belgium) BASE BELGIUM Mobistar S.A. Mobistar BULGARIA Mobiltel M-tel CHINA, PEOPLES REP. China Mobile China Mobile CHINA, PEOPLES REP. China Unicom China Unicom CROATIA Croatian Telecom Inc. Croatian Telecom (former T-Mobile) CYPRUS MTN Cyprus Ltd (Areeba) MTN CYPRUS Cyprus Telecommunications Cytamobile- Vodafone CZECH REPUBLIC Telefónica O2 (EuroTel) Telefónica O2 CZECH REPUBLIC T-Mobile Czech Rep T-mobile CZECH REPUBLIC Vodafone Czech Rep Vodafone DENMARK TDC TDC DENMARK Telenor Denmark Telenor EGYPT Etisalat Misr Etisalat EGYPT Vodafone Egypt Vodafone ESTONIA Elisa Eesti Elisa ESTONIA Estonian Mobile Telephone EMT ESTONIA Tele2 Eesti Tele2 FAROE ISLANDS, THE Faroese Telecom Faroese Telecom FINLAND DNA Finland (fd Networks DNA (Finnet) FINLAND Elisa Finland Elisa FINLAND TeliaSonera Finland TeliaSonera FRANCE Bouygues Telecom Bouygues FRANCE Orange (France Telecom) Orange FRANCE Vivendi SFR Area of Territory – RP126 Page 2 (3) Version D rel01, 2012-11-21 GERMANY E-Plus Mobilfunk E-plus GERMANY Telefonica O2 Germany O2 GERMANY Telekom Deutschland GmbH Telekom (former T-mobile) Deutschland GERMANY Vodafone D2 Vodafone GREECE Vodafone Greece (Panafon) Vodafone GREECE Wind Hellas Wind Telecommunications HUNGARY Pannon GSM Távközlési Pannon HUNGARY Vodafone Hungary Ltd. -

MPSC Case No. U-13746 FRANCE TELECOM CORPORATE

MPSC Case No. U-13746 FRANCE TELECOM CORPORATE SOLUTIONS L.L.C. DIRECT TESTIMONY OF JEAN-SEBASTIEN FALISSE EXHIBIT 3 (A-) FINANCIAL STATEMENTS OF FRANCE ThLlkOM S.A. AND BANK STATEMENT OF FRANCE TELECOM CORPORATE SOLUTIONS L.L.C. France Telecom Corporate Solutions L.L.C. Demonstration of Financial Capability As a newly-formed company, Applicant does not have any audited financial statements. Applicant is majority owned and controlled by France T&corn S.A. (“France Telecom”), one of the largest communications companies in the world. Applicant’s financial information will be fully consolidated in the financial statements of its parent company.’ A copy of France Telecom’s consolidated audited financial statements for the last three years is attached. France Telecom is a leading integrated communications company which is publicly- traded on both the Paris Stock Exchange and the New York Stock Exchange. As indicated in its audited 2001 financial statements, France Telecom’s consolidated revenue for the year was S43.026 billon, EBITDA was E12.32 billion, and operating income was S5.2 billion.2 The attached financial documents demonstrate that France Telecom Corporate Solutions L.L.C. clearly possesses the requisite tinancial capability to provide intrastate telecommunications services in this State. ’ See Consolidated Financial Statements - France Telecom, 2001, 2000 and 1999 at p. 7 (“companies which are wholly owned or which France Telecom controls, either directly or indirectly, are fully consolidated”). 2 Id. at p. 3. As of September 12, 2002, the exchange rate between the euro and the U.S. dollar was approximately cl to US$O.98. -

APSCC Monthly E-Newsletter

APSCC Monthly e‐Newsletter October 2020 The Asia‐Pacific Satellite Communications Council (APSCC) e‐Newsletter is produced on a monthly basis as part of APSCC’s information services for members and professionals in the satellite industry. Subscribe to the APSCC monthly newsletter and be updated with the latest satellite industry news as well as APSCC activities! To renew your subscription, please visit www.apscc.or.kr. To unsubscribe, send an email to [email protected] with a title “Unsubscribe.” News in this issue has been collected from September 1 to Septmebr 30. INSIDE APSCC APSCC 2020 Conference Series Season 2 Starts from October 7: LIVE Every Wednesday 9AM HK l Singapore Time from October 7 to November 25 APSCC 2020 is the largest annual event of the Asia Pacific satellite community, which incorporates industry veterans, local players as well as new players into a single platform in order to reach out to a wide-ranging audience. Organized by the Asia Pacific Satellite Communications Council (APSCC), APSCC 2020 this year is even stretching further by going virtual and live. Every Wednesday mornings at 9 AM Hong Kong and Singapore time, new installments in APSCC 2020 will be presented live - in keynote speeches, panel discussions, and in presentations followed by Q&A format. Topics will range across a selection of issues the industry is currently grappling with globally, as well as in the Asia-Pacific region. Register now and get access to the complete APSCC 2020 Series with a single password. To register go to https://apsccsat.com. SATELLITE BUSINESS Nelco and Telesat Partner to Bring Advanced LEO Satellite Network to India September 30, 2020 - Nelco has entered into a cooperation agreement with Telesat, a leading global satellite operator that has been addressing complex connectivity challenges for over 50 years. -

Numbers Zona Establec. Llamada (€) € Por Minuto Destinos 88299 Blocked Aeromóvil 93 Internacional 6 0,00 0,35 Afganistán 9

Establec. € por Numbers Zona Destinos llamada (€) minuto 88299 Blocked Aeromóvil 93 Internacional 6 0,00 0,35 Afganistán 9377 Internacional 6 0,00 0,35 Afganistán, móvil Areeba 9375 Internacional 6 0,00 0,35 Afganistán, móvil AT 9370 Internacional 6 0,00 0,35 Afganistán, móvil AWCC 9378 Internacional 6 0,00 0,35 Afganistán, móvil Etisalat 9379 Internacional 6 0,00 0,35 Afganistán, móvil Rosham 1907 Internacional 2 0,00 0,15 Alaska 355 Internacional 3 0,00 0,20 Albania 35568 Internacional 5 0,00 0,30 Albania, móvil 35569 Internacional 5 0,00 0,30 Albania, móvil 3554 Internacional 3 0,00 0,20 Albania, Tirana 213 Internacional 4 0,00 0,25 Argelia 21321 Internacional 4 0,00 0,25 Argelia, Argel 2131 Internacional 4 0,00 0,25 Argelia, Área CAT 2136 Internacional 4 0,00 0,25 Argelia, móvil AMN 21398 Internacional 4 0,00 0,25 Argelia, móvil AMN 21399 Internacional 4 0,00 0,25 Argelia, móvil AMN 2137 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21390 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21391 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21392 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21393 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21394 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21395 Internacional 4 0,00 0,25 Argelia, móvil Orascom 21350 Internacional 4 0,00 0,25 Argelia, móvil Wataniya 21351 Internacional 4 0,00 0,25 Argelia, móvil Wataniya 21352 Internacional 4 0,00 0,25 Argelia, móvil Wataniya 21353 Internacional 4 0,00 0,25 Argelia, móvil Wataniya 21354 Internacional 4 0,00 0,25 Argelia, móvil Wataniya -

Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017

Report of Activities Pursuant to Act 44 of 2010 Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017 Appendix D: Securities Held by Funds The Four Funds hold thousands of publicly and privately traded securities. Act 44 directs the Four Funds to publish “a list of all publicly traded securities held by the public fund.” For consistency in presenting the data, a list of all holdings of the Four Funds is obtained from Pennsylvania Treasury Department. The list includes privately held securities. Some privately held securities lacked certain data fields to facilitate removal from the list. To avoid incomplete removal of privately held securities or erroneous removal of publicly traded securities from the list, the Four Funds have chosen to report all publicly and privately traded securities. The list below presents the securities held by the Four Funds as of June 30, 2017. 1345 AVENUE OF THE A 1 A3 144A AAREAL BANK AG ABRY MEZZANINE PARTNERS LP 1721 N FRONT STREET HOLDINGS AARON'S INC ABRY PARTNERS V LP 1-800-FLOWERS.COM INC AASET 2017-1 TRUST 1A C 144A ABRY PARTNERS VI L P 198 INVERNESS DRIVE WEST ABACUS PROPERTY GROUP ABRY PARTNERS VII L P 1MDB GLOBAL INVESTMENTS L ABAXIS INC ABRY PARTNERS VIII LP REGS ABB CONCISE 6/16 TL ABRY SENIOR EQUITY II LP 1ST SOURCE CORP ABB LTD ABS CAPITAL PARTNERS II LP 200 INVERNESS DRIVE WEST ABBOTT LABORATORIES ABS CAPITAL PARTNERS IV LP 21ST CENTURY FOX AMERICA INC ABBOTT LABORATORIES ABS CAPITAL PARTNERS V LP 21ST CENTURY ONCOLOGY 4/15 -

European Fibre Networks V Building the Gigabit Society – Incumbent Deployments Accelerating

4 September 2020 Equity Research Europe European Fibre Networks V Building the gigabit society – incumbent deployments accelerating Integrated Telecommunication Services | Theme Summary: In our fifth annual review of fibre-to-the-home (FTTH) in Europe, we look at Research Analysts the current landscape for both public and private fibre network deployment. FTTH deployments are accelerating across Europe (and in our view will accelerate further) and we Jakob Bluestone, CFA expect fibre assets to re-rate over time. We introduce our FTTH market dashboard for 44 20 7883 0834 ranking future FTTH investment opportunities. [email protected] Fibre deployment accelerating: In Western Europe, nearly 40% of premises were passed Ben Lyons by FTTH at end-2019 with the pace of deployment accelerating +15% to 12.5m incremental 44 20 7888 8742 [email protected] premises passed. We expect a further +10% acceleration in homes passed in 2020 and FTTH coverage to reach 74% by 2024. In particular, incumbent deployments are picking up; Paul Sidney e.g. in the UK, France and the Netherlands, incumbents are accelerating build. 44 20 7888 6015 [email protected] Demand growing but still lagging: FTTH uptake is lagging deployment, with 15% of premises taking FTTH-broadband, but we expect this to rise to 33% by 2024. We believe Evgeny Kudinov in a post-COVID-19 world, demand for fixed connectivity generally – and FTTH in particular 44 20 7888 1791 – will be higher. We also expect FTTH to take share from cable, which has tended to lose [email protected] market share when faced with FTTH-based infrastructure competition.