A Study on Free-Floating Carsharing in Europe Impacts of Car2go and Drivenow on Modal Shift, Vehicle Ownership

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Value Configurations in Sharing Economy Business Models

Review of Managerial Science https://doi.org/10.1007/s11846-020-00433-w ORIGINAL PAPER Value confgurations in sharing economy business models Andreas Reuschl1 · Victor Tiberius2 · Matthias Filser3,4 · Yixin Qiu5 Received: 30 November 2019 / Accepted: 24 December 2020 © The Author(s) 2021 Abstract The sharing economy gains momentum and develops a major economic impact on traditional markets and frms. However, only rudimentary theoretical and empiri- cal insights exist on how sharing networks, i.e., focal frms, shared goods providers and customers, create and capture value in their sharing-based business models. We conduct a qualitative study to fnd key diferences in sharing-based business models that are decisive for their value confgurations. Our results show that (1) customiza- tion versus standardization of shared goods and (2) the centralization versus particu- larization of property rights over the shared goods are two important dimensions to distinguish value confgurations. A second, quantitative study confrms the visibility and relevance of these dimensions to customers. We discuss strategic options for focal frms to design value confgurations regarding the two dimensions to optimize value creation and value capture in sharing networks. Firms can use this two-dimen- sional search grid to explore untapped opportunities in the sharing economy. Keywords Sharing economy · Business model · Customization · Standardization · Property rights · Value creation · Value capture · Value confguration JEL Classifcation L15 · M10 · M13 1 Introduction The sharing economy comprises all activities related to sharing or granting access to goods and services (Hamari et al. 2016). Sharing is organized in sharing networks. A focal frm manages the platform which connects the shared goods providers and customers. -

Efficient Dynamics

A subsidiary of BMW AG BMW U.S. Press Information For Release: October 24, 2013 – 6:00pm EDT/3:00pm PDT Contact: Matthew Russell Product and Technology Communications Manager 201-307-3783 / [email protected] David J. Buchko Product and Technology Communications 201-307-3709 / [email protected] Julian Arguelles Product and Technology Communications 201-307-3755 / [email protected] The All-New BMW 2 Series Coupe A new dimension for The Ultimate Driving MachineTM Woodcliff Lake, N.J. – October 24, 2013 – 6:00pm EDT/3:00pm PDT. BMW today announced the introduction of an entirely new model series with the introduction of the all-new BMW 2 Series Coupe. This new take on The Ultimate Driving MachineTM will arrive in the US in the first quarter of 2014 as the 228i and the M235i. The BMW M235i, the first M Performance Automobile offered in the US, includes an impressive list of performance enhancing features. This successor to the successful 1 Series Coupe will continue the decades-long tradition of premium sub-compact coupes with impeccable driving dynamics when it makes its world debut at the North American International Auto Show in January 2014. The 2014 BMW 2 Series Coupe will be offered at a Manufacturer’s Suggested Retail Price of $33,025 for the 228i and $44,025 for the M235i, including $925 destination and handling. The BMW 2 Series Coupe • BMW celebrates the premiere of another new model series – The BMW 2 Series Coupe which raises the bar in the premium sub-compact segment in terms of dynamic ability, aesthetic appeal and emotional allure; a distinctive vehicle concept unique in its segment, with a two-door body in classic three-box design typical of BMW Coupes, four seats, rear-wheel drive and a pair of engines and chassis set-up focused squarely on sporting ability; market launch from March 2014, line-up to include a BMW M Performance Automobile – the BMW M235i Coupe. -

Télécharger La Synthèse De L'enquête Nationale Sur L'autopartage 2019

Enquête nationale sur l’autopartage - Edition 2019 Actualisation et étude de l’impact des services d’autopartage sur l’équipement des ménages et sur les kilomètres parcourus en voiture UNE ÉTUDE RÉALISÉE PAR 6T-BUREAU DE RECHERCHE SUR UN COFINANCEMENT 6T ET ADEME Contexte Enjeux Publiées en 2012 et 2016, les deux premières Tout comme en 2012 et 2016, l’édition 2019 porte éditions de l’Enquête Nationale sur l’Autopartage1 principalement sur l’autopartage en boucle. Elle vise constituaient les premières études d’envergure sur deux objectifs : les usagers, usages et impacts de l’autopartage en France. mettre à jour les résultats de la précédente édition : les usagers, usages et impacts de l’autopartage ont- Menées auprès d’au moins 2 000 usagers abonnés ils évolué entre 2016 et 2019 ? d’une vingtaine de services d’autopartage différents, ces enquêtes ont mis en évidence l’effet « déclencheur affiner la compréhension des usagers, usages et de multimodalité » de l’autopartage en boucle : impacts de l’autopartage : notamment, qui sont les l’autopartage permet aux habitants des villes de usagers de l’autopartage ? Une fois abonnés à s’affranchir de la voiture individuelle, de découvrir l’autopartage, leurs pratiques de déplacements et de s’approprier d’autres modes de déplacement. évoluent-elles de la même manière ? Quels sont les usages et les impacts de l’autopartage entre Trois ans après la dernière enquête, l’autopartage particuliers et de l’autopartage en contexte joue-t-il encore le même rôle dans la mobilité professionnel ? urbaine ? Ses usagers sont-ils restés les mêmes ? Ses usages, ses impacts ont-ils évolué ? Le rapport d’étude complet est disponible sur notre blog : Lien Autopartage B2C en boucle : (fr Autopartage B2C en trace Autopartage entre l’objet principal de l’étude directe particuliers ou P2P Le véhicule est rendu dans la Avec stations : le véhicule peut Réalisée entre particuliers station de départ. -

Efficient Dynamics

A subsidiary of BMW AG BMW U.S. Press Information For Release: Immediate Contact: Oleg Satanovsky BMW Product & Technology Spokesperson 201-307-3755 / [email protected] Alex Schmuck BMW Product & Technology Communications Manager [email protected] 201-307-3783 BMW Model Year 2020 Update Information. Woodcliff Lake, NJ – August 1, 2019… Information on design and technical changes, as well as changes to standard equipment, lines, packages and standalone options are included in this document. This document will be continuously updated with the most recent MY20 information as it becomes available. The following upholsteries on X5 (G05), X6 (G06), and X7 (G07) models are not currently (Aug 2019) available for order but will be re-introduced at a later date. • Canberra Beige Vernasca Leather • Cognac Vernasca Leather (available on G07 w/Captain’s Chairs only) • Extended Tartufo Merino Leather (available on G07 w/ Captain’s Chairs only) • Full Tartufo Merino Leather • Amarone Merino Leather Discontinued models for 2020 • BMW 3 Series GT • BMW 6 Series Gran Coupe - 2 - 2020 BMW i3 120Ah BMW i3 battery was upgraded from 94Ah to 120Ah for 2019. Electric only range increased up to 153 miles from 94Ah / 115 miles. 2019 BMW i3 120Ah press release. MY20 i3 information is still tba. 2020 BMW i8 Coupe and Roadster MY20 i8 Coupe and Roadster information is still tba. 2020 BMW 2 Series Coupe and Convertible Prices remain unchanged from 2019. MY20 2 Series Coupes and Convertibles began production in 3/2019. The M2 Competition was new for 2019. 2019 M2 Competition press release The MY20 2 Series receives a second refresh as of March 2019 and has been enhanced with the following features: • New darker taillights • New high-gloss black kidney frame on 230i • Cerium Grey kidney frame, badges, front/side air inserts on M240i • High-gloss black mirror caps on M240i Standard Equipment Changes: • Smoker’s Package has been removed from the standard profile for all 2 series. -

New BMW 2 Series Convertible.Pdf

A subsidiary of BMW AG BMW U.S. Press Information For Release: September 9, 2014 6:00pm EDT/3:00pm PDT Contact: Matthew Russell Product & Technology Communications Manager 201-307-3783 / [email protected] David J. Buchko Product & Technology Communications Spokesperson 201-307-3709 / [email protected] Julian Arguelles Product & Technology Communications Spokesperson 201-307-3755 / [email protected] The New BMW 2 Series Convertible Style and dynamics of the acclaimed BMW 2 Series Coupe combined with open-air driving Available in the US as 228i and M235i All-wheel drive 228i xDrive available from launch Woodcliff Lake, NJ – September 9, 2014 6:00pm EDT/3:00pm PDT. Few new cars have been more anticipated than the BMW 2 Series Coupe when it arrived in early 2014. Hot on the heels of the widely acclaimed BMW 228i and M235i Coupe, BMW announces the new BMW 2 Series Convertible. Available in the US as the 228i and M235i, the 2 Series Convertible blends the style and dynamic driving character for which the 2 Series Coupe is already renowned with the open-air pleasure of a folding soft-top. The BMW 2 Series Convertible will make its world debut at the Paris Motor Show. The 2015 M235i and 228i as well as the 228i xDrive, featuring BMW’s intelligent all-wheel drive system, will arrive in US showrooms in early 2015. The 2015 BMW 2 Series Convertible will be offered at a Manufacturer’s Suggested Retail Price of $38,850 for the 228i, $40,650 for the 228i xDrive, $48,650 for the M235i, including $950 destination and handling. -

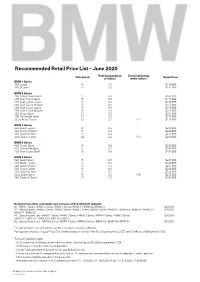

Recommended Retail Price List – June 2020

Recommended Retail Price List – June 2020 Fuel Consumption Electrical Energy VES (band) Retail Price (l/100km) (kWh/100km) BMW 1 Series 118i Luxury B 5.9 $139,888 118i M Sport B 5.9 $142,888 BMW 2 Series 216i Active Tourer Sport B 6.3 $141,888 216i Gran Tourer Sport B 6.5 $147,888 216i Gran Tourer Luxury B 6.5 $154,888 216i Gran Tourer M Sport B 6.5 $157,888 218i Gran Coupe Luxury B 5.9 $155,888 218i Gran Coupe M Sport B 5.9 $158,888 218i Coupe Sport C1 5.5 $161,888 218i Convertible Sport C1 5.8 $177,888 225xe Active Tourer B 2.4 17.4 $176,888 BMW 3 Series 320i Sedan Luxury B 6.3 $200,888 320i Sedan M Sport B 6.3 $206,888 330i Sedan M Sport B 6.4 $233,888 330e Sedan Luxury A2 2.2 15.4 $240,888 BMW 4 Series 420i Coupe Sport B 5.8 $200,888 420i Convertible Sport B 6.2 $242,888 420i Gran Coupe Sport B 5.8 $194,888 BMW 5 Series 520i Sedan Sport B 6.5 $237,888 520i Sedan Luxury B 6.5 $240,888 520i Sedan M Sport B 6.5 $251,888 530i Sedan Luxury B 6.5 $256,888 530i Sedan M Sport B 6.5 $274,888 530e Sedan Sport B 2.0 15.6 $272,888 540i Sedan M Sport C1 7.3 $345,888 Booking Fees (Non-refundable and inclusive of $10,000 COE deposit): A1. -

Impact of Car Sharing on Urban Sustainability

sustainability Review Impact of Car Sharing on Urban Sustainability Vasja Roblek 1 , Maja Meško 2,3 and Iztok Podbregar 3,* 1 Faculty of Organisation Studies in Novo Mesto, 8000 Novo Mesto, Slovenia; [email protected] 2 Faculty of Management, University of Primorska, 6000 Koper, Slovenia; [email protected] 3 Faculty of Organizational Sciences, University of Maribor, 4000 Kranj, Slovenia * Correspondence: [email protected] Abstract: The article gives us an insight into the key issues of car sharing and its impact on urban sus- tainability. A selection of 314 articles published in peer-reviewed journals from the Scopus database were analysed using Leximancer 5.0 for Automated Content analysis. A total of seven themes were identified explaining the researched topic of the car sharing situation in Europe, which are sharing, economy, model, systems, electrical car sharing, policy and travel. There are two ways of sharing owned cars in Europe; access to cars from the fleet of private organisations and P2P car sharing. Sustainable environmental solutions in the context of the electrification of cars are used. Car sharing usually takes place online and can be free or for a fee as defined by The European Economic and Social Committee. The article provides an overview of understanding the concept of urban car sharing in Europe. Keywords: sustainability; urban sustainability; car sharing; Europe 1. Introduction This article aims to provide an overview of understanding the concept of urban car sharing, whose growth and development has been influenced by the recent financial crisis Citation: Roblek, V.; Meško, M.; that caused an economic recession in both the US and Europe between 2007 and mid-2009, Podbregar, I. -

Free-Floating Carsharing in Copenhagen: a Study on User Experience in a Cycling City

Downloaded from orbit.dtu.dk on: Sep 25, 2021 Free-floating carsharing in Copenhagen: A study on user experience in a cycling city Garrett, Anna Hviid; Nielsen, Janet; Nielsen, Thomas Sick; Haustein, Sonja Published in: Danish Journal of Transportation Research - Dansk tidskrift for transportforskning Publication date: 2021 Document Version Publisher's PDF, also known as Version of record Link back to DTU Orbit Citation (APA): Garrett, A. H., Nielsen, J., Nielsen, T. S., & Haustein, S. (2021). Free-floating carsharing in Copenhagen: A study on user experience in a cycling city. Danish Journal of Transportation Research - Dansk tidskrift for transportforskning, 3, 14-34. General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. Users may download and print one copy of any publication from the public portal for the purpose of private study or research. You may not further distribute the material or use it for any profit-making activity or commercial gain You may freely distribute the URL identifying the publication in the public portal If you believe that this document breaches copyright please contact us providing details, and we will remove access to the work immediately and investigate your claim. Danish Journal of Transportation Research – Dansk Tidsskrift for Transportforskning Vol 3. (2021) 14-34 Free-floating carsharing in Copenhagen: A study on user experience in a cycling city Anna Hviid Garrett, City of Copenhagen, email: [email protected] Janet Nielsen, email: [email protected] Thomas Sick Nielsen, Danish Road Directorate, email: [email protected] corresponding author Sonja Haustein, Technical University of Denmark, DTU, email: [email protected] Article info Abstract Free-floating carsharing is emerging in cities around the world. -

20-03 Residential Carshare Study for the New York Metropolitan Area

Residential Carshare Study for the New York Metropolitan Area Final Report | Report Number 20-03 | February 2020 NYSERDA’s Promise to New Yorkers: NYSERDA provides resources, expertise, and objective information so New Yorkers can make confident, informed energy decisions. Mission Statement: Advance innovative energy solutions in ways that improve New York’s economy and environment. Vision Statement: Serve as a catalyst – advancing energy innovation, technology, and investment; transforming New York’s economy; and empowering people to choose clean and efficient energy as part of their everyday lives. Residential Carshare Study for the New York Metropolitan Area Final Report Prepared for: New York State Energy Research and Development Authority New York, NY Robyn Marquis, PhD Project Manager, Clean Transportation Prepared by: WXY Architecture + Urban Design New York, NY Adam Lubinsky, PhD, AICP Managing Principal Amina Hassen Associate Raphael Laude Urban Planner with Barretto Bay Strategies New York, NY Paul Lipson Principal Luis Torres Senior Consultant and Empire Clean Cities NYSERDA Report 20-03 NYSERDA Contract 114627 February 2020 Notice This report was prepared by WXY Architecture + Urban Design, Barretto Bay Strategies, and Empire Clean Cities in the course of performing work contracted for and sponsored by the New York State Energy Research and Development Authority (hereafter the "Sponsors"). The opinions expressed in this report do not necessarily reflect those of the Sponsors or the State of New York, and reference to any specific product, service, process, or method does not constitute an implied or expressed recommendation or endorsement of it. Further, the Sponsors, the State of New York, and the contractor make no warranties or representations, expressed or implied, as to the fitness for particular purpose or merchantability of any product, apparatus, or service, or the usefulness, completeness, or accuracy of any processes, methods, or other information contained, described, disclosed, or referred to in this report. -

Quickar(PDF 8.49

7 September 2017 The Secretary, Economy and Infrastructure Committee Parliament House, Spring Street EAST MELBOURNE VIC 3002 Dear Secretary, Please accept this cover letter and attached report as a submission to the Committee’s Inquiry into Electric Vehicles. A mushrooming of Melbourne’s population over the next 20 years combined with the phenomena of significant population detachment from economic hubs driven by growing rates of car ownership and burgeoning investment by government in private car driver-driven infrastructure is a looming urban mobility crisis. We risk sleepwalking into a situation where our once “world’s most livable city” has insufficient public transport, overloaded infrastructures, a default logarithmic expansion of motorised means of transport, a vast rise in air and noise pollution and CO2 emissions, a concomitant parking capacity problem and increasing disparity in the social equity standards between communities of very near proximity. What should the Victorian Government do? The attached report assesses the opportunity for Free Floating Car Sharing in Zero Emission urban transport. This report concludes that Free Floating Car Sharing is an innovative technology with a smart operating model that improves cities. It offers cities a no-cost, scaleable transport alternative to supplement existing transport systems and reduce inner urban vehicle congestion. Moreover, Free Floating Car Sharing offers Melbourne’s best opportunity for a definitive, practical and evolutionary pathway into a sustainable Zero Emission urban mobility future through the accelerated uptake of Electric Vehicles. Quickar Pty Ltd (ABN 99 611 879 513) Melbourne, 3000 Victoria, Australia Page 1 of 66 In light of these conclusions, the Victorian Government should: • Enable Free Floating Car Sharing. -

Plattformbasiertes Sharing Und Pooling Im Verkehrssektor – Ein Systematisierungsansatz

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Viergutz, Kathrin et al. Article Plattformbasiertes Sharing und Pooling im Verkehrssektor – ein Systematisierungsansatz Wirtschaftsdienst Suggested Citation: Viergutz, Kathrin et al. (2020) : Plattformbasiertes Sharing und Pooling im Verkehrssektor – ein Systematisierungsansatz, Wirtschaftsdienst, ISSN 1613-978X, Springer, Heidelberg, Vol. 100, Iss. 2, pp. 117-123, http://dx.doi.org/10.1007/s10273-020-2581-y This Version is available at: http://hdl.handle.net/10419/215584 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), -

Ischannel Volume 12 Online

iS CHANNEL Closed Platforms Open Doors: Deriving Strategic Im- plications from the Free-Floating Car Sharing Platform DriveNow Curtis Goldsby MSc in Information Systems and Digital Innovation Department of Management London School of Economics and Political Science KEYWORDS ABSTRACT Open platforms This paper examines the free-floating car-sharing company DriveNow, Closed platforms governed by a joint venture of BMW Group and Sixt SE. The platform-mediated network model is used to determine DriveNow is a closed platform. Relating Drivenow this to adoption/appropriability characteristics, I show how the closed nature Car-sharing of the platform strategically affects DriveNow. Business strategy It is concluded that DriveNow, although closed, can pursue at least three Platform strategy successful platform strategies, but struggles capitalizing on multi-sided network effects. The paper thus shows how a closed platform born through traditional ventures, despite growth bottlenecks, also has the potential to disrupt industries. 1. Introduction a closed platform that does not yet fully capitalize on open multi-sided network effects. Digital platforms are radically transforming every industry today (de Reuver, Sørensen, & Basole, 2017). The relevance of exploring digital platforms and The competitive edge and profit growth achieved researching them in the IS field has been recently through digital platforms indicate why so many emphasized by de Reuver, Sørensen, & Basole (2017). firms are including the power of platforms into their The challenges highlighted by the researchers stem existing business strategies (Parker, Van Alstyne, & from the exponentially growing scale of platform Choudary, 2016). For some “born-digital” companies innovation, increasing complexity of architectures like Microsoft and Amazon, this inclusion of and and the spread of digital platforms to many industries diversification through platforms is easier than for (de Reuver, Sørensen, & Basole, 2017).