Georgia Modal Profile Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jasper Ocean Terminal Project Update

December 2020 December 2020 Environmental Impact Statement Project Update Introduction The U.S. Army Corps of Engineers Charleston District is preparing an Environmental Impact Statement to assess the potential impacts associated with the construction and operation of a new marine container terminal on the Savannah River by the Jasper Ocean Terminal Joint Venture, a partnership between the Georgia Ports Authority IN THIS ISSUE and the South Carolina Ports Authority. The JOT marine container terminal would be constructed on an approximately 1,500-acre site (an existing Dredged Material Containment Area) on the north bank of the Savannah River in Jasper County, South Carolina across the Savannah River from Elba Island in Chatham County, Georgia. Introduction ..................................1 The JOT would be a state-of-the-art marine container terminal to transfer containerized JOT Project Map .......................... 2 cargo between container ships, over-the-road trucks, and intermodal rail cars. The proposed JOT is required for the GPA and the SCPA to meet the current forecasted demand for additional containerized cargo for the Port of Savannah and the Port of Work Accomplished to Date Charleston through the Design Year 2055. for EIS ............................................ 3 Elements of the proposed JOT project would include: What’s New with JOT? ............... 3 Terminal Site Road & Rail Access Corridor Current Related Activities in • 12,500-foot long pile supported wharf • 4-lane divided highway to connect and a 210-foot wide -

Freight and Intermodal Transportation

C H A P T E R 5 FREIGHT AND INTERMODAL TRANSPORTATION FREIGHT AND INTERMOD AL TRANSPORTATION A region’s industry and employment characteristics play a large role in the freight composition. Glynn County is largely a service-driven economy. The private sector employs about 76 percent of residents, with manufacturing employing approximately six percent and services employing about 65 percent of Glynn County residents. Federal, state and local government employs about 24 percent of County residents1. As such, the County primarily consumes goods rather than produces them. Existing Freight Conditions In order to create a freight movement profile for Glynn County the Federal Highway Administration Freight Analysis Framework data was compiled to develop an approximate estimate of freight movements. A total of about 816,000 tons were inbound in 2012 valued at approximately $3.0 billion (primarily motorized vehicles from eastern Asia to Los Angeles and nonmetallic minerals from Europe to the Philadelphia, PA area), while outbound totaled approximately 954,000 tons valued at $2.3 billion (primarily motorized vehicles and newsprint/paper to Europe). There were approximately 142 million tons moving regional with an approximate value of over $63 billion. Trucks carried 95 percent of the total 141.9 million tons of freight flowing through the area, while rail carried five percent of the share. Water and intermodal modes carry less than one percent each. The dominance of truck is due to the mode’s flexibility in terms of being able to handle varying shipment sizes and ability to achieve door-to-door delivery virtually anywhere without making any additional mode transfers. -

Using the Port of Jacksonville to Lower Your Cost to Market

® MAKING THE CASE FOR Using the Port of Jacksonville to Lower Your Cost to Market Situated within a day’s drive of 70+ million consumers, America’s logistics center is a place where shippers of all sizes and across all industries come to lower their cost to market and grow their enterprises. PEERLESS CONTENT CREATION JACKSONVILLE PORT AUTHORITY MAKING THE CASE USING THE PORT OF JACKSONVILLE TO LOWER YOUR COST TO MARKET It’s a Fact: Jacksonville is the Logistics Center of America RIVE INTO JACKSONVILLE, FLA., and you’ll probably notice a roadside sign that Dstates, “America’s Logistics Center.” Aptly named, this Florida city is positioned at the nation’s center when it comes to moving shipments from Point A to Point B. “This isn’t just propaganda; it’s a fact,” says Scott Lane, CIO at Jacksonville-based Beaver Street Fisheries, a wholesaler of seafood and meat that sells to mass discounters, grocers, distributors, food service companies, and restaurant chains. “Look at where Jacksonville is on the map, and we’re sitting here between two Class I railroads, three major highway systems, and a port that carries over 1.3 million TEUs of cargo annually.” Peel back JAXPORT’s layers a little further and you’ll find a robust logistics infrastructure that spans all modes of transportation, ocean carriers of all sizes, and third-party logistics (3PL) companies. “When you factor in the many 3PLs that are based here in Jacksonville,” says Lane, “our logistics footprint is clearly expansive.” Wanted: The Right Logistics Hub Many factors are taking a toll on shippers’ bottom lines: international tariffs, global competition, rising freight rates, fluctuating transportation capacity, and the need to fulfill customers’ orders at lightning speed. -

Georgia Ports Authority

gaports.com Gateway To The World Gateway To The World Index American businesses, shipping products to A deepened harbor is important because the “The Port of Savannah plays a key role in delivering on that promise.” — Target 4 destinations across the globe, have chosen the Port of shipping industry is moving to larger vessels. Savannah as a critical gateway in their supply chains. In 2016, the Panama Canal will complete its expansion. In the following pages, industry leaders will detail The new locks will send ships to Savannah that are as “With partners such as the Georgia Ports Authority… we are able to flow product to the size and scope of their operations, and how their much as three times the capacity of ships currently and from the facility… and get to our end customer efficiently.” — Home Depot 6 businesses and the nation’s economic wellbeing would able to transit the Canal. be jeopardized — if not for Savannah’s continued Major manufacturers and retailers look to the “Working directly with Caterpillar, the GPA considers the entire transportation reliable, efficient and cost-effective operation. harbor deepening as an important opportunity to — Caterpillar and logistics chain… to best serve our needs.” 8 Today, the Port of Savannah reaches 44 percent become more competitive at home and abroad. of the American population — roughly 140 million U.S. Army Corps of Engineers studies show that Super people — within a two-day drive. Post-Panamax vessels more efficiently served by “Deepening the Savannah Harbor will allow us to keep our markets that we have It serves as the cargo hub for a region covering a deeper Savannah harbor will lower shipping costs and go out and get others.” — Bell Farms 10 the entire U.S. -

Georgia Ports Authority Year in Review for the Georgia Department of Transportation Board

Georgia Ports Authority Year in review For the Georgia Department of Transportation Board CURTIS J. FOLTZ Executive Director Georgia Ports Authority GPA'S MISSION GEORGIA’S PORTS ARE GATEWAYS TO 136.4 MILLION U.S. CONSUMERS DEVELOP, MAINTAIN AND OPERATE OCEAN AND INLAND RIVER PORTS WITHIN GEORGIA; FOSTER INTERNATIONAL TRADE AND NEW INDUSTRY FOR STATE AND LOCAL COMMUNITIES; PROMOTE GEORGIA'' S AGRICULTURAL, INDUSTRIAL AND NATURAL RESOURCES; AND MAINTAIN THE NATURAL QUALITY OF THE ENVIRONMENT. 2 GEORGIA’S DEEPWATER & INLAND PORTS FASTER TO MARKET. BETTER FOR BUSINESS. PORT OF SAVANNAH Garden City Terminal Ocean Terminal 3 GEORGIA’S DEEPWATER & INLAND PORTS FASTER TO MARKET. BETTER FOR BUSINESS. PORT OF BRUNSWICK Colonel’s Island Terminal East River Terminal & Mayor’s Point Terminal Lanier Docks 4 THE ECONOMIC IMPACT OF GEORGIA’S DEEPWATER PORTS STATEWIDE • 352,146 full & part-time jobs • $66. 9 billion i n sal es • $32.4 billion in gross state product • $18. 5 billion in income • $2.5 billion in state & local taxes Source: Terry College of Business, University of Georgia, FY2011 5 THE ECONOMIC IMPACT OF GEORGIA’S DEEPWATER PORTS ESTIMATED JOBS BY REGIONAL COMMISSION NW Georgia 23, 750 GA Mountains 15,359 Atlanta NE Georgia 156,698 13,500 Central Savannah River Area 18,925 Three Rivers 13,032 Middle GA 14,624 River Valley Heart of Georgia Coastal 9,613 Altamaha Georgia 10,515 55,385 SW Georgia Southern Georgia 9,927 10,821 6 THE ECONOMIC IMPACT OF GEORGIA’S DEEPWATER PORTS NATIONWIDE • $4.5 billion in federal taxes* • 8.1% of U.S. containerized trade** • 10.1% of U.S. -

GLOBAL CONTAINER SERVICES PORT of SAVANNAH January 25, 2019

GLOBAL CONTAINER SERVICES PORT OF SAVANNAH January 25, 2019 Garden City Terminal Services Garden City Terminal Services EC1 East Coast Loop 1 AL2 Atlantic Loop 2 EC2 East Coast Loop 2 AL3 Atlantic Loop 3 EC3 East Coast Loop 3 AL5 Atlantic Loop 5 AUE/TWS Asia-US East Coast Service/Taiwan Strait TAT2/ATE1/Lib Br Transatlantic 2/Atlantic East Coast Express AWE2/NUE2/Man Br All Water Express 2/North Asia-US East Coast 2 TA2/NEUATL2 Transatlantic 2/North Europe Atlantic Service 2 AWE4/NUE/Vespucci All Water Express 4/North Asia-US East Coast Service TA4/NEUATL4 Transatlantic 4/North Europe Atlantic Service 4 AWE5/SAX All Water Express 5/South Atlantic Express RTW PAD Round the World Panama Direct ZCP/TP10/Amberjack ZIM Container Service Pacific/Transpacific 10/Amberjack TAT1/Amerigo/AL6 Transatlantic 1/Amerigo/Atlantic Loop 6 TP16/Emerald/ZSA Transpacific 16/Emerald/ZIM Sunny Atlantic Express TA5/MEDUSEC Transatlantic 5/Mediterranean US Service EC4 East Coast Loop 4 ZCA/AL7 ZIM Container Service Atlantic/Atlantic Loop 7 EC5 East Coast Loop 5 Turkon Turkon US Line AWE3/CJX/SEAP/PE1 All Water Express 3/Columbus Pendulum NAE/ACX North Atlantic Express/Atlantic Caribbean Express INDAMEX India America Express SAE South Atlantic Express Indus Express Indus Express Cagema Cagema Main Liner MECL Middle East Colombo Service MSC ECSA East Coast South America String 1 TP11/Elephant/ZNF Transpacific 11/Elephant/ZIM New Frontier MSC Can Gulf Br MSC Canada Gulf Bridge TP17/America/Z7S Transpacific 17/America/ZIM Seven Star Express EC1 THE- HAPAG LLOYD, -

Profiles of Top U.S. Agricultural Ports

Agricultural Marketing le, WA tt Service a Profiles of Top U.S. e S Tacom September 2013 a , W A Agricultural Ports a, WA m York, N la ew Y a anco N K V uv e r , W A e ilad lph h ia P , P P R A o O O rtland, ak land, CA ston, ou TX H A , V ve No olk al sto rf G n L , o A s C T , X Angeles A S G a , va ah L nn o A n C g h, Beac J a L c F C , k le o so il nv L r X p T F u i, , s t s C is B X hr e e T P a , o d u nt r la mo t Everg N e LA w , M Orleans L iami, F he agricultural community uses the ocean Top 20 U.S. Ports Moving Waterborne Agricultural Trade, 2011 transportation network extensively to serve its global customers. In calendar year 2011, 80 percent Imports Exports Total T Rank U.S. Ports State Share of U.S. agricultural exports (146.5 million metric tons), Metric Tons and 78 percent of imports (40.7 million metric tons) were waterborne (Census Bureau, U.S. Department of 1 New Orleans Port Region* LA 1,905,984 59,716,467 61,622,450 33% Commerce, and PIERS). The following Agricultural Port 2 Los Angeles CA 2,725,490 7,666,611 10,392,101 6% Profiles provide a view of the top 20 U.S. -

Garden City Terminal at the Port of Savannah

2.0 GARDEN CITY TERMINAL The Garden City Terminal is the main container to and from inland distributors, stores, and processors. shipping terminal at the Port of Savannah, Georgia, As such, the port is an integral economic component and it is one of the largest and fastest growing of several scales: locally, it supports many households container shipping terminals in the Southeastern in and around Chatham County; regionally, the port United States. The terminal allows retail suppliers such supports wider distribution networks and regional as Home Depot, IKEA, and Target to bring overseas agriculture and manufacturing; and the port serves as merchandise to American consumers from all over the a gateway to global markets. world. Simultaneously, the terminal supports an even higher volume of exports by weight to Europe and other The Terminal has grown tremendously to become an destinations, supporting numerous agricultural and economic powerhouse, but its location on the water to manufacturing jobs in the southeastern United States. be accessible to ocean-going ships makes it potentially However, the port’s economic links are not just related vulnerable to the sea level rise. Sea levels are projected to the consumers and producers whose goods transit to rise by approximately three feet over the next 100 through it; the port also supports several thousand years. While the rise will not inundate the port, it will jobs onsite and many more jobs in the surrounding decrease the dock heights relative to the water and warehouses and distribution networks that carry freight may increase vulnerability to flooding under severe 9 storms, salt water damage, or decreased efficiency. -

Appalachian Regional Port

Appalachian Regional Port Kentucky CONNECTING Northwest Georgia to the World Tennesee North Carolina H Appalachian Regional Port South Carolina Alabama H Port of Savannah Georgia • CSX Transportation, Class I Rail Provider • Import, Export and Domestic Cargo • Cost-effective Geographic Advantage • Serves Fastest-growing Region in the U.S. Florida How tomorrow moves ™ Bill Barrs Regional Sales Manager [email protected] • (912) 658-1541 Mark Troughton Global Accounts Executive [email protected] • (912) 964-3958 V.July-2015 gaports.com APPALACHIAN REGIONAL PORT Georgia Ports Authority GPA and CSX Move Cargo More Efficiently he Appalachian Regional Port is a joint effort of Governor Nathan Deal’s office and the State of Georgia, Murray County, CSX and the Georgia Ports T Authority. This transportation asset will provide a powerful new gateway to the Port of Savannah, the second busiest port on the East Coast. • The Appalachian Regional Port, • The inland port sits on 42 acres in through CSX, will provide a direct, Northwest Georgia’s Murray County. 388-mile rail route to the Georgia The site features easy access to A FOR Ports Authority’s Garden City Interstate 75 and U.S. 411, as well Better Option Terminal. It will create and expand as direct rail service to Savannah. Northwest Georgia, Alabama, Tennessee and Kentucky international markets for regional businesses. • The state of Georgia, GPA, Murray Graphic rendering of future Appalachian Regional Port County and CSX Transportation • The inland port offers an efficient recently signed a Memorandum option to an all-truck dray to the of Agreement, creating a partnership deepwater Port of Savannah for which will provide cost savings, traffic target markets in Georgia, Alabama, mitigation, and additional operational DIRECT Rail Route to the Tennessee and Kentucky. -

GEORGIA PORTS the Southeast Gateway for the U.S

GEORGIA PORTS The Southeast Gateway for the U.S. Griff Lynch Chief Executive Officer May 23, 2018 OUR MISSION To empower entrepreneurs, strengthen industries, sustain communities and fortify families by relentlessly striving to accelerate global commerce. GEORGIA PORTS AUTHORITY MORE DEEPWATER & INLAND TERMINAL OPTIONS • Chatsworth Garden City Terminal Ocean Terminal Appalachian Regional Port Colonel’s Island Terminal East River Mayor’s Point Terminal Terminal/Lanier Docks GPA: AN ECONOMIC ENGINE STATE OF GEORGIA: • +439,000 full- and part-time jobs • $106 billion in sales (11% of total sales) • $44 billion in state GDP (8% of total GDP) • $25 billion in income (6% of total personal income) NATIONWIDE: • $4.5 billion in federal taxes • 8.5% of U.S. containerized trade** • 10% of U.S. containerized exports** • 19% of U.S. East Coast containerized trade** Source: *Terry College of Business, University of Georgia (FY2017) **U.S. Census Bureau– based on tonnage (CY2017) Chatham ICTF served by CSX Transportation Mason ICTF served by Norfolk Southern Railroad GARDEN CITY TERMINAL TODAY LARGEST SINGLE TERMINAL IN NORTH AMERICA • 9 Container berths • 30 Container cranes • 9,693 ft (2,955 m) of contiguous • 146 Rubber-tired gantries berthing space • 1,200 acres (485.6 ha) terminal area CY2017 (JANUARY - DECEMBER) HIGHLIGHTS • CY2017 Container Volume +11.0% . 4,046,212 TEUs +401,693 TEUs . Laden Imports +12.3% . Laden Exports +7.7% . Empties +14.1% • Total Container Tonnage- 30M +12.9% • Gate Moves- 2.7M +8.9% • Average Turn times 33/54 Minutes -

Expansion Underway

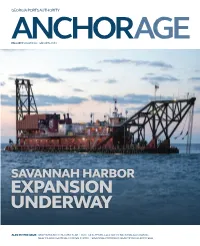

GEORGIA PORTS AUTHORITY ANCHORFALL 2015 VOLUME 68 | GAPORTS.COM AGE SAVANNAH HARBOR EXPANSION UNDERWAY ALSO IN THIS ISSUE: GPA MARKS SIXTH RECORD YEAR | SCOTT & SEYMORE ELECTED TO NATIONAL ILA COUNCIL NEW INLAND TERMINAL TO OPEN IN 2018 | SAVANNAH MOVING CITRUS IMPORTS FROM PERU SAVE THE DATE 48TH ANNUAL GEORGIA FOREIGN GFTC2016 TRADE CONFERENCE February 7-9, 2016 · The Cloister · Sea Island, Georgia Visit gaforeigntrade.com for current information and conference updates. Media Sponsors include: © 2013-2015 Georgia Foreign Trade Conference and the Georgia Ports Authority. All rights reserved. 15GA01792_GFTC_AnchorAge.indd 1 3/2/15 11:52 AM CONTENTS ABOUT THE COVER: Dredging for the Savannah Harbor Expansion began Sept. 10. Cover photo by Stephen B. Morton. ANCHORAGE ROBERT C. MORRIS Editor EDWARD FULFORD Managing Editor EMILY GOLDMAN 10 Associate Editor JULIE KAUFMAN DEBBIE RHODES Copy Editors DEBBIE RHODES Advertising Associate The Georgia Ports Authority ANCHORAGE is Photo by Stephen B. Morton published quarterly and distributed free of Savannah Harbor Expansion Underway charge to more than 9,000 readers worldwide. This publication is not copyrighted and BUSINESS BRIEFS permission is given for the reproduction or SAVE THE DATE Reefer Express Goes Green ......................................................................6 use of any original material, provided GPA’s Corporate Communications Office is contacted. Kia Motors Earns Best Ever Ranking ......................................................6 Port Logistics Group Enters Savannah -

Section 1 Caribbean Encounters

Section 1 Caribbean Encounters ∵ Wim Klooster - 9789004271319 Downloaded from Brill.com09/28/2021 03:32:00PM via free access <UN> Wim Klooster - 9789004271319 Downloaded from Brill.com09/28/2021 03:32:00PM via free access Curaçao as a Transit Center to the Spanish Main and the French West Indies Wim Klooster An official Dutch government report described Curaçao in the late eighteenth century as “the only safe port that the state has in the West Indies, one in which more than 300 ships of the largest size can be sheltered and where they are shielded against the force of wind and sea, where all the ships can be keel- hauled and recover from sustained damage, where a defeated fleet or mer- chantmen coming from our colonies can always flee because of its leeward location…”1 Ideal for shipping traffic, the island had long since been an impor- tant regional market, described by a contemporary author as a “small paradise of earthly abundance.”2 The aim of this chapter is to review the island’s com- mercial heyday, its connections with the Republic, its place in Caribbean trade networks, and the concomitant mobility of its populations. Captured from Habsburg Spain during the last stages of the Dutch Revolt, Curaçao did not immediately become a center of commercial activity. It began its life under Dutch rule as a naval base. Although some military raids were launched from the island to inflict damage on settlements on the Venezuelan coast, Curaçao did not play a key role in the Atlantic theater of the war with Spain.