Brahmagupta E Alguns Elementos Históricos Da Matemática Hindu

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Study on the Contributions of Indian

ISSN: 2456–4397 RNI No.UPBIL/2016/68067 Vol-5* Issue-8* November-2020 Anthology : The Research A Study on the Contributions of Indian Mathematicians in Modern Period Paper Submission: 16/11/2020, Date of Acceptance: 26/11/2020, Date of Publication: 27/11/2020 Abstract The purpose of this paper is to provide an overview of the contributions of Indian mathematicians to a claim about a Diophantine equation in modern times. Vedic literature has contributed to Indian mathematics. About 1000 B.C. and the year 1800 A.D. For the first time, Indian mathematicians have drawn up various mathematics treaties, defining zero, the numeral method, the methods of arithmetic and algorithm, the square root, and the cube root. Although, there is a distinct contribution from the sub-continent during readily available, reliable information. Keywords: Number theory, Diophantine equation, Indian Mathematicians, Shakuntala Devi, and Manjul Bhargava. Introduction The history of mathematics shows the great works, including the mathematical contents of the Vedas, of ancient Indian mathematicians.India seems to have in the history of mathematics, an important contribution to the simplification of inventions.[1] In addition to the Indians, the entire world is proud that ancient India has made great mathematical accomplishments. Thus, without the history of ancient Indian mathematics, the history of mathematics cannot be completed.In the early Ajeet kumar Singh stages, two major traditions emerged in mathematics (i) Arithmetical and Research Scholar, algebraic (ii) geometric (the invention of the functions of sine and cosine). Dept. of Mathematics, The position ofthe decimal number system was its most significant and Himalayan University, most influential contribution. -

MANALI PETROCHEMICALS LIMITED CIN : L24294TN1986PLC013087 Regd Off: 'SPIC HOUSE', 88, Mount Road, Guindy, Chennai- 600 032

MANALI PETROCHEMICALS LIMITED CIN : L24294TN1986PLC013087 Regd Off: 'SPIC HOUSE', 88, Mount Road, Guindy, Chennai- 600 032. Tele-Fax No.: 044-22351098 Email: [email protected], Website: www.manalipetro.com DETAILS OF SHARES TO BE TRANSFERRED TO INVESTOR EDUCATION & PROTECTION FUND ON WHICH NO DIVIDEND HAS BEEN CLAIMED FOR THE FY 2008-09 TO 2015-16 SL.NO FOLIO_DP_ID_CL_ID NAME OF THE SHAREHOLDER NO.OF.SHARES TOBE TRFD TO IEPF 1 A0000033 SITARAMAN G 450 2 A0000089 LAKSHMANAN CHELLADURAI 300 3 A0000093 MANI N V S 150 4 A0000101 KUNNATH NARAYANAN SUBRAMANIAN 300 5 A0000120 GOPAL THACHAT MURALIDHAR 300 6 A0000130 ROY FESTUS 150 7 A0000140 SATHYAMURTHY N 300 8 A0000142 MOHAN RAO V 150 9 A0000170 MURALIDHARAN M R 300 10 A0000171 CHANDRASEKAR V 150 11 A0000187 VISWANATH J 300 12 A0000191 JAGMOHAN SINGH BIST 300 13 A0000213 MURUGANANDAN RAMACHANDRAN 150 14 A0000219 SHANMUGAM E 600 15 A0000232 VENKATRAMAN N 150 16 A0000235 KHADER HUSSAINY S M 150 17 A0000325 PARAMJEET SINGH BINDRA 300 18 A0000332 SELVARAJU G 300 19 A0000334 RAJA VAIDYANATHAN R 300 20 A0000339 PONNUSWAMY SAMPANGIRAM 300 21 A0000356 GANESH MAHADHEVAN 150 22 A0000381 MEENAKSHI SUNDARAM K 150 23 A0000389 CHINNIAH A 150 24 A0000392 PERUMAL K 300 25 A0000423 CHANDRASEKARAN C 300 26 A0000450 RAMAMOORTHY NAIDU MADUPURI 150 27 A0000473 ZULFIKAR ALI SULTAN MOHAMMAD 300 28 A0000550 SRINIVASAN K 150 29 A0000556 KANAKAMUTHU A 300 30 A0000561 KODANDA PANI CHIVUKULA 300 31 A0000565 VARADHAN R 150 32 A0000566 KARTHIGEYAN S 150 33 A0000598 RAMASASTRULU TRIPIRNENI 150 34 A0000620 -

The Indian Tradition in Science and Technology: an Overview

The Indian Tradition in Science and Technology: An Overview Dr. M.D. Srinivas & Dr. J.K. Bajaj Any study of the Indian tradition of science has to start with linguistics. Not only linguistics is the earliest of Indian sciences to have been rigorously systematised, but also this systematisation became the paradigm example for all other sciences. Like all sciences and arts of India, Linguistics finds its first expression in the Vedas. For most of the Indian sciences, the elements of study and the categories of analysis were established in the Vaidika period, and the basic data was collected and preliminary systematisation achieved already at that stage. Thus, for the science of Linguistics, we find, in the siksha and pratisakhya texts associated with the various Vedas, a complete and settled list of phonemes appropriately classified into vowels, semi-vowels, sibilants and the five groups of five consonants, all arranged according to the place of articulation that moves systematically from the throat to the lips. Phonetics and phonology are therefore taken for granted by all post-Vaidika authorities on etymology (nirukta) and grammar (vyakarana), including Yaska and Panini. In the pratisakhya literature we also find the morpho-phonemic (sandhi) rules and much of the methodology basic to the later grammatical literature. Indian Linguistics finds its rigorous systematisation in Panini’s Ashtadhyayi. The date of this text, like that of much of the early Indian literature, is yet to be settled with certainty. But it is not later than 500 BC. In Ashtadhyayi, Panini achieves a complete characterisation of the Sanskrit language as spoken at his time, and also specifies the way it deviated from the Sanskrit of the Vedas. -

The Methodology of Indian Mathematics and Its Contemporary Relevance

THE METHODOLOGY OF INDIAN MATHEMATICS AND ITS CONTEMPORARY RELEVANCE Abstract : While considerable attention has been paid to the achievements of Indian mathematicians, by cataloguing the results and processes discovered by them, very little work seems to have been done on the methodological foundations of Indian mathematics, its under- standing of the nature of mathematical objects, the nature of mathematical knowledge and the methods of validation of mathematical results and processes. Traditionally such issues have been dealt with mainly in the so called 'commentarial literature' which (though it formed an important component in traditional learning) has been completely ignored by modern scholarship. An attempt is made in this paper to present a preliminary view of the methodology of Indian mathematics as may be gathered from the major commentarial works, the commentary Buddhivilasini of Ganesha Daivajna (c 1545) on Bhaskaracharya's Lilavati (c 1150) and the commentary Bijanavankura of Krishna Daivajna (c 1601) on Bhaskaracharya's Bijaganita (c 1150). While these commentaries provide a general exposition of many basic aspects of Indian mathematics, their main emphasis is in presenting what they refer to as upapatti (roughly translatable as demonstration, proof) for every result and process enunciated in the original texts of Bhaskaracharya. We present a few examples of such upapattis including a long demonstration (involving a series of demonstrations of many intermediate results) of the so called kuttaka process for the solution of first order indeterminate equations. As we see, one main feature of the Indian upapattis as contrasted with the Greek or the modern Western notion of 'proof is that the former does not involve any reference to formal deductions performable from some fixed set of axioms. -

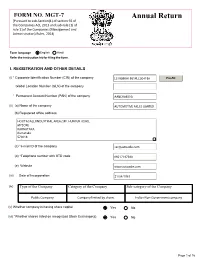

Annual Return [Pursuant to Sub-Section(1) of Section 92 of the Companies Act, 2013 and Sub-Rule (1) of Rule 11Of the Companies (Management And

FORM NO. MGT-7 Annual Return [Pursuant to sub-Section(1) of section 92 of the Companies Act, 2013 and sub-rule (1) of rule 11of the Companies (Management and Administration) Rules, 2014] Form language English Hindi Refer the instruction kit for filing the form. I. REGISTRATION AND OTHER DETAILS (i) * Corporate Identification Number (CIN) of the company Pre-fill Global Location Number (GLN) of the company * Permanent Account Number (PAN) of the company (ii) (a) Name of the company (b) Registered office address (c) *e-mail ID of the company (d) *Telephone number with STD code (e) Website (iii) Date of Incorporation (iv) Type of the Company Category of the Company Sub-category of the Company (v) Whether company is having share capital Yes No (vi) *Whether shares listed on recognized Stock Exchange(s) Yes No Page 1 of 16 (a) Details of stock exchanges where shares are listed S. No. Stock Exchange Name Code 1 2 (b) CIN of the Registrar and Transfer Agent Pre-fill Name of the Registrar and Transfer Agent Registered office address of the Registrar and Transfer Agents (vii) *Financial year From date 01/04/2020 (DD/MM/YYYY) To date 31/03/2021 (DD/MM/YYYY) (viii) *Whether Annual general meeting (AGM) held Yes No (a) If yes, date of AGM (b) Due date of AGM 30/09/2021 (c) Whether any extension for AGM granted Yes No II. PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY *Number of business activities 1 S.No Main Description of Main Activity group Business Description of Business Activity % of turnover Activity Activity of the group code Code company C C11 III. -

First Name Middlena Me Last Name Father/Husban D First Name Father

First Name MiddleNa Last Father/Husban Father/Hus Father/Hu Address Country State District Pincode Folop Number of Investment Type Amount Proposed Date me Name d First Name band sband Last Securities of Transfer to MiddleNa Name IEPF me A C BAJAJ NA 7-B DEEP JYOTI CO-OP,HSG, SOCIETY 209, ESTERN INDIA MAHARASHTR 401105 DEWA000000000 Amount for 10.50 21-Sep-2013 EXPRESS HIGHWAY, BHAYANDAR (EAST), THANE A A001503 unclaimed and unpaid dividend A M A R C/O A R MAHENDRAN NO.8 EAST IYEN STREET, INDIA TAMIL NADU 612001 DEWA000000000 Amount for 150.00 21-Sep-2013 KRISHNAKUMA MAHENDRAN KUMBARONAM A002422 unclaimed and R unpaid dividend A M A R C/O A R MAHENDRAN 18,TAGORE STREET, INDIA TAMIL NADU 609001 DEWA000000000 Amount for 150.00 21-Sep-2013 RAMKUMAR MAHENDRA MAYILADUTHURAI TAMIL NADU A002423 unclaimed and unpaid dividend A NA 32 22 4TH CROSS ROAD GANDHI NAGAR VELLORE INDIA TAMIL NADU 632004 DEWAIN3002141 Amount for 223.50 21-Sep-2013 MADHUSUDHA TAMILNADU 1625155 unclaimed and N CHOUDARY unpaid dividend A P NAYYAR D R NAYYAR C - 4 NARAYANA VIHAR NEW DELHI INDIA DELHI 110028 DEWAIN3005891 Amount for 75.00 21-Sep-2013 0118313 unclaimed and unpaid dividend A R NA NO.8, EAST IYEN STREET KUMBAKONAM INDIA TAMIL NADU 612001 DEWA000000000 Amount for 154.50 21-Sep-2013 MAHENDRAN A000009 unclaimed and unpaid dividend A RAMADEVI NA PLOT NO 37 BALAJI NAGAR RAM NAGAR GUNDU INDIA ANDHRA 500044 DEWAIN3030285 Amount for 75.00 21-Sep-2013 HYDERABAD PRADESH 0043622 unclaimed and unpaid dividend A SRIKANT A NARAYANA C/O.P.RASHORAM 302, GOLDEN TOWERS STREET INDIA -

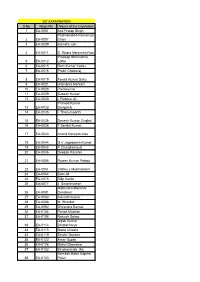

1ST EXAMINATION S No Regn No Name of the Candidate 1 EA-0001 Atul Pratap Singh Padmanabha Ramanuja 2 EA-0007 Chari 3 EA-0009 Jitendra Jain

1ST EXAMINATION S No Regn No Name of the Candidate 1 EA-0001 Atul Pratap Singh Padmanabha Ramanuja 2 EA-0007 Chari 3 EA-0009 Jitendra Jain 4 EA-0011 G Rudra Narsimha Rao Pradeep Shrikrishna 5 EA-0012 Lothe 6 EA-0015 Ram Kumar Yadav 7 EA-0016 Prabir Chattoraj 8 EA-0019 Aswini Kumar Sahu 9 EA-0021 Hitendera Mehtani 10 EA-0028 Premkumar 11 EA-0029 Subesh Kumar 12 EA-0030 L Rafique Ali Pramod Kumar 13 EA-0032 Dangaich 14 EA-0035 I Thanumoorthi 15 EA-0036 Devesh Kumar Singhal 16 EA-0038 T Senthil Kumar 17 EA-0043 Anand Narayan Kale 18 EA-0044 G V Jagadeesh Kumar 19 EA-0045 P Chandramouli 20 EA-0046 Deepak Kaushik 21 EA-0055 Rajeev Kumar Pahwa 22 EA-0061 Vishnu J Mulchandani 23 EA-0064 Babu M 24 EA-0075 Dilip Sarda 25 EA-0077 J Swaminathan Mahendra Manohar 26 EA-0081 Dandekar 27 EA-0083 Avinash Kumar 28 EA-0086 M Bhaskar 29 EA-0092 Dhirendra Bansal 30 EA-0104 Pande Madhav 31 EA-0108 Rakesh Sahay Dipak Kumar 32 EA-0114 Bhattacharya 33 EA-0115 Manu Chawla 34 EA-0119 Shishir Saxena 35 EA-0122 Amar Gupta 36 EA-0128 Mukul Ghanekar 37 EA-0132 Binobananda Jha Ramesh Babu Guptha 38 EA-0133 Paluri 39 EA-0136 Sukuru Ramarao Sanjay Bhanudasrao 40 EA-0142 Joshi 41 EA-0148 Mahesh Kumar Madan 42 EA-0149 Swapan Kumar Dutta 43 EA-0155 Desai Gaurang 44 EA-0157 Raj Kumar Porwal 45 EA-0159 Devanand Patil 46 EA-0160 Achyuta Nanda Mohanty 47 EA-0178 Mahesh Chandani 48 EA-0179 R K Aggarwal 49 EA-0183 G Pasupathy 50 EA-0184 Sandeep Kumar Jain 51 EA-0185 B D Gupta 52 EA-0187 Mohammad Abul Kalam 53 EA-0191 Arun Kanti Bala 54 EA-0192 G Sankar 55 EA-0200 R Balasubramanian 56 EA-0203 V Kumaran 57 EA-0205 Sarvesh Kumar 58 EA-0207 C Sethuraman 59 EA-0216 Pramath Sanghavi 60 EA-0220 Pawan B Agarwal 61 EA-0223 Subrat Kishore Nayak 62 EA-0232 Upendra Pratap Singh 63 EA-0233 Shailendra Pandey 64 EA-0236 Tukaram K. -

List of Certified Energy Auditors

LIST OF CERTIFIED ENERGY AUDITORS S No Regn No Name of the Candidate IST EXAM - MAY 2004 1 EA-0001 Atul Pratap Singh 2 EA-0007 Padmanabha Ramanuja Chari 3 EA-0009 Jitendra Jain 4 EA-0011 G Rudra Narsimha Rao 5 EA-0012 Pradeep Shrikrishna Lothe 6 EA-0015 Ram Kumar Yadav 7 EA-0016 Prabir Chattoraj 8 EA-0019 Aswini Kumar Sahu 9 EA-0021 Hitendera Mehtani 10 EA-0028 Premkumar 11 EA-0029 Subesh Kumar 12 EA-0030 L Rafique Ali 13 EA-0032 Pramod Kumar Dangaich 14 EA-0035 I Thanumoorthi 15 EA-0036 Devesh Kumar Singhal 16 EA-0038 T Senthil Kumar 17 EA-0043 Anand Narayan Kale 18 EA-0044 G V Jagadeesh Kumar 19 EA-0045 P Chandramouli 20 EA-0046 Deepak Kaushik 21 EA-0055 Rajeev Kumar Pahwa 22 EA-0061 Vishnu J Mulchandani 23 EA-0064 Babu M 24 EA-0075 Dilip Sarda 25 EA-0077 J Swaminathan 26 EA-0081 Mahendra Manohar Dandekar 27 EA-0083 Avinash Kumar 28 EA-0086 M Bhaskar 29 EA-0092 Dhirendra Bansal 30 EA-0104 Pande Madhav 31 EA-0108 Rakesh Sahay 32 EA-0114 Dipak Kumar Bhattacharya 33 EA-0115 Manu Chawla 34 EA-0119 Shishir Saxena 35 EA-0122 Amar Gupta 36 EA-0128 Mukul Ghanekar 37 EA-0132 Binobananda Jha 38 EA-0133 Ramesh Babu Guptha Paluri 39 EA-0136 Sukuru Ramarao 40 EA-0142 Sanjay Bhanudasrao Joshi 41 EA-0148 Mahesh Kumar Madan 42 EA-0149 Swapan Kumar Dutta 43 EA-0155 Desai Gaurang 44 EA-0157 Raj Kumar Porwal 45 EA-0159 Devanand Patil 46 EA-0160 Achyuta Nanda Mohanty 47 EA-0178 Mahesh Chandani 48 EA-0179 R K Aggarwal 49 EA-0183 G Pasupathy 50 EA-0184 Sandeep Kumar Jain 51 EA-0185 B D Gupta 52 EA-0187 Mohammad Abul Kalam 53 EA-0191 Arun Kanti Bala 54 EA-0192 G Sankar 55 EA-0200 R Balasubramanian 56 EA-0203 V Kumaran 57 EA-0205 Sarvesh Kumar 58 EA-0207 C Sethuraman 59 EA-0216 Pramath Sanghavi 60 EA-0220 Pawan B Agarwal 61 EA-0223 Subrat Kishore Nayak 62 EA-0232 Upendra Pratap Singh 63 EA-0233 Shailendra Pandey 64 EA-0236 Tukaram K. -

Mathematics in India: from Vedic Period to Modern Times Prof. M.D. Srinivas Department of Mathematics Indian Institute of Technology – Bombay

Mathematics in India: From Vedic Period to Modern Times Prof. M.D. Srinivas Department of Mathematics Indian Institute of Technology – Bombay Lecture – 39 Mathematics in Modern India 1 So, today we will this first lecture on mathematics in Modern India. There will be two lectures covering the modern period roughly from 1750 to the present time. As you can see it is a long period and a lot of historical records and lot of events have happened, so we will have to focus on important things in this period. (Refer Slide Time: 00:36) So, I will first say something about the way that the indigenous tradition in astronomy and mathematics continued late into 19th-century. We tell you something about the nature of indigenous education system in India in early part of 19th-century before the British started the English education system here and how that system survived of course very limpingly till the later part of 19th century. Then, I will say something about the Modern European scholarship on the Indian tradition of astronomy and mathematics during the two centuries, 18th and 19th centuries and then how Indians themselves participated in this rediscovery of tradition in the latter part of 19th century. Then, of course this new system of education that was started in the middle of 19th century, how did that develop, but the main part of today's lecture, we will look into the life and work of Srinivasa Ramanujan and its impact today. So, till about 50 years ago most modern scholars most textbooks had Indian mathematics died with Bhaskaracharya II around 1150. -

Journey of Indian Mathematics from Vedic Era

ESSENCE—IJERC International | Nidhi Handa Journal (2018) for Envir| IX (1):onmental 217—221 Rehabilitation and Conservation ISSN: 0975 — 6272 IX (1): 217— 221 www.essence—journal.com Original Research Article Journey of Indian Mathematics from Vedic Era Handa, Nidhi Department of Mathematics, Gurukul Kangri Vishwavidyalya, Haridwar, Uttarakhand, India Corresponding Author: [email protected] A R T I C L E I N F O Received: 28 January 2018 | Accepted: 30 April 2018 | Published Online: 15 August 2018 DOI: 10.31786/09756272.18.9.1.127 EOI: 10.11208/essence.18.9.1.127 Article is an Open Access Publication. This work is licensed under Attribution—Non Commercial 4.0 International (https://creativecommons.org/licenses/by/4.0/) ©The Authors (2018). Publishing Rights @ MANU—ICMANU & ESSENCE—IJERC. A B S T R A C T The paper points out how initially proposed theories by European scholars of Mathematics, consider- ing algebra and geometry of Greek and / or Old—Babylonian origin came to be discarded as studies expanded to Vedic works like Shatpath Brahamana and Taittiriya Samhita. K E Y W O R D S Indian Mathematics | Vedic Era | Ancient mathematics C I T A T I O N Handa, Nidhi (2018): Journey of Indian Mathematics from Vedic Era. ESSENCE Int. J. Env. Rehab. Conserv. IX (1): 217—221. https://doi.org/10.31786/09756272.18.9.1.127 https://eoi.citefactor.org/10.11208/essence.18.9.1.127 217 ESSENCE—IJERC | Nidhi Handa (2018) | IX (1): 217—221 Introduction Vedas, the paper presents the following points: Existence of Mathematics before Christ may be referred as foundation of Mathematics. -

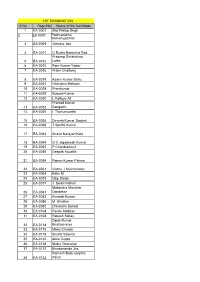

1ST EXAMINATION S No Regn No Name of the Candidate 1 EA-0001 Atul Pratap Singh 2 EA-0007 Padmanabha Ramanujachari 3 EA-0009 Jitendra Jain

1ST EXAMINATION S No Regn No Name of the Candidate 1 EA-0001 Atul Pratap Singh 2 EA-0007 Padmanabha RamanujaChari 3 EA-0009 Jitendra Jain 4 EA-0011 G Rudra Narsimha Rao Pradeep Shrikrishna 5 EA-0012 Lothe 6 EA-0015 Ram Kumar Yadav 7 EA-0016 Prabir Chattoraj 8 EA-0019 Aswini Kumar Sahu 9 EA-0021 Hitendera Mehtani 10 EA-0028 Premkumar 11 EA-0029 Subesh Kumar 12 EA-0030 L Rafique Ali Pramod Kumar 13 EA-0032 Dangaich 14 EA-0035 I Thanumoorthi 15 EA-0036 Devesh Kumar Singhal 16 EA-0038 T Senthil Kumar 17 EA-0043 Anand Narayan Kale 18 EA-0044 G V Jagadeesh Kumar 19 EA-0045 P Chandramouli 20 EA-0046 Deepak Kaushik 21 EA-0055 Rajeev Kumar Pahwa 22 EA-0061 Vishnu J Mulchandani 23 EA-0064 Babu M 24 EA-0075 Dilip Sarda 25 EA-0077 J Swaminathan Mahendra Manohar 26 EA-0081 Dandekar 27 EA-0083 Avinash Kumar 28 EA-0086 M Bhaskar 29 EA-0092 Dhirendra Bansal 30 EA-0104 Pande Madhav 31 EA-0108 Rakesh Sahay Dipak Kumar 32 EA-0114 Bhattacharya 33 EA-0115 Manu Chawla 34 EA-0119 Shishir Saxena 35 EA-0122 Amar Gupta 36 EA-0128 Mukul Ghanekar 37 EA-0132 Binobananda Jha Ramesh Babu Guptha 38 EA-0133 Paluri 39 EA-0136 Sukuru Ramarao Sanjay Bhanudasrao 40 EA-0142 Joshi 41 EA-0148 Mahesh Kumar Madan 42 EA-0149 Swapan Kumar Dutta 43 EA-0155 Desai Gaurang 44 EA-0157 Raj Kumar Porwal 45 EA-0159 Devanand Patil 46 EA-0160 Achyuta Nanda Mohanty 47 EA-0178 Mahesh Chandani 48 EA-0179 R K Aggarwal 49 EA-0183 G Pasupathy 50 EA-0184 Sandeep Kumar Jain 51 EA-0185 B D Gupta 52 EA-0187 Mohammad Abul Kalam 53 EA-0191 Arun Kanti Bala 54 EA-0192 G Sankar 55 EA-0200 R Balasubramanian 56 EA-0203 V Kumaran 57 EA-0205 Sarvesh Kumar 58 EA-0207 C Sethuraman 59 EA-0216 Pramath Sanghavi 60 EA-0220 Pawan B Agarwal 61 EA-0223 Subrat Kishore Nayak 62 EA-0232 Upendra Pratap Singh 63 EA-0233 Shailendra Pandey 64 EA-0236 Tukaram K. -

Trans-Local Mobilities and Spatial Politics of Dance Across/Beyond the Early Modern Coromandel

UNIVERSITY OF CALIFORNIA Los Angeles Performative Geographies: Trans-Local Mobilities and Spatial Politics of Dance Across & Beyond the Early Modern Coromandel A dissertation submitted in partial satisfaction of the requirements for the degree Doctor of Philosophy in Culture and Performance by Pallavi Sriram 2017 Copyright by Pallavi Sriram 2017 ABSTRACT OF DISSERTATION Performative Geographies: Trans-Local Mobilities and Spatial Politics of Dance Across & Beyond the Early Modern Coromandel by Pallavi Sriram Doctor of Philosophy in Culture and Performance University of California, Los Angeles, 2017 Professor Janet M. O’Shea, Chair This dissertation presents a critical examination of dance and multiple movements across the Coromandel in a pivotal period: the long eighteenth century. On the eve of British colonialism, this period was one of profound political and economic shifts; new princely states and ruling elite defined themselves in the wake of Mughal expansion and decline, weakening Nayak states in the south, the emergence of several European trading companies as political stakeholders and a series of fiscal crises. In the midst of this rapidly changing landscape, new performance paradigms emerged defined by hybrid repertoires, focus on structure and contingent relationships to space and place – giving rise to what we understand today as classical south Indian dance. Far from stable or isolated tradition fixed in space and place, I argue that dance as choreographic ii practice, theorization and representation were central to the negotiation of changing geopolitics, urban milieus and individual mobility. This study traces change through intersecting movement of people, ideas and repertoires anchored in specific new and changing urban milieus; developing the concept of performative geographies It unpacks the ways in which multiple stakeholders, themselves often on the move, drew from diverse milieus (performative, geopolitical, temporal and social), connecting through the subcontinent and across the Bay of Bengal.