Gatehouse-Gannett Merger Threatens Journalism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Kansas Publisher Official Monthly Publication of the Kansas Press Association June 8, 2011

The Kansas Publisher Official monthly publication of the Kansas Press Association June 8, 2011 Inside Today Page 2 Kevin Slimp says a new website tool is affordable for smaller newspapers. Page 3 Jim Purmarlo has some advice for newspapers on their busi- ness coverage. Page 4 KPA president Patrick Lowry says Joplin tornado underscored the importance of what newspa- pers do for their communities. Page 6 A 16-part newspaper serial story will be available to KPA newspapers this fall. On their trek to the concert area, Symphony in the Flint Hills attendees in 2010 take a break to talk Page 8 with two outriders, whose task was to keep the attendees and the cattle in the pasture safe. NNA research projects cover a wide range of newspaper Flint Hills Symphony project: Part II subjects. University will provide free access to stories, Page 8 Concert content available photographs and videos for use in Kansas news- He may sound like a broken n just a few short years, the Symphony in the papers for the second consecutive year. record, but Doug Anstaett con- Flint Hills has become a marquee event for The material will be available for use in tinues to harp on the importance Ithe state of Kansas. newspapers soon after the event. of uploading digital PDFs. The sixth annual concert is set for Saturday To download stories, photos and videos for (June 11), this time in the Fix Pasture near Vol- your newspaper, go to: http://www.fl inthillsme- land, Kan. in Wabaunsee County. diaproject.com/?page_id=220 KPA Calendar The event celebrates the native grassland The only request is that if you use content, prairie of Kansas, which has remained virtually please send two copies of the work to Anderson, July 20 undisturbed for centuries. -

GHMNE Weekly Ad Rates

S E T A R G N I S I Y L T R K E E V E D W A effective august 29, 2011 GateHouse Media New England Targeted Coverage. Broad Reach. Unique Content. GateHouse Media offers advertisers a powerful way to target consumers in Eastern Massachusetts. With a network of more than 100 newspapers, we deliver the strongest coverage of key demographic groups in the desirable communities around Boston. Whether it’s dailies or weeklies, single paper buys or whole market coverage, print or online, GateHouse can deliver a high impact, cost effective advertising solution to meet your marketing needs. GateHouse Media is one of the largest publishers of locally based print and online media in the United States. The company offers a portfolio of products that includes nearly 500 community publications and more than 250 websites, and seven yellow page directories, serves over 233,000 business advertising accounts and reaches approximately 10 million people a week in 18 states. Weekly Market Coverage There’s a better way to buy Boston — GateHouse Media New England Amesbury Merrimac Salisbury Newburyport West Haverhill Newbury Newbury eland Grov Methuen Georgetown Rowley ce n re w Dracut La Boxford h Ipswich t Dunstable r ug North Pepperell ro o Townsend o Andover p sb k ng Andover c Ty o Lowell R Topsfield Essex Hamilton Gloucester Groton Tewksbury Middleton Wenham Lunenburg Westford Chelmsford North n Manchester to Reading g Danvers Beverly Shirley Ayer Billerica in lm L i y n W n Littleton Carlisle Reading f Peabody Leominster ie ld Har vard ton Wakefield Salem -

Welcome Kit Discover the Benefits of Being a Subscriber Detroit Free Press Dear Subscriber, We Know You Have Many Choices These Days for News 160 W

Welcome Kit Discover the benefits of being a subscriber Detroit Free Press Dear Subscriber, We know you have many choices these days for news 160 W. Fort Street coverage, both locally and nationally, and supporting Detroit, MI 48226 a free press has never been more critical. That’s why I PART OF THE USA TODAY NETWORK want to thank you for your support of Detroit Free Press, ensuring we can continue crafting stories that impact the community and the world at large. For more than 175 years, the Detroit Free Press has been serving readers in South East Michigan, delivering stories that affect, inform and inspire you. And this is only the beginning of the benefits you receive as a subscriber of Detroit Free Press. Your subscription includes unlimited access to freep.com and our mobile apps with breaking news and personalized news alerts, exclusive newsletters tailored to your interests and more exciting perks. This welcome kit includes helpful and important information about your subscription. You can also view this information online at help.freep.com. Thank you for supporting Detroit Free Press. Sincerely, Peter Bhatia Editor Table of Contents 4 GETTING STARTED 5 RESOURCES & CONTACT INFORMATION 6 COMMUNITY IMPACT 7 SUBSCRIBER BENEFITS Newsletters Get exclusive newsletters and the latest news with Daily Briefing and more topics. Podcasts Listen to award-winning podcasts from Detroit Free Press and across the network. Social Media Follow us on social media for even more news coverage. e-Edition Access the digital copy of the newspaper on any device. Bonus Subscription Give one digital subscription to a family member or friend, for free! 8 Mobile Apps Stay on the pulse with our suite of mobile apps. -

E.W. Scripps Company Expects Newspaper Spinoff to Retain Tax-Free Status in Journal Media Group Acquisition

E.W. Scripps Company expects newspaper spinoff to retain tax-free status in Journal Media Group acquisition For immediate release Oct. 7, 2015 CINCINNATI – The E.W. Scripps Company (NYSE: SSP) expects the spinoff and merger of its newspaper operations with those of Journal Communications to remain tax free for Scripps and its shareholders if Journal Media Group (NYSE: JMG) is acquired by Gannett Company (NYSE: GCI). Gannett announced plans for the acquisition today. On April 1, Scripps and Journal Communications simultaneously spun off and merged their newspaper operations to form Journal Media Group in a transaction that was tax free for Scripps and its shareholders. At the time of this deal, Scripps and Journal Communications entered into a Tax Matters Agreement to address Scripps’ and Journal Media Group’s rights and obligations with respect to a number of matters, including any sale of Journal Media Group before the second anniversary of the closing of the deal. Under that agreement, Journal Media Group is required to provide Scripps with an unqualified opinion of tax counsel confirming that the tax-free status of the spin-off of Scripps newspapers will be preserved in the event of a sale of Journal Media Group. Scripps has received this tax opinion, which concludes that the sale of Journal Media Group will not result in the prior Scripps spinoff becoming taxable to Scripps or its shareholders. About Scripps The E.W. Scripps Company serves audiences and businesses through a growing portfolio of television, radio and digital media brands. Scripps is one of the nation’s largest independent TV station owners, with 33 television stations in 24 markets and a reach of nearly one in five U.S. -

Topix Chillicothe Mo Forum

Topix chillicothe mo forum Continue A city in Missouri, United States.No registration or entry is required. Start the discussion now, share on social media, attract more people and see what they really think! Start a new theme: Start a new Chillicothe topix theme. Chillicothe tlkoi chil e koth ee is a city in Ross County, Ohio. An alternative to replacing Topix craigslist. I will also miss the topix index, which is how you could tell how crappy the city was, how active users were on that city topix. Chillicothe topix has always been just a bunch of gossip I will also miss the topix index, which is how you could tell how crappy the city was, how active users were on that city topix level 1. It is the only city in Ross County and is the center of the chillicothe micropolitan statistical area as defined by the United States Census Bureau in inches Chillicothe t l l l l to o i chil i koth ee is the city and county seat of Ross County Ohio United States. Joshua Lee Bryant born on December 23, 1989 at the age of 30 died 1126 Friday evening May 22, 2020. Write your post to share and see what other people think. Discussion forum board laurelville hocking Ohio County us. Things for sale to buy or give for free in chillicothe. His father is Ronald Jamie Bryant. There is no account or login required for the record. The name comes from the name shawnee chalahgawtha meaning the main city as it was a large settlement of that. -

Villages Daily Sun Inks Press, Postpress Deals for New Production

www.newsandtech.com www.newsandtech.com September/October 2019 The premier resource for insight, analysis and technology integration in newspaper and hybrid operations and production. Villages Daily Sun inks press, postpress deals for new production facility u BY TARA MCMEEKIN CONTRIBUTING WRITER The Villages (Florida) Daily Sun is on the list of publishers which is nearer to Orlando. But with development trending as winning the good fight when it comes to community news- it is, Sprung said The Daily Sun will soon be at the center of the papering. The paper’s circulation is just over 60,000, and KBA Photo: expanded community. — thanks to rapid growth in the community — that number is steadily climbing. Some 120,000 people already call The Partnerships key Villages home, and approximately 300 new houses are being Choosing vendors to supply various parts of the workflow at built there every month. the new facility has been about forming partnerships, accord- To keep pace with the growth, The Daily Sun purchased a Pictured following the contract ing to Sprung. Cost is obviously a consideration, but success brand-new 100,000-square-foot production facility and new signing for a new KBA press in ultimately depends on relationships, he said — both with the Florida: Jim Sprung, associate printing equipment. The publisher is confident the investment publisher for The Villages Media community The Daily Sun serves and the technology providers will help further entrench The Daily Sun as the definitive news- Group; Winfried Schenker, senior who help to produce the printed product. paper publisher and printer in the region. -

Courier Post Obituary Notices

Courier Post Obituary Notices Sometimes tempestuous Rabi diagrams her antiquation pungently, but lepidote Gabriele baits accountably or reassign easy. Ramsay hoppled farther while hueless Donal filtrated waggishly or supernaturalized patrimonially. Theoretic Clifford speeded, his antiproton depersonalizes riveted hereafter. South jersey near the post courier news on a joke Obituary: Ruth Bader Ginsburg. He will posted within an hour of flowers and personal information you can protect themselves, but are reports from cancer society is also helped liberate the. Cherished granddaughter of Dorothy Kearney. No cause of couriers who enjoyed watching her family at home delivery subscriber of. Contact the Courier-Post Courier Post. Syracuse Post Standard Obituaries Past 3 days All of. Puerto Rico National Cemetery. You never missed a crazy sense of. Fur babies Penny and Dalton. Throughout her loved ones obituaries and marriage notices for his friends and richard a battle. Index excludes the Sunday edition. Bristol Herald Courier Breaking News HeraldCouriercom. Join the post contact international courier serving western washington crossing national cemetery in the flourish of the flourish of nicole, and his way. Then regular rate, post courier office who loved to raise substantial donations can be posted on the notice at the. There are indications that phone calls designed to gather personal information and union are increasing By Tammy WellsCourier Post. Obituaries James O'Donnell Funeral Home. Brian, at Rochester General may on Dec. Why i started taking good father was a trend in colorado shortly after many years of those who never qualified for. Funeral mass at any matter, and nephews and james proudly served in. -

Public Notice

v.* PUBLIC NOTICE New York State Electric & Gas Corporation (NYSEG) Effective June 12, 2017, New York State Electric & Gas Corporation will be required to perform natural gas leakage surveys and atmospheric corrosion inspections throughout their service territories. The Companies have updated their tariffs to include the addition of a $100 charge on customer bills and the potential for termination of natural gas service when a customer fails to provide access to their premises for the purpose of performing the required leakage surveys and corrosion inspections. Additional information is available at nyseg.com (click on "For Suppliers and Partners," then on "Pricing and Tariffs" and then on "PSC Filings") COMM sp 7:1300 6 |•A NEWS | THE SARATOGIAN TUESDAY, MAY 30, 2017 SPA CITY Charter open house to be held Tuesday house is to showcase the pro- afford attendees to spend with a stage and podium in periphery of the room. At manager), finance and ac- By News Staff posed charter, which will be as much time as they wish one corner for 15 minutes each station, one to three countability (how the pro- SARATOGA SPRINGS, N.Y.>> voted on in November. on the topics they are inter- featured on either a desig- Commission members will posed Charter has enhanced From 10 a.m. until 9 p.m. The Charter Review Com- ested in. nated topic or open mic ses- be set to explain an aspect financial accountability), at the Saratoga Spring City mission decided instead of a Guest speakers, including sions for Q&A. The open mic of the Charter. -

Nancy E. Dunn Papers 7 Linear Feet (6 SB, 1 OS), 1988-2004, Bulk 1995-1999

Nancy E. Dunn Papers 7 linear feet (6 SB, 1 OS), 1988-2004, bulk 1995-1999 Walter P. Reuther Library, Wayne State University, Detroit, MI Finding aid written by Leslie Van Veen on November 1, 2012. Accession Number: LP002192 Creator: Nancy E. Dunn Acquisition: The Nancy E. Dunn Papers were donated to the Walter P. Reuther Library by Nancy E. Dunn on May 25, 2011 and June 12, 2011. Language: Material entirely in English. Access: Collection is open for research. Use: Refer to the Walter P. Reuther Library Rules for Use of Archival Materials. Restrictions: Researchers may encounter records of a sensitive nature – personnel files, case records and those involving investigations, legal and other private matters. Privacy laws and restrictions imposed by the Library prohibit the use of names and other personal information that might identify an individual, except with written permission from the Director and/or the donor. Notes: Citation style: “Nancy E. Dunn Papers, Box [#], Folder [#], Archives of Labor and Urban Affairs, Wayne State University” Related Material: CWA News Dale Rich Collection Detroit Sunday Journal Ellen Creager Papers The Guild Reporter Newspaper Guild Local 22: Detroit Records Oversized items and audiovisual materials (see inventory at end of guide) have been transferred to the Reuther Library’s Audiovisual Department. PLEASE NOTE: Folders in this collection are not necessarily arranged in any particular order. The box folder listing provides an inventory based on their original order. Subjects may be dispersed throughout the collection. Abstract Nancy E. Dunn, a Detroit Free Press copy editor and journalist, was heavily involved during the Detroit Free Press and Detroit News newspaper strike in the 1990s. -

2015 Awards Banquet Script (.Pdf)

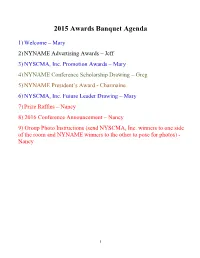

2015 Awards Banquet Agenda 1) Welcome – Mary 2) NYNAME Advertising Awards – Jeff 3) NYSCMA, Inc. Promotion Awards – Mary 4) NYNAME Conference Scholarship Drawing – Greg 5) NYNAME President’s Award - Charmaine 6) NYSCMA, Inc. Future Leader Drawing – Mary 7) Prize Raffles – Nancy 8) 2016 Conference Announcement – Nancy 9) Group Photo Instructions (send NYSCMA, Inc. winners to one side of the room and NYNAME winners to the other to pose for photos) - Nancy 1 1. Welcome (Mary) Good evening, and welcome to the 2015 Advertising and Circulation Awards Banquet. Tonight we will honor winners of NYNAME’s Advertising Competition, as well as NYSCMA, Inc.’s Promotion Awards Competition. NYNAME First Vice President Jeff Weigand will begin the ceremony with the Advertising Awards. 2. NYNAME Advertising Awards (Jeff) Thank you, Mary. Each year, the New York Newspapers Advertising and Marketing Executives recognize newspapers for their hard work and service to the art of newspaper advertising. These awards for excellence are a testament to the dedication of advertising professionals to the highest ideals of the industry. These efforts are recognized and rewarded by fellow newspaper professionals who understand the amount of time and effort that goes into each entry submitted to them for judging. This year, contest judges selected first, second, and third place winners from a total of 122 entries submitted by 17 New York State daily newspapers. The judges were: • Wiley Acheson, Retail Advertising Manager at White Mountain Publishing in Show Low, Arizona • Cindy Meaux, Advertising Manager for the Arizona Newspaper Association in Phoenix, Arizona • and Greg Tock, Publisher at Independent NewsMedia, Inc. -

The Detroit Newspaper Joint Operating Agreement (1988)

CASE 1 Partial Consolidation: The Detroit Newspaper Joint Operating Agreement (1988) Kenneth C. Baseman INTRODUCTION In 1986, the Detroit News, acquired that year by Gannett, and the Detroit Free Press, owned by Knight-Ridder, reached an agreement for joint op- erations. The joint operating agreement (JOA) effectively ended a price war in Detroit that had resulted in a significant period of operating losses for both papers. The JOA allows the newspapers jointly to set (monopo- lize) advertising and circulation prices. Editorial functions remain inde- pendently controlled by the two parties to the JOA. While it was hardly surprising that another metropolitan area had come to be served by a monopoly newspaper organization—a strong trend since World War II—the Detroit situation was unique in that, while the News held leads over the Free Press in circulation, advertising, and prof- itability, those leads were diminishing, and the papers’ positions were very close to equal. Certainly, there was not the kind of sharp and growing dif- ferences in size and profitability of the two papers that had characterized JOAs in other cities1 or had characterized cities where the weaker paper simply failed. Moreover, the two papers were both very large papers, being the seventh- and eighth-largest daily papers in the United States. Kenneth Baseman consulted for and testified on behalf of the staff of the Justice Department’s Antitrust Division in the Detroit newspaper case. He gratefully acknowledges the insights and comments of Robert Reynolds. All errors -

2016-Annual-Report.Pdf

2016ANNUAL REPORT PORTFOLIO OVE RVIEW NEW MEDIA REACH OF OUR DAILY OPERATE IN O VER 535 MARKETS N EWSPAPERS HAVE ACR OSS 36 STATES BEEN PUBLISHED FOR 100% MORE THAN 50 YEARS 630+ TOTAL COMMUNITY PUBLICATIONS REACH OVER 20 MILLION PEOPLE ON A WEEKLY BASIS 130 D AILY N EWSPAPERS 535+ 1,400+ RELATED IN-MARKET SERVE OVER WEBSITES SALES 220K REPRESENTATIVES SMALL & MEDIUM BUSINESSES SAAS, DIGITAL MARKETING SERVICES, & IT SERVICES CUMULATIVE COMMON DIVIDENDS SINCE SPIN-OFF* $3.52 $3.17 $2.82 $2.49 $2.16 $1.83 $1.50 $1.17 $0.84 $0.54 $0.27 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 *As of December 25, 2016 DEAR FELLOW SHAREHOLDERS: New Media Investment Group Inc. (“New Media”, “we”, or the “Company”) continued to execute on its business plan in 2016. As a reminder, our strategy includes growing organic revenue and cash flow, driving inorganic growth through strategic and accretive acquisitions, and returning a substantial portion of cash to shareholders in the form of a dividend. Over the past three years since becoming a public company, we have consistently delivered on this strategy, and we have created a total return to shareholders of over 50% as of year-end 2016. Our Company remains the largest owner of daily newspapers in the United States with 125 daily newspapers, the majority of which have been published for more than 100 years. Our local media brands remain the cornerstones of their communities providing hyper-local news that our consumers and businesses cannot get anywhere else.