Islay Energy Options Appraisal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Four Facts About Whisky Casks Distillers Don't Want You to Know

Malt Maniacs E-pistle #2010-08 By Oliver Klimek, Germany This article is brought to you by 'Malt Maniacs'; an international collective of more than two dozen fiercely independent malt whisky aficionados. Since 1997 we have been enjoying and discussing the pleasures of single malt whisky with like-minded whisky lovers from all over the world. In 2010 our community had members from 16 countries; The United Kingdom, Sweden, Germany, Holland, Belgium, France, Switzerland, Italy, Greece, The U.S.A., Canada, India, Japan, Taiwan, Australia & South Africa. More information on: www.maltmaniacs.org . Four Facts About Whisky Casks Distillers Don't Want You to Know "All casks are different." This a commonplace and it's one of the basic rules all aspiring maltheads and apprentice whisky anoraks will learn rather early on after they have started their journey into the whisky wonderland. When you take the step from standard distillery expressions to single cask whiskies mainly bottled by independents you will discover a seemingly endless variety of malts that sometimes can have very different characteristics, even if they are made in the same distillery. In this E-pistle I would like to highlight a few aspects of whisky casks that for some strange reason do not get very much attention, even though their consequences are rather significant. 1. Seaweed? What Seaweed? Tasting notes of Islay malts usually feature descriptors like “seaweed”, “sea spray”, “Atlantic jetty” or the likes. We all know that Islay is both caressed and mistreated by the powers of the Irish Sea, so in a way it is not a surprise that we can find maritime flavours in Islay whisky. -

Oban to Belfast

Cruising Route: Oban and west Argyll to the Antrim coast and Belfast Lough This is a beautiful cruising ground with a combination of inshore and offshore sailing amid wonderful and varied scenery. The channels among the southern Hebrides offer a number of alternative routes. From Oban, the track inside the islands leads either down the Sound of Luing to Crinan or further south, or else via Cuan Sound to Kilmelford or Craobh. In these sounds – and indeed almost everywhere on this route – the tidal stream is the first consid- eration in passage planning. The tide runs very fast in Cuan Sound and in the Dorus Mor leading to Crinan, and at a significant rate in the Sound of Luing, gradually lessening down the Sound of Jura. Loch Craignish and Ardfern offer a pleasant and scenic side-trip. There are visitors’ moorings at Craighouse and Gigha. An alternative route south from Oban is offshore, via Colonsay and the Sound of Islay, with Port Askaig providing a possible stopover. The Sound of Islay is also a tidal gate, with five knot tides. It is worth remembering that working these tides to advantage can result in very fast passages! The marina at Port Ellen is only a few miles to the west whether coming east or west of Jura. An alternative route south from Oban is offshore, via Colonsay and the Sound of Mull Oban Islay, with Port Askaig providing a possible stopover. The Sound of Islay is also a tidal Kilmelford gate, with five knot tides. It is worth remem- Craobh Ardfern bering that working these tides to advan- Oban to Colonsay 32 Colonsay tage can result in very fast passages! The Crinan Jura marina at Port Ellen is only a few miles to the west whether coming east or west of Jura. -

Rural Economy and Connectivity Committee Inquiry Into Construction and Procurement of Ferry Vessels in Scotland Submission From

RURAL ECONOMY AND CONNECTIVITY COMMITTEE INQUIRY INTO CONSTRUCTION AND PROCUREMENT OF FERRY VESSELS IN SCOTLAND SUBMISSION FROM ISLAY COMMUNITY COUNCIL FERRY COMMITTEE The Islay Community Council Ferry Committee (ICCFC) is a sub group of Islay Community Council and formally represents the ferry and related infrastructure interests of the Isle of Islay on behalf of the community and local organisations and businesses. The Committee was represented in the Transport Scotland team, set up to establish fairness and transparency during CHFS contract procurement process and has ongoing active membership of the Clyde and Argyll Ferry Stakeholder’s Group. The Committee also has a member who sits on the Calmac Community Board, an independent body established to represent communities’ strategic interests in regard to ferries and the ferry network. In September 2019, a Ferry Summit was held on Islay by the ICCFC, chaired by Cabinet Minister, Michael Russell and attended by senior representatives of Transport Scotland, Calmac, CMAL, Argyll and Bute Council, Hitrans, HIE, the Scotch Whisky Association (SWA) and their consultants Systra, local distilleries and businesses, including transport, construction and tourism and marketing, as well as Islay and Jura community interests. Its purpose was to discuss uniquely major growing capacity needs of the Islay ferry service based on forecast increases in distillery traffic and ongoing growth in tourism - and to seek solutions. Discussions are ongoing but the growth has already started and the situation is becoming increasingly urgent. The delay in completion and delivery of vessels 801 and 802 has limited the scope to find solutions, as well as having adversely impacted the island’s development and economy since mid 2018. -

National Retailers.Xlsx

THE NATIONAL / SUNDAY NATIONAL RETAILERS Store Name Address Line 1 Address Line 2 Address Line 3 Post Code M&S ABERDEEN E51 2-28 ST. NICHOLAS STREET ABERDEEN AB10 1BU WHS ST NICHOLAS E48 UNIT E5, ST. NICHOLAS CENTRE ABERDEEN AB10 1HW SAINSBURYS E55 UNIT 1 ST NICHOLAS CEN SHOPPING CENTRE ABERDEEN AB10 1HW RSMCCOLL130UNIONE53 130 UNION STREET ABERDEEN, GRAMPIAN AB10 1JJ COOP 204UNION E54 204 UNION STREET X ABERDEEN AB10 1QS SAINSBURY CONV E54 SOFA WORKSHOP 206 UNION STREET ABERDEEN AB10 1QS SAINSBURY ALF PL E54 492-494 UNION STREET ABERDEEN AB10 1TJ TESCO DYCE EXP E44 35 VICTORIA STREET ABERDEEN AB10 1UU TESCO HOLBURN ST E54 207 HOLBURN STREET ABERDEEN AB10 6BL THISTLE NEWS E54 32 HOLBURN STREET ABERDEEN AB10 6BT J&C LYNCH E54 66 BROOMHILL ROAD ABERDEEN AB10 6HT COOP GT WEST RD E46 485 GREAT WESTERN ROAD X ABERDEEN AB10 6NN TESCO GT WEST RD E46 571 GREAT WESTERN ROAD ABERDEEN AB10 6PA CJ LANG ST SWITIN E53 43 ST. SWITHIN STREET ABERDEEN AB10 6XL GARTHDEE STORE 19-25 RAMSAY CRESCENT GARTHDEE ABERDEEN AB10 7BL SAINSBURY PFS E55 GARTHDEE ROAD BRIDGE OF DEE ABERDEEN AB10 7QA ASDA BRIDGE OF DEE E55 GARTHDEE ROAD BRIDGE OF DEE ABERDEEN AB10 7QA SAINSBURY G/DEE E55 GARTHDEE ROAD BRIDGE OF DEE ABERDEEN AB10 7QA COSTCUTTER 37 UNION STREET ABERDEEN AB11 5BN RS MCCOLL 17UNION E53 17 UNION STREET ABERDEEN AB11 5BU ASDA ABERDEEN BEACH E55 UNIT 11 BEACH BOULEVARD RETAIL PARK LINKS ROAD, ABERDEEN AB11 5EJ M & S UNION SQUARE E51 UNION SQUARE 2&3 SOUTH TERRACE ABERDEEN AB11 5PF SUNNYS E55 36-40 MARKET STREET ABERDEEN AB11 5PL TESCO UNION ST E54 499-501 -

Kintour Landscape Survey Report

DUN FHINN KILDALTON, ISLAY AN ARCHAEOLOGICAL SURVEY DATA STRUCTURE REPORT May 2017 Roderick Regan Summary The survey of Dun Fhinn and its associated landscape has revealed a picture of an area extensively settled and utilised in the past dating from at least the Iron Age and very likely before. In the survey area we see settlements developing across the area from at least the 15 th century with a particular concentration of occupation on or near the terraces of the Kintour River. Without excavation or historical documentation dating these settlements is fraught with difficulty but the distinct differences between the structures at Ballore and Creagfinn likely reflect a chronological development between the pre-improvement and post-improvement settlements, the former perhaps a relatively rare well preserved survival. Ballore Kilmartin Museum Argyll, PA31 8RQ Tel: 01546 510 278 [email protected] Scottish Charity SC022744 ii Contents 1. Introduction 1 2. Archaeological and Historical Background 2 2.1 Cartographic Evidence of Settlement 4 2.2 Some Settlement History 6 2.3 A Brief History of Landholding on Islay 10 3. Dun Fhinn 12 4. Walkover Survey Results 23 5. Discussion 47 6. References 48 Appendix 1: Canmore Extracts 50 The Survey Team iii 1. Introduction This report collates the results of the survey of Dun Fhinn and a walkover survey of the surrounding landscape. The survey work was undertaken as part of the Ardtalla Landscape Project a collaborative project between Kilmartin Museum and Reading University, which forms part of the wider Islay Heritage Project. The survey area is situated on the Ardtalla Estate within Kildalton parish in the south east of Islay (Figure 1) and survey work was undertaken in early April 2017. -

Islay February 2019

Islay February 2019 February 20th : Sandwich Bay to Islay The group left the Observatory at 5 a.m. and had a straightforward run up to Gatwick with the ever-efficient Airport Connections. Our Easyjet flight to Glasgow was delayed by an hour but the flight itself was quicker than scheduled – did the pilot really put his foot on the accelerator? At Glasgow Airport we met with Peter and the mini-bus was then duly collected from a large company based about 20 minutes away in Clydeside. Peter and Ken came back to the airport to collect the group and then we were on our way in dreich conditions out of the city and north along the shores of Loch Lomond, then off through the sea lochs and mountains of Argyll. We stopped for lunch at the Loch Fyne Centre and again for a short stretch of the legs at historic Inveraray and, near the journey’s end, at Tarbert. Here we saw the first ‘good’ birds of the trip in the form of 5 Black Guillemots out in the harbour. From there it was a short journey to the ferry terminal at Kennacraig and, with night fast approaching, there were some rather nice sunset effects through the now-lifting clouds. A Red-throated Diver was swimming around the jetty as the M. V. Isle of Arran appeared from the south to take us across to Islay. A smooth crossing, landing at Port Askaig, and then across the dark island to the hotel at Port Charlotte for a decent night’s sleep in this very comfortable hotel set overlooking the outer reaches of Loch Indaal. -

Sound of Gigha Proposed Special Protection Area (Pspa) NO

Sound of Gigha Proposed Special Protection Area (pSPA) NO. UK9020318 SPA Site Selection Document: Summary of the scientific case for site selection Document version control Version and Amendments made and author Issued to date and date Version 1 Formal advice submitted to Marine Scotland on Marine draft SPA. Nigel Buxton & Greg Mudge. Scotland 10/07/14 Version 2 Updated to reflect change in site status from draft Marine to proposed and addition of SPA reference Scotland number in preparation for possible formal 30/06/15 consultation. Shona Glen, Tim Walsh & Emma Philip Version 3 Creation of new site selection document. Emma Susie Whiting Philip 17/05/16 Version 4 Document updated to address requirements of Greg revised format agreed by Marine Scotland. Mudge Kate Thompson & Emma Philip 17/06/16 Version 5 Quality assured Emma Greg Mudge Philip 17/6/16 Version 6 Final draft for approval Andrew Emma Philip Bachell 22/06/16 Version 7 Final version for submission to Marine Scotland Marine Scotland, 24/06/16 Contents 1. Introduction .......................................................................................................... 1 2. Site summary ........................................................................................................ 2 3. Bird survey information ....................................................................................... 5 4. Assessment against the UK SPA Selection Guidelines .................................... 6 5. Site status and boundary ................................................................................. -

Product Specification We Believe That an Islay Whisky

WE BELIEVE AN “ISLAY” THIS 10-YEAR-OLD PORT A WHISKY MADE BY PEOPLE WHISKY SHOULD LIVE AND CHARLOTTE HAS BEEN NOT SOFTWARE; A WHISKY “ WE BELIEVE THAT BREATHE THE FRESH SALT CONCEIVED, DISTILLED, WATCHED OVER EVERY TANG OF ISLAY AIR, ALL ITS MATURED AND BOTTLED DAY OF ITS MATURING AN ISLAY WHISKY LIFE. THIS IS NOT A SPIRIT ON ISLAY ALONE. LIFE BY THOSE WHO MADE DISTILLED ON THE ISLAND WE ARE A YOUNG TEAM IT; A WHISKY BORN OF SHOULD BE AS ISLAY AND IMMEDIATELY SHIPPED WITH DEEP-ROOTED A COMMUNITY WITH A OFF TO THE MAINLAND VALUES, AND AN AMBITION VISION AND A MISSION TO AS POSSIBLE TO MATURE IN SOME TO MAKE THE ULTIMATE KICK START A SINGLE MALT UNDISCLOSED WAREHOUSE. “ISLAY” ISLAY WHISKY. WHISKY REVOLUTION, THIS - SIMON COUGHLIN ” PORT CHARLOTTE 10-YEAR- OLD IS WHO WE ARE. THIS IS WHERE WE’RE FROM. PRODUCT SPECIFICATION WHISKY TYPE: BARLEY PROVENANCE: BOTTLING: CHEAT SHEET: HEAVILY PEATED 100% SCOTTISH BARLEY BOTTLED ONSITE WITH THIS FIRST PERMANENT RELEASE ISLAY SINGLE MALT FROM INVERNESSHIRE ISLAY SPRING WATER, OF PORT CHARLOTTE 10 YEAR OLD SCOTCH WHISKY REGION NON CHILL FILTERED & REPLACES THE MULTI VINTAGE CUVEE COLOURING FREE SCOTTISH BARLEY. AS THE FLAGSHIP PHENOL LEVEL: MATURATION PROFILE: PORT CHARLOTTE IT SHOWCASES THE 40 PARTS PER MILLION • 65% 1ST FILL AMERICAN LIQUID COLOUR: SMOKY, BARBECUE QUALITIES OF OUR WHISKEY CASKS PRIMROSE TO CITRINE SPIRIT. A NEW BESPOKE GREEN GLASS VINTAGE/AGE: • 10% 2ND FILL AMERICAN BOTTLE IS A NOD TO THE HEAVILY- 10 AGED YEARS WHISKEY CASKS TASTE DESCRIPTOR: PEATED MALTS OF “ISLAY”, BUT UNLIKE • 25% 2ND FILL FRENCH BARBECUE SMOKINESS, MANY IS CONCEIVED, DISTILLED, ALCOHOL STRENGTH: WINE CASKS RICH AND SPICY WITH MATURED AND BOTTLED ON ISLAY. -

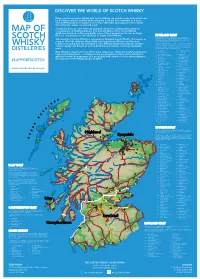

2019 Scotch Whisky

©2019 scotch whisky association DISCOVER THE WORLD OF SCOTCH WHISKY Many countries produce whisky, but Scotch Whisky can only be made in Scotland and by definition must be distilled and matured in Scotland for a minimum of 3 years. Scotch Whisky has been made for more than 500 years and uses just a few natural raw materials - water, cereals and yeast. Scotland is home to over 130 malt and grain distilleries, making it the greatest MAP OF concentration of whisky producers in the world. Many of the Scotch Whisky distilleries featured on this map bottle some of their production for sale as Single Malt (i.e. the product of one distillery) or Single Grain Whisky. HIGHLAND MALT The Highland region is geographically the largest Scotch Whisky SCOTCH producing region. The rugged landscape, changeable climate and, in The majority of Scotch Whisky is consumed as Blended Scotch Whisky. This means as some cases, coastal locations are reflected in the character of its many as 60 of the different Single Malt and Single Grain Whiskies are blended whiskies, which embrace wide variations. As a group, Highland whiskies are rounded, robust and dry in character together, ensuring that the individual Scotch Whiskies harmonise with one another with a hint of smokiness/peatiness. Those near the sea carry a salty WHISKY and the quality and flavour of each individual blend remains consistent down the tang; in the far north the whiskies are notably heathery and slightly spicy in character; while in the more sheltered east and middle of the DISTILLERIES years. region, the whiskies have a more fruity character. -

Public Document Pack Argyll and Bute Council Comhairle Earra Ghaidheal Agus Bhoid

Public Document Pack Argyll and Bute Council Comhairle Earra Ghaidheal agus Bhoid Customer Services Executive Director: Douglas Hendry Kilmory, Lochgilphead, PA31 8RT Tel: 01546 602127 Fax: 01546 604435 DX 599700 LOCHGILPHEAD 13 December 2013 SUPPLEMENTARY PACK 1 PLANNING, PROTECTIVE SERVICES AND LICENSING COMMITTEE - COUNCIL CHAMBERS, KILMORY, LOCHGILPHEAD on WEDNESDAY, 18 DECEMBER 2013 at 10:30 AM I enclose herewith items 6 and 13 which were marked “to follow” on the Agenda for the above meeting along with a supplementary report for item 8. ITEMS TO FOLLOW AND SUPPLEMENTARY REPORT 6. MR JAMES PAUL DALY AND ANDREENA DALY: ERECTION OF DWELLINGHOUSE, FORMATION OF CAR PARKING AND SITING OF STEEL CONTAINER UNIT (PARTIALLY RETROSPECTIVE): 3 KYLE VIEW, KILCREGGAN, HELENSBURGH (REF: 13/02045/PP) Report by Head of Planning and Regulatory Services (Pages 1 - 26) 8. MR SEUMAS MACARTHUR: ERECTION OF FLAG POLE (RETROSPECTIVE): FORESHORE, OPPOSITE 7 SHORE STREET, PORTNAHAVEN, ISLE OF ISLAY (REF: 13/02075/PP) Report by Head of Planning and Regulatory Services (Pages 27 - 28) 13. 13/02270/S36: CONSULTATION FROM MARINE SCOTLAND RELATIVE TO PROPOSED WEST ISLAY TIDAL ENERGY PARK Report by Head of Planning and Regulatory Services (Pages 29 - 48) PLANNING, PROTECTIVE SERVICES AND LICENSING COMMITTEE Councillor David Kinniburgh (Chair) Councillor Gordon Blair Councillor Rory Colville Councillor Robin Currie Councillor Mary-Jean Devon Councillor George Freeman Councillor Alistair MacDougall Councillor Robert Graham MacIntyre Councillor Donald MacMillan Councillor -

Islay Whisky

The Land of Whisky A visitor guide to one of Scotland’s five whisky regions. Islay Whisky The practice of distilling whisky No two are the same; each has has been lovingly perfected its own proud heritage, unique throughout Scotland for centuries setting and its own way of doing and began as a way of turning things that has evolved and been rain-soaked barley into a drinkable refined over time. Paying a visit to spirit, using the fresh water a distillery lets you discover more from Scotland’s crystal-clear about the environment and the springs, streams and burns. people who shape the taste of the Scotch whisky you enjoy. So, when To this day, distilleries across the you’re sitting back and relaxing country continue the tradition with a dram of our most famous of using pure spring water from export at the end of your distillery the same sources that have been tour, you’ll be appreciating the used for centuries. essence of Scotland as it swirls in your glass. From the source of the water and the shape of the still to the wood Home to the greatest concentration of the cask used to mature the of distilleries in the world, spirit, there are many factors Scotland is divided into five that make Scotch whisky so distinct whisky regions. These wonderfully different and varied are Islay, Speyside, Highland, from distillery to distillery. Lowland and Campbeltown. Find out more information about whisky, how it’s made, what foods to pair it with and more: www.visitscotland.com/whisky For more information on travelling in Scotland: www.visitscotland.com/travel Search and book accommodation: www.visitscotland.com/accommodation Islay BUNNAHABHAIN Islay is one of many small islands barley grown by local crofters. -

Boisdale of Mayfair Whisky Bible

BOISDALE Boisdale of Mayfair Whisky Bible 1 All spirits are sold in measures of 25ml or multiples thereof. All prices listed are for a large measure of 50ml. Should you require a 25ml measure, please ask. All whiskies are subject to availability. 1. Springbank 10yr 19. Old Pulteney 17yr 37. Ardbeg Corryvreckan 55. Glenfiddich 21yr 2. Highland Park 12yr 20. Glendronach 12yr 38. Ardbeg 10yr 56. Glenfiddich 18yr 3. Bowmore 12yr 21. Whyte & Mackay 40yr 39. Lagavulin 16yr 57. Glenfiddich 15yr Solera 4. Oban 14yr 22. Royal Lochnagar S. Res. 40. Laphroaig Quarter Cask 58. Glenfarclas 10yr 5. Balvenie 21yr PortWood 23. Talisker 10yr 41. Laphroaig 10yr 59. Macallan 18yr 6. Glenmorangie Signet 24. Springbank 15yr 42. Ardbeg Uigeadail 60. Highland Park 18yr 7. Suntory Yamazaki 18yr 25. Ailsa Bay 43. Tomintoul 16yr 61. Glenfarclas 25yr 8. Cragganmore 12yr 26. Caol Ila 12yr 44. Glenesk 1984 62. Macallan 10yr Sherry Oak 9. Brora 25yr 2008 27. Port Charlotte 2008 45. Glenmorangie 25yr QC 63. Glendronach 12yr 10. Clynelish 14yr 28. Balvenie 15yr 46. Strathmill 12yr 64. Balvenie 12yr DoubleWood 11. Isle of Jura 10yr 29. Glenmorangie 18yr 47. Glenlivet 21yr 65. Aberlour 18yr 12. Tobermory 15yr 30. Macallan 12yr Sherry 48. Macallan 12yr Fine Oak 66. Auchentoshan 3 Wood 13. Glenfiddich 26yr Excellence Cask 49. Glenfiddich 12yr 67. Dalmore King Alexander III 14. Dalwhinnie 15yr 31. Bruichladdie Classic Laddie 50. Monkey Shoulder 68. Auchentoshan 12yr 15. Glenmorangie Original 32. Chivas Regal 18yr 51. Glenlivet 25yr 69. Benrinnes 23yr 2 16. Bunnahabhain 12yr 33. Chivas Regal 25yr 52. Glenlivet 12yr 70.