Nbcuniversal Media, LLC (Exact Name of Registrant As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pr-Dvd-Holdings-As-Of-September-18

CALL # LOCATION TITLE AUTHOR BINGE BOX COMEDIES prmnd Comedies binge box (includes Airplane! --Ferris Bueller's Day Off --The First Wives Club --Happy Gilmore)[videorecording] / Princeton Public Library. BINGE BOX CONCERTS AND MUSICIANSprmnd Concerts and musicians binge box (Includes Brad Paisley: Life Amplified Live Tour, Live from WV --Close to You: Remembering the Carpenters --John Sebastian Presents Folk Rewind: My Music --Roy Orbison and Friends: Black and White Night)[videorecording] / Princeton Public Library. BINGE BOX MUSICALS prmnd Musicals binge box (includes Mamma Mia! --Moulin Rouge --Rodgers and Hammerstein's Cinderella [DVD] --West Side Story) [videorecording] / Princeton Public Library. BINGE BOX ROMANTIC COMEDIESprmnd Romantic comedies binge box (includes Hitch --P.S. I Love You --The Wedding Date --While You Were Sleeping)[videorecording] / Princeton Public Library. DVD 001.942 ALI DISC 1-3 prmdv Aliens, abductions & extraordinary sightings [videorecording]. DVD 001.942 BES prmdv Best of ancient aliens [videorecording] / A&E Television Networks History executive producer, Kevin Burns. DVD 004.09 CRE prmdv The creation of the computer [videorecording] / executive producer, Bob Jaffe written and produced by Donald Sellers created by Bruce Nash History channel executive producers, Charlie Maday, Gerald W. Abrams Jaffe Productions Hearst Entertainment Television in association with the History Channel. DVD 133.3 UNE DISC 1-2 prmdv The unexplained [videorecording] / produced by Towers Productions, Inc. for A&E Network executive producer, Michael Cascio. DVD 158.2 WEL prmdv We'll meet again [videorecording] / producers, Simon Harries [and three others] director, Ashok Prasad [and five others]. DVD 158.2 WEL prmdv We'll meet again. Season 2 [videorecording] / director, Luc Tremoulet producer, Page Shepherd. -

TV Channel Distribution in Europe: Table of Contents

TV Channel Distribution in Europe: Table of Contents This report covers 238 international channels/networks across 152 major operators in 34 EMEA countries. From the total, 67 channels (28%) transmit in high definition (HD). The report shows the reader which international channels are carried by which operator – and which tier or package the channel appears on. The report allows for easy comparison between operators, revealing the gaps and showing the different tiers on different operators that a channel appears on. Published in September 2012, this 168-page electronically-delivered report comes in two parts: A 128-page PDF giving an executive summary, comparison tables and country-by-country detail. A 40-page excel workbook allowing you to manipulate the data between countries and by channel. Countries and operators covered: Country Operator Albania Digitalb DTT; Digitalb Satellite; Tring TV DTT; Tring TV Satellite Austria A1/Telekom Austria; Austriasat; Liwest; Salzburg; UPC; Sky Belgium Belgacom; Numericable; Telenet; VOO; Telesat; TV Vlaanderen Bulgaria Blizoo; Bulsatcom; Satellite BG; Vivacom Croatia Bnet Cable; Bnet Satellite Total TV; Digi TV; Max TV/T-HT Czech Rep CS Link; Digi TV; freeSAT (formerly UPC Direct); O2; Skylink; UPC Cable Denmark Boxer; Canal Digital; Stofa; TDC; Viasat; You See Estonia Elion nutitv; Starman; ZUUMtv; Viasat Finland Canal Digital; DNA Welho; Elisa; Plus TV; Sonera; Viasat Satellite France Bouygues Telecom; CanalSat; Numericable; Orange DSL & fiber; SFR; TNT Sat Germany Deutsche Telekom; HD+; Kabel -

DISCOVER NEW WORLDS with SUNRISE TV TV Channel List for Printing

DISCOVER NEW WORLDS WITH SUNRISE TV TV channel list for printing Need assistance? Hotline Mon.- Fri., 10:00 a.m.–10:00 p.m. Sat. - Sun. 10:00 a.m.–10:00 p.m. 0800 707 707 Hotline from abroad (free with Sunrise Mobile) +41 58 777 01 01 Sunrise Shops Sunrise Shops Sunrise Communications AG Thurgauerstrasse 101B / PO box 8050 Zürich 03 | 2021 Last updated English Welcome to Sunrise TV This overview will help you find your favourite channels quickly and easily. The table of contents on page 4 of this PDF document shows you which pages of the document are relevant to you – depending on which of the Sunrise TV packages (TV start, TV comfort, and TV neo) and which additional premium packages you have subscribed to. You can click in the table of contents to go to the pages with the desired station lists – sorted by station name or alphabetically – or you can print off the pages that are relevant to you. 2 How to print off these instructions Key If you have opened this PDF document with Adobe Acrobat: Comeback TV lets you watch TV shows up to seven days after they were broadcast (30 hours with TV start). ComeBack TV also enables Go to Acrobat Reader’s symbol list and click on the menu you to restart, pause, fast forward, and rewind programmes. commands “File > Print”. If you have opened the PDF document through your HD is short for High Definition and denotes high-resolution TV and Internet browser (Chrome, Firefox, Edge, Safari...): video. Go to the symbol list or to the top of the window (varies by browser) and click on the print icon or the menu commands Get the new Sunrise TV app and have Sunrise TV by your side at all “File > Print” respectively. -

Pearl CES 2020 FINAL

NEWS For Immediate Release MORE BROADCAST MARKETS, MORE RECEIVER OPTIONS, MORE INNOVATIONS WILL DRIVE NEXT STEPS IN NEXTGEN TV DEPLOYMENT Majority of American Viewers Expected to Have Available NEXTGEN TV Broadcasts by Fall 2021 Washington, D.C. – January 7, 2021 – On the heels of the initial rollout of NEXTGEN TV broadcasting that has now reached more than 20 cities and 80 TV stations, America’s broadcasters are now planning a push this year that will initiate next-generation ATSC 3.0 service in nearly 20 more cities By the end of the summer. Pearl TV, a Business group comprised of owners of more than 750 Broadcast stations, and the Phoenix Model Market partners announced the plans today in the lead-up to the virtual 2021 CES®. “Today, almost 20 percent of America’s TV viewers already have access to NEXTGEN TV broadcasts, and the television broadcasting industry is moving aggressively to expand the reach of NEXTGEN TV in a herculean, collaborative effort to reach over half of American TV viewers by this fall. Broadcasters are working like never before to launch new NEXTGEN TV channels that offer better picture and more expansive audio options for viewers. As the consumer technology industry Begins to diversify its choices with more models and more affordaBle products for viewers, broadcasters will continue to push ahead with plans to initiate NEXTGEN TV service in key markets throughout the country. We’re also doing our part to help to educate consumers about the benefits of NEXTGEN TV,” said Pearl TV Managing Director Anne Schelle. “The Future of Television Has Arrived” Pearl’s promotional effort highlights the capabilities of NEXTGEN TV powered by the groundbreaking ATSC 3.0 standard. -

Appendix a Stations Transitioning on June 12

APPENDIX A STATIONS TRANSITIONING ON JUNE 12 DMA CITY ST NETWORK CALLSIGN LICENSEE 1 ABILENE-SWEETWATER SWEETWATER TX ABC/CW (D KTXS-TV BLUESTONE LICENSE HOLDINGS INC. 2 ALBANY GA ALBANY GA NBC WALB WALB LICENSE SUBSIDIARY, LLC 3 ALBANY GA ALBANY GA FOX WFXL BARRINGTON ALBANY LICENSE LLC 4 ALBANY-SCHENECTADY-TROY ADAMS MA ABC WCDC-TV YOUNG BROADCASTING OF ALBANY, INC. 5 ALBANY-SCHENECTADY-TROY ALBANY NY NBC WNYT WNYT-TV, LLC 6 ALBANY-SCHENECTADY-TROY ALBANY NY ABC WTEN YOUNG BROADCASTING OF ALBANY, INC. 7 ALBANY-SCHENECTADY-TROY ALBANY NY FOX WXXA-TV NEWPORT TELEVISION LICENSE LLC 8 ALBANY-SCHENECTADY-TROY PITTSFIELD MA MYTV WNYA VENTURE TECHNOLOGIES GROUP, LLC 9 ALBANY-SCHENECTADY-TROY SCHENECTADY NY CW WCWN FREEDOM BROADCASTING OF NEW YORK LICENSEE, L.L.C. 10 ALBANY-SCHENECTADY-TROY SCHENECTADY NY CBS WRGB FREEDOM BROADCASTING OF NEW YORK LICENSEE, L.L.C. 11 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM CW KASY-TV ACME TELEVISION LICENSES OF NEW MEXICO, LLC 12 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM UNIVISION KLUZ-TV ENTRAVISION HOLDINGS, LLC 13 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM PBS KNME-TV REGENTS OF THE UNIV. OF NM & BD.OF EDUC.OF CITY OF ALBUQ.,NM 14 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM ABC KOAT-TV KOAT HEARST-ARGYLE TELEVISION, INC. 15 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM NBC KOB-TV KOB-TV, LLC 16 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM CBS KRQE LIN OF NEW MEXICO, LLC 17 ALBUQUERQUE-SANTA FE ALBUQUERQUE NM TELEFUTURKTFQ-TV TELEFUTURA ALBUQUERQUE LLC 18 ALBUQUERQUE-SANTA FE CARLSBAD NM ABC KOCT KOAT HEARST-ARGYLE TELEVISION, INC. -

Federal Register/Vol. 85, No. 103/Thursday, May 28, 2020

32256 Federal Register / Vol. 85, No. 103 / Thursday, May 28, 2020 / Proposed Rules FEDERAL COMMUNICATIONS closes-headquarters-open-window-and- presentation of data or arguments COMMISSION changes-hand-delivery-policy. already reflected in the presenter’s 7. During the time the Commission’s written comments, memoranda, or other 47 CFR Part 1 building is closed to the general public filings in the proceeding, the presenter [MD Docket Nos. 19–105; MD Docket Nos. and until further notice, if more than may provide citations to such data or 20–105; FCC 20–64; FRS 16780] one docket or rulemaking number arguments in his or her prior comments, appears in the caption of a proceeding, memoranda, or other filings (specifying Assessment and Collection of paper filers need not submit two the relevant page and/or paragraph Regulatory Fees for Fiscal Year 2020. additional copies for each additional numbers where such data or arguments docket or rulemaking number; an can be found) in lieu of summarizing AGENCY: Federal Communications original and one copy are sufficient. them in the memorandum. Documents Commission. For detailed instructions for shown or given to Commission staff ACTION: Notice of proposed rulemaking. submitting comments and additional during ex parte meetings are deemed to be written ex parte presentations and SUMMARY: In this document, the Federal information on the rulemaking process, must be filed consistent with section Communications Commission see the SUPPLEMENTARY INFORMATION 1.1206(b) of the Commission’s rules. In (Commission) seeks comment on several section of this document. proceedings governed by section 1.49(f) proposals that will impact FY 2020 FOR FURTHER INFORMATION CONTACT: of the Commission’s rules or for which regulatory fees. -

Case M.8861 - COMCAST / SKY

EUROPEAN COMMISSION DG Competition Case M.8861 - COMCAST / SKY Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 15/06/2018 In electronic form on the EUR-Lex website under document number 32018M8861 EUROPEAN COMMISSION Brussels, 15.6.2018 C(2018) 3923 final In the published version of this decision, some information has been omitted pursuant to Article 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and PUBLIC VERSION other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a general description. To the notifying party Subject: Case M.8861 - Comcast/Sky Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/20041 and Article 57 of the Agreement on the European Economic Area2 Dear Sir or Madam, (1) On 7 May 2018, the European Commission received notification of a proposed concentration pursuant to Article 4 of the Merger Regulation by which Comcast Corporation ("Comcast" or the "Notifying Party", United States) proposes to acquire within the meaning of Article 3(1)(b) of the Merger Regulation sole control of the whole of Sky plc ("Sky", United Kingdom and the "Proposed Transaction"). Comcast and Sky are collectively referred to as the "Parties".3 1. THE OPERATION (2) Comcast is a US listed global media, technology and entertainment company, with two primary businesses: Comcast Cable and NBCUniversal ("NBCU"). Comcast is present in Europe almost entirely through NBCU, which is active in Europe in: (i) production, sales and distribution of film and television content; (ii) wholesale supply of TV channels and on-demand services; (iii) CNBC, a business news service, as well as NBC News; (iv) the provision of television content to end users through NBCU’s video on demand service; (v) the licensing of its 1 OJ L 24, 29.1.2004, p. -

12 Pica PT. 1

Five Tips For A Stress-Free Holiday Shopping Season (NAPSA)—The holidays can be could need or want, think about a hectic time of year. Between hol- making a dinner reservation to iday parties, shopping for the spend time with one another. Remembering The Holidays right gifts and spending time with Experiential gifts are a great way (NAPSA)—Like a whirlwind, Five Easy Steps To A New Countertop your family, the balancing act of to catch up with the people you the holiday season flies by in a sea (NAPSA)—Choosing a counter- getting everything done within love and show them you’re think- of chaos filled with family, friends, your budget or forgetting a gift ing about them. Spend time with top doesn’t have to be a daunting food, shopping and gifts. Before task. can be stressful. However, with friends over manicures and pedi- people know it, the holidays are the proper time management, cures, book a family vacation for To begin, you may want to visit over until the following year. Fam- a dealer to look at all the options money and budgeting tools, and a some quality time with your loved ilies are left asking themselves little creativity ones or plan a weekend of com- available to you. There may be where the time went and how the several types of materials that can sprinkled on top, gift munity service with friends and holidays were spent. As time givers can enjoy the family. give you the look you want at vari- passes, many people find it hard ous prices and with different holidays and stay Don’t forget your manners. -

APPENDIX a – Initial List of Stations Eligible for Analog Nightlight Program

Federal Communications Commission FCC 08-281 APPENDIX A – Initial List of Stations Eligible for Analog Nightlight Program Market Facility ID Call sign City ST Analog Digital Anlg Ch. Post Pre Status of Analog Transition Transition DTV Ch. DTV Ch. (*) Anchorage, AK 804 KAKM Anchorage AK PBS PBS 7 8 Anchorage, AK 13815 KIMO Anchorage AK ABC ABC 13 12 Anchorage, AK 10173 KTUU-TV Anchorage AK NBC NBC 2 10 Anchorage, AK 4983 KYUK-TV Bethel AK 4 3 Fairbanks, AK 13813 KATN Fairbanks AK ABC ABC 2 18 Fairbanks, AK 20015 KJNP-TV North Pole AK 4 20 Fairbanks, AK 49621 KTVF Fairbanks AK NBC NBC 11 26 Fairbanks, AK 69315 KUAC-TV Fairbanks AK 9 9 24 Juneau, AK 8651 KTOO-TV Juneau AK PBS PBS 3 10 Juneau, AK 60520 KUBD Ketchikan AK CBS CBS 4 13 Birmingham, AL 71325 WDBB Bessemer AL 17 18 Dothan, AL 43846 WDHN Dothan AL ABC ABC 18 21 Huntsville-Decatur-Florence, AL 57292 WAAY-TV Huntsville AL ABC ABC 31 32 Montgomery, AL 714 WDIQ Dozier AL PBS PBS 2 10 Ft. Smith-Fayetteville-Springdale-Rogers, AR 66469 KFSM-TV Fort Smith AR CBS CBS 5 18 Ft. Smith-Fayetteville-Springdale-Rogers, AR 60354 KHOG-TV Fayetteville AR ABC ABC 29 15 Little Rock-Pine Bluff, AR 33440 KARK-TV Little Rock AR NBC NBC 4 32 Little Rock-Pine Bluff, AR 2770 KETS Little Rock AR PBS PBS 2 7 Terminating 1/3/09 Little Rock-Pine Bluff, AR 11951 KLRT-TV Little Rock AR Fox Fox 16 30 Little Rock-Pine Bluff, AR 37005 KWBF Little Rock AR 42 44 Reduced 10/31/08 Phoenix, AZ 41223 KPHO-TV Phoenix AZ CBS CBS 5 17 Phoenix, AZ 40993 KTVK Phoenix AZ 3 24 Phoenix, AZ 68886 KUTP Phoenix AZ 45 26 Tucson, -

Comcast Channel Lineup

• Basi.c Service , $ 14.99 Equipment and Options (prices per month) The minimum level of service available and is required before you HOTV Equipment Charge~ ... .., ...............•.........$ 7.00 can subscribe to additional services, HO OVR Service .................•........................$ 15.95 SO DVR Service ..................................•........$ 8.95 Starter Cable , $ 55.99 Digital/Analog Converter . .. .....................•........$ 3.20 Includes Starter Cable channels plus OCT & Remote. Analog Converter for Basic Service Only ......•............ " .$ 1.00 Digital/Analog Remote Control . .•.......•.. ,... .$ 0.20 Digital Preferred ,,,,, $ 16.95 This package can be added to Starter Cable and includes the Installation and Service' channels in Digital Classic. Home Installation (Wired) ......., .......•........ , .$ 23.99 Home InstaiJation (Unwired) ............................•... .$ 33.99 Digital Preferred Plus Package , $ 107.99 Additional Connection at Time of Imliallnstall , $ 12.99 Includes the channels in Starter Cable. Digital Classic, and HBO Additional Connection Requiring Separate Trip ..........•.....$ 20.99 and STARZl. Move Outlet ........................................•. , ..$ 16.99 Upgrade of Services _.......•.. , ..$ 14.99 Digital Premier Package , ,.$ 127,99 Downgrade of Services ,... .. , ..........•.........•....$ 10.95 Includes the channels in Starter Cable, Digital Classic, Sports Change of Service or Equipment Activation ........•......•.....$ 1.99 Entertainment Tier, HBO, Showtime, Cinemax and Starzl. Connect VCR at Time of InitiallnstaiJ $ 5.99 Connect VCR Requiring Separate Trip .................•......$ 12.99 Digital Premium Services. ,,,,, $ 19.99 Hourly Service Charge. .........,.. $ 30.99 Premium services can be added to any Digital package, Select Service Call Trip Charge ........ $ 27.20 from HBO, Showtime, Cinemax, The Movie Channel, STARZI Administrative Fee for Delinquent Accounts at 30 Days $ 5.95 or E(1core. Administrative Fee for Delinquent Accounts at 60 Days ,$ 5.95 Additional Late Fee Every 30 Days After. -

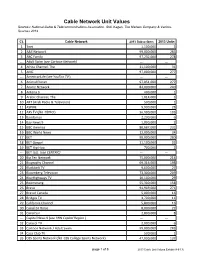

Cable Network Unit Values Sources: National Cable & Telecommunications Association, SNL Kagan, the Nielsen Company & Various Sources 2013

Cable Network Unit Values Sources: National Cable & Telecommunications Association, SNL Kagan, The Nielsen Company & Various Sources 2013 Ct. Cable Network 2013 Subscribers 2013 Units 1 3net 1,100,000 3 2 A&E Network 99,000,000 283 3 ABC Family 97,232,000 278 --- Adult Swim (see Cartoon Network) --- --- 4 Africa Channel, The 11,100,000 31 5 AMC 97,000,000 277 --- AmericanLife (see YouToo TV ) --- --- 6 Animal Planet 97,051,000 277 7 Anime Network 84,000,000 240 8 Antena 3 400,000 1 9 Arabic Channel, The 1,014,000 3 10 ART (Arab Radio & Television) 500,000 1 11 ASPIRE 9,900,000 28 12 AXS TV (fka HDNet) 36,900,000 105 13 Bandamax 2,200,000 6 14 Bay News 9 1,000,000 2 15 BBC America 80,687,000 231 16 BBC World News 12,000,000 34 17 BET 98,000,000 280 18 BET Gospel 11,100,000 32 19 BET Hip Hop 700,000 2 --- BET Jazz (see CENTRIC) --- --- 20 Big Ten Network 75,000,000 214 21 Biography Channel 69,316,000 198 22 Blackbelt TV 9,600,000 27 23 Bloomberg Television 73,300,000 209 24 BlueHighways TV 10,100,000 29 25 Boomerang 55,300,000 158 26 Bravo 94,969,000 271 27 Bravo! Canada 5,800,000 16 28 Bridges TV 3,700,000 11 29 California Channel 5,800,000 16 30 Canal 24 Horas 8,000,000 22 31 Canal Sur 2,800,000 8 --- Capital News 9 (see YNN Capital Region ) --- --- 32 Caracol TV 2,000,000 6 33 Cartoon Network / Adult Swim 99,000,000 283 34 Casa Club TV 500,000 1 35 CBS Sports Network (fka CBS College Sports Network) 47,900,000 137 page 1 of 8 2013 Cable Unit Values Exhibit (4-9-13) Ct. -

Downloading of Movies, Television Shows and Other Video Programming, Some of Which Charge a Nominal Or No Fee for Access

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO Commission file number 001-32871 COMCAST CORPORATION (Exact name of registrant as specified in its charter) PENNSYLVANIA 27-0000798 (State or other jurisdiction of (I.R.S. Employer Identification No.) incorporation or organization) One Comcast Center, Philadelphia, PA 19103-2838 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (215) 286-1700 SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: Title of Each Class Name of Each Exchange on which Registered Class A Common Stock, $0.01 par value NASDAQ Global Select Market Class A Special Common Stock, $0.01 par value NASDAQ Global Select Market 2.0% Exchangeable Subordinated Debentures due 2029 New York Stock Exchange 5.50% Notes due 2029 New York Stock Exchange 6.625% Notes due 2056 New York Stock Exchange 7.00% Notes due 2055 New York Stock Exchange 8.375% Guaranteed Notes due 2013 New York Stock Exchange 9.455% Guaranteed Notes due 2022 New York Stock Exchange SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.