Newfield Exploration Company

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Newfield Exploration Company 2016 Annual Report

ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING FOCUSING • OPTIMIZING • ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING ADVANCING • EXECUTING • DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING DELIVERING • FOCUSING • OPTIMIZING • ADVANCING • EXECUTING -

Gas Production for OCS Operators

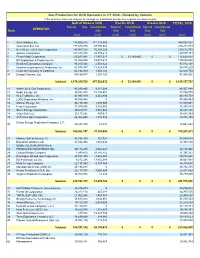

Gas Production for OCS Operators in CY 2006 - Ranked by Volume (The volumes here are subject to change as additional production reports are processed) Gulf of Mexico OCS Pacific OCS Alaska OCS TOTAL OCS Natural Gas Casinghead Natural Casinghead Natural Casinghead OPERATOR Rank Gas Gas Gas Gas Gas (mcf) (mcf) (mcf) (mcf) (mcf) (mcf) (mcf) 1 Shell Offshore Inc. 188,505,018 181,319,506 369,824,524 2 Chevron U.S.A. Inc. 177,525,875 57,755,858 235,281,733 3 Kerr-McGee Oil & Gas Corporation 148,907,524 70,205,226 219,112,750 4 Apache Corporation 161,837,488 22,739,613 184,577,101 5 Exxon Mobil Corporation 125,637,461 17,857,017 0 33,189,450 0 0 176,683,928 6 BP Exploration & Production Inc. 81,806,055 89,027,613 170,833,668 7 Newfield Exploration Company 95,305,826 2,568,322 97,874,148 8 Dominion Exploration & Production, Inc 81,514,387 13,323,833 94,838,220 9 Union Oil Company of California 63,186,059 1,494,725 64,680,784 10 Energy Partners, Ltd. 50,159,807 1,291,120 51,450,927 Subtotal 1,174,385,500 457,582,833 0 33,189,450 0 0 1,665,157,783 11 Walter Oil & Gas Corporation 45,242,496 3,115,388 48,357,884 12 Noble Energy, Inc. 35,591,474 12,134,601 47,726,075 13 W & T Offshore, Inc. 41,937,859 4,261,894 46,199,753 14 LLOG Exploration Offshore, Inc. -

Ranking Operator by Gas 1947

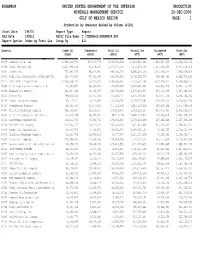

PDRANKOP UNITED STATES DEPARTMENT OF THE INTERIOR PRODUCTION MINERALS MANAGEMENT SERVICE 22-DEC-2000 GULF OF MEXICO REGION PAGE: 1 Production by Operator Ranked by Volume (4120) Start Date : 194701 Report Type : Report End Date : 199512 ASCII File Name: C:\TIMSWork\PDRANKOP.DAT Report Option: Order by Total Gas Group By : All Operator Crude Oil Condensate Total Oil Natural Gas Casinghead Total Gas (BBLS) (BBLS) (BBLS) (MCF) (MCF) (MCF) 00078 Chevron U.S.A. Inc. 1,926,333,769 137,016,779 2,063,350,548 11,063,925,241 2,504,607,294 13,568,532,535 00689 Shell Offshore Inc. 1,417,893,524 85,274,236 1,503,167,760 7,372,318,798 2,025,230,206 9,397,549,004 00001 Conoco Inc. 797,691,267 90,614,940 888,306,207 6,665,540,300 1,270,468,340 7,936,008,640 00540 MOBIL OIL EXPLORATION & PRODUCING SOUT 323,970,684 67,931,345 391,902,029 6,452,624,776 498,954,383 6,951,579,159 00276 Exxon Mobil Corporation 1,093,558,792 56,026,660 1,149,585,452 5,223,562,198 1,323,290,927 6,546,853,125 00985 Union Exploration Partners, Ltd. 172,994,887 68,962,600 241,957,487 5,693,340,954 248,803,779 5,942,144,733 00081 Tenneco Oil Company 213,224,062 48,335,567 261,559,629 5,587,612,854 279,449,349 5,867,062,203 00040 Texaco Inc. 189,506,674 33,936,036 223,442,710 4,576,194,031 442,571,025 5,018,765,056 00114 Amoco Production Company 97,147,101 34,421,651 131,568,752 3,175,779,982 235,024,436 3,410,804,418 00167 PennzEnergy Company 191,565,059 26,157,422 217,722,481 2,812,024,858 262,674,308 3,074,699,166 00967 Atlantic Richfield Company 242,193,417 18,221,055 260,414,472 -

Hydraulic Fracturing Case Studies Technical Workshop Participant Bios

BIOGRAPHY Technical Workshop on Case Studies to Assess Potential Impacts of Hydraulic Fracturing on Drinking Water Resources Greg Appleton, Corporate Energy Technology Group, Devon Energy Greg Appleton works in the Corporate Engineering Technology Group for Devon Energy. He is currently working to assist the operating divisions with well stimulation and completion best practices while evaluating new technology for strategic use within Devon. Additional responsibilities include support for corporate communications technical initiatives and oversight of Devon funded University research and consortium efforts in the United States. Appleton has worked in both geology and engineering roles within the Devon midcontinent, new ventures and corporate divisions. Prior to joining Devon in 2008, Appleton worked at Halliburton as a field engineer for oil/gas well stimulation, cementing, tools and testing. He served as District Engineer for the southeast New Mexico work area and then the global training manager for stimulation, tools and TCP engineers. At the onset of his career, Appleton worked for three years for Exxon as an exploration and operations geologist in Brazil, West Africa, South China Sea and the Permian Basin. Appleton is a licensed Geologist in the state of Texas and also is an active member in the American Association of Petroleum Geologists and the Society of Petroleum Engineers. He attained a MS degree in Petroleum Geology in 1997 from the University of Oklahoma. Sina Arjmand, Graduate Assistant, University of Pittsburgh Sina Arjmand is currently a PhD student in the Water Resources Engineering program at the University of Pittsburgh. He is a hydrogeologist with expertise in the fate and transport of contaminants in groundwater, with over six years of research experience in hydrology and water resources engineering. -

Newfield Exploration Company Annual Report

NEWFIELD EXPLORATION COMPANY2003ANNUAL REPORT NEWFIELD EXPLORATION COMPANY Year-Ended December 31, 2003 2002 2001 2000 1999 (In thousands, except per share data) Oil and gas revenues$ 1,016,986 $ 626,835 $ 714,052 $ 479,876 $ 265,603 Income from operations382,788 167,657 184,851 201,026 54,768 Net income199,489 73,847 118,954 132,349 33,204 Basic earnings per common share$ 3.67 $ 1.64 $ 2.69 $ 3.13 $ 0.81 Diluted earnings per common share3.57 1.61 2.56 2.93 0.79 Weighted average number of shares outstanding (basic)54,347 45,096 44,258 42,333 41,194 Weighted average number of shares outstanding (diluted)56,744 49,589 48,894 47,228 42,294 Capital expenditures$ 646,748 $ 888,482 $ 846,451 $ 365,253 $ 202,409 Net cash provided by continuing operating activities 659,167 383,257 495,623 289,384 178,916 Net cash used in continuing investing activities(614,708) (501,816) (754,540) (339,303) (205,971) Net cash provided by (used in) continuing financing activities $ (85,352) 137,030 273,127 15,933 67,758 Total assets2,733,089 $2,315,753 $1,663,371 $1,023,250 $ 781,561 Long-term debt643,459 709,615 428,631 133,711 124,679 Convertible preferred securities– 143,750 143,750 143,750 143,750 and reserve data Stockholders’ equity1,368,578 1,009,231 709,978 519,455 375,018 summary financial Oil and condensate reserves (MBbls)37,774 34,037 30,959 22,551 19,637 Gas reserves (MMcf)1,090,140 977,115 718,312 519,723 440,173 Total proved reserves (MMcfe)1,316,786 1,181,337 904,066 655,029 557,992 • We significantly expanded our Gulf Coast operations. -

Corporate List

Corporate Name Change & Merger Index Current As Of: March 12, 2020 Issuing Original or Previous Company Name Current Company Name Date of Memo State Office 08/08/2018 1986 STEA Ltd Partnership I Program Acquisition Company 05/21/2001 WY 1986 STEA Ltd Partnership II Program Acquisition Company 05/21/2001 WY 1987-STEA Ltd Partnership Program Acquisition Company 05/21/2001 WY 1987-II STEA Ltd Partnership Program Acquisition Company 05/21/2001 WY 1987III STEA Ltd Partnership Program Acquisition Company 05/21/2001 WY 1987-IV STEA Ltd Partnership Program Acquisition Company 05/21/2001 WY 1987-VI STEA Ltd Partnership Program Acquisition Company 05/21/2001 WY 1988-I TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 1988III TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 1988IV TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 1988-V TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 1988-VI TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 1988VII TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 1989III TEAI Ltd Partnership Program Acquisition Company 05/21/2001 WY 3TECH Energy Corp PXP Gulf 07/17/2003 NM 44 Canyon, L.L.C. Pure Resources, LP 06/08/2006 NM A 1 Corporate Name Change & Merger Index Current As Of: March 12, 2020 Issuing Original or Previous Company Name Current Company Name Date of Memo State Office AA Development Corporation AA Energy Corp 02/11/1985 WY Amended Decision-Additional Lease 10/29/1985 WY AA Energy Corp AMR Energy Corp 02/11/1985 WY Amended Decision-Additional Lease 10/29/1985 WY Aberdeen American Petro Aberdeen Petro (USA) Inc 04/10/1990 WY 05/14/2013 CO Abraxas Operating, LLC Abraxax Petroleum Corporation 08/26/2013 WY Abraxas Production Co Abraxas Petroleum Corp 11/30/1999 WY ABO Petroleum Corporation EOG A Resources Inc. -

Leasing Activities Information

Leasing Activities Information U.S. Department of the Interior Minerals Management Service MMS Gulf of Mexico OCS Region LEASE SALE 205 CGOM STATISTICS As of February 15, 2008 107 Tracts in Phase 1 - Bids Deemed Acceptable 723 Total Tracts + 596 Tracts in Phase 2 - Bids Deemed Acceptable 703 Tracts - Bids Deemed Acceptable 703 Total Tracts - Bids Deemed Acceptable - 18 Tracts - Bids Rejected - 2 Tracts - Bids Forfeited 0 Tracts Remaining Bids on the following tracts were deemed acceptable on , February 14, 2008, in Phase 2 of the GOM Central Sale 205. The tracts are listed in GOM Company Number order. PHASE 2 ACCEPTANCES BY SUBMITTER 00059 Hess Corporation G31684 Garden Banks 987 G31852 Keathley Canyon 20 00078 Chevron U.S.A. Inc. G31644 Garden Banks 674 G31662 Garden Banks 807 G31668 Garden Banks 862 G31669 Garden Banks 863 G31676 Garden Banks 907 G31681 Garden Banks 953 G31682 Garden Banks 954 G31686 Garden Banks 996 G31688 Garden Banks 998 G31854 Keathley Canyon 22 G31857 Keathley Canyon 64 00689 Shell Offshore Inc. G31677 Garden Banks 910 00724 Marathon Oil Company G31733 Green Canyon 492 01207 Petrobras America Inc. G31679 Garden Banks 951 G31680 Garden Banks 952 G31776 Green Canyon 1001 G31777 Green Canyon 1002 02079 Nexen Petroleum Offshore U.S.A. Inc. G31865 Keathley Canyon 110 G31884 Keathley Canyon 302 02169 Hydro Gulf of Mexico, L.L.C. G31891 Keathley Canyon 368 02421 Devon Energy Production Company, L.P G31886 Keathley Canyon 325 02481 BP Exploration & Production Inc. G31631 Garden Banks 587 G31632 Garden Banks 588 G31687 Garden Banks 997 02748 Statoil Gulf of Mexico LLC G31635 Garden Banks 630 G31636 Garden Banks 631 02873 Cobalt International Energy, L.P. -

Gulf of Mexico Produced Water Bioaccumulation Study Executive

Gulf of Mexico Produced Water Bioaccumulation Study Executive Summaries April 1997 (Reformatted for Microsoft Word in May 2009) Prepared For: Prepared By: Offshore Operators Committee Continental Shelf Associates, Inc. P.O. Box 50751 759 Parkway Street New Orleans, Louisiana 70150 Jupiter, Florida 33477 ACKNOWLEDGEMENTS WE WOULD LIKE TO ACKNOWLEDGE THE OOC BIOACCUMULATION STUDY CO-SPONSORS FOR THEIR SUPPORT OF THE PROJECT: AEDC (USA), Inc. Agip Petroleum Company, Inc. Amerada Hess Corporation American Exploration Company Amoco Production Company Anadarko Petroleum Company ANR Production Company Apache Corporation (includes Aquila Energy Resources) Ashland Exploration, Inc. Ashlawn Energy, Inc. Aviara Energy Corporation (formerly Columbia Gas Development Corporation) BHP Petroleum (Americas) Incorporated Blue Dolphin Exploration Company (includes Ivory Production Company) BP Exploration British-Borneo Exploration, Inc. Chevron USA Prod. Company CNG Producing Company, Inc. Coastal Oil & Gas Corporation Cockrell Oil Corporation Conn Energy, Inc. Conoco, Inc. CXY Energy, Inc. Elf Exploration Inc. Enron Oil & Gas Company Enserch Exploration Company (includes DALEN Resources Oil & Gas and EP Operating Ltd. Partnership) Exxon Co., USA Fina Oil & Chemical Flores & Rucks, Inc. Forcenergy Gas Exploration, Inc. Forest Oil Corporation Freeport-McMoran Oil & Gas Company Greenhill Petroleum Corporation Gulfstar Energy, Inc. Gulfstream Resources, Inc. Hall-Houston Oil Company Houston Exploration Company Howell Petroleum Company Kerr-McGee Corporation i Louisiana Land & Exploration Company Marathon Oil Company Matrix Oil & Gas Company Meridian Oil Mesa Operating Ltd. Partnership MidCon Offshore Corporation Mitchell Energy Corporation Mobil E & P Company Murphy Exploration & Production Company NCX Company, Inc. Newfield Exploration Company Nippon Oil Exploration USA (NOEX) Norcen Explorer, Inc. Oryx Energy Company Oxy USA, Inc. O.E.D.C. -

US Oil and Gas Reserves and Production Study 2019 Table of Contents

US oil and gas reserves and production study 2019 Table of contents Study overview 1 Study highlights 2 Capital expenditures 4 Revenues and results of operations 5 Oil reserves 7 Gas reserves 9 Performance measures Proved reserve acquisition costs, finding and development 10 costs and reserve replacement costs Production replacement rates 11 Production costs 13 Company statistics 14 Peer groups 26 Appendix 27 Contacts 29 Study overview The US oil and gas reserves and production study is a compilation and analysis of oil and gas reserve disclosure information as reported by publicly traded companies in their annual reports filed with the United States Securities and Exchange Commission (SEC). This report presents the US exploration and production (E&P) results for the five-year period from 2014 through 2018 for the 50 largest companies based on 2018 end-of-year US oil and gas reserve estimates. The study companies cover approximately 42% of the US combined oil and gas production for 2018 (44% for 2017). Activities related to acquisitions have also been reflected as described in the appendix. Study companies Due to the significance of the oil and gas reserves attributable to the study companies, the results of these companies are generally representative of the US E&P industry as a whole. Total US production is fast approaching a leading global position, giving this study’s findings an impact beyond the US borders, but it should be noted that results for these companies and for the E&P industry as a whole may be significantly different in other regions of the world. -

Oil and Gas in the Gulf of Mexico a North American Perspective

Center for Energy Studies Oil and Gas in the Gulf of Mexico A North American Perspective David E. Dismukes Center for Energy Studies Louisiana State University Heads of Mission, EnerNet Conference Houston, TX March 20, 2007 Importance of the Gulf of Mexico to the US Center for Energy Studies The Gulf of Mexico region accounts for: • Approximately 30 percent of total U.S. crude oil production; • Roughly 20 percent of total natural gas production; • Over $6 billion in federal royalties and fees; • Over 45 percent of total U.S. petroleum refining capacity and 62 percent of the capacity east of the Rockies; • 60 percent of all U.S. crude oil imports; and • 43 percent of the Strategic Petroleum Reserve (“SPR”) storage capacity. 2 Center for Energy Studies Nature of the Energy Business in the Gulf of Mexico 3 Nature of the Energy Business Oil and Gas Production Center for Energy Studies • Currently: 89 rigs operating in the Gulf of Mexico. • In 2005, 468,000 Bbls and 3.2 Tcf of natural gas were produced in the Gulf of Mexico. • Employs 160,000 workers in the Gulf Coast region. • Contributes about $73 billion to Gulf Coast states’ GDP. Note: Gulf Coast states include Louisiana, Texas, Mississippi and Alabama Source: Bureau of Economic Analysis, US Department of Commerce; Energy Information Administration, US Department of Energy; and Baker Hughes. 4 Nature of the Energy Business Pipelines Center for Energy Studies Pipelines can transport a variety of raw, unprocessed hydrocarbons, or finished (refined) products that include natural gas, natural gas liquids, crude oil, gasoline, diesel, among others. -

Africa Lakes: Regional Offshore Exploration and Production Profile

Africa Lakes: Regional Offshore Exploration and Production Profile The countries in the Africa Lakes regional grouping Total Oil Production (onshore/offshore): include Malawi and Uganda, and focus on some of No production the major lakes with hydrocarbon activity. Total Gas Production Specifically, hydrocarbon exploration has mainly (onshore/offshore): taken place in Lake Malawi and Lake Albert in Malawi and Uganda, respectively. Lake Victoria is No production another lake of interest, but due to its low level of exploration activity, environmental factors were only considered. Lake Malawi is an African Great Lake in the East African Rift* between Malawi, Mozambique, and Tanzania. It is the ninth largest lake in the world. The Malawian government has divided Malawi’s oil exploration area into six blocks: “three cover the lake and the rest are on land in the north and south of the country along the Rift Valley1.” The prospecting licenses were awarded to South- African based SacOil (Block 1), UK-based Surestream Petroleum (Blocks 2 and 3), the United Arab Emirates’ RAK Gas (Blocks 4 and 5), and Indonesian-based Pacific Oil & Gas (Block 6). Lake Malawi has been listed as a World Heritage site, and civil societies have expressed their concerns about the effects of oil extraction on the lake. Lake Albert is another one of the African Great Lakes, and is the seventh-largest lake in Africa. It is situated between Uganda and the Democratic Republic of Congo. In 2010, London-based multinational oil and gas exploration company Tullow Oil began to accelerate development of the Lake Albert rift basin by purchasing Heritage Oil and Gas Limited’s (a Bailiwick of Jersey company, headquartered off the coast of Normandy, France) ownership of blocks EA-1 and EA- 3A. -

Grown up Suite 2020 NEWFIELD EXPLORATION COMPANY / 2005 ANNUAL REPORT Houston, Texas 77060 281-847-6000

NEWFIELD EXPLORATION COMPANY 363 North Sam Houston Parkway East All Grown Up Suite 2020 NEWFIELD EXPLORATION COMPANY / 2005 ANNUAL REPORT Houston, Texas 77060 281-847-6000 www.newfield.com NEWFIELD EXPLORATION COMPANY / 2005 ANNUAL REPORT COMPANY NEWFIELD EXPLORATION ‘05 Newfield Exploration Company 363 N. Sam Houston Parkway E., Suite 2020 Houston, Texas 77060 Ph: 281-847-6000 Fax: 281-405-4242 Newfield Exploration Mid-Continent Inc. ‘04 110 West 7th, Suite 1300 Tulsa, Oklahoma 74119 Ph: 918-582-2690 Fax: 918-582-2757 Newfield Rocky Mountains Inc. 1401 Seventeenth Street, Suite 1000 Denver, Colorado 80202 Ph: 303-893-0102 ‘03 Fax: 303-893-0103 Newfield Petroleum UK Limited First Floor 21 Dartmouth Street London SW1H 9BP Ph: + 44 (0) 20 7304 7012 Fax: + 44 (0) 20 7304 7094 ‘02 Newfield Sarawak Malaysia Inc. Newfield Peninsula Malaysia Inc. Level 53, Tower 2, Petronas Twin Towers Kuala Lumpur City Centre 50088 Kuala Lumpur Ph: + (603) 2382 4148 Fax: + (603) 2382 6003 Newfield China LDC Fortune Plaza ‘01 No.7 Dongsanhuan Zhong Road, Suite 3501B Chaoyang District, Beijing 100020, P.R. China Ph: + 8613511008725 CORPORATE INFORMATION Executive Officers Directors DAVID A. TRICE (57) PHILIP J. BURGUIERES (***) (62) Chairman, President and Chief Executive Officer Chief Executive Officer JUANITA F. ROMANS (**) (***) (55) EMC Holdings, LLC Senior Vice President of Memorial DAVID F. SCHAIBLE (45) Hermann Healthcare System and Executive Vice President – Vice Chairman Chief Executive Officer of Memorial Hermann Operations and Acquisitions Houston Texans Hospital ELLIOTT PEW (51) PAMELA J. GARDNER (**) (***) (49) DAVID F. SCHAIBLE (45) Executive Vice President – Exploration President, Business Operations of Executive Vice President – Houston McLane Company TERRY W.