Q1 2021 Investor Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Notice of Annual Meeting and Special Meeting of Unitholders and Management Information Circular

Notice of Annual Meeting and Special Meeting of Unitholders and Management Information Circular March 24, 2017 BOYD GROUP INCOME FUND NOTICE OF ANNUAL MEETING AND SPECIAL MEETING OF UNITHOLDERS TO BE HELD MAY 12, 2017 NOTICE IS HEREBY GIVEN that the Annual Meeting and Special Meeting of the Unitholders of Boyd Group Income Fund (the “Fund”) will be held at the Hilton Winnipeg Airport Suites Hotel, 1800 Wellington Avenue, Winnipeg, Manitoba on Friday, May 12 at 1:00 p.m. (local time) for the following purposes: 1. to receive the consolidated financial statements of the Fund for the year ended December 31, 2016 and the Auditor’s Report thereon; 2. to appoint Trustees for the ensuing year; 3. to elect nominees of the Fund to serve as Directors of The Boyd Group Inc. and Boyd Group Holdings Inc.; 4. to appoint auditors for the ensuing year and authorize the Board of Trustees to fix their remuneration; 5. to pass a special resolution, confirming an amendment to the Trust Declaration, adding Section 12.12, Nominations of Trustees 6. to transact such other business as may properly come before the Meeting, or any adjournment thereof. Unitholders who are unable to attend the meeting in person are requested to complete, date and sign the enclosed form of Proxy and return it, in the envelope provided, to the Secretary-Treasurer of the Fund, c/o Computershare Trust Company of Canada, 8th Floor, 100 University Avenue, Toronto, Ontario, M5J 2Y1, Attention: Proxy Department or via Phone: 1-866-732-8683, or by Internet voting at www.investorvote.com, at least 24 hours prior to the Meeting or any adjournment thereof, failing which the Proxy will be invalid. -

Fpbonds Corporate FM.Vp

FP Bonds — Corporate 2018 1 Introduction FP Bonds – Corporate 2018, the third edition to be published by Grey House Publishing Canada, lists outstanding publicly and privately held debt securities – together with their features and provisions – issued by Canadian incorporated companies, as well as brand new introductory material related to the corporate bond market. Separate tables list convertible, exchangeable, retractable and extendible debt issues. An additional table lists outstanding asset-backed securities. Corporate debt issues outstanding as at May 8, 2018 have been included. An important part of investing in the debt market is determining the quality of a debt issue. Credit ratings are forward looking measures which assess an entity’s ability to make timely payments of interest and principal. As such, a credit rating combines both quantitative and qualitative analysis. FP Bonds – Corporate 2018 includes ratings supplied by Dominion Bond Rating Service(DBRS). The DBRS ratings, dated May 8, 2018, are presented in two tables, in addition to being shown with each issue. The first table lists issues by rating, from lowest to highest. Generally, a DBRS rating of BBB is considered to be investment grade and anything below that could be considered as non-investment grade or high-yield debt. As well, unrated securities are also considered to be high-yield if its spread to a comparable Government of Canada issue is substantially higher than the spread between investment-grade corporate bonds and Government of Canada issues. A second table -

Investor Presentation

AUTOCANADA INVESTOR PRESENTATION SCOTIABANK CONFERENCE SEPTEMBER 15, 2020 Forward-Looking Statements Certain information contained in this presentation looks forward in time and deals with other than historical or current facts for AutoCanada Inc. (the “Company”). The use of any of the words “could”, “expect”, “believe”, “will”, “projected”, “estimated”, “anticipated” and similar expressions and statements relating to matters that are not historical facts are intended to identify forward- looking information and are based on the Company’s current belief or assumptions as to the outcome and timing of such future events. In particular, forward-looking statements in this presentation include, but are not limited to, references to the future operations and performance of the Company or its segments. Although the Company believes that the expectations reflected by the forward-looking statements in this presentation are reasonable, these statements have been based on assumptions and factors concerning future events that may prove to be inaccurate. Actual future results may differ materially. The Company’s annual information form for the year ended December 31, 2019 and other documents filed with securities regulatory authorities (accessible through the SEDAR website www.sedar.com) describe the risks, material assumptions and other factors that could influence actual results and which are incorporated herein by reference. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise. 2 WHO WE ARE AutoCanada Overview A Leading North American Multi-Location Automobile Dealership Group At a Glance1 • One of Canada’s largest multi-location automobile dealership groups with 3,700 49 13 Franchises in Canada Franchises in Illinois, U.S. -

Live Canadian Bank and Supplier Connections NAME TYPE

Live Canadian Bank and Supplier Connections NAME TYPE ENHANCED Alterna Savings Banks and Credit Cards Amazon.ca Rewards Visa from Chase Banks and Credit Cards American Express (Canada) Banks and Credit Cards YES American Express Merchant Services (EUR) Banks and Credit Cards Assiniboine Credit Union Banks and Credit Cards ATB Financial (Business) Banks and Credit Cards YES ATB Financial (Personal) Banks and Credit Cards BMO Debit Card Banks and Credit Cards YES BMO Nesbitt Burns Banks and Credit Cards BMO Online Banking for Business Banks and Credit Cards Canadian Tire Options MasterCard Banks and Credit Cards Canadian Western Bank Banks and Credit Cards YES Capital One Mastercard (Canada) Banks and Credit Cards CHASE Bank Canada Banks and Credit Cards CIBC Banks and Credit Cards YES CIBC Wood Gundy Banks and Credit Cards Coast Capital Savings Banks and Credit Cards YES Costco Capital One Credit Card Banks and Credit Cards CUETS: Choice Rewards Mastercard Banks and Credit Cards Desjardins Business Banks and Credit Cards Desjardins VISA Banks and Credit Cards Envision Financial Banks and Credit Cards First National Financial Banks and Credit Cards Ford Credit (Canada) Banks and Credit Cards HBC Credit Card Banks and Credit Cards Home Depot Consumer Credit Card (Canada) Banks and Credit Cards Home Depot Revolving Commercial Charge Card (Canada) Banks and Credit Cards HSBC Bank Canada Banks and Credit Cards HSBC MasterCard Banks and Credit Cards Interior Savings Credit Union Banks and Credit Cards Island Savings Banks and Credit Cards MBNA -

Frequently Asked Questions Regarding the Chicago Jr Blackhawks Brick Team

Frequently Asked Questions regarding the Chicago Jr Blackhawks Brick team What is the Brick tournament? For those not familiar with the Brick tournament, it is one of the most prestigious hockey events available for players at the 10 & Under age level. The Chicago Jr Blackhawks Brick team is the only sanctioned program (for the past 11 years) that can bring an Illinois team to the actual Brick Tournament in Edmonton, Alberta. The Brick is offered for the 2011 age group in the summer of 2021. Select teams from all over the North American continent attend this renowned summer tournament which offers many young promising hockey players and their parents a first opportunity to compete in a very elite international environment. Not only does the tournament provide great hockey, but also a number of off-ice activities including the famous Brick Tournament Beach Party at the Water Park and skills competition which makes the tournament a special fun-filled hockey experience for the entire family. We have sent a Chicago Jr. Blackhawks team for the past nine years and it is easy to see why the Brick is so highly regarded. There is no stone left unturned by the tournament staff and the production of games is at an NHL level. From the introduction of the teams to warm up music to the playing of the anthems to the post game drinks and food in the locker rooms to the media credentialing to the play by play call of every game to the team photographers to the gift bag that each player receives. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Leduc Common NWC of Highway 2 & 50 Avenue Leduc, AB

LEDUC COMMON NWC OF HIGHWAY 2 & 50 AVENUE LEDUC, AB RETAIL SPACE FOR LEASE IMMEDIATE POSSESSION 1,200 - 6,728 SQ. FT. 50 AVENUE HIGHWAY 2 61,570 VPD (2011) NOW OPEN! DETAILS FEATURES • Area: 1,200 sq. ft. - 5,835 sq. ft. • Join this premier shopping destination anchored • Net Asking Rate: $30.00/sq. ft./year by Wal-Mart, Canadian Tire, and Rona • Additional Rent: $7.94/sq. ft./year (2015) • Many national tenants are present in Leduc • Parking: 6.86/1,000 sq. ft. Common: Tim Hortons, Dairy Queen, Staples, • Occupancy: Immediate possession Sportmart, Shell, TD, Canadian Western Bank, • Leduc Population: 27,241 people (2014) The Brick, Penningtons, Reitmans, Mark’s Work • Primary Trade Area: 86,000 people Wearhouse, Warehouse One, Sport Chek, • County of Leduc Average Household Income: $108,000 Winners and Michaels For more information, please contact: CUSHMAN & WAKEFIELD EDMONTON BRETT KILLIPS BRANDON ROSSER Suite 2700, TD Tower Partner Sales Associate 10088 102 Avenue (780) 702 2948 (780) 701 3286 Edmonton AB T5J 2Z1 [email protected] [email protected] www.cwedm.com No warranty or representation, expressed or implied, is made as to the accuracy of the information contained herein, and same is submitted subject to errors, omissions, change of price, rental or other conditions, withdrawal without notice, and to any specific listing condition, imposed by our principals. LEDUC COMMON 1,200 - 6,728 SQ. FT. Retail Space for Lease AVAILABLE 25.26% LEDUCY COMMON 349 CARS 349 269 CARS269 R A1-2 ± 6,500 ± S.F. ± 72,290 ± S.F. ± 18,000 ± S.F. -

Autocanada Inc

AUTOCANADA INC. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS For the period ended March 31, 2012 As of May 8, 2012 READER ADVISORIES The Management’s Discussion & Analysis (“MD&A”) was prepared as of May 8, 2012 to assist readers in understanding AutoCanada Inc.’s (the “Company” or “AutoCanada”) consolidated financial performance for the three month period ended March 31, 2012 and significant trends that may affect AutoCanada’s future performance. The following discussion and analysis should be read in conjunction with the unaudited consolidated financial statements and accompanying notes (the “Interim Consolidated Financial Statements”) of AutoCanada for the three months ended March 31, 2012, the consolidated financial statements and accompanying notes of the Company for the year ended December 31, 2011 and management’s discussion and analysis for the year ended December 31, 2011. Results are reported in Canadian dollars. Certain dollar amounts have been rounded to the nearest thousand dollars. References to notes are to the Notes of the Consolidated Financial Statements of the Company unless otherwise stated. To provide more meaningful information, this MD&A typically refers to the operating results for the three-month period ended March 31, 2012 of the Company, and compares these to the operating results of the Company for the three-month period March 31, 2011. This MD&A contains forward-looking statements. Please see the section “FORWARD-LOOKING STATEMENTS” for a discussion of the risks, uncertainties and assumptions used to develop our forward-looking information. This MD&A also makes reference to certain non-GAAP measures to assist users in assessing AutoCanada’s performance. -

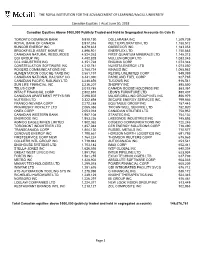

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2018 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts (in Cdn $) TORONTO DOMINION BANK 9,910,190 DOLLARAMA INC 1,209,739 ROYAL BANK OF CANADA 8,917,316 KELT EXPLORATION LTD 1,188,512 SUNCOR ENERGY INC 6,879,833 QUEBECOR INC 1,183,053 BROOKFIELD ASSET MGMT INC 4,896,921 ENERFLEX LTD 1,150,883 CANADIAN NATURAL RESOURCES 4,524,263 FIRST QUANTUM MINERALS LTD 1,145,213 CGI GROUP INC 4,482,828 MULLEN GROUP LTD 1,083,045 CCL INDUSTRIES INC 4,351,728 ENCANA CORP 1,073,348 CONSTELLATION SOFTWARE INC 4,212,781 NUVISTA ENERGY LTD 1,073,050 ROGERS COMMUNICATIONS INC 3,788,734 KINAXIS INC 1,065,983 ALIMENTATION COUCHE-TARD INC 3,581,197 RECIPE UNLIMITED CORP 949,389 CANADIAN NATIONAL RAILWAY CO 3,441,390 PARKLAND FUEL CORP 927,785 CANADIAN PACIFIC RAILWAY LTD 3,240,856 TUCOWS INC 916,541 SUN LIFE FINANCIAL INC 3,236,207 SHOPIFY INC 895,850 TELUS CORP 3,013,785 CANADA GOOSE HOLDINGS INC 883,361 INTACT FINANCIAL CORP 2,802,815 LEON'S FURNITURE LTD 880,407 CANADIAN APARTMENT PPTYS REI 2,498,502 MAJOR DRILLING GROUP INTL INC 856,979 NUTRIEN LTD 2,322,898 SECURE ENERGY SERVICES INC 799,566 FRANCO-NEVADA CORP 2,272,288 EQUITABLE GROUP INC 787,443 PRAIRIESKY ROYALTY LTD 2,065,386 TRICAN WELL SERVICE LTD 782,920 ONEX CORP 2,053,018 CANADIAN UTILITIES LTD 758,952 CANADIAN WESTERN BANK 1,987,108 STANTEC INC 754,132 ENBRIDGE INC 1,953,226 LASSONDE INDUSTRIES INC 745,893 AGNICO EAGLE MINES LIMITED 1,902,362 COGECO COMMUNICATIONS -

Management Information & Proxy Circular

(formerly reporting as Boyd Group Income Fund) Notice of Annual Meeting and Special Meeting of Shareholders and Management Information Circular May 25, 2020 BOYD GROUP SERVICES INC. (formerly reporting as Boyd Group Income Fund) NOTICE OF ANNUAL MEETING AND SPECIAL MEETING OF SHAREHOLDERS TO BE HELD JUNE 29, 2020 NOTICE IS HEREBY GIVEN that the annual meeting and special meeting (“Meeting”) of the holders of common shares (“Shareholders”) of Boyd Group Services Inc. (“BGSI”) will be held at BGSI’s head office at 1745 Ellice Avenue, Unit C1, Winnipeg, Manitoba on Monday, June 29, 2020 at 1:00 p.m. (local time) for the following purposes: 1. to receive the consolidated financial statements of Boyd Group Income Fund for the year ended December 31, 2019 and the Auditor’s Report thereon; 2. to fix the number of Directors at nine; 3. to appoint Directors for the ensuing year; 4. to appoint auditors for the ensuing year and authorize the Board of Directors to fix their remuneration; 5. to vote on an advisory resolution on BGSI’s approach to executive compensation; 6. to approve a special resolution to amend BGSI’s articles to allow the Directors to appoint one or more additional directors, who shall hold office for a term expiring not later than the close of the next annual meeting, and not to exceed one third of the number of directors elected at the previous annual meeting of shareholders, as described in the Information Circular; and 7. to transact such other business as may properly come before the Meeting, or any adjournment thereof. -

Chase Gardiner Cinematographer / Storyteller 403.990.1087 • [email protected] •

Chase Gardiner cinematographer / storyteller 403.990.1087 • [email protected] • www.cgcinematography.com Feature Length Director / DP Bone Hunters Cinematographer Documentary Director: Ryan Northcott John 316 Cinematographer Narrative Film Director: Jarvis Greiner Thousand Yard Stare Cinematographer Narrative Film Director: Aaron Kurmey Award Winning Michelles Hope Cinematographer Documentary Director: Jillian Lee True Fiction A Camera Operator Narrative Film DP: Ian Lister Award Nominated There by Grace A Camera Operator Narrative Film DP: Brad Allen Award Winning Everfall Gaffer Narrative Film DP: Aaron Bernakavitch Award Nominated And the Oscar Goes To Gaffer Foreign Film Director: Salim Amd Gone by Dawn Cinematographer Narrative Film Director: Shaun Donnelly Breaking Spirits Cinematographer Narrative Film Director: Shaun Donnelly Rock Paper Dice Enter 1st AC / 2nd Unit Cinematographer Narrative Film DP: Adam Lee Award Winning Commercial (selection) Agency AMA - April Fools Cinematographer Social Media / Pre Roll Freshwater Creative Award Winning AMA - Travel (various) Cinematographer Social Media / Pre Roll Freshwater Creative Award Winning Pepsi - Oilers 2018 Camera Operator / Local Producer Broadcast BBDO Under Armour - Storm the Centre Camera Operator Social Media / Pre Roll Unified Content Tim Hortons - Family Feel Good Producer / Director Social Media / Pre Roll Chase Media West Edmonton Mall Cinematographer Broadcast / Various GruvPixs Edmonton Airport Cinematographer Various Releases GruvPixs City of Edmonton - City -

Awards of Excellence in Corporate Reporting JUDGES’ BOOK 2016

Awards of Excellence in Corporate Reporting JUDGES’ BOOK 2016 A proud heritage, a bright future We celebrate a milestone Presentation is also changing dramatically. this year–the 65th anniversary Organizations today augment printed materials of the Awards of Excellence with electronic formats that cover a spectrum of in Corporate Reporting social media platforms and include mobile apps (CR Awards). and dynamic interactive analytical tools. A lot has changed in corporate reporting in that time and the Raising the bar CPA Canada is proud to recognize the companies program has evolved to help reporters stay ahead and Crown organizations that rise to meet these of those changes. When it launched in 1951 as ever-evolving challenges. Spotlighting excellence the Annual Report Awards, the competition was sets a clear path for others. Yesterday’s innovations open to public companies only. Judges reviewed become today’s table stakes. The bar moves higher. hard copy annual reports that contained very little information beyond the fi nancials. Some Fostering continual improvement is a primary 40 years later, Management Discussion and objective of the CR Awards. All entrants receive Analysis was added. In the 1990s the program feedback from the judges that shows how they further expanded to include environmental measured up against benchmarks and provides reporting and corporate governance disclosures. advice for improvement. The Electronic Disclosure category was included in 2001. We opened the competition to Crown organizations in 2007. Moving forward with strength Looking back on 65 years gives important context about where corporate reporting has been. The Increasingly complex needs require landscape will continue to change and strong sophisticated reporting Canadian companies will continue to respond in kind.